John C Bogle made a lot of us focus on investment cost.

While we do not know the range of returns that we will get, the cost is fixed. If the cost of investment is high, the cost will also compound like your profits, but to your investment detriment.

So we should try our best to minimize the cost.

The younger Singapore investor may buy into this message better because some of them read more. This is from my observation.

What I observe is that they will seek out investments with an eye on cost. But often, what I noticed is that they place the sales costs, commission and recurring asset under management access fee as the highest priority when evaluating their investment strategy.

Giving them sound advice is a bit tough.

On the one hand, there are many organisations out there trying to tell you they deliver so much value that it is worth it to pay the high fees and commission. In my opinion, many of them overrate the value delivered and are just trying to justify high commissions and fees.

Yet a young person, they should also consider other important aspects of the securities they invest in or the strategies used.

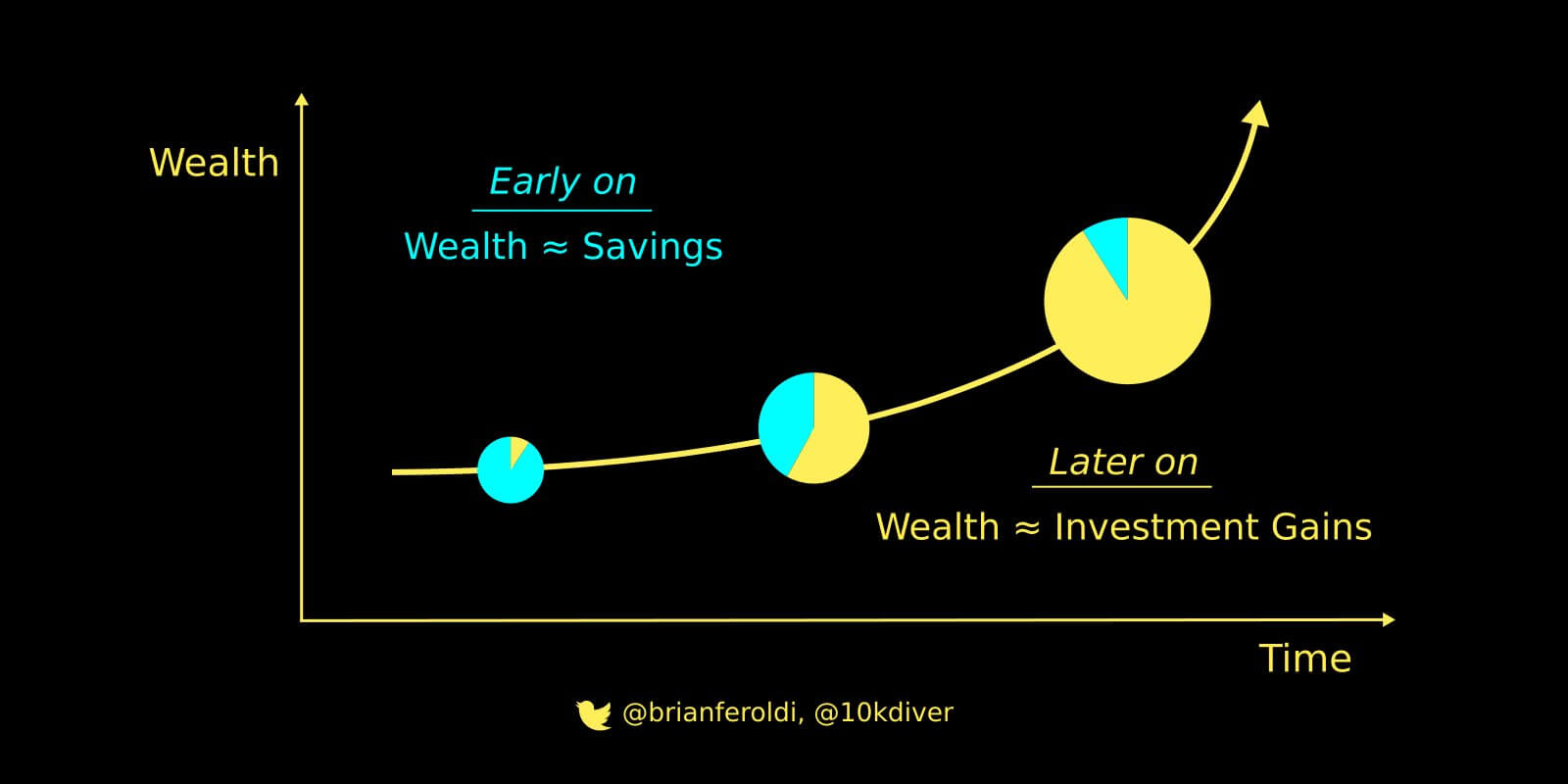

Last week, I came across this Tweet with a great illustration of how wealth is built.

I do have something very similar in my Wealthy Formula.

Brian Feroldi illustrates that early on you would need to have enough savings or what I would call surplus from work.

The majority of your net wealth is in blue, which are made up of savings. When you look at your investment on capital, you will wonder what is the point of investing since the amount is so small.

This may be a reason why cryptos and investing in high-growth business will look appealing as you can get a high growth rate fast.

During this phase, getting a handle on your earning from work, optimizing your expenses and investing your surplus is important.

The next phase would be the phase where you start seeing greater return on your capital. This is illustrated by the more balanced blue/yellow pie chart.

If you get to this stage, you will start beliving in your wealth machine, or your investment strategy because you are starting to see your investment capital grow.

The young investor at the start may wonder how does compounding work if we do not earn interest income on our investments. I do admit this can be challenging to visualize.

Perhaps, if you get to the last phase, you would see it. By this stage, the majority of your portfolio value is made up of the gains that grow overtime from your capital.

Your capital is lesser than your gains. Every annual growth are mainly growth from a smaller percentage of original capital from work and higher percentage from past gains on portfolio.

If you ask me, most likely you will get to the second phase (where you see meaningful investment gains) at about 6 to 10 years in.

The pace will depend on your savings/surplus rate. Some crazy people workng in certain industry built up $500,000 in 4 years. You will see meaningful investment gains that will make you a believer and make you wanna double down on growing your wealth.

Some will be smaller.

Ultimately, some of you might not understand this diagram until you end up at phase 3. This is normal.

To be fair, I don’t think I got to phase 3. I think I am closer to phase 2.

You may understand it better if you have a stock that gains 100% and you watching its growth after the 100% gain.

What you will notice is that the gains seemed to jump a lot more than when its less than 100%.

That is perhaps the best illustration of phase 3.

Keep a Lid on Investment Cost But Don’t Let it Guide All Your Investment Decisions.

Going back to the original cost discussion, your cost matters but during the initial phase, the cost do not compound that much. UNLESS your investment cost is crazy like 2% or more a year.

So the sensible thing is: keep cost low but don’t be over-sensitive to cost.

Remember also: You can always shift your wealth from one type of financial security to another.

Your investments are rather fungible and there are fewer frictions to change. This is why I would often advocate against insurance plans such as whole life, endowments and investment-linked policy. They have this lock-in that most often works against you.

Some of my friends and readers felt that paying 0.6 to 0.8% a year in access fee to Robo advisers are quite costly.

I am not going to argue with that but I would just like to say when your capital is low, when your annual surplus is low, invest with a Robo adviser because the pros they provide outweighs a lot of the cost.

You might even say they are worth it:

- Fundamentally sound financial securities

- Well curated and well-balanced portfolio

- Allows you to regularly invest in smaller sum.

- More intuitive interface.

Invest in one and when your capital grows, you would have options to optimize better.

There are also investors who wish to invest with a low-cost, efficient broker such as Interactive Broker but they find the starting cost to be prohibitive.

These are mainly readers who wish to invest in a portfolio of low-cost, tax-efficient UCITS ETFs listed on the London Stock Exchange or Hong Kong in a passive manner.

I do advocate longer term investors to use Interactive Brokers due to various advantages.

If your account is less than US$100,000, there is a monthly activity fee of US$10. This comes up to US$120 a year. The activity fee goes away when your value is more than US$100,000.

Your commission is deducted from this monthly activity fee so if your activity is low the max you will pay is US$120 a year. This looks expensive but if you ask an old bird like me, we are used to paying SG$29 commission a pop when we started.

You can use Interactive Brokers if you commit to the platform for the long term. Eventually you will have US$100,000 and the cost goes away. Your cost will be greater today but the cost amortizes over 20 to 30 years.

If your annual savings/surplus is $20,000 then the cost is (120*1.345)/20000 = 0.80% a year.

That don’t look too bad.

If it is:

- $15,000 a year: 1.0%

- $10,000 a year: 1.6%

- $5,000 a year: 3.2%

Honestly, if your annual investment amount is more than $15,000 a year, I think is ok to go with Interactive Brokers. If your amount is less than that, maybe go with a Robo such as MoneyOwl.

Lastly, let us take a step back and admire this illustration. This is where we wanna end up and it lets us know that at certain point, saving is important but at some point, managing your investment portfolio well is more important.

Here are some of my guides to get you up to speed:

My Comprehensive Interactive Brokers How-to Guides

Interactive Brokers is a great low-cost, financially strong brokerage platform that can be the standard broker for holding your long-term investments. You can access 150 global exchanges, including exchanges such as Singapore, the US, Hong Kong, London, European and Canada.

You will enjoy cheap commissions and zero minimum recurring platform fees or maintenance fees. Convert your funds to different currencies at near-spot rates, paying a flat US$2 fee.

To get started or become familiar with Interactive Brokers, check out my past articles on how to invest with Interactive Brokers. I hope the guides make your life and investing experience easier and brighter.

An Easy Step-By-Step Guide to Setup Interactive Brokers (IBKR)

How to Fund & Withdraw Funds from Your Interactive Brokers Account

How to Convert Currencies in Interactive Brokers

How to Buy and Sell Stocks and Securities on Interactive Brokers

How Competitive are Interactive Brokers Commissions Pricing?

How Safe is it to Custodized Your Money at Interactive Brokers? The things they do better than other brokers.

How Safe is it to Custodized Your Money at Interactive Brokers (2)? Financial strength of IB during recent banking crisis and during Great Financial Crisis

Interactive Brokers have Eliminated the US$10 monthly inactivity fee. More details here.

How to Transfer your shares from Standard Chartered Online Trading to Interactive Brokers

How to trade after-hours and premarket

Create Customized Reports and automatically send them to your email

What is the PortfolioAnalyst Report and Automatically Send the PortfolioAnalyst Report to Your Email

Send Money from TransferWise to Interactive Brokers

Interactive Brokers’ Fluid Interest Income on Cash

Introducing IMPACT by Interactive Brokers

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Julia Ng

Saturday 3rd of April 2021

Hi Kyith

Thanks for the sharing. Is it advisable to get a margin acct with IB? When would interest kick in?

Marc

Sunday 4th of April 2021

Small precision with respect to

> you will have to wait like 2 days after the money transferred in before you can use the cash for trading

Actually, in 99% of the cases, there's no need to wait. You can convert the cash, and use the converted amount to trade on the same day.

This is because the settlement dates of the currency conversion and the settlement date of the trade usually fall on the same date (T+2 usually). The only case where this may not work is around public holidays different in SG vs the US, as the currency conversion settlement date may be extended by a few days, and the trade still at T+2.

But except for these special cases, converted cash in cash account can be used immediately in most of the cases.

Kyith

Sunday 4th of April 2021

Hi Julia,

It is no issue getting a margin account if your intention isn't to always use the margin. The margin account gives you more flexibility in that if you are on the cash account, you will have to wait like 2 days after the money transferred in before you can use the cash for trading. The margin account makes things seamless. the interest will only kick in if you borrow. The best indicator of margin is that your cash value went negative. for example you may have a SGD account that have 10,000 and USD account that currently have 100. If you buy a USD stock that cost 5000, your USD account will show -4900. This means you have started borrowing leverage, even through you have 10000 in SGD. You can stop the margin by converting your SGD into USD but you get the picture.