You know… I have been explaining to people I talked to about the default low-cost, diversified portfolio setup that they should have.

Depending on your risk capacity (how much volatility you are able to take when you really experience volatility), you will have different percentages of equities to bond:

- X% invested in an unit trust or ETF that tracks MSCI All Country World Equity Index (E.g. VWRA traded on the LSE).

- 100% – X% invested in a unit trust or ETF that tracks the Bloomberg Global Aggregate Bond/Fixed Income Index (E.g. AGGU traded on the LSE or the Amundi Index Global Aggregate Fund on Endowus).

In the past year, there is this niggling feeling in my mind that has been bothering me.

If we want a bond allocation to complement other risk assets, do we really need the credit risk aspect that we get from having some investment-grade bonds given by the Bloomberg Global Aggregate Bond index?

My conclusion is:

Trying to capture the credit risk is less important if we have equities in our portfolio. To be clear, if you have an ETF or unit trust that tracks the Bloomberg Global Aggregate Bond index, my conclusion does not mean you need to change.

It just concludes that if you are thinking for the same bond tenor that matches closer to your financial goal, if you are considering a portfolio of government bonds, corporate bonds, or government + corporate bonds, the weight of your decision is not so heavy.

I think that is a good enough conclusion personally because it means I won’t be too weigh down if I need to choose between a Global Aggregate Bond ETF/unit trust versus a government one.

I will deconstruct the stuff I think about in the rest of this article.

Before We Start… The Role of Fixed Income Will Be Different Depending On What It Plays in Your Wealth Strategy

Investors often get misdirected by articles or content about a very specific topic, and fixed income may be one such area.

People are worried or excited based on what they read out there but I think many thnk about it without an overall idea about their investment strategy.

The role of bonds is different, and sometimes unnecessary, depending on your strategy.

I run a systematic, strategic, low-cost and often passive portfolio strategy like what I have described at the start of this post (you can read about my strategy in my personal notes here).

Strategy 1: The fixed income in this systematic and strategic portfolio strategy is to:

- Reduce the volatility of the portfolio. This is done because historically equities have low correlation with fixed income. Note that I say low correlation not negative correlation. If a 100% equity portfolio drops 50%, a 50% equity and 50% fixed income allocation should drop closer to 25% instead and that is more livable. For income planning, having fixed income is to reduce the “volatility drag” on the portfolio so that the investment portfolio can survive better.

- Make the investment experience more livable. For example, if I cannot take the drawdown of a full 100% equity portfolio on $5 million dollars, having components that don’t go down that much make the experience more livable.

- Reduce volatility drag if we are concurrently spending down from the portfolio. If you don’t spend from your portfolio, if your portfolio go down 50%, you have all the money there for it to recover when the portfolio returns 100%. However, if your portfolio go down 50% and you spend 5% of the portfolio by extracting income, that places stress on the portfolio such that you need a 122% to get back to where it is.

- Don’t missed out of investment return opportunity cost too much. It is not about earning high returns because the high returns will be earn by other components. You just want this portion not to lose out to the better performing components in the portfolio too much.

#4 is what we are going to discuss the most later.

Do note that when we refer to fixed income here, we are looking at it as a portfolio of fixed income not a single bond.

Strategy 2: Now… if your view about bonds is that you are very, very risk averse, or low risk capacity, and want a 100% fixed income portfolio, then the needs are very different:

- Take care of the volatility of the portfolio so that the experience is more livable.

- Earn a decent investment return for the risks that I take.

- Make sure that the average duration of your fixed income ETF/unit trust is less than the time you need the money (your break-even point)

The main difference here is that there are no other components to drive your returns except for fixed income. So you will have to be thoughtful about how you structure your fixed income portfolio.

The question in your mind is how much more risk do you wish to take:

- Term risk: How long of a tenor do you wish your fixed income portfolio to be?

- Credit risk: How poorer grade of bonds do you wish your fixed income portfolio to be?

The longer the tenor, the poorer the credit quality, the higher the potential return but the volatility will be higher. In order to earn higher return, you need to take on greater risks.

Do note that when we refer to fixed income here, we are looking at it as a portfolio of fixed income not a single bond.

Strategy 3: Buy individual bonds. Those that you buy at $250,000 per clip.

This is what many older, richer investors have in mind when we talk about fixed income but I shall not go too much into it.

The thing is… if you talk to enough people, they have no freaking idea what the fxxk they are doing with their bonds. They think in Strategy 2 or 3 but actually their situation in Strategy 1.

Taking Adequate Term and Credit Risks with a Global Aggregate Bond Index in Order to Earn a Decent Return.

In order to earn a higher return in fixed income, you got to take on greater term and credit risks.

So some richer, Singaporeans decide to take this to a whole new level by buying individual bonds issued by Rickmers Maritime Trust in the past. Longer tenure, higher coupon.

They took on the risk but eventually lived with a bond default.

Reflecting back, the problem wasn’t the bond but more of the investor. We gambled that the risks is actually lower than what the bond is priced at and we got it wrong.

If you look at the spectrum of risks, at one end will be short, 1-month tenor, government bond bills and on the other end is 5-year high-yield bonds issued by some risky listed small cap company (or even unrisky one).

What is the risk you will take on this spectrum? It is good to think about this and I think some of you might wonder about this from time to time.

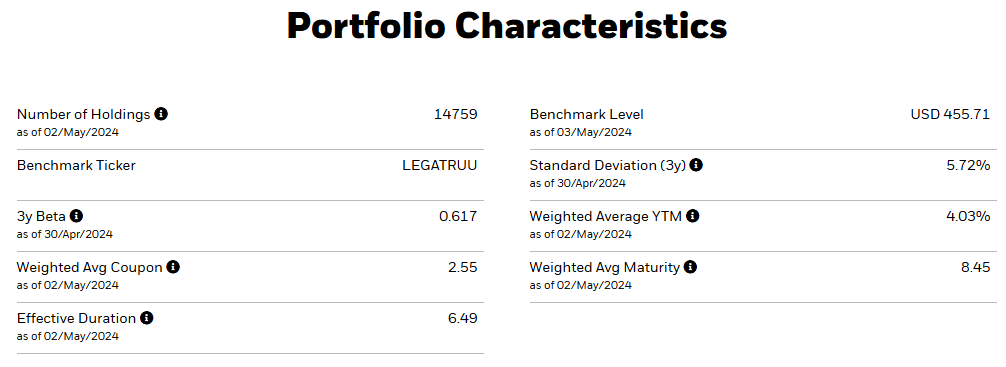

I lifted the following portfolio characteristics from iShares Bloomberg Global Aggregate Bond factsheet:

The portfolio of bonds is very diversified but the effective duration of 6.49 years show the sensitivity towards interest rate. A 1% move up in market interest rate, would reduce the index return by 6.49% theoretically (in practice the relationship is not linear but there is a relationship).

The weighted average maturity of 8.45 years show the length of a tenor.

If you are using this bond ETF solely to do asset-liability matching for a financial goal, the time you need the money needs to be longer than 6.49 years (the duration) at least to break even (not to capture the return).

This index is more risky due to this term risk, compare to not much term risk if you are using a 1-month bond or bill.

More than 50% of the index is made up of government bonds which explains why majority is AA rated and above. We can see that this index is like half investment grade and half government and that will help us make decision.

If you wish for higher return, you can push this further out such as:

- The TLT (or DTLA, which is the UCITS version) which is the ETF for 20-year US Treasury.

- High yield junk bond ETF.

So you have options.

If We are Running Strategy 1, How Much Term Risks Should We Take?

This is a good question for me to think about.

This question is asking indirectly:

What is the length of time till I need to use the money?

This is a time horizon question. If your goal is a 40-year accumulation towards your retirement, technically you can have 20, or 30-year bonds in your portfolio but if you need the money in 12 years and you wish to have both equities and fixed income in your portfolio, you may need to use bonds of lower duration.

Daedalus is to be geared to distribute income and therefore it seems I “already need the money today”. If so, what is important is less about the length of time, but reducing the volatility of the portfolio.

This means that I should cap the duration of the fixed income component.

I considered that the duration of the Global Aggregate Fixed Income averages 6.4 years despite having an average 8-year tenor.

6.4 years is not long, long but I do think that more and more, I see the appeal of keeping to a duration or tenor of 4-5 years.

If we break our portfolio into equity and fixed income during spending, and we wonder which portion to sell our units to get income, a rational consideration will be:

- If the equity market is down, sell part of the fixed income portion.

- If equity market is up, either sell equally or sell more of the equity portion.

The fixed income acts like your cash holding.

But we know that fixed income is more volatile than cash. If I can keep my fixed income to a shorter duration, that would minimize the volatility.

4-5 years is not so far away in that most of our planning is for money we need in 3 years time but if fixed income does not do well… either

- We lived with some smaller losses

- or delay our plans a little more.

6 to 8 years is relatively further away.

But we know that we may be losing out on some term risk premium.

How Much Term Premium Are We Talking About?

I want to see the difference in return for credit quality and term.

We have the total return (capital gains plus income) for only selected fixed-income indexes. Most are based on United States fixed income but that is okay because what I am more interested in is the interplay between term and credit quality.

I use:

- 1-month US Treasury bill as a proxy for very short duration bonds, to the extend that it is considered as cash.

- 5-Year US Treasury Note as a proxy for risk-free government bonds, or fixed income without credit risk.

- Bloomberg U.S. Credit Corporate Investment Grade Bond Index as a proxy for corporate fixed income with credit and term risk.

I have the bond data from 1973 to March 2024 or 51 years.

I am more interested in two investing periods:

- 5-years: Long enough for fixed income to break even if the time horizon is longer than the duration.

- 3-years: What happens if the time horizon is too short and investor invest in a portfolio of longer tenor bonds.

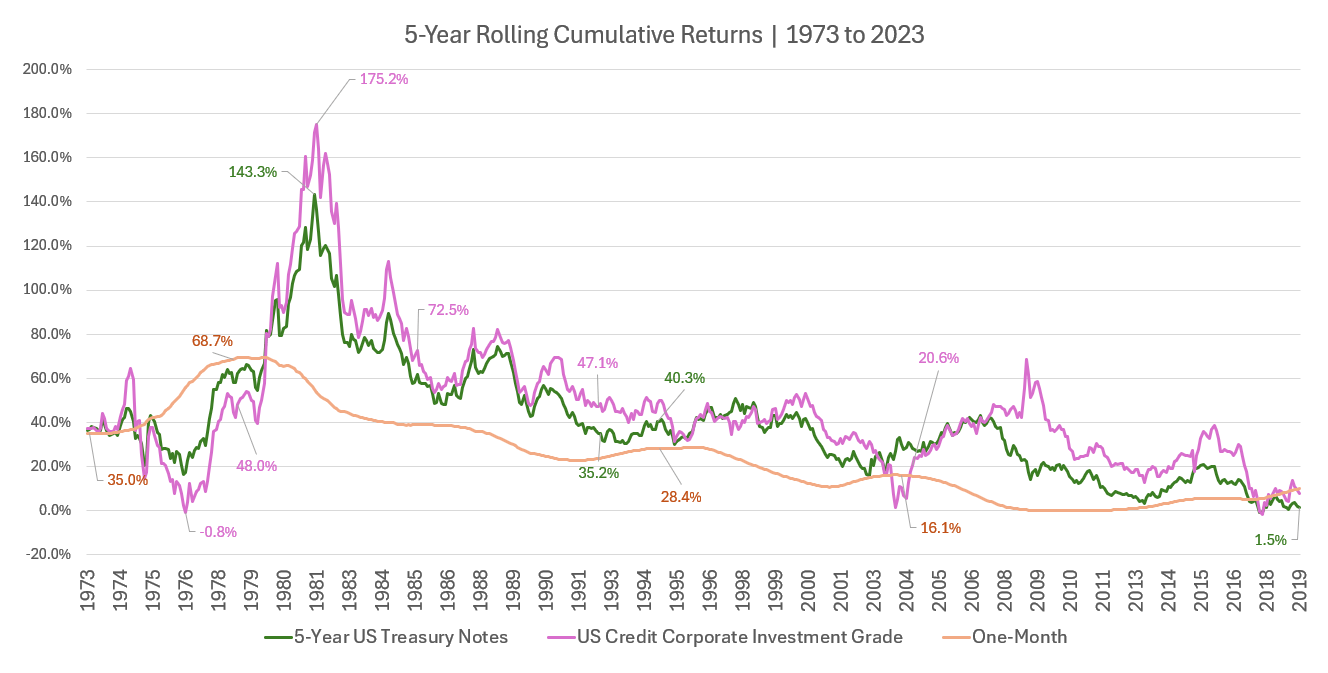

The first chart shows the rolling five year returns:

Each point on this chart represent a cumulative (as opposed to annualized) 5-year return. So from Jan 1973 to Dec 1977 the cumulative return is 35%.

The first thing we observe is that if we abide to the duration so that we are not longer than the duration, some of the lowest return (which are the years starting in 2019 and those starting in 1975) will still be closer to positive.

This duration should be something you should take note if you require some sort of principal certainty.

The orange line is the one-month short fixed income or cash rate.

You will observe that if you invest for five years, you stand a high chance that investing in longer tenure bond portfolio gives you higher return.

This is more important for Strategy 2.

However, there are periods where the five year returns is closer to the orange line, such as those years starting in 1975 to 1980.

Note: It is not that you don’t earn returns or losses! It is more of that you seem to have taken risk with not much reward.

But the thing is: would you be able to spot this regime shift before this? And if you take risk but earn cash like return, is it as bad as losing money?

I think not.

The pink line for the most part, is above the green line, which indicates the credit premium.

But there are some five year periods such as the years starting in 1976-1980, 2004 where you are not rewarded for buying lower grade bonds.

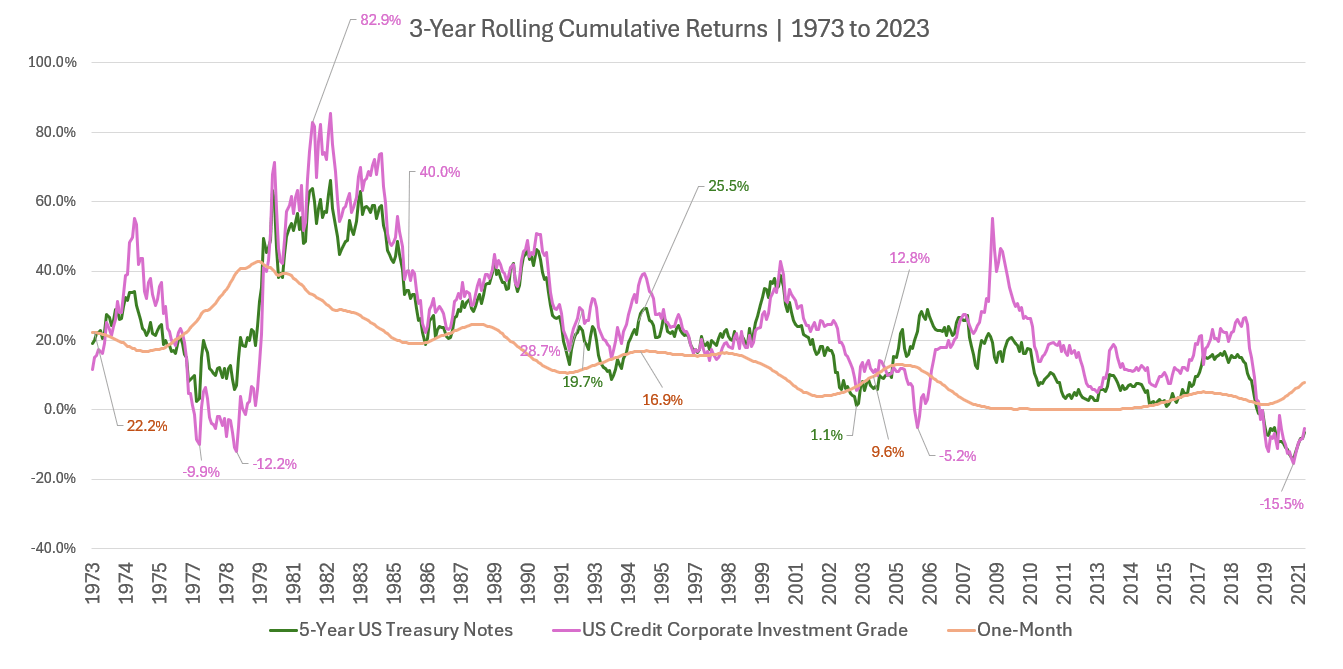

The second chart here shows the rolling three year returns:

This chart show your experience if you invest in more than 5 year duration fixed income portfolio and needing the money in a shorter term.

What you will notice is that there are periods where you suffer unrealized losses (1977 to 1979, 2006 for credit corporate, 2020 recently)

The one-month treasury doesn’t suffer losses.

A summary of uncertainty:

- Whether taking risks with lower credit quality gets rewarded.

- Whether taking risks with longer tenure bonds gets rewarded.

And because you don’t have a crystal ball, there is uncertainty, and therefore there is a risk premium to be earned.

If I am investing for more than 15 Years, How Much More Returns Above Risk-Free Rate Are We Talking About?

We can see a certain premium if we invest in lower credit quality and longer-term bonds, but how much are we talking about?

Does it matter enough?

If I am more concerned about Strategy 1, most are wondering if there is a big premium difference if we hold on for a longer period.

15 years should be a good period to judge. This length is not as long as the traditional retirement accumulation period but long enough for some longer-term goals such as accumulating for your child’s education.

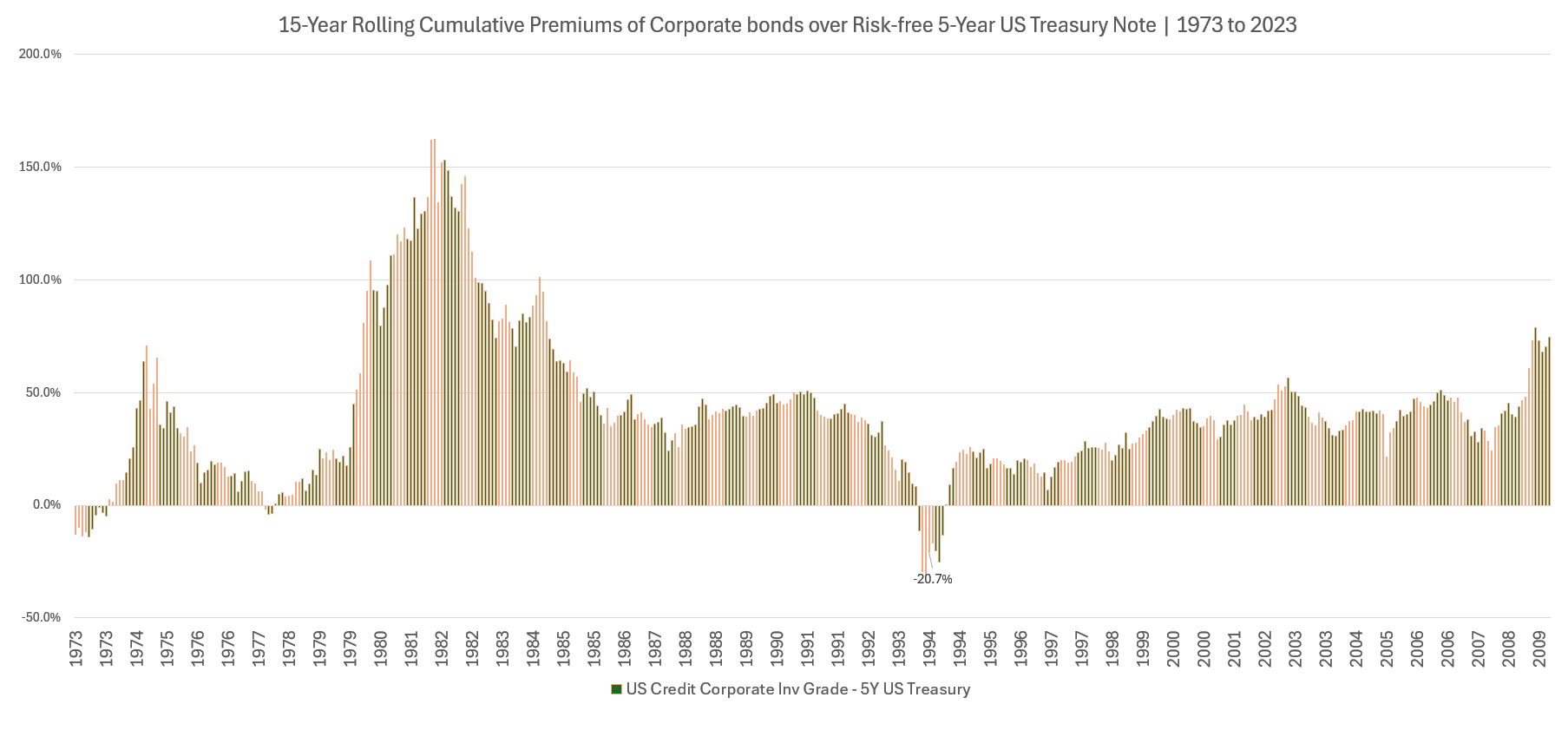

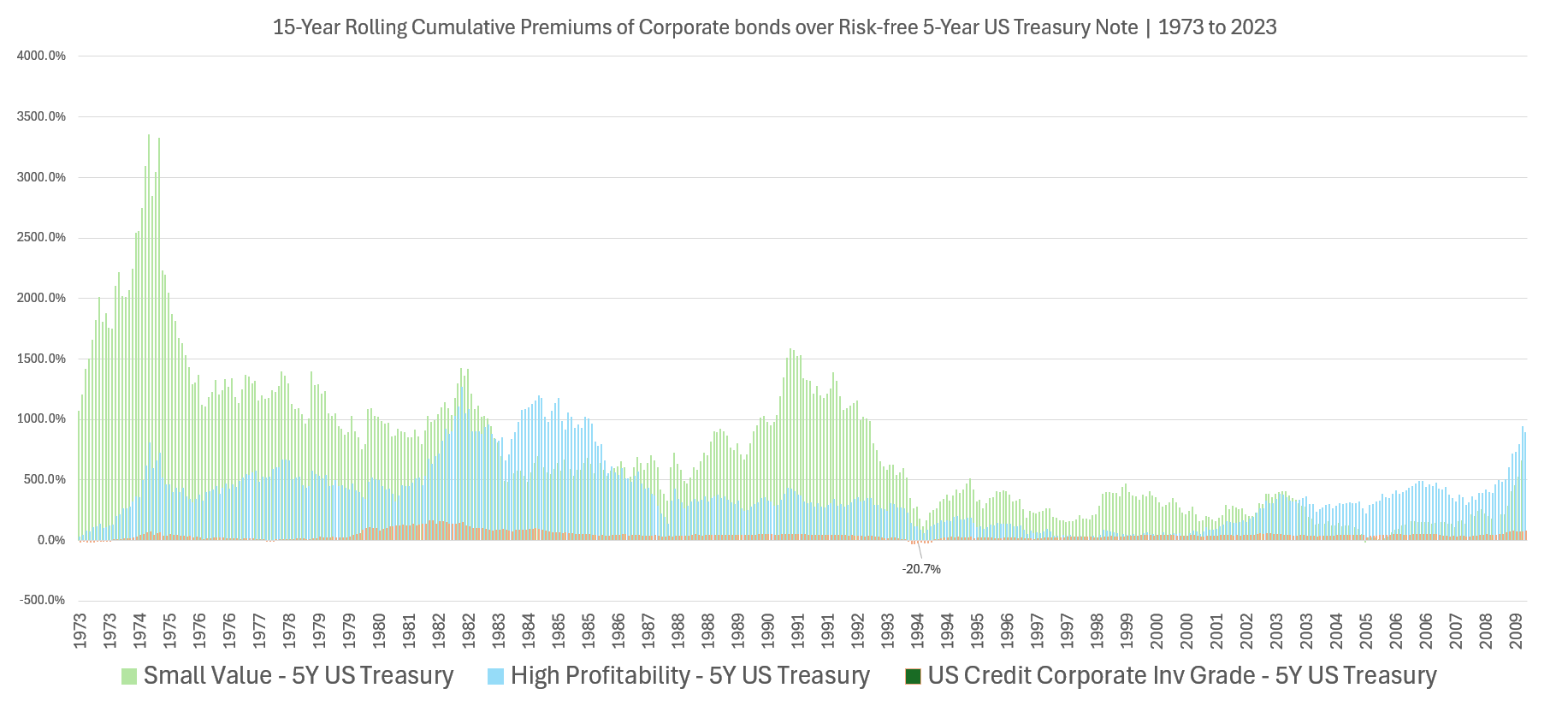

The bar chart below shows the returns difference if we take the 15-year return of the US Credit Corporate Investment Grade index minus the 5-Year US Treasury Note index:

A positive bar means that US credit corporate investment grade bonds perform better than the US 5-year treasury if you buy and hold and stay invested for 15 years.

A negative means the opposite.

We observe that the cumulative 15-year premium hovers slightly below 50%.

This looks significant.

If you are doing Strategy 1 and are deciding between a government bond ETF and a pure investment-grade bond ETF, most of the time, the pure investment-grade bond ETF will do better.

A long term investor adopting a strategic, systematic, diversified buy-and-hold passive portfolio earns that credit premium not always (see those 1973-74 and 1993-94 15-year periods).

Are Government Bonds Better than Credit Corporate Bonds When Equities Don’t Do So Well?

The role of fixed income in Strategy 1 is when equities don’t do so well, having an allocation of fixed income make it more livable.

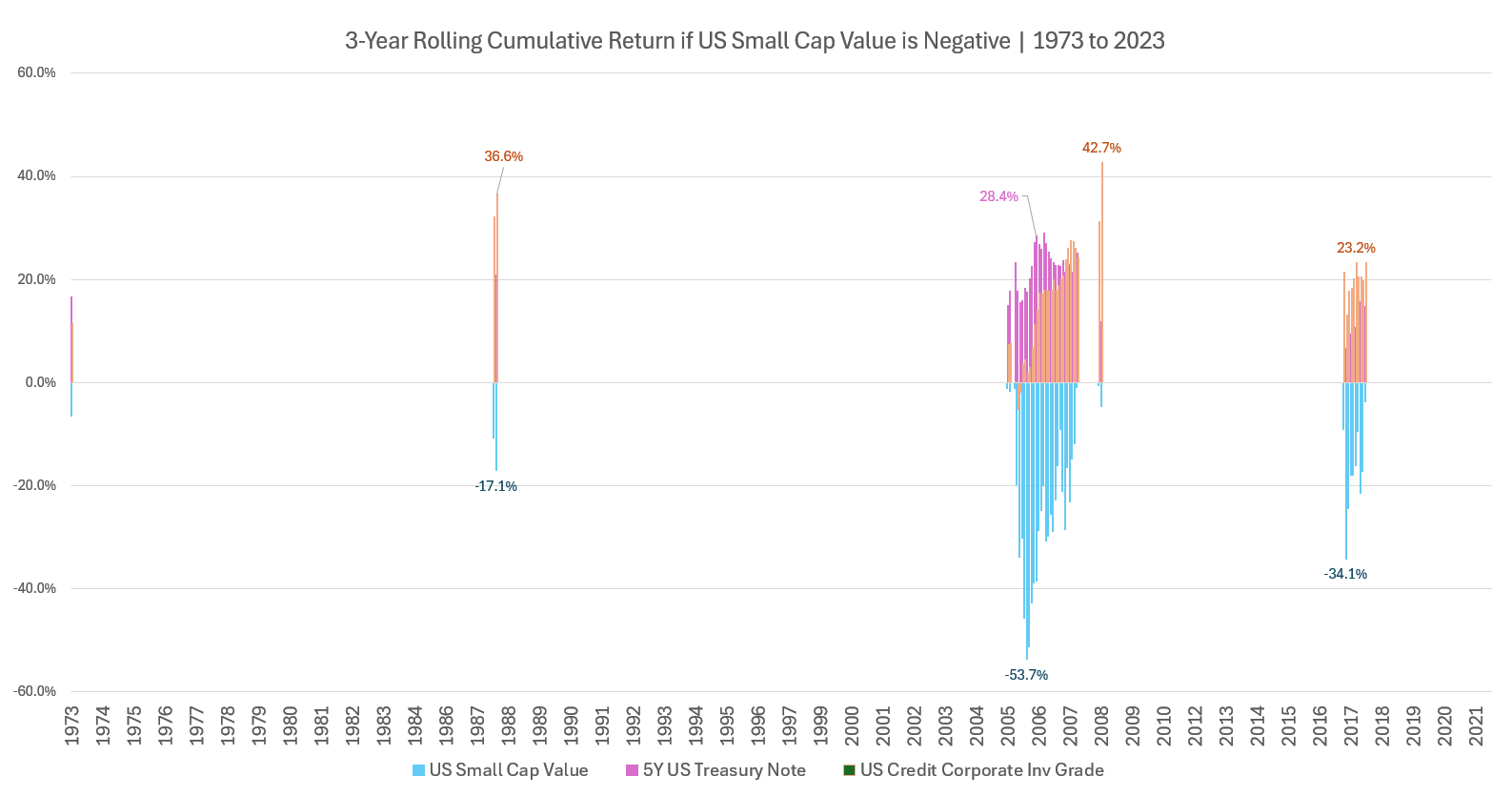

In the chart below, I plotted the 3-year cumulative returns of 5-Year US Treasury Note and US Credit Corporate Investment Grade, when equities, represented by Fama/French US Small Cap Value is negative for 3 years:

If we use a 3-year timeframe instead of a 1 year or 6-month time frame, there are not many distressed periods in the past 51 years. This is a data point.

When equities return is negative, both bond indexes did well.

This is what you want.

The interesting thing is despite credit corporate bonds having higher risks, when judged over a 3 year timeframe, they also did better.

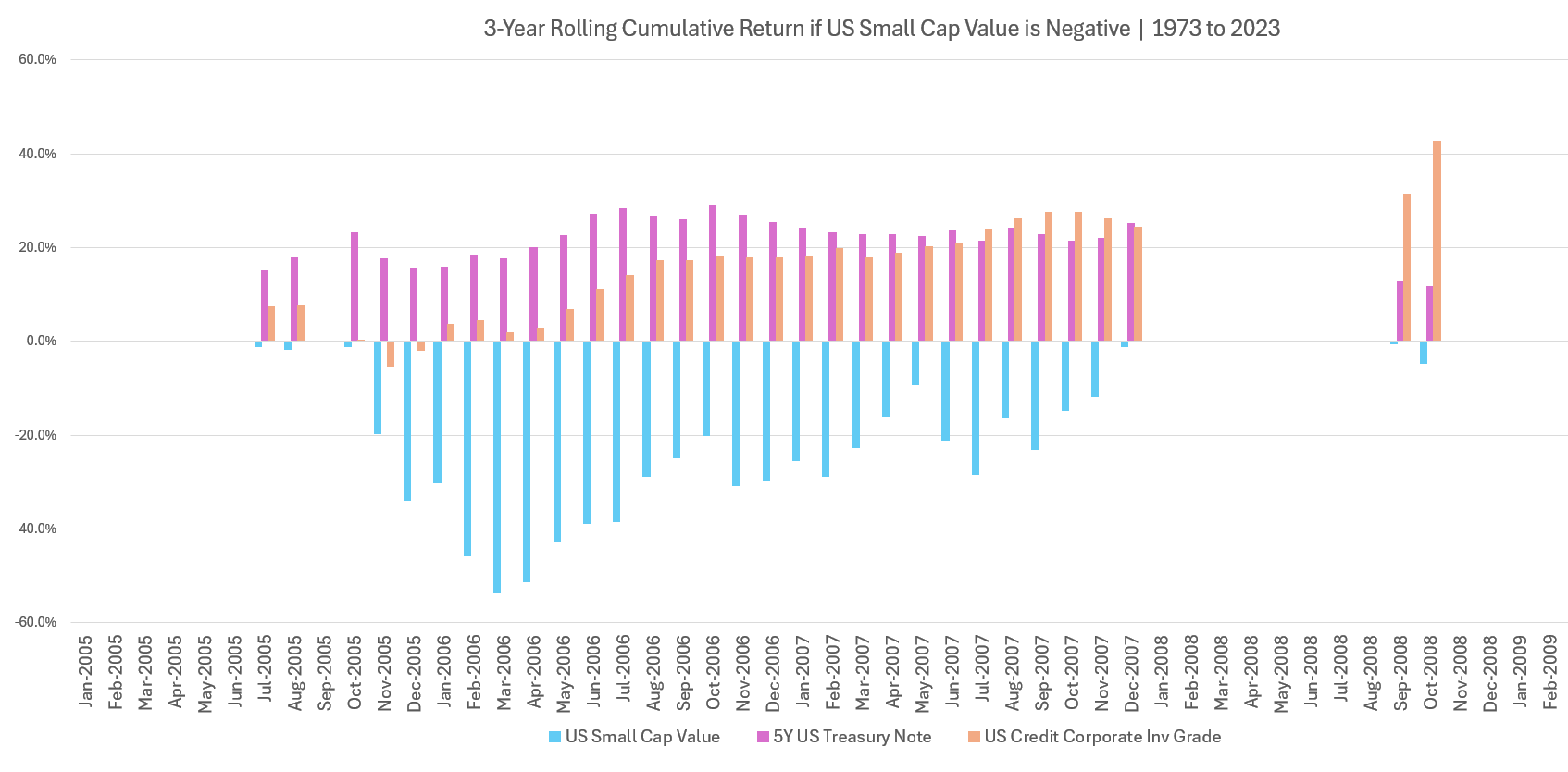

Let us zoomed into the periods after 2004 so that we can appreciate the data better (ignore the time period in the header. That is wrong):

During those period when US Small Cap is down for 3 years, US Treasury is more consistent.

There were periods like those starting in November and Dec 2005 where US credit corporate did not do such a good job buffering the portfolio.

We have to dig in and ask what role we want for the fixed-income portion of the portfolio.

If such events happen next time, do we want the fixed income portion to do what it is suppose to, if this is the main reason we have it in our portfolio? Or is something else more important than this?

I think how you answer this will decide which one you pick.

Credit corporate investment grade bond index actually did better in the downturn during Sep and Oct 2008. The cause of each distressful period is not always the same.

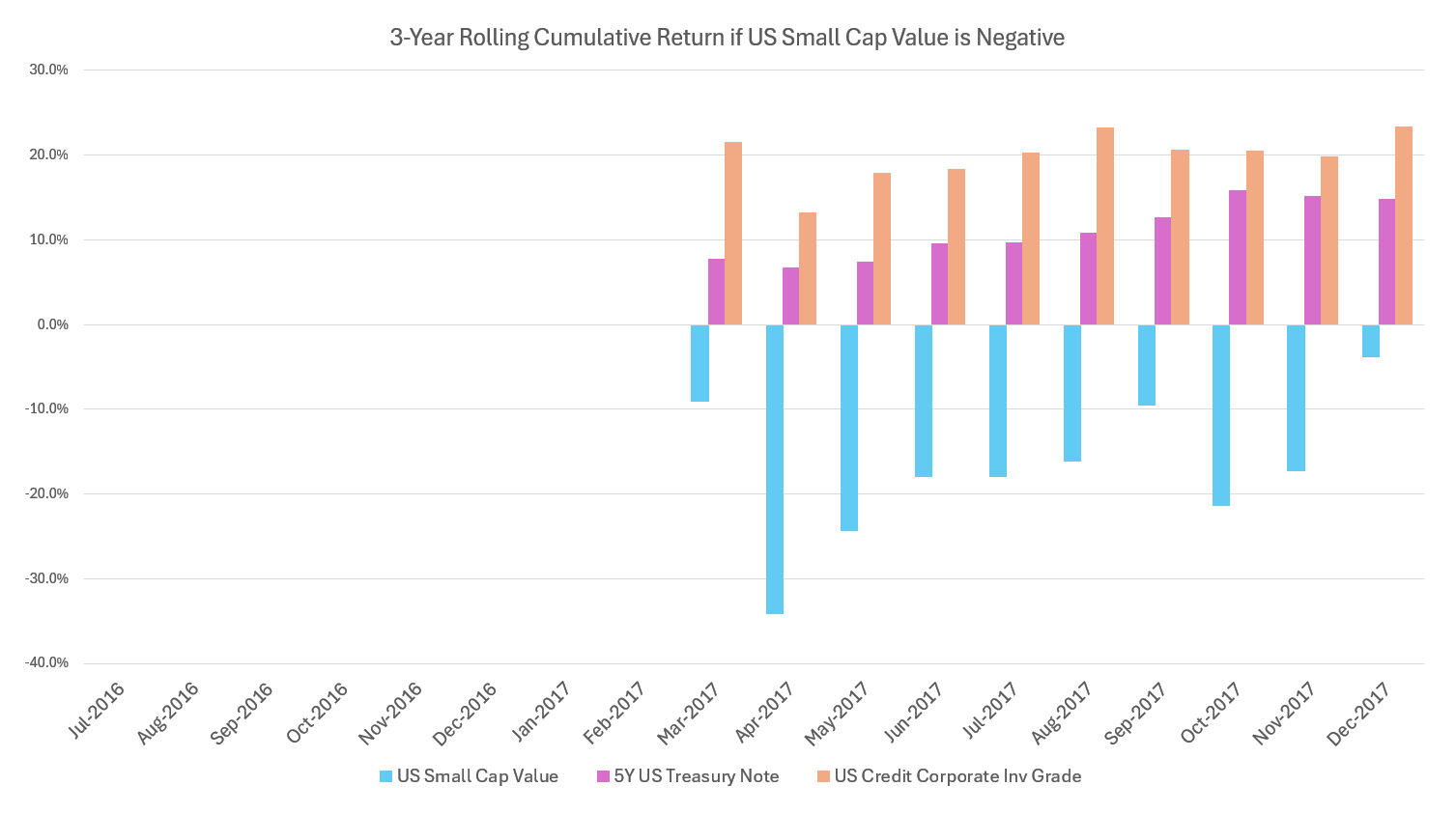

Here is the comparison if we zoom into the 2018 period:

Corporate bonds, the absence of specific distress, actually did better.

My personal answer to that question is that I lean towards having government bonds of the right term if possible, if the role of the bond is more to make the process more livable because if there are periods of distress that involve corporate credit as well, I want my fixed income portion to work the way I want (refer to the Nov 2005 to May 2006 period).

The data at least tells us that if you have 40% bonds, you don’t lose money on that allocation, even if you have corporate credit as part of a Bloomberg Global Aggregate Bond index, if we look at it with a 3-year time frame.

I heave a sign of relieve there isn’t a big problem here, regardless of my eventual decision.

What will Drive the Return Will be Equities for Strategy 1

Some folks might be thinking… The returns on bonds are low if we don’t take risk with it.

The 15-Year Rolling Cumulative US Credit Corporate Minus 5-Year US Treasury Chart clearly shows that there is a credit premium.

But what if we layer the 15-Year Cumulative return of US Small Cap Value and US High Profitability Index by Fama/French here (Some of you will ask why I use this instead of the S&P 500 and its because I am selfish and am concern about returns of these two factor investing segment. But these two should be reflective of general equities in some ways).

Here is the same chart as before, but we take the Fama/French Small Cap Value Research, and High Profitability minus the 5Y US Treasury Note return:

You can see both of them dwarf the premium of taking fixed-income risks.

If your fixed income is part of Strategy 1, what drives the return will be the other sections.

If the Role of Fixed Income in Your Strategy is Different from Strategy 1, Your Conclusion May be Different.

If you are doing Strategy 2, or a direct bond strategy, how much risk that you take, whether you should be taking those risks will be kind of different.

Should you push all the way to high yield?

I don’t know. You got to figure out whether buying an individual high yield bond or buying it as a collective is fundamentally sound.

I only managed to have the data for High Yield bonds which I presented in this article here.

The Beauty of High Yield Bond Funds – What the Data Tells Us

My honest opinion is

Most people have low true risk capacity and cannot take volatility. But they think all fixed income are the same. That means they are safer than equities and not much risk. But the problem is there is a spectrum of risk in fixed income as well.

Many are also lured into the safety of predictable single direct bond issue. They don’t understand bonds packaged in a unit trust and because they don’t understand, they don’t trust it.

What fxxks up most people is not fixed income but the way people marry these beliefs together. Bonds are generally safe. Single direct bond issue you can see your principal return clearer and the coupon earnings better.

So they end up buying single direct, high yield bonds that are dangerous with minimum of $250,000.

And they are encouraged by their bankers to leverage.

The data do show us if we have a long enough time horizon (greater than three years), investing in some corporate bonds, taking some risks, but not extreme risks, can be decent.

Last Word

Okay, that’s it. Time for breakfast.

I was going to do some on what are some good bond ETF alternatives to slice and dice things but I will keep it to another article.

This is a long article and if you wish to focus on:

- If we don’t push out too far in the fixed income risk curve, both corporate bonds and government bonds, when invest in a basket is quite decent.

- To break even, make sure that the duration of the basket of fixed income is shorter than the time of investment till you need the money.

- If fixed income in our portfolio is to cushion the short term poor returns of equities to make the experience more livable, both government and corporate bonds can do the job but government bonds is more consistent (this is for strategy 1).

- If you don’t know what is the role of fixed income in your investment or wealth strategy, it is time to figure out because there is no best, best stuff out there but more what fits the needs.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Johnny

Sunday 5th of May 2024

For bond funds, my understanding is that you have to be able to hold for 2x the duration of the fund in the event of a rising interest rate environment, not just 1x the duration of the fund.

Johnny

Monday 6th of May 2024

@Kyith, https://content.csbs.utah.edu/~lozada/Research/IniYld_6.pdf

Kyith

Monday 6th of May 2024

Hi Johnny thanks for sharing this perspective. Could you point to the resource that will explain that? Thank you.