I have a 54-year-old reader contacting me about his situation.

Let’s call him J.

J’s original plan was to work for four more years or wait till 65 years old to consider retirement.

But recently, he realized that there is a potentially re-organization plan in his company. By his own admittance, he tends to be more paranoid about certain things, and while there are no official announcements, he feels anxious about his own situation.

J does not see himself stopping work, but getting a job might be harder if he eventually gets the cut.

He wonders if he doesn’t get a job, would he still be able to meet his commitments? Can he retire at 55 years old?

Financial Security is Preciously Sought for but Difficult to Describe.

I feel like many people are similar to J in that they do not wish to stop working but they have enough insecurity about their work situation that they seek out financial independence.

In truth, what they are afraid of is never able to find a job that is as good as what they have currently.

And so financial independence is the antidote to their problem.

But if we look at it, you can buy financial security with:

- Twelve months of an emergency fund.

- Enough buffer to pay for your mortgages.

- Five or ten years’ worth of your current annual spending.

Why is this good enough?

- You don’t want to stop work, probably young enough to pivot (willingly or reluctantly) into another job.

- You just want a good margin of safety so that you can build your career back-up.

- You don’t want your family’s lifestyle to be compromised too much.

Then again, ten years worth of current annual spending is not a small amount either but you have to ask yourself if a five-year runway or a ten-year runway is safe enough.

In my opinion, having some runway is better than no runway at all!

We have to recognize that J is also getting close to the age where he can officially retire.

For a person of his profile, finding out the answer to whether he can fully retire at 55 years old is quite valid.

I could do an in-depth analysis but I feel that J is looking for some handles about his current financial security above other stuff, so that is my focus area.

His Family Situation

J is the sole income earner in his family. He currently earns $8,709 a month and brings home $7,400 a month. There is something that I cannot square about the income and the asset build-up but I decide to leave that aside.

J has a daughter that is still pretty young (7 years old).

He would like to set aside S$500,000 for his daughter’s university education in ten years’ time. This is based on the cost of an overseas degree today.

He has a retirement goal at 65 years old through a combination of his stocks portfolio, bonds and cash and he would like a way to support his elderly parents who is in their late 70s and 80s. But that wasn’t really well articulated to me.

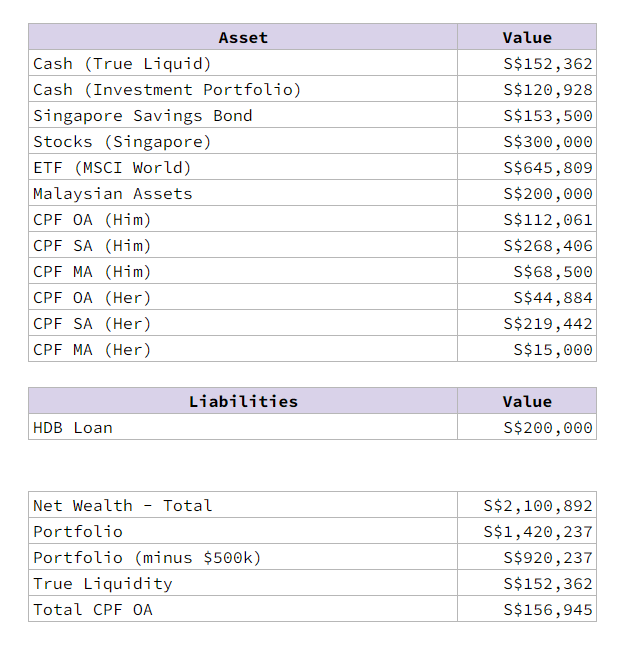

His Financial Assets

The table below shows J’s family assets and liabilities:

The first question that pops into my head is how a single income can amaze a net wealth like this!

But that is not the most important thing. What is important to figure out is what to do from this point onwards.

J still has $200,000 in outstanding mortgage on his HDB mortgage. He has also separated the cash which does not have a goal ($152,362) and the cash meant for his investment portfolio ($120,928).

Both his wife and him has reached CPF Full Retirement Sum (FRS). This means that by 65-years old they have an annuity income close to $3,200 monthly to depend upon to hedge their longevity risk.

His portfolio is made up of Singapore stocks, MSCI World ETF, cash, SSB and Malaysian Assets. All these totalled up close to $1.4 million.

Since J is one year away from 55 years old, this means that both their CPF OA becomes liquid and they have $156,945.

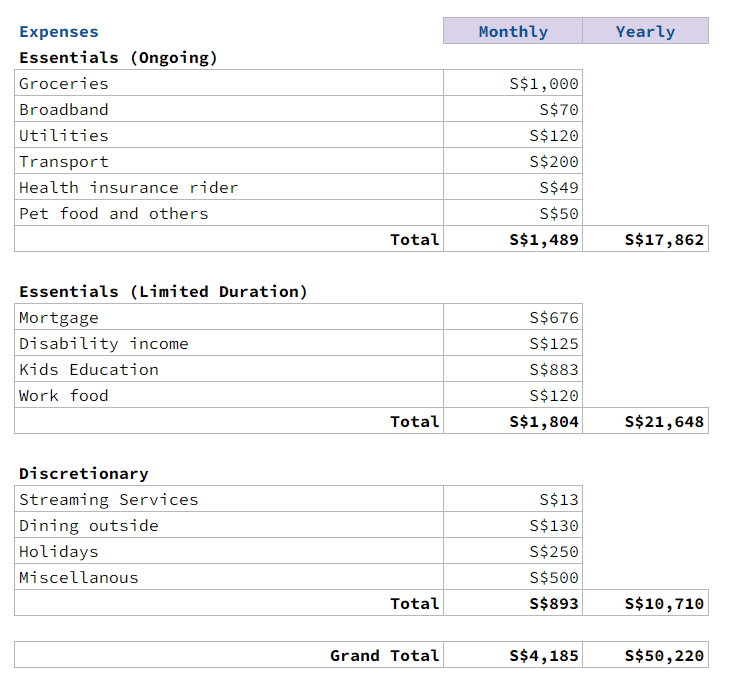

Their Family Spending

After the last case study, I think readers will now dutifully provide an idea about their spending desires.

J provided me with his desired spending lifestyle:

I decided to regroup some of their family’s spending into two groups of essential spending, a part that is ongoing and a part that is limited to duration.

There are some spending such as mortgage, kid’s current education and living expenses, disability income that will come off at a certain point.

To me, it is inefficient to accumulate a bunch of assets to provide income for some spending that will eventually go away.

J’s desired lifestyle would be $4,000 monthly but in truth, I think it is closer to $3,500 a month.

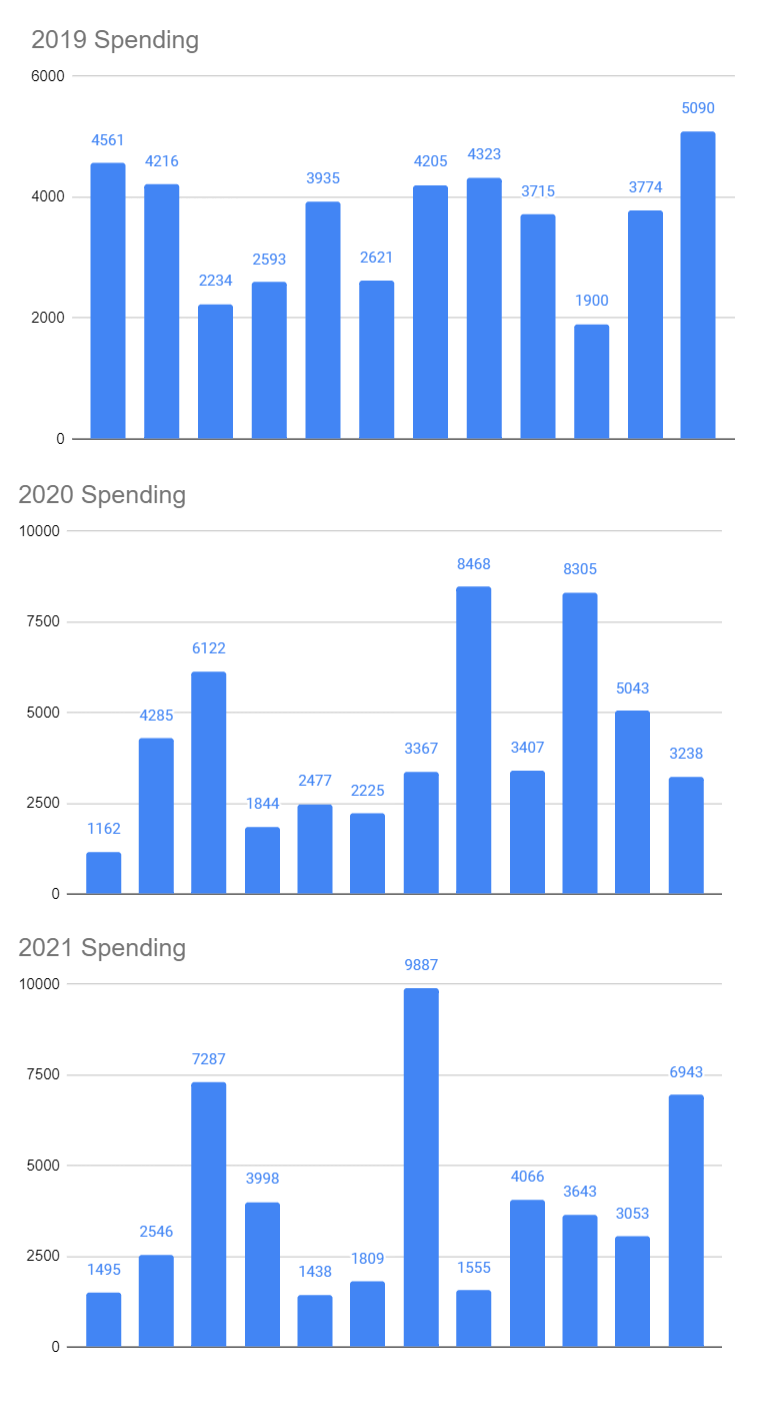

J also provided me a glimpse of their family spending for the past three years:

The annual spending works out to be:

- 2019: $43,167

- 2020: $49,943

- 2021: $48,743

The change between the 2019 spending and the 2020 spending was a surprise for me. J shared with me that this is because of the shift in spending patterns due to Covid. He pays for most things (especially kids education) with a credit card and he pays for the debt next month. This caused a lot of spending volatility.

It feels to me that as a base, the family spends around $1,500 a month but in some years you get very lumpy spending, but its kind of scary that some of the lumpy spending just jacks up to $10,000 (unless it is income taxes).

The other possibility is if it includes something that should not be included.

The worry I have is less about the assets origination but whether their desired future spending lifestyle is realistic given the volatile spending pattern.

Remember Kyith is a human FI calculator. If you give him something that doesn’t make sense, the conclusion is something that won’t give you enough security as well.

My Planning Approach

The most important question to answer is: If he loses his job, how bad would his situation be?

We have to think about what is the most desirable lifestyle in that situation.

There are two desired situations.

The first one:

- Have an income equivalent to current spending, at least until he finds a new job or until he reaches retirement.

The second one:

- Separate the financial assets to fund the financial goals that are important to him.

- See if the residual income allows him to stop working.

I prefer the second approach because it is much more optimised. Most people would prefer the first approach but usually, the first approach would need you to have much more capital.

It may also mean you will have less margin of safety.

For example, if we go with the first approach, we will need an income stream that can generate a consistent inflation-adjusted $21,648 yearly for a long time. Whether we use 3% or 4% safe withdrawal rate, the capital needed just for this portion is between $541k to $721k.

But due to the certain nature of this spending, we could just set aside $350,000 today and be done with it. What we are left with may be $190,000 to $371,000 in capital for his other spending.

With that this is my general approach:

- We want to set aside $500,000 for the daughter’s education since this is dear to the family.

- We want to be mortgage-free if we stop working.

- We can commit a lump sum for the fixed disability income insurance for ten years.

- We commit to an inflation-adjusted lump sum for the kid’s expenses, which will include education, enrichment and future tuition costs.

- Whatever that is left over would be the income for their family’s essential and discretionary expenses.

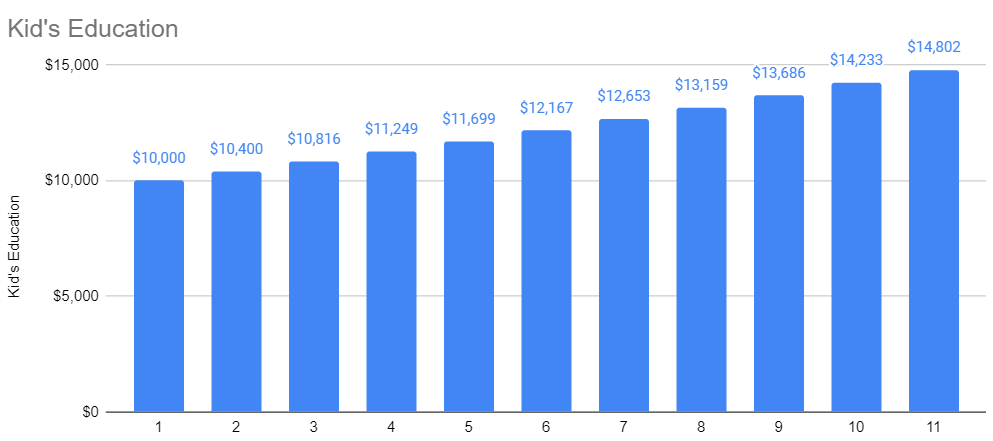

The Kid’s Future Spending (not inclusive of her tertiary education cost).

J felt rather strongly to provide for his daughter’s studies as best as he could.

Given that the daughter has eleven years of education more to go, the expenses should look like this, if we use 4% a year inflation:

I think J has catered enough and I applied a higher than normal inflation adjustment. If this is inadequate, I think J is ok with make do with less.

We can set aside $135,000 in lumpsum for this.

Even if we wish to create a income stream from this, the short time horizon of the goal would mean that it eventually works out to a capital of $145,000, which is not too different from $135k.

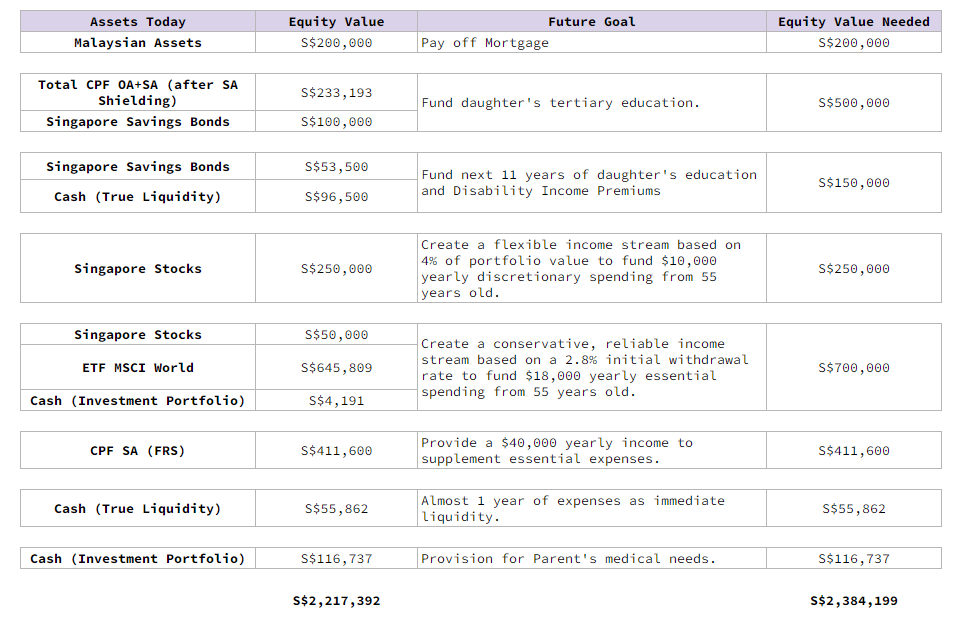

Resources Allocation to Fulfill J’s Family’s Financial Goals.

Given what J has (in Assets), and his wishes (his financial goals), we can see if what he has today, can fulfill his financial goals.

The resources allocation table below re-arranges what he has based on what we need to fund his financial goals today:

What J has today comes up to $2.2 million, less off the monies in both their CPF Medisave, which is not included in the table here.

The money is arrange in an order, best suited to fund the future goal. For example, if there is a need to pay off the mortgage, the Malaysian assets, which is valued at $200,000 today, would be sold off to pay off the mortgage. J has the option to use another asset if he wishes to.

Almost all his family’s goals are funded except for how to fund his parent’s later life medical expenses. For that I carved out $116,737 from the cash in his investment portfolio in case he needs the money.

Equity Value should add up to be equal to Equity Value Needed except for the funding for J’s daughter’s tertiary education. I used a lower amount because of the high certainty of earning the return within the next 10-11 years to reach $500,000. J will need to shield his CPF SA so that the monies left can earn a higher interest.

Let us take a look at the income for expenses.

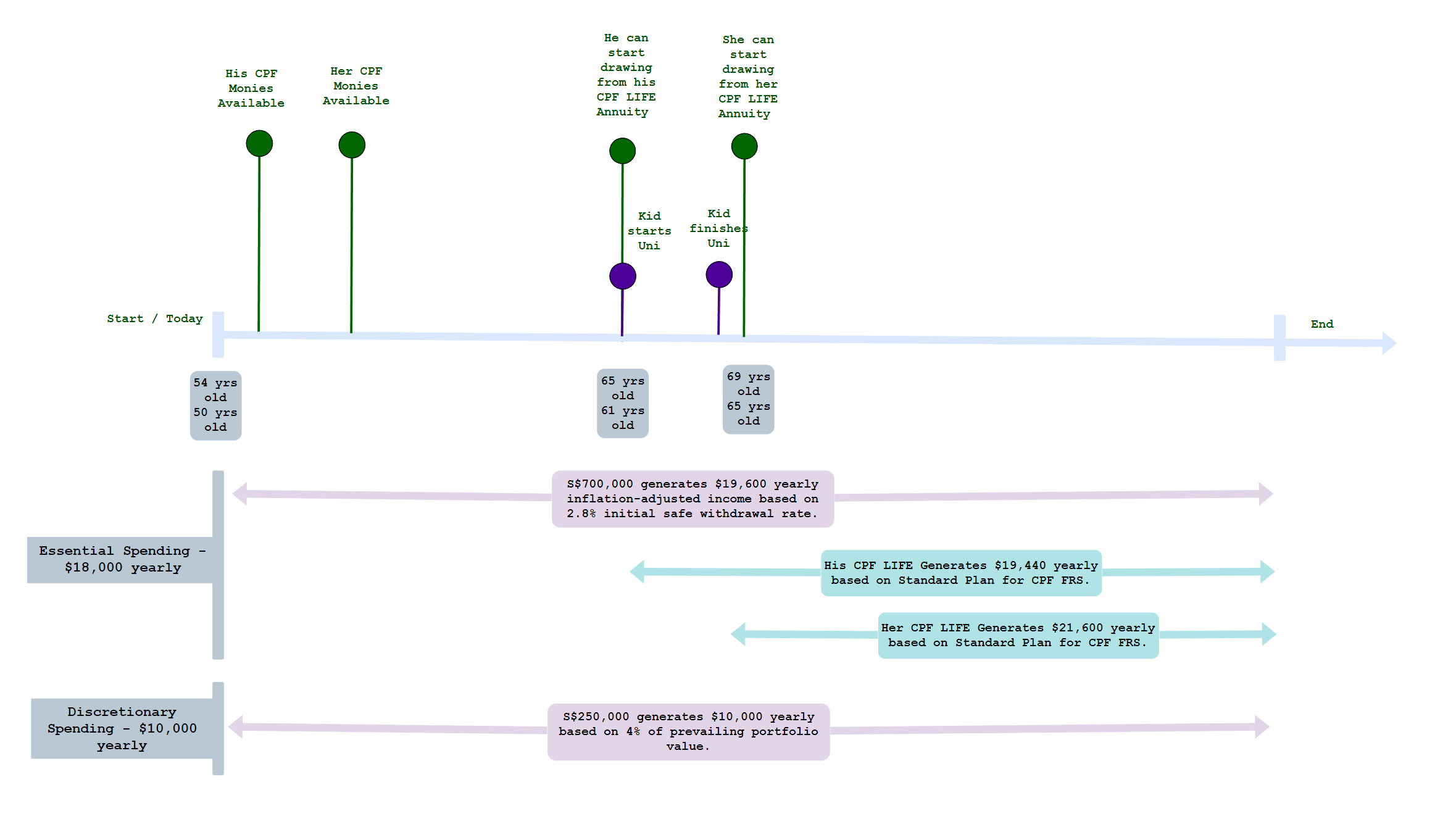

Fulfilling His Income Needs if He is Unemployed

The illustration below explains J’s family income needs from now till end-of-life:

The challenge always is that our CPF LIFE income only becomes active at 65 years old. In the meantime, the income needed will have to come from either a lump sum or a portfolio.

In the past, I would use a lump sum, which means setting aside about $350,000 to take care of the $18,000 yearly essential spending and $10,000 yearly discretionary spending from 54 to 65 years old.

But I think J has enough assets to provide income if he is immediately unemployed for 40 years. If he experiences favourable inflation and market returns, perhaps 50-60 years.

We can carve out $700,000 to provide an income of nearly $19,600 yearly to address the need for $18,000 yearly spending on essential spending. Separately, $250,000 is earmarked to generate between $5,000 to $10,000 yearly depending on market performance for discretionary expenses.

The split is due to the nature of spending needs.

Most people are flexible with their spending but how flexible can you be so that you would not compromise the life of your portfolio? Can you reduce your income by 20%, 30%, 40% or 50%? How would that improve the sustainability of the portfolio?

The truth is that it is difficult to figure that out. By separating the flexible portion, we at least can compartmentalize how much flexibility and inflexibility we have.

In J’s plan, the CPF LIFE annuity income acts more as buffer to supplement his spending in the later years to make the plan more robust.

Most likely, the additional income is ideal to pay for future annual healthcare cost and insurance premiums.

On His Parent’s Medical Needs

J’s parents are in their 80s and while they are healthy, experience tells us things can go downhill quickly.

J doesn’t have a figure because he does not know how to support his parents. They have their CPF income from the old RSS scheme, and their own savings and they are private about their situation.

So the best way is to provide out a sum of money in case we need it.

What can $116,737 do?

A whole lot.

Is not everything but it can buy a bunch of stuff.

J can reference my personal post about how much a potential critical illness event can cost to measure if this amount is enough: $50,000 Portfolio to Supplement Lifetime Critical Illness Coverage.

Finding Some Sensible Job Will Greatly Secure His Family’s Situation

Sometimes, I find it absurd that if you have $2.1 million in net wealth and both spouses are able-bodied, we cannot have some sort of financial security.

I see enough job postings for full-time retail services staff that earns a gross $3,000 a month in income.

In J’s situation, any of these jobs is enough to provide security.

This is because the majority of his financial goals are well-funded.

If he doesn’t want to stop working, then most jobs improve his situation.

Conclusion

I feel that Financial Security is a lifestyle scheme or a type of F.I that many of us cannot explain well if asked but what many are looking for.

And for my reader, financial security became important as his tenure in the company became challenging.

You don’t always need to yearn for retirement to pursue F.I. Most people yearn for some sort of security whether you admit or not.

Given what he has and what he is looking for, my reader has enough financial security but the question is whether he can satisfy the majority of his goals.

There is also some subtle slack in his spending if we are willing to dig.

If the job is uncertain, perhaps it is time to start interviewing before they officially retrench you.

There are some goals in J’s plan that he would seriously need to weigh, especially the $500,000 tertiary education. If life is so hard, do you wish to compromise that?

(Let me know if you have interesting case studies like this, and are comfortable to share publically.)

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- The Cheapest Way to Extend Your Laptop to TWODisplay that I Can Find. - April 29, 2024

- My Quick Thoughts on the Net Cash, 4% Yielding Boustead. - April 28, 2024

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

honest_me

Monday 10th of July 2023

One possible reason for that high networth could be a winner from the crypto bull run during the 2019-2021. Perhaps he managed to gather 10X during that run.