My CEO Christopher Tan sat down with my colleague Jin to deconstruct his latest article that appeared in Business Times called How to make life decisions.

You can view the vid here:

Chris and Jin touch upon a few points that I think many readers will appreciate. The central theme surrounds the topic of Enough and Ikigai. We should make life decisions before financial decisions most of the time but can we wisely make good decisions?

This has always been something that interests Chris and he explains in this interview how he got interested in understanding Ikigai deeper. So much so that he is now a certified Ikigai coach. Chris recently conducted a half-day workshop for us.

He will say we are his guinea pig, but I told him that many would resonate with the true concept of Ikigai because it would not be a bridge too far for most people.

Ikigai is the second part of the show, but the first part focuses upon the philosophy of sufficiency, or what is enough?

If you do not know, the philosophy of sufficiency is the anchor of everything we do at Providend.

It is central to whether prospects lean closer to someone we can serve better. Whatever framework or stuff I structure at work, I got to check against that philosophy as well.

But enough can be… a subjective concept to comprehend on a deep enough level.

Chris shared that some Providend staff also asked him how to define what is enough.

This is how he puts it:

Enough is not something that can be defined concretely. It is influenced by your mindset of contentment. You know you cannot have everything, but as long as you have those things that are important to you, then it is enough.

What are those things that are important?

That, accordingly to Chris is what we called life decisions. Life decisions are also Ikigai decisions.

You might identify with this definition or that you find it still very abstract.

I think enough is a personal state of mind than just numbers.

This may be what fxxk enough people up.

You may find it befuddling why someone with $28 million question whether he or she has enough but that is because you are imprinting your lifestyle against that $28 million. Technically, that person with the money may have enough but he won’t feel that he has enough if a few “conditions” are achieved.

I would like to believe that I understand the concepts about philosophy of sufficiency, making life decisions before financial decisions well.

Hell, most who are serious on the F.I. path would have to deal with this stuff at some point. But understand them deep enough is another thing. Whether we all practice the concepts well is also another thing.

While I accept that enough and sufficiency are mostly about intangible things, the numbers part of enough/sufficiency I feel is critical enough as well.

I struggled with the concept of “Enough” Returns

For the longest time, I struggled to make sense of the concept of having enough returns in the philosophy of sufficiency.

If we practice the philosophy of sufficiency in our own financial planning, we seek just enough returns to help us achieve our goals.

The contrast to just earning enough returns is to maximise returns.

We may observe more people practising investment or punting strategies and conclude that their goal is to maximise returns.

But I struggle with understanding what does enough returns mean.

I would like to think that in the spectrum of people that understand returns and investing, I would lean closer to the folks who understood it slightly better.

But how the f do we earn enough returns?

And not overshoot the point of enough returns? If I overshoot, then I would be branded in the camp of trying to maximise returns.

If We Are Able to Find that Investment Holy Grail, I Won’t Struggle With Enough Returns

Suppose I found the perfect investment instrument which is an instrument that gives me 7% a year.

Regardless when I sell the investments, I can get a compounded return of 7% a year.

In finance-speak, this perfect investment instrument does not have any volatility in its value.

With such an instrument, I won’t have much problems with my planning.

If I work the numbers and deem that I need $1.25 million to be “enough” for my needs, and I have $X today and can put away $Y every year and increase at 3-4% over time, I know where my cut-off is.

The greatest benefit is that I won’t overwork myself.

Actual Realized Return Can Be Far from Sound and Sensible Planning Returns

We know that the perfect investment instrument does not exist.

Whether it is bonds, equities, commodities or properties the returns are uncertain and volatile. Even cash returns are volatile.

If returns are volatile, then how do we deem to just have “enough” returns to abide for a philosophy of sufficiency?

Chris mentioned in the video that we should have a sound investment strategy backed by enough empirical evidence and implemented with sound financial instruments.

The thing is… even with that, returns exist in a spectrum.

Suppose we implement a sound, evidenced-based investment strategy with sound equity and bond funds. With the evidence of history, we can use a planning return of 7% p.a. if we are investing in a 100% equity portfolio.

Let us assume that whichever strategy I implement, the strategy is sound enough.

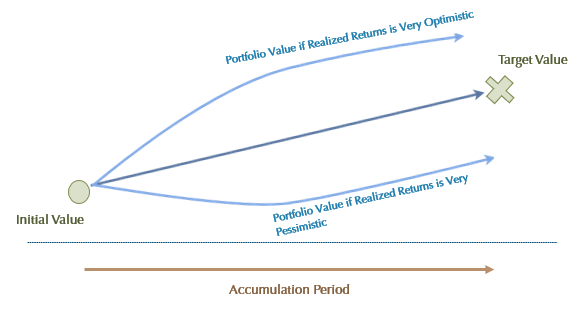

The right way to frame how the value of your portfolio will grow is to visualize it as a cone, like the one below:

I can use a sound, evidence-backed return of 7% p.a. and that will reach the cross or target value. But when I say returns are 7% p.a for the next 20 years, there is every chance that I will earn a compounded return of 11% p.a. for the next 20 years.

This also means there is every chance I will earn a compounded return of 4% p.a. for the next 20 years.

And whether it is 11% or 4% p.a., the planning return of 7% p.a. is sound. 4% or 11% is to be expected. You cannot say that my planning return is unsound.

This framing is what I feel many people struggle with.

Even if your time horizon is long enough (like 30 years or 40 years), the returns we expect is still… a range.

It is not one number.

But How We Perceive Returns May be Critical In Our Life Planning

Many people feel that returns are the most important thing in financial planning so much so that returns will make and break their life goals.

I felt that the so call returns maximizers, like what Chris talked about in the interview, are very misunderstood.

The returns we all want are the returns that we think is “enough” for us to meet our financial goals.

Yes, there are greedy people around.

But most feel that without the returns in their mind, they don’t have “enough” returns.

I mean, I can make a case that those who take risk and try to earn a high return of “5% p.a.” are profit maximizers. You pushed yourself to take on more risk to be in a 40% equity 60% bond portfolio because you are greedy.

But how we perceived returns, affect our degree of enough.

Suppose there is this person that comes to find Kyith.

He has $30 million dollar.

He wants to know from Kyith how much is enough for him to live off. This person think that $30 million is more than enough to live off and should have excess.

He has a grand goal for the excess money.

Just like billionaire Chuck Feeney, he wants to spend his life giving away all the excess money, aside from the amount he needs.

He wants a good answer how much he should set aside, for his needs (let us say his needs are well thought out). What is his enough point?

We can use a return to determine how much he set aside so that he can give away the rest.

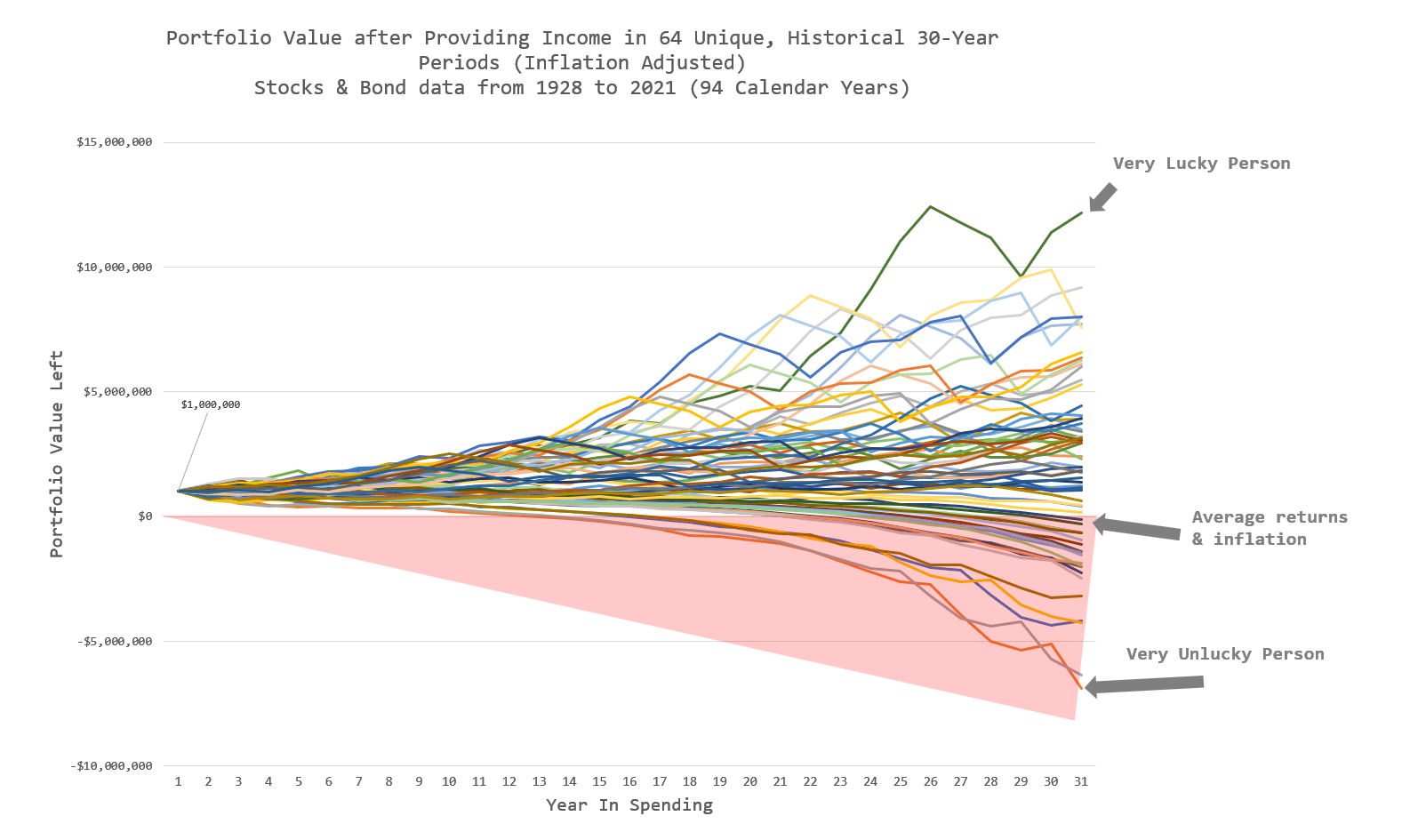

But if returns is a spectrum, then what if he is unlucky? How unlucky could he be?

He has or has given away the rest of his money already!

We could have used a strategy that centers around a sound return, for a person in the accumulation stage, or a person spending down the money, but may live them not having enough eventually.

A good illustration of the spectrum of outcome during spending down may be the illustration below:

We don’t know what the future will be, whether we are going to be lucky or unlucky.

The perception over returns, will affect your decision, or planning recommendation, which can have a critical effect on our lives.

Where I Think True Financial “Enoughness” Lies

The technical or financial aspect of knowing your enoughness is something that has been on my mind for quite a while not just for my personal planning but because I think understanding well help us craft the most sound and appropriate planning solution for our clients.

And this is where I think I differ in my interpretation over a particular aspect about the philosophy of sufficiency.

True financial enoughness is to severely reduce, to the extent of trying hard to eliminate the effect of returns on your overall plan.

The uncomfortable truth is that you need to be rich enough to really have enough.

A rich person have $100 million but suppose his “modest” lifestyle is equivalent to 0.5% of his $100 million. That is $1 million annually.

Now, lets say this rich person err in his allocation and put a large portion of his portfolio in risky investments. In the first year, it resulted in his $100 million being left with $30 million or a loss of 70%.

If you take $1 mil / $30 mil, it is still 3%.

His income stream becomes more risky, but based on the safe withdrawal rate methodology, in the grand scheme of things, his plan still leans towards being safer, even after such a catastrophic financial deployment disaster.

In most situations, even a fall of 40% still doesn’t affect this rich man’s plan.

You may tell me: “Kyith, spending 0.5% of your portfolio is absurd. How many of us can do that?”

Not many, but if you want true sufficiency, the hard truth may be that you need a lot of money.

This translates into different forms:

- I previously shared that I use a 2% initial withdrawal rate to plan for how much portfolio capital I need for the spending that I am most concerned about ( You can read my personal planning notes here and here). I could have used 2.5% like what I advocate for the income duration, but the lower you go down, the more you eliminate the effect of returns on the success of your plan.

- I once heard in my Telegram group, people would only retire if they have 2 or 3 times their spending in dividend income. I am not sure whether there are empirical evidence to using that absolute 2 or 3 times dividend income figure, but by adopting that plan, it also severely reduce the effect of returns (which is capital gain and dividend income variability) from the plan. The plan leans closer to safe than reckless.

My Last Word

Personally, I struggled with how much enough returns should feature in the concept of sufficiency because of the way returns tend to be in reality.

Planning for just about the right returns is very challenging in reality.

But I don’t know. That is how I interpret and understand things. Perhaps, luckily, more people are enlightened enough to run into the same conceptual and application struggles.

I do think that having enough is not elusive.

I find this part of what Chris shared to be the most important:

It is influenced by your mindset of contentment. You know you cannot have everything, but as long as you have those things that are important to you, then it is enough.

Too many people felt that needing so much is “modest”.

The people who can be more reflective, and intentional about what is really important, can technically have enough, even though they don’t have the traditional high paying job, or the kind of $5 million net wealth I mention previously.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- The Cheapest Way to Extend Your Laptop to TWODisplay that I Can Find. - April 29, 2024

- My Quick Thoughts on the Net Cash, 4% Yielding Boustead. - April 28, 2024

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

Jan

Saturday 3rd of February 2024

Kyith, I like the content of the various articles that you wrote but it will be great if it can be more succinct :)

Kyith

Sunday 4th of February 2024

Hi Jan, thanks for the comment. So in this article, where do you think is the part that I can be more succint?

lim

Saturday 3rd of February 2024

I fully agree with Chris, though the concept of 'enough' is nothing new - eg: its featured in Morgan Housell's Book.

Contentment is a mindset, but there is another mindset that may affect your ability to feel content, and that is one of the "worrying" mindset (I'm sure self-help books have a better term).

I suspect that is where ideas like "I once heard in my Telegram group, people would only retire if they have 2 or 3 times their spending in dividend income." This suggests that such people have the "worrying mindset" so they need an enormous margin of safety. As a result they end up "spending too little for their own good", to quote the Tree of Prosperity blogpost. On the negative side, its possible that such people also hoard their money and do not give generously to charity.

And this is the crucial point - if you feel you have enough, you will have no problems giving regularly to charity so that others can benefit.

I actually heard Chris speak at a charity function sometime back talking about his purpose-driven version of FIRE - It's great that he is supporting charities too and talking about shifting the FIRE mindset from a 'selfish' mindset to one that talks about having enough and thereby freeing you to give to others!

Kyith

Sunday 4th of February 2024

Hi lim, thanks for your points. I think I have no issue with what you said but that the crux is that many would know their point of enough. It is just that the way returns work, each of us have different degree of confidence if our eventual plan, will give us the income, for the period we need. If we are less firm about whether that willwork, we tend to hoard. I mean... you cannot fault the person who needs 2 to 3 times the spending income if the $20,000 a year income can easily be cut to $10,000 a year and he needs ALL of it isn't it? He would also want a piece of mind right? I think if most have an income stream like the income holy grail that I describe, they would have less of this because they fully trust the income is enough.

But with the range of outcomes we can get, a lot of people cannot trust the income stream.

The safe withdrawal rate is borned to solve this problem.