Seems the prediction is shaping up really well.

After Astrea IV 10 year 4.35% and Temasek 5 year 2.70% bonds, SIA followed their cue to release a retail tranche for their just announced bond issue.

SIA will be releasing $500 mil worth of bonds, with the public being allocated $300 mil out of this and the rest going to institutional investors. Should the bond be oversubscribed, they will expand it up to $750 mil.

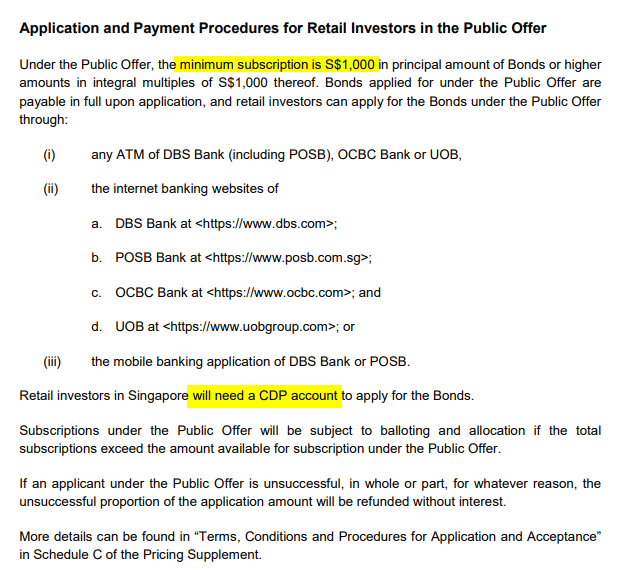

The minimum denomination is $1,000 which makes it affordable for most people. And you can apply it at your ATM or through internet banking like an initial public offering (IPO)

A low denomination will also allow you the retail investor to diversify their bond allocation.

The bond pays a coupon of 3.03% semi annually. At the end of 5 years, you get back your principal.

If SIA cannot pay the coupon, or the principal, they default on your bond. Then you will go through the same liquidation procedures that the Hyflux creditors are doing right now.

What you need to do is to access the ability for SIA to pay the interest on their debts.

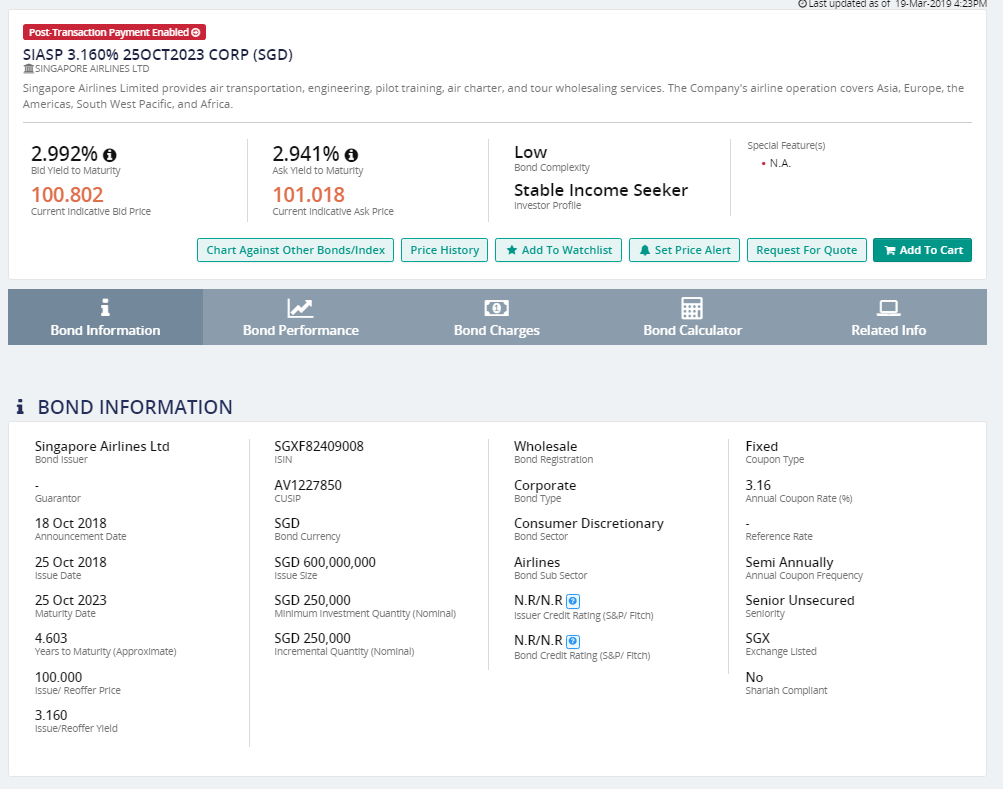

SIA issued $600 mil worth of bonds last year at a yield pretty similar to the current one. That bond is not rated, and while it is not stated, I do assume that this bond is also not rated. This bond, issued in 2018, currently trades at 2.99%, which is not too far off this issue.

The yield is hardly exciting and perhaps a reflection of the credit worthiness of the issuer. This yield is slightly higher than last year’s hot Temasek 5 year 2.70% bond.

For reference, the yield on the 10 year SGS bond is 2.10% and the 5 year SGS bond is around 1.99%.

Still, maybe it is a good idea to take a look at SIA’s financials.

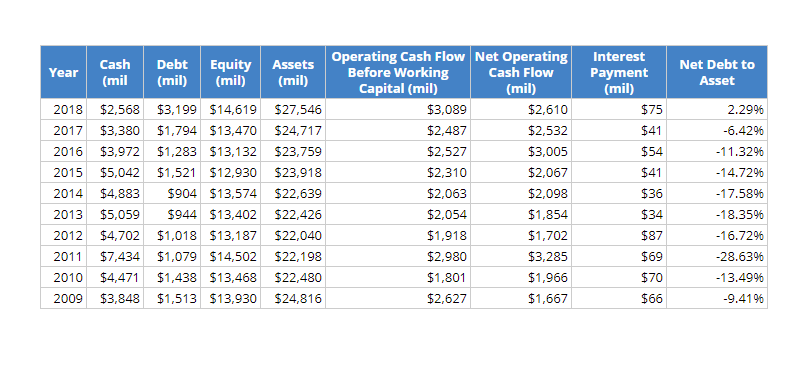

The following is some selected 10 year financial data that I have tallied:

Instead of profit or free cash flow, I decided to tally the operating cash flow before working capital, and net operating cash flow. Since we are purchasing a bond, which is a debt instrument, the company SIA has an obligation to pay the coupon or interest payment before they think of what they would do with the excess money, be it pay a dividend, reinvest in their business or retain it as cash. (to learn more about the different kind of cash flow, you can read my cash flow guide here)

Instead of profit or free cash flow, I decided to tally the operating cash flow before working capital, and net operating cash flow. Since we are purchasing a bond, which is a debt instrument, the company SIA has an obligation to pay the coupon or interest payment before they think of what they would do with the excess money, be it pay a dividend, reinvest in their business or retain it as cash. (to learn more about the different kind of cash flow, you can read my cash flow guide here)

We observe the operating cash flow before working capital and net operating cash flow to be many many times the interest payment on debt.

The net debt to asset also showed that in the past 10 years, SIA have been in net cash position (cash more than debt). However, this has been deteriorating. SIA is now in net debt position.

However, the level of debt is still very very low.

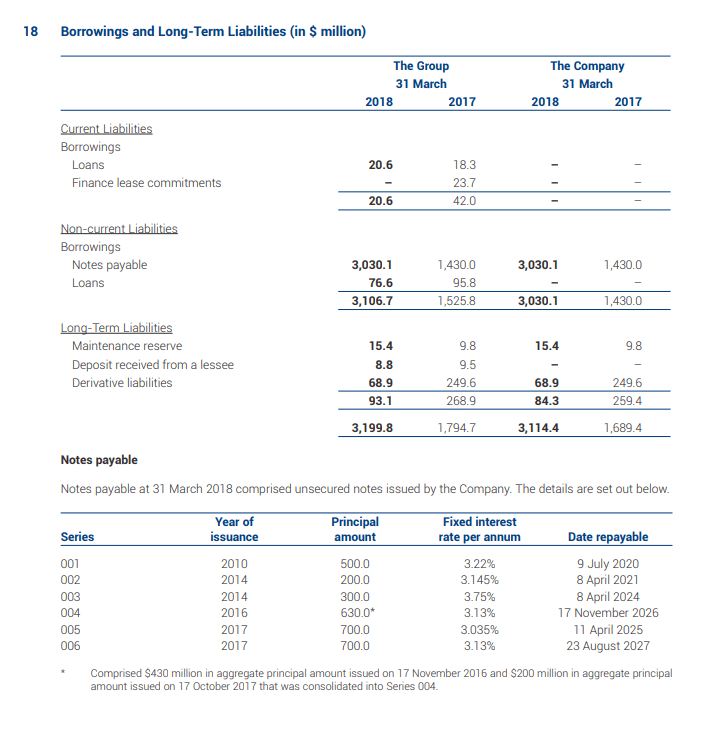

The illustration above shows the latest debt schedule for SIA currently. There are not much bank loans and majority are bond issues in the past.

The illustration above shows the latest debt schedule for SIA currently. There are not much bank loans and majority are bond issues in the past.

2 bond issues are coming due in 2020 and 2021, and it might be the case this issue is used to refinance one of the loans expiring in 2020.

6 days prior, SIA have announced that they have set up a $2 billion medium term bond program, which will be used to refinance existing borrowings, finance investments and fixed assets and for general working capital purposes.

Their financial position looks strong enough to pay the coupon payment. (If you want to compare this to Hyflux’s historical financial strength prior to their perpetual issue, you can take a look at this analysis that I did not long ago)

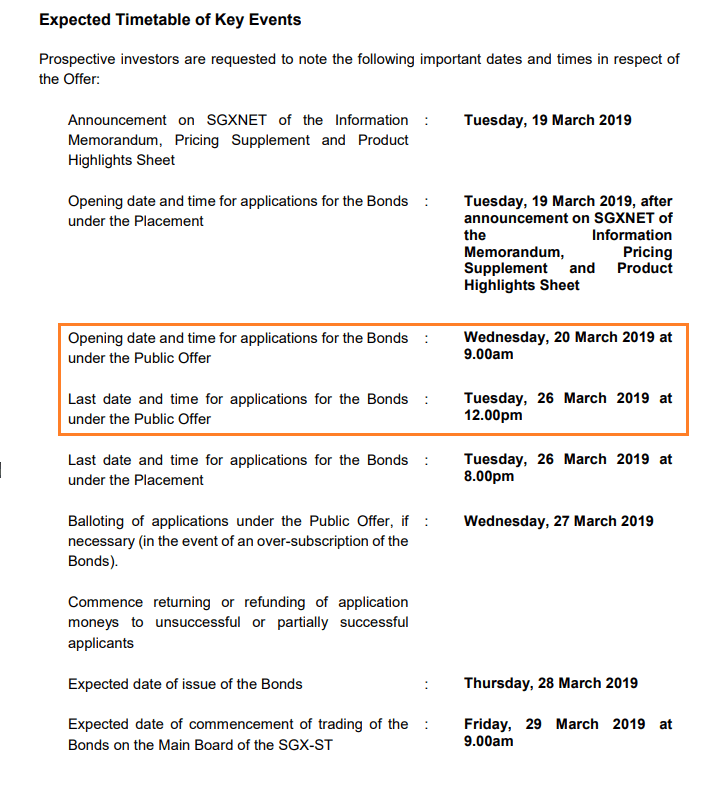

The following is the time table:

Do note the application is open from tomorrow 9 am (20th March) till 26 March 12 pm.

Do note the application is open from tomorrow 9 am (20th March) till 26 March 12 pm.

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- The Cheapest Way to Extend Your Laptop to TWODisplay that I Can Find. - April 29, 2024

- My Quick Thoughts on the Net Cash, 4% Yielding Boustead. - April 28, 2024

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

Angus

Sunday 24th of March 2019

Hi Kyith,

I am looking at the 2018 Financial report for SIA. How did you derive Assets= $27,546 on page 97. Can enlighten me.

Henry

Sunday 24th of March 2019

The ratings of bonds is just a guide. Who rates them? How reliable are the ratings? Most of the mortage backed bonds in the USA back in 2000 were also rated and by 2008, things started to unravel, rated or not.

Credit worthiness is primarily based on past and projected cashflows. Many things can change over the course of the bond's life. Cold comfort if there is legal recourse. Would a retail investor with half, a quarter or 1/10 of a million invested, spend legal fees to attempt recovery?

Trying to gather a group large enough of investors with each a $100K or so to seek repayment is akin to getting agreement on en en bloc sale.

Being a money lender is not so easy. Terms are dictated by the borrower. Issuing bonds by a business is much easier than issuing shares or borrowing from banks. Banks need collateral. Issuing bonds just needs the bank to market it. ( The bank gets a nice fee though ).

If buying $10K worth of SIA shares cause high anxiety, can $10K worth of bonds create peace of mind?

Kyith

Sunday 24th of March 2019

Hi Henry that is alot of questions. some that i agree. i think i would have a piece of mind if i am diversified enough.

Nicholas

Saturday 23rd of March 2019

May I know is Astrea IV 10 year 4.35% and Temasek 5 year 2.70% bonds, also are unsecured bonds ? Compare the 3 bonds, is it advisable to buy SIA bond?( which has 3.03% compare to Temasek 5 year 2.70% bonds,)

Kyith

Saturday 23rd of March 2019

Hi Nicholas, the Astrea IV is a structured product but rated as A, the Temasek bond is also rated. This SIA bond is not.

lim

Saturday 23rd of March 2019

Thanks for the writeup. Always good to be able to point people to some good and sound analysis because inevitably some people always try to spread fear on the internet and claim this will be like Hyflux.

Unfortunately, despite their best attempts, this is probably going to be oversubscribed and will trade above face value so one can exit in the short run at any time with a profit.

Kyith

Saturday 23rd of March 2019

Thanks Lim. Apparently a lot think it will be like this

Retired Uncle

Wednesday 20th of March 2019

Do take note, this bond is an Unsecured Bond and not a Secured Bond mentioned in the new earlier. If anything goes wrong within the next 5 years, it will be like Hyflux. Do read the risks in the prospectus thoroughly. Below extracted from the prospectus. The Bonds constitute unsecured obligations of the Issuer. Accordingly, on a winding-up of the Issuer at any time prior to maturity of any Bonds, the Bondholders will not have recourse to any specific assets of the Issuer and its subsidiaries and/or associated companies (if any) as security for outstanding payment or other obligations under the Bonds and/or Coupons owed to the Bondholders and there can be no assurance that there would be sufficient value in the assets of the Issuer after meeting all claims ranking ahead of the Bonds, to discharge all outstanding payment and other obligations under the Bonds and/or Coupons owed to the Bondholders.

Kyith

Wednesday 20th of March 2019

You could say that about all unsecured debts.

Kopisoh

Wednesday 20th of March 2019

There is a question in the FAQ section of their webpage about negative pledge. Means they cannot use all their aircraft as security? At most they can sell their planes to pay?

The terms and conditions of the Bonds contain a negative pledge clause which restricts SIA from creating or having any security outstanding over its assets so long as any Bonds remain outstanding, unless, amongst other things, the security falls within any one of the following exceptions: any security that was already existing as at the date of the establishment of the Programme and was disclosed to the trustee prior to the establishment of the Programme; any security arising solely by operation of law; any security created over any fixed asset acquired by SIA after the date of establishment of the Programme for the sole purpose of financing the acquisition of that fixed asset; any security created over any asset to secure any of SIA’s indebtedness provided that, the aggregate amount of assets (excluding right-of-use assets) securing such indebtedness does not exceed 33 per cent of SIA’s total fixed assets; and any other security created or outstanding over any fixed asset approved at a bondholder meeting.

For the avoidance of doubt, if SIA wants to create security under limb (iv) above, SIA will have to perform certain calculations to ascertain whether the limit set out in limb (iv) has been reached. The 33 per cent. limit does not apply if the security to be created by SIA is intended to be created under limbs (i), (ii) and (iii) above.