For the first time, Temasek Holding is making available its least risky, private equity bond to retail investors like yourself.

As of 6th Jun, the interest yield for Class A-1 is a yield of 4.35% for 10 years, callable in 5 years.

According to Ho Ching, Temasek CEO, this is to help supplement your retirement income.

This is not the first time corporate Singapore decide to come out with a low denominated bond so that common folks like myself can easily invest, without breaking the bank. For those who are unaware, bonds or debt instruments from organizations, corporate are typically denominated in $250,000. This makes it unavailable to a lot of wealth builders like yourself.

Even if you can afford the bond, you cannot be well diversified. Thus bond unit trust, and in recent years bond exchange traded funds like the ABF Bond Fund became more popular.

This public issue is denominated in S$1,000 and the minimum to subscribe is S$2,000. So its very manageable. It reminds me of the Capitaland Mall Retail Bond issue some years ago.

Bonds, compared to stocks or equity, are less volatile, and when you have them as part of your portfolio or net worth, allows you to sleep better at night.

This article will furnish you some details and does not sought to tell you to buy or don’t buy.

The opinion portion will be kept to this section and I won’t go into detail. The rest of the article are just some numbers and information.

There are much conspiracy to whether Temasek is running out of money, thus they are raising money this way.

They are raising a portion of S$242 mil from the retail investors like yourself. Remember that the recent few months Singapore Savings Bonds have been oversubscribed. The size of the Singapore Savings Bonds subscription is likely more than this amount.

If Temasek have problems raising less than 242 mil, then we should all be really worried.

Raising money from the retail crowd is longer compared to institutional investors, so I felt that what Temasek is doing, is that they are again trying to take the lead and get more corporate to explore issuing part of their bond tranches to retail investors.

This would be able to provide more invest-able instruments for retail investors to build wealth with less volatility.

My gripe for this issue is that why is there a difference in interest between the Class A-1 bond and Class A-2 bonds, since they are the same seniority?

Are the retail investors short changed by minimizing the interest yield compare to the institutional investors?

There are also reservations about the riskiness of bonds issued by private equity.

If Temasek would like to set a precedence, they could very well issue bonds directly, in smaller denominations. They should be more safe.

However, my opinion is that because they are more safe, their bond yield might be lower, and less popular.

The Astrea IV PE Bond

Temasek subsidiary Azalea Group have made available a portion of the S$242 mil worth of Astrea IV Class A-1 Retail Bond for the retail public to be invested.

There are other classes of the same Astrea IV bonds but those are not available to the retail investors. In total Azalea plans to rase a total of US$500 mil from this bond issuance.

There are 3 classes:

- Class A-1 (SGD): Highest Rank and Highest Priority of Payment. This is the one available to the public

- Class A-2 (USD): Same ranking in seniority as Class A-1 and Second in Priority of payment

- Class B (USD): Lower ranking, more risky and lower priority in payment

The interest yield for the different classes is as follows:

- Class A-1:

4.625%4.35% (this is the one available to retail investors) - Class A-2:

5.625%5.50% - Class B:

7.00%6.75%

Note: As of writing, the bond yield might change which should be firmed up after 5th Jun and around 6th Jun. The yield would be changed due to demand.

Update: Interest is now amended to the fixed rate.

The credit rating of the different classes of bonds are as follows:

The maturity date of the class A-1 bond is 2028, or 10 years later.

The min denomination is in S$1,000. There are 2 other class of bonds (A-2 and B-1) but they are not available to the retail investors.

To subscribe by the public, the minimum amount is S$2,000.

The Class A-1 Bond is Callable after 5 years. This means that from year 1 to 5, Azalea cannot buy back the principal of this Class A-1 bond. After year 5, which is in 2023, Azalea can recall or buy back the principal, return you the money.

The call redemption requires certain stipulations for it to happen. For one, it requires a certain Reserve to be funded first by the funds cash flow payment. Once this Reserve is built up to the amount required to redeem Class A-1, then they can call for a redemption.

In the event the bond is not redeem, after 2023, there will be a step up interest of XX%.

The Time Table

The window for bond issues, unlike rights issues for REITs is rather small.

So let me see if I can list out.

- Offer Period for Public Tranche: 6 Jun 2018 9 am to 12 Jun 2018 12 pm

- Expected Issue Date: 14 Jun 2018

- Expected Listing Date: On or About 18 Jun 2018

Who is Azalea?

Azalea is in the business of investing in private equity (PE) funds. They are a wholly own subsidiary of Temasek Holdings.

Before 2016 Azalea launch 2 portfolios of PE funds, Astrea I and Astrea II. In 2016, Azalea launched Astrea III, which introduced the first listed notes in Singapore that is backed by PE cash flows.

What are PE and PE funds?

PE are a specific asset class that traditionally not available to retail crowd. They involve holding equity positions in unlisted companies, business, or listed companies that were privatized.

PE funds, are funds managed by managers who specifically holds a portfolio of these privatized or unlisted companies. For example, in 2016, StanChart private equity arm acquired a big stake in Phoon Huat, who you may be familiar with for selling baking stuff and Crystal Jade Culinary Concepts Holding Pte Ltd. PAG Asia Capital acquires stake in SEA-based restaurant chain Paradise Group.

Private equity managers sought to find businesses that are cash flow generating, purchase them with debt or borrowed money, then try to cut cost, improve them, so that they are more cash flow generating.

The end game is usually to sell off these assets as higher value assets, when the fund nears maturity.

The Astrea IV Fund

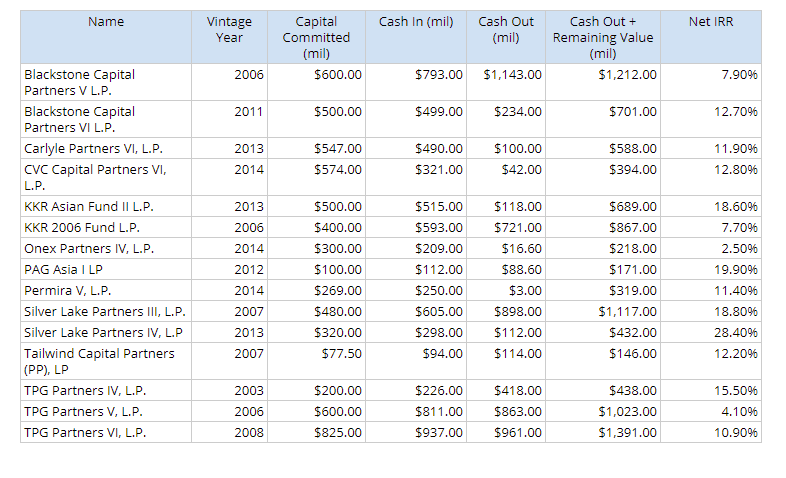

Azalea IV’s portfolio contains 36 fund investments with US$ 1 bil in total net asset value.

Inside these 36 funds, they own a total of 596 investee companies.

The weighted average vintage year is 2011 and the range of vintage years is from 2003 to 2014. What vintage year means is the first influx of investment capital is delivered to a project or company. This marks when capital is contributed by venture capital, a private equity fund or a partnership drawing down from its investors.

Seems these are not new funds. However, the majority are in 2011 to 2014.

There should be an exit date for some of these private equity funds. The reason why some fund in 2003 have not exit might mean that their returns are not up to par of the funds target and are still in the process of waiting for the value to realize.

The following are the 36 funds that make up Astrea IV fund:

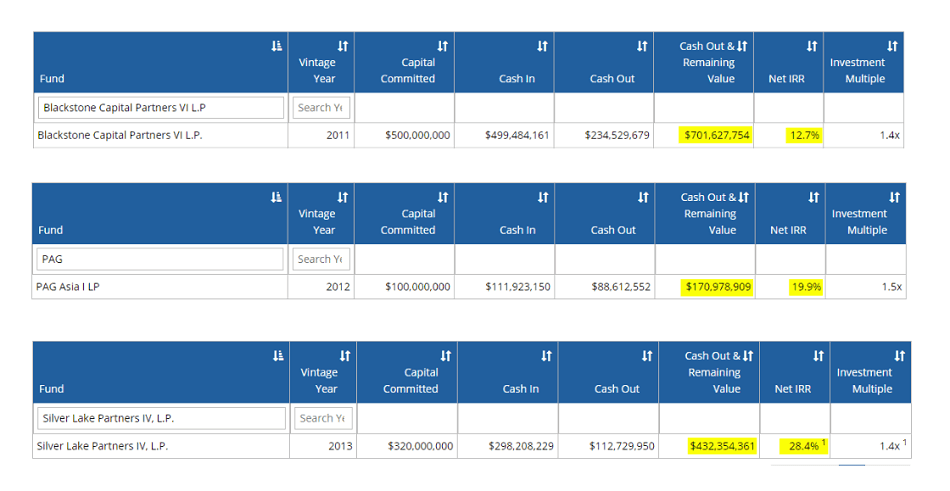

There are a lot of funds in US and Europe and the most concentrated are 9.1% in Blackstone Capital Partners IV, 6.6% in PAG Asia I, 6.4% in Silver Lake Partners IV.

Majority is made up of Buyout funds, which means the funds acquire a controlling stake in the underlying business and try to improve the results through cost cutting, streamlining processes, introducing to new markets, new partners.

14 out of the 36 funds are more than 10 years old.

There is a higher concentration in Information Technology and Energy companies.

Let’s Take a Look at Some of the Funds Returns

California Public Employees’ Retirement System or CalPERS is one of the largest pension funds in the world, and it seems, they are invested in many private equity funds like this.

So they provided a wonderful resource for us to hunt down the returns of these funds.

The returns are measured in Internal Rate of Return.

This is like the interest CALPERS investing their cash outflow into these funds over the holding period.

The rest of the definition is as follows:

The longest fund is TPG Partners IV, L.P.

Surprising this fund is doing well with a IRR of 15.5%. From my search it seems the targeted return is between 15-20% IRR.

If we observe, the cash out of $418 mil is pretty close to the cash out & remaining value of $438 mil. This likely means that majority of the return is in the form of cash distribution and the net asset value left if TPG Partners IV is sold is very little.

It might make sense to collect the cash flow from the underlying business.

The 3 Biggest fund:

- Blackstone Capital Partners VI L.P

- PAG Asia I LP

- Silver Lake Partners IV, L.P.

I tried to find the results for IK IV Limited and Warburg Pincus funds but couldn’t as CALPERS was not invested in them.

Some really not bad results, and if we are loaning them money, you wonder who gets the better deal, Temasek or the bond holders.

I think our returns should be measured against the risk taken.

The following are the funds that coincidentally CALPERS are also invested:

What do they mean when they say Astrea IV PE Bonds are backed by Cash Flows?

If you read the prospectus, you will keep seeing that this bond is backed by cash flows but what does it actually mean?

There will be cash from each of these individual private equity funds released to the investors.

Astrea IV is an investor in these 36 funds. When these funds return cash distributions (see the conceptual illustration), Astrea IV will have cash.

These available cash flow will then pay the taxes, expenses, hedge costs, liquidity funding and managerial fees. then they will pay the Class A-1 bond holders (this is where the retail investors are)

If we revisit CALPERS tabulation of their investment in TPG partners IV, Astrea IV oldest investment, we might understand better.

The invested capital is $200 mil. Through the years, the cash distributions, from the underlying business as well as the sale, amounts to $418 mil.

This $418 mil is the total cash out over its lifetime from 2003 to 2017 and not in 1 year.

This will be the cash flow that will pay the interest for your bonds.

But how much is from dividend cash flow of the business and how much is due to one time large distributions from sale of underlying companies or special dividends?

It is hard to find out, but let us look at the younger funds. There are a few that is 2014 which is probably the youngest.

Onex IRR is low at this point. Taking out the cash distribution these past 3 years, the value is still break even. We can see the cash distribution is probably less than the interest proposed.

Permia V did better but its cash out of 3 mil is just 1.2% of committed capital.

It remains to be seen what were the total cash inflow from distributions for Astrea IV and whether it is adequate to pay for the interest that retail investors will earn.

To pay for the Class A-1 bond interest, we would need probably S$242 mil x 0.046 = S$11 mil or US$8.3 mil.

I think it is a manageable sum that they would not default.

Collateralized Fund Obligations is not Without Risks

While it is easy to gloss over and say we had the safest of the stuff, if we have the safest of the risky stuff, then how safe are we?

One area we can learn about this is by reading some analysis of Astrea III, which the Astrea IV is modeled after.

And Fundsupermart have written an analysis titled The Astrea III Bonds Today which would prove a good read on the risk of collaterized fund obligations.

Update: Fundsupermart have written 2 very comprehensive articles on the Astrea IV bonds. You can read it here and here. Urge you guys to read this at least.

Comparison Against Other Bonds

To ascertain whether to invest or not, you need to compare against the risk and reward of other comparable.

The closest is perhaps other retail bonds and government bonds available.

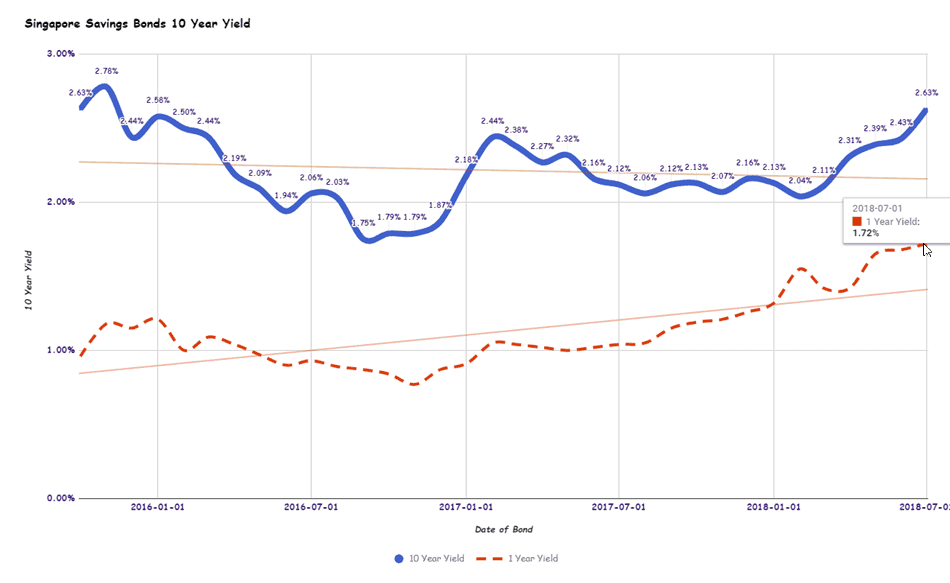

One comparable is the Singapore Savings Bonds. This is a wrapper for Singapore Government Bonds which is AAA rated. The recent July 2018 issue of Singapore Savings Bonds yields 2.63% if you hold it for the same 10 years.

This is perhaps near the risk free rate that you should be comparing against.

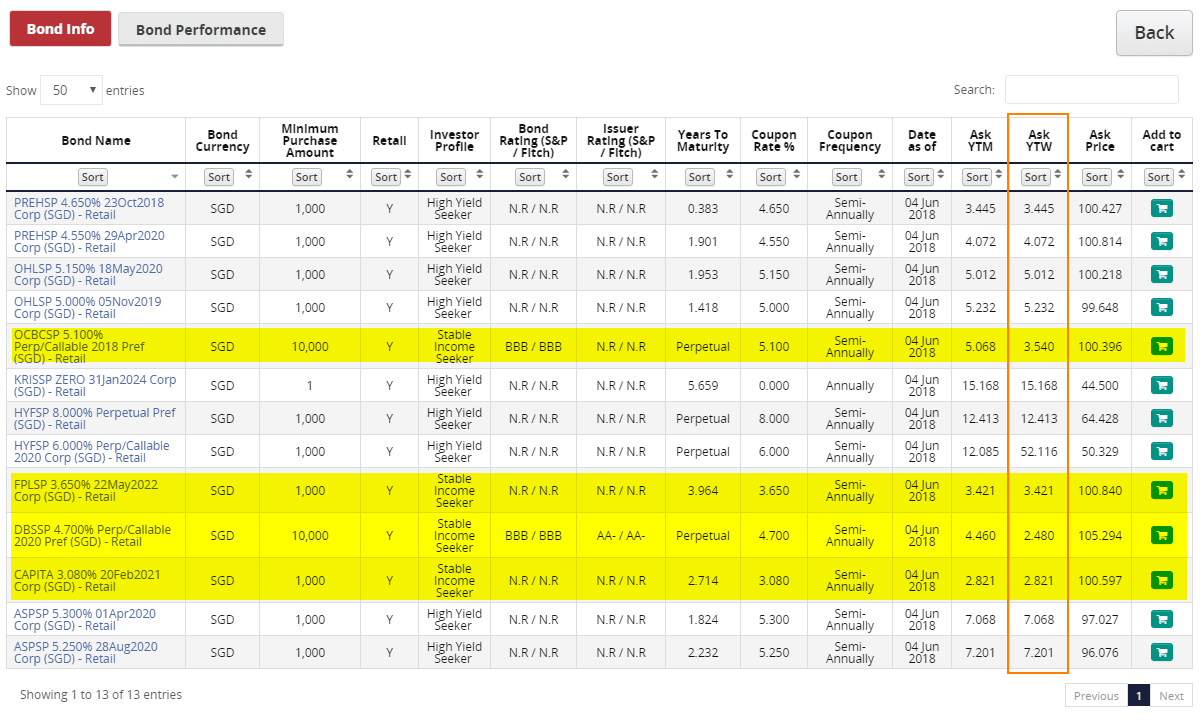

If you go to Fundsupermart.com, and use their bond selector, you can filter by the retail bonds, listed on the SGX that you can get access to and see how they measure up.

Over here, we see them classified into 2 groups, the Stable Income Seeker and the High Yield Seeker. The stable income seeker is a categorization Fundsupermart used to segregate those that are probably from more blue chip companies.

So you see the OCBC perpetual that is callable in 2018, The Frasers Property Limited bond, the DBS perpetual and Capitaland Retail bond. Their yield to worst, which is likely the yield to earliest call is between 2.48% to 3.54%

Other than that you have your more risky corporate bonds. Their yield could be from 3.4% for a Perennial bond to 52% for the Hyflux perpetual which is in the news. Hyflux have cut the recent coupon payment to the perpetual and are exploring some financing options for their main business.

What is the Minimum Amount You Need to Apply?

Since this is a retail bond made available to us, the minimum amount required is S$2,000.

How can We Apply?

You apply just like how you applied for a company that is undergoing initial public offering (IPO)

This can be done by going to the ATM and apply.

Can I Sell Off the Bond If I Need Money?

Azalea IV PE Bond will be listed on the Singapore stock exchange SGX. You can view all the retail bonds under the retail bond section.

You can then buy and of course, sell the Azalea IV PE Bond like how you would do with a normal stock.

Can you use Your CPF Funds to Purchase the Bond?

No you cannot.

Can you use Your SRS Funds to Purchase the Bond?

No you cannot.

To get started with dividend investing, start by bookmarking my Dividend Stock Tracker which shows the prevailing yields of blue chip dividend stocks, utilities, REITs updated nightly.

Make use of the free Stock Portfolio Tracker to track your dividend stock by transactions to show your total returns.

For my best articles on investing, growing money check out the resources section.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

YT

Sunday 12th of August 2018

How do I know if I have successfully subscribed the bonds via atm?

Kyith

Sunday 12th of August 2018

You should be able to check it in your CDP account

Anson

Tuesday 12th of June 2018

Many thanks for the write up. As always, your article is very good & useful.

Jack

Sunday 10th of June 2018

It was really great sharing, thank you so much for the generous sharings and contributions Kyith! As a beginner, may I clarify some doubts:

1. What does it mean by coupon step-up of 1% applies if tenor exceeds five years? Does that mean that we will get 4.35%+1%=5.35% we continue to hold the share after 5 years and all the way to the 10th year?

2.How does the bonus redemption premium of 0.5% work?

3. I don't understand why ASTREA III is generating a lower return of 3.9% for institutional investors than ASTREA IV of 4.35% returns? Does this means that ASTREA III is more stable than ASTREA IV?

4. Since this is a bond, we are not able to auto-reinvest the 4.35% annual interest back?

Bella

Sunday 10th of June 2018

Good report, many thanks! Saves the trouble of reading the entire prospectus.

Sinkie

Thursday 7th of June 2018

Fundsupermart also has a good overview of Astrea IV, especially the fund structures.

The "safety" is not really in this being "Temasek approved" coz if SHTF like in 2008, I doubt if govt will allow taxpayer money to bail this out.

Rather the safety lies in the fund structure of having a starting LTV of only 45%, a STRICT covenant to ensure LTV doesn't exceed 50%, and ongoing building up of reserve deposits to redeem the bonds in 5 yrs.

Basically it's a ABS of USD$500M being backed by USD$1.1B of PE funds.

During a recession when PE fund NAV drops, the reserve deposits help to maintain the 50% LTV. If still not sufficient, then Astrea IV will start selling some of the PE funds to reduce LTV.

Hence the fund structure is such that it is very hard for the bond to blow up unless most of the underlying companies / PE funds go bankrupt or go to zero overnight. E.g. major nuclear war or something similar.

They are bending over backwards for the sake of mom & pop investors.

Kyith

Friday 8th of June 2018

Hi Sinkie, thanks for sharing your thoughts. Could you explain how does the reserve stops the violation of LTV in the even of NAV fall? Is it that because the reserve is part of equity it will limit the fall?

If i am right they might have specifically get a rating for only the Class A-1 tranche from the other rating agency, perhaps just to provide additional assurances.

Sinkie any thoughts why they did this instead of a normal bond?