Back when Temasek’s subsidiary Azalea Group issued the Astrea IV Bonds, I made the guess that the direction the government wants is for wealth building to be more broad based instead of being very concentrated in property and very safe instruments.

To do that, the public requires more options. So when the Astrea IV came out, I think it let’s us know perhaps what is ahead.

Yesterday, it was announced that Temasek will issue a 5 year bond yielding 2.70%.

This Temasek 5 year bond gave us that indication that maybe there are more issues to come.

One of the gripes people have about the Astrea IV was that that the Astrea IV was not issued directly by Temasek but is a structured product by the private equity subsidiary.

So this time round, Temasek decide to provide a retail tranche with a low denomination of $1000 minimum.

The hopes I think, is to create a more liquid market, and for the corporate to follow their lead to issue more retail tranches.

A few friends and family members was asking for my opinion and I thought this is a pretty good issue.

So here are my thoughts.

What is the T2023-S$ Temasek Bond

Temasek will be issuing $400 mil worth of a bond that is 5 years in tenure.

All the information can be found in this website here.

A bond is an IOU.

When you buy a bond, you are essentially lending the money to the issuer. The issuer have an obligation to pay you a coupon, which is your interest.

At the end of the tenure, the borrower (issuer) will pay you back the principal.

Now, like borrowing money to your friend, the friend can delay or stop paying interest to you. The friend can also stop paying you back the principal you lend him.

This is called a default.

So this happens when you lend to institutions as well. Typically, there are rating agencies that group these institutions into various groups based on their credit worthiness.

The T2023-S$ Temasek Bond is issued by Temasek. Temasek is borrowing money from you.

The duration is 5 years.

In return for lending Temasek the money, Temasek is obliged to pay you 2.70% per year, on a semi annual basis, for these 5 years.

The image above shows the details.

There are 2 tranches one for the institutions with a minimum application of S$250,000 and one for the retail investors with a minimum application of S$1,000.

Click to view larger

The timeline above shows you that, upon your investment, you will be paid half yearly. At the end of 5 years you will get your money back.

Here are some more characteristics you need to know about.

1. This is a Public Offer. The way this will go about is that it will be very similar to a Singapore stock IPO. It is a way for a company to raise money via equity (stock) or debt.

The table above shows the time table of the offering events.

Usually bond issues are very fast. So the timetable is also very short. In fact as of today, the offering is open.

You have 6 days till 23rd Oct 12pm to apply.

2. You can apply via ATM or Internet Banking. Like all IPO, you can apply through your OCBC, UOB and DBS ATM or internet banking.

Your shares will be stored in your CDP account, just like Singapore stocks.

3. It does not mean that you will get all. This offering can be rather hot, and Temasek themselves expected it to be rather hot.

So if a lot of people applies, and it becomes oversubscribed, you may not get all that you bid for.

So it might be the case you bid for $3000 and you get only one third of it. Or you might get more.

4. You can buy and sell the bond in the secondary market. Just like a stock, once it is listed and not redeemed, you can buy more of this bond if you like it off the Singapore SGX Exchange.

You can sell it if you wish to redeem it as well.

You can view the other retail bonds listed here.

5. Bond is subjected to interest rate, liquidity and inflation risks. If you held the bond to maturity, your principal is guaranteed. However, there are opportunity costs for tying up your money for 5 years.

If the prevailing interest rate rises in 1 years time, the bonds issued then gives a higher coupon. Would people want your bond?

If you were to sell, it your bond value will need to go down. The opposite is true as well.

Interest rate is often use to combat inflation. And thus if inflation rises, and interest rate goes up, then by holding this bond, you will lose a lot of purchasing power, or opportunity cost.

6. You can subscribe to this with your CPF OA. You can subscribe to this bond with your CPF investment account. Just like stocks, you can only use 35% of your CPF OA for this. You can subscribe with cash, CPF, or partially with both.

You might be able to earn the difference between 2.50% and 2.70%. However, do watch the size you applied for. There are quarterly custodian fees for investing your CPF.

This might negate the spread.

The Financial Stability of the Issuer

There are some who commented that this bond yield is rather low, in a period where the interest rate is rising.

However, you would have to evaluate the bond across a few metric.

The key one being its ability to pay you the interest and principal.

This might be something that you take it for granted. However, in recent years we have instances where investors invest in unrated or lower rating bonds and they couldn’t get back their principal.

- In 2015, oil prices fell, a lot of oil companies was greatly impacted. Those listed companies that issued bonds to investors defaulted on their debt

- In recent times, well known listed firm Hyflux also face problems paying the coupon on their perpetual

In this case, the issuer is AAA by international rating agencies. It is very difficult to get AAA rated and it means the chances of Temasek defaulting on their debt is very very very very low.

I sometimes debate which is safer, putting your money in the bank or these Temasek bonds. For most of us, who have money in DBS Bank, Temasek is the parent of the bank itself.

In the table above, it shows the various financial metrics and they show how well capitalized Temasek is. Net Portfolio Value divided by Total debt shows how low Temasek’s debt is with respect to their assets.

Temasek’s balance sheet is net cash as of now.

Their liquid assets is also 9 times of their total debt.

Whenever you are wondering if investing in this bond issue is a good idea or not, whether your money remains safe is the highest consideration.

The T2023-S$ Bond versus the Competition

All these products make it difficult to compare. It is very difficult to do an apples to apples consideration.

I would say, the bond yield alone is not always the most attractive. There are other close competitors that yield around the same range.

But you have to compare it across a few metrics:

- Lock in Versus No Lock In. There are insurance endowments such as Great Eastern’s 3 year 2.05%/yr last year Sep. The yield looks pretty comparable with the T2023 higher and the T2023 do not have lock in. If you redeemed the endowment plan early, you might lose part of your principal. With the T2023, you can sell it in the market. You may lose part of your principal as well, but you do have an option to liquidate if you need to.

- Hurdles Versus no Hurdles to Jump Through. 2.70% is attractive but if you look at my best short term savings account in 2018 list, you will see some hurdle accounts such as the DBS Multiplier, OCBC 360, UOB One, and BOC Smartsaver account. These accounts may give 2.5% to 3.5% bonus interest which is very attractive. However, to do that, you have to carry out hurdles such as depositing salary into the bank, meet a minimum spending of $500-$700/mth. These may be hurdles you cannot hit

- Capped Maximum Amount. Now for each of these competitors, usually there is a maximum amount you could put in to earn a highest interest. The Singapore Savings Bonds is $100,000, Citibank Maxigain is $150,000, UOB One is $75,000 and DBS Multiplier is $50,000. These are some of the examples. Should you have a larger amount that you wish to not subject to volatility.

- Changes in Terms. A lot of the better yielding accounts that are comparable to the T2023 bond exist in a low interest environment. They are put out to attract deposits. Overtime, as banks have reached their aim, they know that consumers do not switch accounts easily, so they will make the hurdles more difficult, or the interest earned lower. With the T2023, these terms are set in stone and the structure is simple, so you have less of these problems.

Finally, one of the biggest competition would be the Singapore Savings Bonds. It is big because the Singapore Savings Bonds is made up of Singapore Government Bonds, which is also AAA rated.

The table above shows the Nov 2018 issue of the Singapore savings bonds.

If you hold the SSB for 10 years you will earn an average of 2.48%, which is not too far from the Temasek T2023 Bond.

IF we compare the 5 year tenure, the SSB will yield 2.22%. While lower, the advantage of the SSB is that its principal is protected.

You redeem the SSB at the cost price. If you sell the T2023 on the stock exchange, depending on the market price, you might gain/lose money.

The T2023 have an advantage over the SSB in that its 2.70% is paid out uniformly. The SSB interest (see the 2nd row Interest %) is a slow step up.

The table above shows the yield to maturity and yield to call of the retail bonds out there. Notice that only the Azlea IV is rated close to A(sf). A lot of the corporate retail bonds are not rated.

How to make use of the Temasek Bond

With that said, here are some things I thought of that you might want to use this bond with.

1. Use it as a medium term savings for conservative wealth builders. Not everyone have a large appetite for risk. If you have a goal that is about 5 years away, and you need the money then, this and some of its competitors might be ideal for you to park the money.

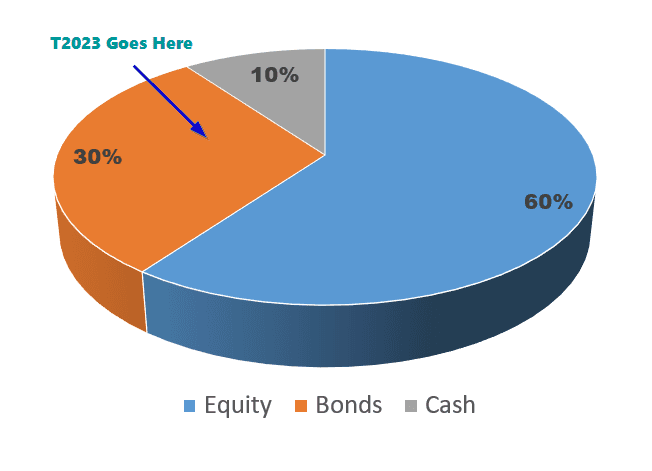

2. Assign this to your bond allocation. If you are a buy and hold investor, you would have fixed up a strategic allocation of equities, bonds and cash.

Your allocation may be something like this:

The T2023 Temasek Bonds would fit into your bond allocation. I do caution that, if you form your allocation with bond funds or bond exchange traded funds, you might wish to keep it simple by relying just on those funds instead of purchasing an individual bond.

3. Slowly Shift to Bond Allocation to De-Risk Your Portfolio. Suppose you held more of a equity heavy, cash/bond low allocation. And you actively manage your equity positions.

Given your outlook on the investing climate, you do forsee that the economy can still go on further. Central banks will raise the interest rates to prevent an overheating economy.

When rates rise, this means your current bond value goes down. At some point, the rate raised will cool the economy. Then the cycle would reverse, and rates will go down.

As the rates go higher, you can shift your equity allocation into bonds.

It might start now with the T2023 Temasek bonds. Then as the rates go higher, and the bonds become cheaper, you purchase more systematically.

In this strategy you can still have exposure to equity, but are de-risking your portfolio systematically by buying the cheaper asset class (bond), selling the more expensive asset class (equity).

When the market turns, and when the interest rate are lowered, the bond value goes up.

Then we rebalance the bonds, by selling bonds like the T2023 Temasek bonds and buy equities with them.

Some Non-Financial Final Thoughts

For those who wish to learn more about this bond, SGX have a free seminar on 19th, 20th and 22th of Oct to explain more about this bond. You can find out more about it here.

I think this issue is not bad.

There are the folks who wonder whether Temasek is running out of money.

The size of this issue is really small.

If they are running out of money, the last person that they would borrow is from the retail investors.

I would think it makes more sense to create a financial structure such as a mandatory private pension system where you are forced to funnel your money into them.

This one is optional. You can choose not to subscribe.

I infer that this issue is more to lead the market to encourage more corporate to take this route to make the retail investing scene more vibrant.

Time will tell whether they are successful or not.

I do think that there won’t be too many of these issues by Temasek.

I generally like this more than the Astrea IV, although the Astrea IV is higher yield, it seems hard to be understood. This one is more straight forward.

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – The Deeper stuff on REIT investing

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Ram

Friday 19th of October 2018

Thanks for the info

Mr Chan

Friday 19th of October 2018

Hello Wrt “I do caution that, if you form your allocation with bond funds or bond exchange traded funds, you might wish to keep it simple by relying just on those funds instead of purchasing an individual bond.”

Individual bond r u referring to example such as Temasek bond?

Y is it a caution not hold both ETF/fund bond n individual bond?

Thanks.

Kyith

Friday 19th of October 2018

Hi Mr Chan, i think the bonds is ok and if you choose, you can hold both an individual bond and a bond fund. My comment is more to advise against holding 2 if you wish to be really aligned to a simplified portfolio. In that case using bond funds would do.