I subscribed to former 1M65 Telegram group member Patrick Teo’s channel CPF Wealth Tree. If you are interested in his thoughts about life and money, you can subscribe to it as well.

Patrick views how life should be lived as we near retirement as that we should be open to working longer. I have no problems with that but the more he explained, I became disconnected from some of the reasons brought up.

I am too tired from work to reason about what I disconnect with (and my views are probably not strong enough).

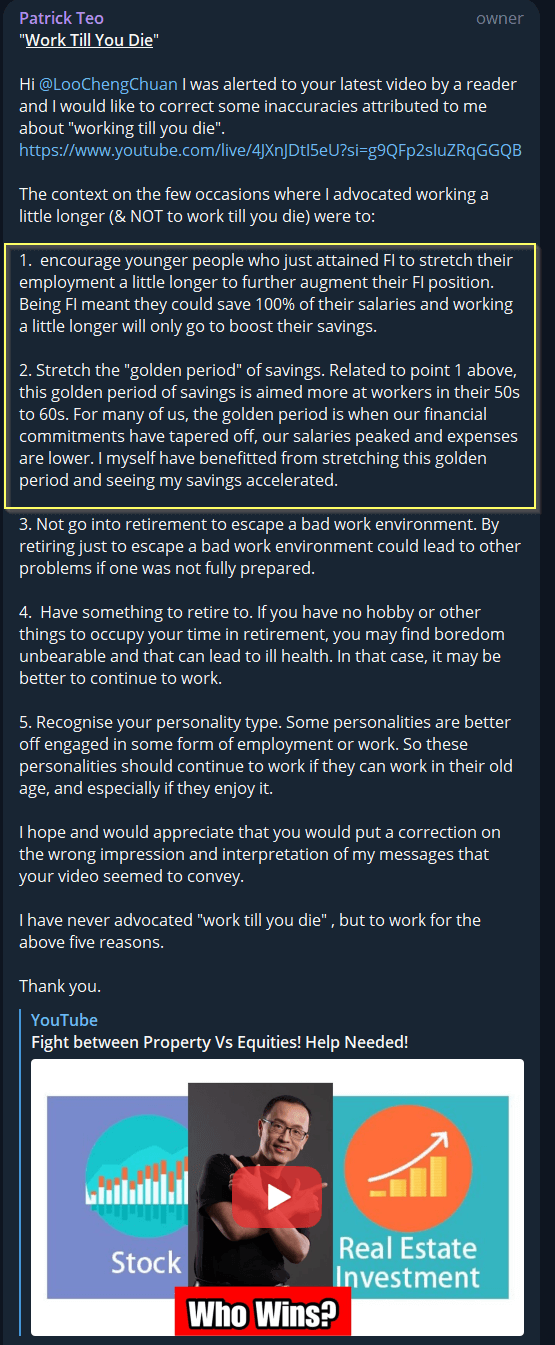

But when I read two of the points Patrick brought up to correct inaccuracies in Mr Loo’s video about Working Till You Die and had stronger thoughts. They are highlighted in yellow:

I cannot understand what it means to say we have reached F.I. status, but we still need to augment our money in FI. If we are already “financially independent”, doesn’t that mean we are independent financially already? So why do we need to augment further?

How much longer do I need to augment my F.I.??? When can I stop augmenting it???

I think in the first place, some of the definitions of what is considered F.I. are not very numbers-driven and that is why we have this need to augment it further.

Think about it.

Suppose Kyith tells you that if you need $120,000 a year in income, and you have a capital that is equivalent to generating 1% in the first year (that’s $12 million), you are financially independent.

And you tell Kyith: “I have $14 million, what does that mean?”

I am going to tell you that you are financially independent.

“Then, Kyith, do I need to continue working to save 100% of my income?”

Of course not!

Unless…

That $12 mil x 1% = $120,000 plan is…. flawed.

Unless…

Accumulating all those financial assets is not the be-all-end-all to financial independence.

To be able to retire, I believe you have to reach a certain state of mental and financial independence, that mentally you know you are REALLY financially okay.

Many aren’t mentally ready because they might not trust that their income model is well-thought-out, or that they cannot connect with the income model that they have chosen, not able to understand certain nuances of the plan that would have given them mental peace of mind.

I have enough people ask me: “Kyith, I am able to have $XXXX annual dividend income that covers my expenses of $YYYY; what do you think?”

We often have to deal with the uncertainty of the markets, and market uncertainty makes people wonder if their plan is robust enough or whether they are missing something that they have not considered. So they look for others for validation, hoping that those who asked would give them good news.

If you need to augment your F.I. numbers further, mentally, you are not F.I. yet, whether its a plan problem or some other problem.

I wish we could be a little more numbers-based when defining F.I. status

Even if you tell me that you need 1.3 times in dividend income compared to your need, or 2 times, or 3 times, at least:

- There is an end to the accumulation.

- We can debate about the robustness.

A lack of robustness in the plan, or understanding of why your plan is safe enough, is what makes your salary so addictive and so hard to wean off.

I have this philosophy:

People over-complicate things.

The richer people have mental peace of mind in their passive income stream because their passive income stream is generated with a vastly larger asset base such that their income stream does not depend on the asset returns at all.

This means the income-to-capital ratio is the most important above anything.

If I need $120,000 and I have $12 million, even if my $12 million gets cut in half (which in their plans should not happen at all due to proper diversification). that income is still 2% of their capital after what the market shaved off, which is still very conservative.

If inflation brings their total income requirement up 50% suddenly (think the rest of us will suffer greatly in that scenario), their income is just 1.5% of their portfolio.

If you respect that ratio, you will get a lot of peace of mind, but you need… more capital.

Different people have different definitions of F.I., which is based on different income model robustness.

I would like to contend that… being financially independent is more than just having a reliable income stream.

There are other areas to take care of such as:

- Sinking fund for your medical goals

- Sinking fund for XXXXX which you held dearly

- The non-financial side of things

If you have not save for those, then it make sense to continue but there should be different numerical degrees to how much you need.

On the second point, if we keep thinking about the opportunity cost lost of good earnings, we will never pull the plug to retire.

But everything links to a quiet problem that Patrick didn’t address clearly: Give me an F.I. number to aim for. Give me a model. 3 times the dividend income I can generate? 4 times? If I reach this number, I can stop accumulating for that goal.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- The Cheapest Way to Extend Your Laptop to TWODisplay that I Can Find. - April 29, 2024

- My Quick Thoughts on the Net Cash, 4% Yielding Boustead. - April 28, 2024

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

Jason

Wednesday 27th of September 2023

The scary part of retirement planning is you never feel that you can plan accurately. And alot of things can change. I'm in my 30s. If I budget strict, yes I can get FI. But my lifestyle has no flexibility to change. Even though I've worked out a nest amount I need for FI. But I don't have faith that it is enough.

I think your approach of quantifying targets should be the basis for planning. It cuts down alot of anxiety & fear of unknown.

Then again, if you dedicated years to achieving FI, could you really just not do anything in retirement?

Kyith

Sunday 1st of October 2023

HI Jason, thanks for your comments. What helped me was going down this route and really thinking hard if I have enough, trying my best to weed out any confirmation bias, or the bias that I have really made it.

As a person doing systems risk management in the past, the first step to think about is: what are all our needs that people know (but maybe I don't) that I need to consider. When we go through them and see how we should have them in our plans... it recalibrate what is readiness.

What is your math parameters when you say that you "can FI"?

lim

Monday 18th of September 2023

I achieved FI in 2021 and I fully appreciate the need for a margin of safety. However, even with the margin of safety achieved, I am totally ok to continue accumulating. I just have to apply my mind to how I want to use my increased wealth. For example, I will use most of the excess for charity work. I may use some for my own benefit as well (I'm not a saint lol), such as business class for short-haul flights (once you are older, business class for long-haul flights is really helpful). If one has no idea how to use wealth that is beyond the FI level+margin of safety, then yes, I can see why one would stop accumulating.

Kyith

Wednesday 20th of September 2023

i think is how one will define what is FI. there are different degrees of FI and if a person do not feel at ease, is it consider FI? How much is the right margin of safety really.

Pugs&Pennies

Monday 18th of September 2023

Hi Kyith, Just wanted to thank you for all your math number crunching. I am building up my healthcare sinking fund and my kids' education fund based on your method. Been following your journey for years. Just wanted to share that we reached an intermediate FI at age 40 for our family. Some of that is based on math info from you, so appreciate it! There's not too many local family based FI info, so I hope to add to what's available at https://pugsandpennies.substack.com

Kyith

Sunday 24th of September 2023

Hi Pugs&Pennies, thank you for your sharing. I try to see but cannot find the post.