NCMP Professor Walter Theseira asked Minister Josephine Teo how much is the average Singapore elderly getting in their CPF payouts after they turned 65 years old

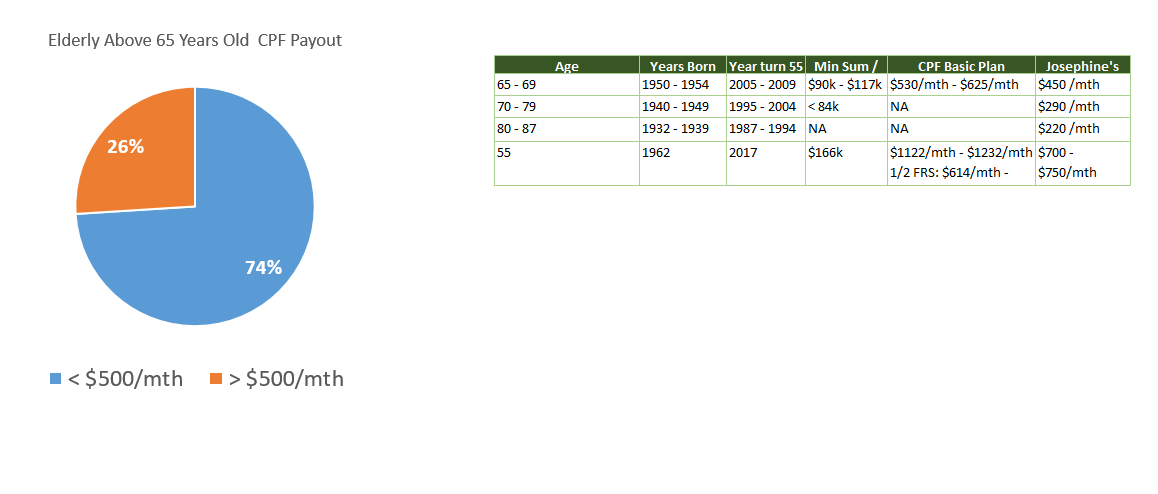

And Josephine Teo replied that 74% had monthly payouts under $500.

That has got to make a good headline. And it is such a good headline that The Online Citizen will need to write about it.

You got to be kidding me if you think I can survive on $500/mth.

Josephine Teo provides further break down on the amount that each elderly age group have gotten:

This looks really poor, and you wonder how the elderly could survive with this amount. That is like $900/mth for 2 person. We will revisit this perhaps later.

I felt that there are some data that is provided by Josephine Teo that was not broken down properly.

Click to view larger illustration!

Josephine Teo updated that of those elderly that received payouts, 74% of them received less than $500/mth in payout. I would assume the rest received greater than $500/mth in payout.

She further provides a breakdown that those 65-69 received $450/mth while those 70-79 received $290/mth and those above received $220/mth.

I provide some corresponding data, including the year these elderly were born, when they turned 55 where they should be committing to their CPF retirement account (RA), the corresponding Minimum sum / Full retirement sum and the estimated CPF payout.

If you are born in 1958 and later, it is mandatory to enrolled in CPF Life, the national annuity income scheme.

If you look at the age of the elderly above age 65, it looks like all of them should be under the old Retirement Sum Scheme, instead of the CPF Life.

What is the difference in terms of yield for CPF Life versus the Retirement Sum Scheme?

The CPF Life is an annuity which means that the resources of the cohort of elderly are pooled together. If someone passes away, the amount would be distributed to the rest of the cohort.

This should increase the payout of the annuity (CPF Life) versus a product that is without this pooling (Retirement Sum Scheme). Thus the income you can get for the same amount when you turn 55 years old should be higher with CPF Life.

However, if I understand correctly, CPF Basic plan, versus CPF Standard plan, should factor in the least when it comes to this pooling concept. This is to say the cash flow performance of CPF Basic, out of the three CPF Life plans (Basic, Standard and Escalating) should match closest to the Retirement Sum Scheme.

For age 65-69 years old, the CPF Life Basic income, computed by the CPF Life estimator is $80-$180/mth higher than the average figures given by Josephine Teo. CPF Life Basic should payout more but not by a lot.

The inference can be that Josephine’s 65-69 year old data shows that they have slightly lower than the minimum sum.

This is not too bad.

I was assuming it to be even lower.

My assumption is for most Singaporeans to pledge their property, so that they only need to satisfy half of minimum sum or the CPF Basic Retirement sum. It seems they have more than that but still less than the minimum sum or the CPF Full Retirement sum.

And this could still be true. If you refer to my conclusions below, I cite one example where a person born in 1954 have a pretty close payout to $450/mth and his minimum sum at age 55 seemed to be half of this minimum sum.

My analysis of this figures seem to point to that those 65-69 cohort satisfy slightly more than half of CPF Minimum Sum at age 55 ($45k to $57k).

Their contribution is meeting up to the government’s expectations.

For those older than that, the payout is much smaller.

The Retirement Sum Scheme is likely both a return on capital (4% interest) and return of capital.

I believe those older, have set aside less than those younger in the amount of CPF Full Retirement Sum.

Josephine Teo also cited that 60% of CPF members who turned 55 in 2017 two year ago would be expecting to get monthly payouts of $700 to $750 after they hit 65 in 8 years’ time.

In the 4th column of my table, I have appended the corresponding Full Retirement Sum ($166,000) and the computed payout for CPF Life Basic. If the data is telling us the CPF members turning 55 years old in 2017 is only getting $700 – $750, that means that most of them have not reached the full retirement sum.

Half of the Full Retirement Sum, or the Basic Retirement Sum pays out around $614/mth.

This likely means that majority of those hitting 55 years old:

- Pledge their properties

- Have at least the Basic Retirement Sum of $83,000

Some Personal Conclusions

I think based on these data I have the following takeaways:

1. In the future, the current full retirement sum CPF Life payout will look so insignificant. At first, I was shocked when I saw the figures. I thought majority could not hit the minimum sum. The 26% of those above who have more than $500/mth in payout probably hit the minimum sum. Those that are 65 to 69 are likely to have slightly less than minimum sum.

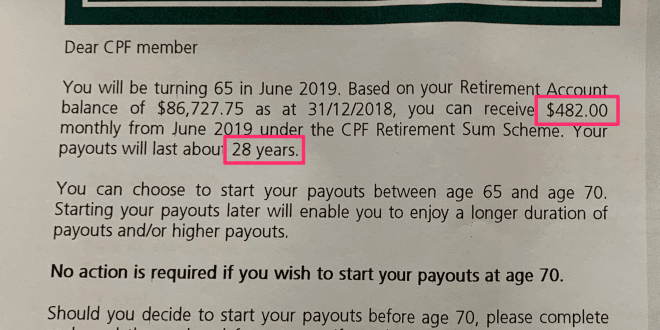

The problem is that we do not keep track of the corresponding estimated income payout for that minimum sum. The math of $450 is not too far off from this letter that have been circulating:

This guy is born in 1954 and the minimum sum should be around $117,000. At 55 years old, he should have less than this minimum sum (estimated $58,589 or half the minimum sum).

$450/mth today, does not look like much. Which is why when people see this article, they get kinda worried.

In actual fact, the math does checks out.

What is horrendous is that inflation have made the purchasing power of $1 to be much lesser than before. If you think $482/mth do not buy much, wait till we see the current $1,200/mth touted in 10 years time.

2. Based on this CPF Data, the elderly need a lot of help. Purely based on the data, it will be quite challenging for the elderly to lived on $220 – $290mth in CPF. And a lot of the help comes in the form of the Silver Support Scheme which gives $2,400/yr to those who qualify, Workfare income support, GST Voucher and Com care.

If there is no such “optimized welfare” then it would have been worse.

Which brings me to my next point.

3. We cannot judge how critical their financial situation, without evaluating the circumstances outside of CPF. The younger folks have often mentioned that they do not get the kind of rapid growth, the cheap housing that their parents and grand parents have.

And with those, they could have more opportunities to build more wealth.

If that is the truth, then perhaps a lot of the wealth of the older generation lies outside of CPF. And we might make the wrong conclusion if we look at the CPF and say our older generations are in dire straits.

4. The majority of you do not shore up their CPF if you are given the chance. It used to be that the employer and employee contribution to the CPF is 50% instead of the 37% now. The rate of return on the CPF used to be higher as well. This gives a lot of incentives for people to actively save their money for retirement.

There is this narrative which asked why do they have to “shift the goal post” by increasing the minimum sum. Why do they forced us to have more money in our CPF.

If saving for retirement, building wealth is a worthwhile goal, then people should be willing to do it, much less an account whose returns are more predictable, sturdier, less risky than other financial assets.

Yet the older folks barely meets the minimum sum.

You wonder if we do not “shift the goal post”, would Singaporeans actively add on to their CPF voluntarily? I think not likely for the majority.

5. There is one point to be worried about and that is what is your future retirement Annual Essential Expenses and how much CPF you have accumulated to provide for this. For too long, the opposition have tried to drum up a conspiracy theory that the CPF returns are too low, your CPF funds are locked away for too long, and sometimes via the always rising full retirement sum or minimum sum.

The complain about the funds locked away for too long, and that full retirement sum should not be rising, is only valid if most of us have accumulated adequate, and even more than enough CPF funds to provide for all our retirement expenses.

Based on what Josephine have provided, that is not the case. We do not have enough in our CPF funds. If your complain is that the cash flow is not adequate to even pay for your annual essential expenses today, then you have accumulated too little in CPF funds. You should not gripe about the rising full retirement sum every year.

On the other hand, if you say that you are unaffected by your CPF funds, to provide for your annual essential expenses, as you have other sources of assets out of CPF or you could get it from your properties and investments. You have did the sensible thing to build wealth and you have done OK.

In this case, the Singapore system works for you because you have more disposable income to work with throughout the years and you have done it splendidly.

While your CPF payout for you is low, when your net worth is viewed in totality, you are better off. There is not much to complain about.

The only ones who should complain about their situation are the ones who:

- Tried to strive and maximize how much they earn throughout their life time but can only achieve so much net worth

- Tried to spend in a very sensible manner (by most of our sensible standards) but could not keep the expenses low

- And did not accumulate enough in CPF and money outside

If majority of the Singaporeans are like this, then the Singapore system have failed us.

6. How has the housing asset liquidation gone for you? This is to build upon #3. In the 1990s and 2000s, some of the prominent ministers tried to drum up that housing is an asset that you could use to accumulate wealth upon.

We have some of the highest home ownership rates in the world and that is largely due to majority of us owning HDB flat.

Now in financial planning, we know the financial assets has this feature that allowed us to do this or that. However, the biggest thing is whether you should do this or do that and whether you could carry out that execution eventually.

Those same politicians are trying to be financial planners now.

And they seemed to know how you work behaviorally to recommend wealth accumulation through a single, very concentrated, financial asset, that just so happen you could lived in.

For most, half of their CPF is in the form of that housing asset so the cash flow should consist of:

- Your CPF Retirement Income Stream

- How you monetize and liquidify your home

For #2 this could be:

- Downgrading (Property Size Arbitrage or Geographical Location Arbitrage or Both) and taking the cash and cash flow it (in the most sensible manner)

- Rent out some rooms

- Sell your leases back to HDB, which topped up your CPF Retirement Account, and this increases your CPF Retirement Income Stream

My suspect is that, behaviorally, people do not do the above actions. And this is a bigger problem when part of our retirement funds is a single property.

Unless you put a mandate: If your money in your CPF retirement account does not reached the CPF full retirement sum, you are forced to downgrade to a smaller home, or a further outskirts home to have that full retirement sum. In other words, retirement takes precedence over the relationship with your home built up.

Or force your children to top up your money to full retirement sum. This would force your children to get educated on this matter and seriously consider all this matter and see how they do not have to top up to full retirement sum, including downgrading the home.

If you create so much flexibility, you got to be ready for the consequences.

My overall conclusion is that, there are the folks that are reluctant to commit to having only their CPF funds for retirement, and have build up assets out of the CPF funds. It would not be right for us to just conclude based on the amount of CPF retirement income gotten that the situation is poor. Part of the Singapore system is that a large part of your disposable income is up to your own responsibility, your own sophistication, your own conscientiousness.

And this data point do not show enough.

The payout looks depressing, and I think 10 years later, we will see a $1200/mth payout to be depressing. And that is the way it is.

If you keep saying Basic Retirement Sum is enough, this is something that you have to lived with.

My other CPF related write ups:

- How I Manage My CPF – Past, Future and Philosophies

- Why it is So Difficult to Raise the CPF Withdrawal Age of Your Citizens

- This is Probably Fake CPF News

- How would Your First $60,000 in CPF Compound Over Time?

- Which CPF Life Plan Gives the Greatest Return? (This shows you the Internal Rate of Return (IRR) of the 3 different CPF Life Plans)

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Fred

Wednesday 13th of March 2019

Let me weigh in, please.

More than 10 years ago before I was 55, I remember the situation then, I had been advising many of my peers, clients and families to quickly divert their CPF OA and SA before they hit 55, one of the eligible means then was to purchase a second house. The purpose was to clear as much as possible if they do not want the G to lock-in after 55. Many did including myself. After clearing the CPF money, there was little left. When I was 55, CPF wrote me that I can have only $300+ per month if I wish to commence my monthly at 60 which is my monthly payout eligible age. My Wife can have only $100+ per month. Due to the Low payout, we leave the money in CPF. Fortunately or unfortunately, enbloc came to force-sale our home which in turn, fatten our CPF accounts as the money with its accrued interest were required to be returned to our CPF. Today, both my wife and my CPF can have its maximum of ERS each. My contemporaries may not have the enbloc fortune but I’m sure they are living off their home investment income over and above their CPF payouts.

Just trying to fill a gap. Hope that helps.

Kyith

Wednesday 13th of March 2019

Hi Fred, congrats to your enbloc. However, I do think whether asking people to put into properties is the way to go. They got in at the right time. If you ask people to do the same in 2013, you wonder if their investment income would outweigh that of CPF Life.

Sinkie

Wednesday 13th of March 2019

This is not new. Way back in the 1990s, govt already knew CPF not enough --- that's why they ramped up Min Sum from $40K to $80K in the late-1990s till early-2000s.

By the time govt did the 2002/2003 CPF review, the conclusion was that minimum subsistence-level retirement amount should be $130K in 2003. But they also know that majority of S'poreans will have heart attack or vote opposition if they up the Min Sum overnight from $80K to $130K.

Hence the plan to increase MS from $80K to $130K over 10 years from 2003 till 2013, but adjusted for inflation. That's why you kept seeing "in 2003 dollars" in the news. But people forgot and during high inflation years like 2008 when the MS increased by $11K, people screamed. So much so that govt had to slow down the increase and stretch by another 2 years to 2015 to hit the target of $130K in 2003 dollars.

These few years the FRS has gone up by roughly 3%p.a. which is above the inflation rate. Hence the FRS today is likely just slightly above the original $130K --- maybe $140K in 2003 dollars. No matter what, this FRS is still basically a subsistence-level living, like the bottom 15% of society. Anybody thinking that just becoz they have FRS means it should provide an average or middle income living is delusional.

All along since the 1990s, govt knows a big problem with CPF (besides being overused for property) is the low rate of returns i.e. the 2.5% OA rate. With rapid salary increase in the 1980s & 1990s, they can overcome this by mandating large increases to Min Sum. But going forward, unless S'poreans experience similar kind of wage increases, I think govt will need to review CPF returns --- probably how other pension funds, SWFs, Uni endowments do it.

Govt has tried to improve CPF returns by SA and extra 1% interest, but I think it's not enough as the bulk is OA, and worse most of it goes to property / mortgages.

They may also do away with the property pledge thing. Looking at my relatives & peers, 90+% of them have or planning to pledge property in order to get more of their CPF out.

Kyith

Wednesday 13th of March 2019

Hi Sinkie, I am astounded how you can remember all these things off your head. IS there any materials to read regaring the big problem with the low rate of returns? that is something that I noticed as well

so1trg

Wednesday 13th of March 2019

This just points to one thing - cost of living is way too extreme!

Createwealth8888

Wednesday 13th of March 2019

May be one of MPs should ask how many CPF members who are receiving low RSS payout at 65 have lost their CPF money in investing pre AFC?

Breakdown of their losses and collating to low RSS payout.

Ricky Soh

Wednesday 13th of March 2019

She also mentioned

Couples only needed so much space to make babies...

Ban modification of exhaust because it encourages speeding...

I wonder how low is her IQ.