I saw this article that came up on my Facebook. It’s purpose looks more like to gain sympathy from us and to educate us on the problems of CPF that people are not telling us about.

Christopher Pereira was a die-hard PAP supporter. He was known for making figurines of some prominent PAP leaders in the past.

He got a shock of his life when he was told by a CPF staff that he should starting saving to top up his CPF savings. He was told he needed at least $171,000 in his retirement account to get a monthly payout of $458/mth for 28 years.

Mr Pereira felt that $458/mth is not enough to pay for his expenses. He is quite disappointed so he decide to switch to making figurines of former Secretary General of Workers Party Low Thia Kiang.

The following is what was posted:

If you are interested in the article you can Google “61 years old die-hard PAP supporter shocked that CPF staff asked him to “save” to top up his CPF”

If you understand the CPF payout, or have used one of their calculators, you would have realize this is closer to a post that is trying to mislead people than to bring some grave to our attention.

Mr Pereira falls under the age where he will auto enrolled in CPF Life, so what the CPF person is talking about should be the Full Retirement Sum (FRS) that he had to hit, to get the designated payout.

However, the payout is abnormally low.

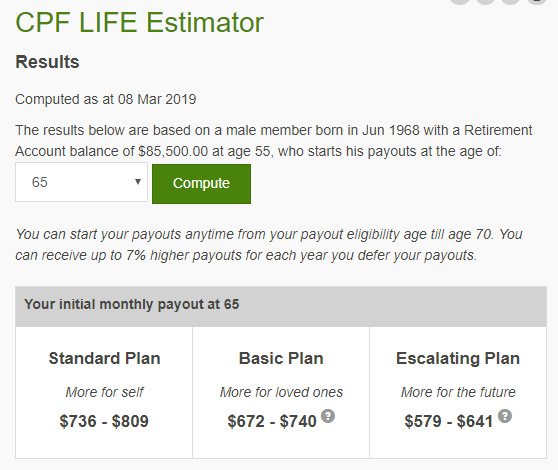

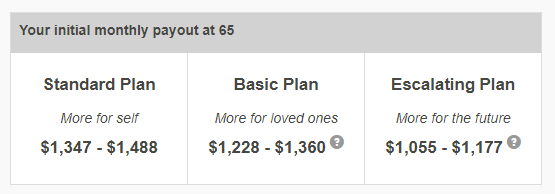

Whether it is real or not, we can probably draw reference from an article in The Online Citizen where a reader wrote in that he is quite shocked that the payout that he would received $482/mth from the Retirement Sum Scheme (note this is different from the FRS stated earlier. Google “Totally illogical to suggest CPF payout term of 28 years where there is no one to receive balance payout”)

The payout is rather similar and in this case we can see the balance that the reader had in the retirement account. In this case, the reader gets a annual yield close to 6.3%. This is hard to find anywhere else.

It is likely Mr Pereira’s CPF retirement account is around this range, and have not reached the FRS of $171,000. In any case as a 61 year old the FRS in 2013 should be closer to $139,000, which is what is applicable for him at age 55.

If we use the CPF Life estimator for half the FRS, which is equivalent to the basic retirement sum, the payout is higher than this $458/mth he said.

The FRS payout for $171,000 is pretty high compared to what is posted as well.

Given this, that post is likely very political driven and serves to shock more people about how deficient the CPF for your retirement. However, it misleads fellow Singaporeans more than helped them in my opinion. If we read the comments section, you realize that Singaporeans are pretty informed to think that there is something wrong with this picture.

I would think that the CPF personnel would not make such mistakes. There is much that have not been said, and that is why the numbers given is much lower.

The self examination is that if you look at such an article(s) and believe that it leans more towards the truth than you think this is false, then you probably do not know enough of the retirement system in the first place.

More worrying, if you expect that despite how much you contribute to the system and you get a sum of $1000 to $3000/mth in annuity income for life, then you need to get financially educated, re-calibrate how much realistic returns financial assets will get us. Then you will realize some mathematics that goes on in your head is a bit ridiculous.

Lastly, having nothing in your CPF is OK. Not satisfying even the basic retirement sum (half the full retirement sum of $171,000 currently) is OK. You just have to have enough wealth out of CPF.

In the worst case that you cannot find something good for your retirement, you could always top up your retirement account and enrolled in CPF Life to get the above high yielding yield.

If you have very little in CPF and very little outside of CPF, then that is a precarious position to be in.

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Victor C.P. Wong

Friday 8th of March 2019

Quote: "In the worst case that you cannot find something good for your retirement, you could always top up your retirement account and enrolled in CPF Life to get the above high yielding yield."

I am not sure CPF Life is "high yielding" as you called it. I came across an article "How Long Does It Take To Beat The “Break-Even” On Your CPF LIFE Plan" by Dinesh Dayani. The writer sets out to show that the break-even age of CPF Life annuity is roughly at 88 years old i.e. 23 years after one starts the annuity at age 65. Anything less than 88 age, one is losing money to the annuity. In another way, the article shows CPF-Life (Annuity) comes at a steep price. The forgone interest payable on the principal sum under the Retirement Sum Scheme (RSS) is the price or premium of the annuity. In the hypothetical case cited in the article, a member who starts CPF-Life at age 65 with a principal sum of $270,000 draws a monthly payout of $1,495 for life. The 4% plus interest which he forgoes under RSS amounts to $113,00. Therefore, this amount is the premium he pays over the 23 years period (i.e. age 65 to age 88). This averages $409 per month which is rather steep at 27% of the monthly payout. In return for this premium, CPF-Life promises payouts beyond age 88. This is the break-even point because similar conditions and uniform payouts over time under the RSS would have lasted up to this point. The question boils down to, at age 65, what is the probability of one living up to age 88 and beyond?

Kyith

Friday 8th of March 2019

Hi Victor, just compute the internal rate of return and compare between the plans. I have an old article that computes for different plans and different life expectancy. its either you get it or your next generation. someone will get it so its not a problem. The CPF life will give a higher cash flow payout than RSs. as for the interest forgone.... no interest is forgone, i think you have a wrong way of looking at things.

the break even is about 20 years. even if you are on RSS you also need some time to break even.

at the end everyone of us goes into the grave. you cannot bring the money away.

Boonhow

Friday 8th of March 2019

CPF is slightly complicated, at least to me. There are constantly changes in the system, difficult to keep up to date. It is not something very knowable and controllable to me. If I do get the $400+ per month, it will be treated as a bonus. Something more knowable and controllable would be to be mindful of own spending and to seriously build up our own "wealth machine"/ retirement fund.