I do not understand this acquisition by LMIR.

They currently have a dividend yield of 10%. Then they proposed to buy this mall which will reduce their dividend yield.

I did some notes for a friend, so I thought I will put it out here.

For those who are invested in real estate investment trusts (REITs), the company not just pays you dividends. Sometimes they do ask for money from you again. And again. So you got to be familiar with all these rights issues, placements, preferential offerings. If you don’t learn about this, better not invest in REITs.

Lippo Malls Indonesia Retail Trust (LMIR) proposed to spend S$430 mil to acquire Lippo Mall Puri, a shopping center located in Jakarta. The shopping center was bought from PT Mandiri Cipta Gemilang, which is an indirectly wholly-owned subsidiary of PT Lippo Karawaci Tbk, the sponsor of LMIR.

What happens is that PT Mandiri developed this shopping center, with 6 apartment towers with a total of 1000 residential units, a school and an office/5 star hotel building. Basically, they build a mini work, live and play environment.

This purchase comes with vendor support. With vendor support, the average valuation is $380 mil. Without its $360 mil.

LMIR will purchase it at S$355 mil.

There is a 5% discount to the appraised value but valuations are often fluid. It is easy to make a purchase look worth it if the valuers give a too optimistic valuation.

The whole acquisition will come up to S$430 mil, inclusive of S$10 mil in AEI.

The property sits on 2 HGB land titles. For more information about HGB land titles and how long are these land titles, you can view this article here.

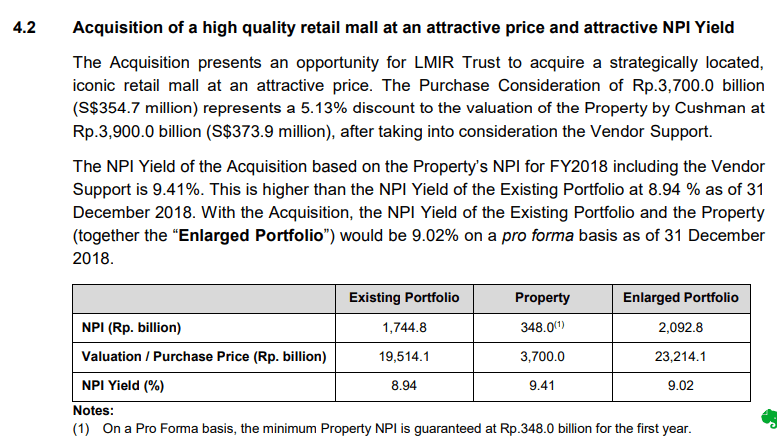

Purchase is Net Property Income Accretive

LMIR show us that the acquisition is NPI accretive. Since LMIR trades so much below book value, I wonder if we should compare NPI yield.

A comparison of NPI yield shows the attractiveness of the current portfolio of properties versus this new one.

And it does show the merit of this property, relative to its purchase price.

However, with LMIR currently trading at this price, does it make sense to purchase this property?

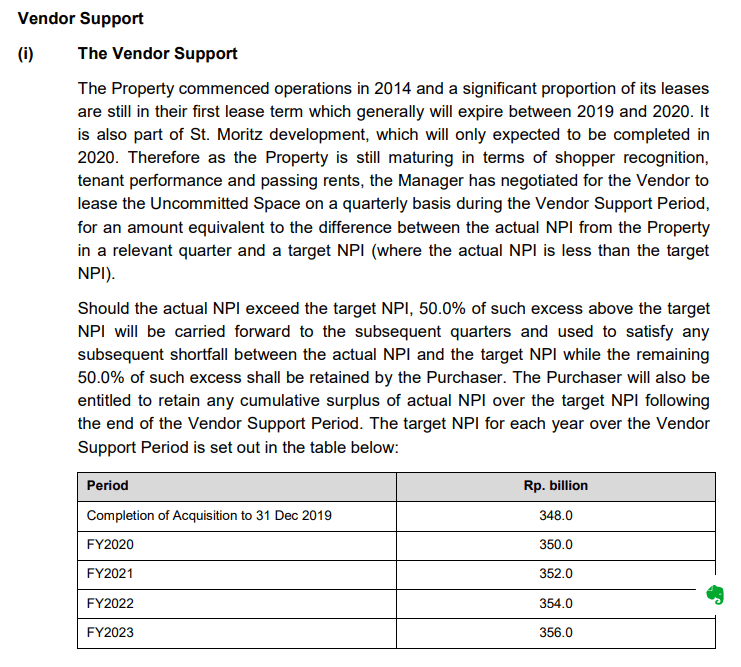

Sponsor is Supporting the Proposed Acquisitions Rent

The vendor is providing income support because the rental income is not matured yet.

The vendor is providing income support because the rental income is not matured yet.

It seems the NPI target may be based in Rupiah, thus they might not be shielded from the depreciating Rupiah versus Singapore Dollar.

2 Different Proposals to Finance the Acquisition

Before the acquisition is approved, the manager proposed a combination of debt and equity raising, to finance this S$430 mil acquisition.

Since this is a related party transaction, shareholders would need to vote in an EGM whether to go ahead with this.

LMIR have proposed 2 different kind of funding:

- A 58% to 42% debt to equity funding. $180 mil in equity and $250 mil in debt

- A 35% to 65% debt to equity funding. $280 mil in equity and $150 mil in debt

Since LMIR share price is so low, and trading at a 10% dividend yield, equity funding is more expensive than debt funding.

The equity raising would likely be a rights issue based on what is proposed.

In a rights issue, the REIT manager asks you, the existing shareholder, whether you want to increase the number of holdings of LMIR, to help fund this acquisition.

If you choose to, you pay them money to get more units. Whether you are better off, versus not subscribing, depends on whether the acquisition increases your overall dividend yield, based on your old shares plus new shares.

If you do not wish to subscribe, likely you can sell off the rights, which is your right to purchase these additional shares, to another person. These rights will be listed on the stock exchange like a normal share. Typically, it will be called R, or R1 or R2. So the rights of LMIR may be called LMIR R.

Selling off the rights, in theory prevents you from being diluted due to the enlarged equity base.

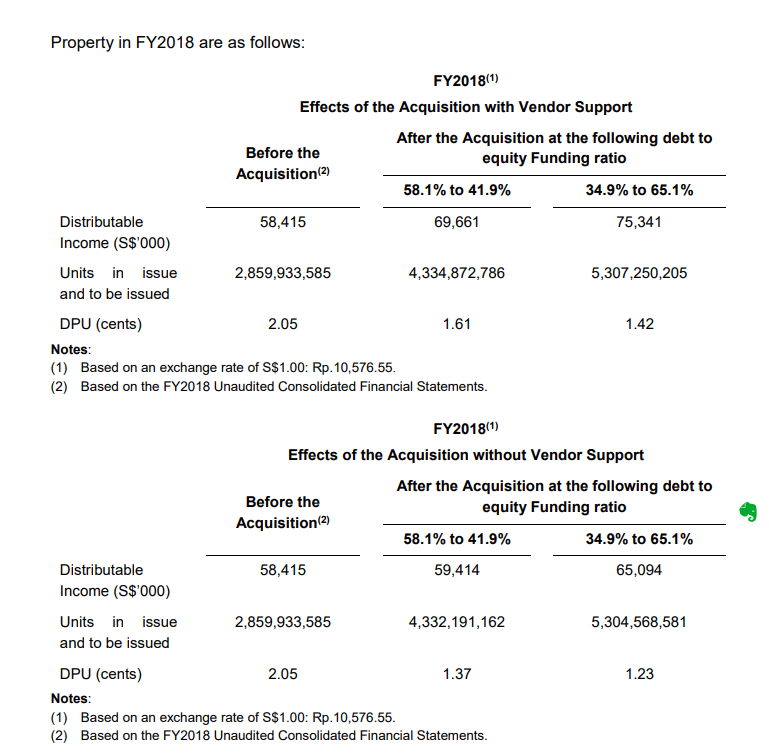

LMIR provided the following guidance. They show 2 sections and the corresponding dividend per unit (DPU) before and after the acquisition.

LMIR provided the following guidance. They show 2 sections and the corresponding dividend per unit (DPU) before and after the acquisition.

From the guidance, the DPU will go down alot from 2.05 cents to 1.61 cents or 1.42 cent if there is Sponsor income support. If without Sponsor income support, the DPU is reduced to 1.37 cents and 1.23 cents respectively.

The conclusion here is that through this way of equity and debt financing, it is not DPU accretive, which means the DPU go down. Thus, if you hold on to your LMIR shares, and do not subscribe to the rights issue, nor sell off your rights in the future, your DPU will go down.

If you choose to subscribe to the rights, like most folks, we do not know if it is dividend yield accretive.

Dividend yield accretive means that the dividend yield after the acquisitions, with the enlarged equity base, is higher than before the acquisition.

So there are 2 different ways of financing. One with higher debt and lower equity. The other one vice versa.

Let us take a look at both ways of financing with the income support from the Sponsor

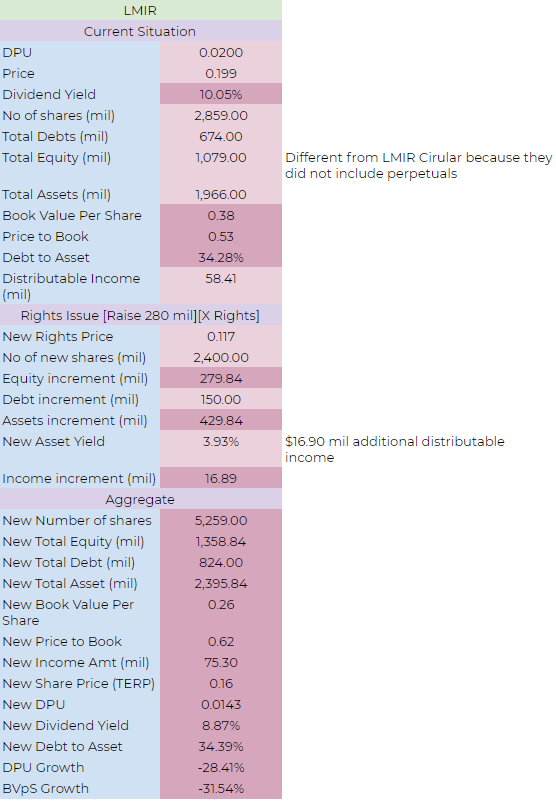

Financing with Higher Debt than Equity, with Income Support

Here is my trusty rights issue or placement calculator.

Here is my trusty rights issue or placement calculator.

How you read it is that notice there are 3 sections:

- The current situation for LMIR before the acquisition

- How the acquisition is financed (the level of debt and equity)

- The aggregate of the acquisition and the current balance sheet

I plugged in LMIR current distributable income, price of $19.9 cents, dividend per unit, its assets, debt and equity in the first section.

LMIR may issue 1500 mil shares at $0.12 and borrow $250 mil.

The rights may be priced at $0.12 or 40% discount.

Notice that the total equity of $1079 mil before the acquisition is higher than LMIR’s figures. This is because my figure includes the perpetual, which LMIR did not include.

The dividend yield before acquisition is 10.5%.

The asset yield of this acquisition is 2.6%. This is the increase in distributable income divided by the total purchase price of $430 mil.

Why is this so low?

LMIR will borrow $250 mil and there is interest expense on that incremental debt that you need to factor in. The yield on equity is closer to 6.2%.

After the acquisition, the ex-rights price (TERP) is $0.17.

The dividend yield fell from 10.5% to 9.29%. The debt to asset went up from 34.28% to 38.56%.

Based on this financing, the acquisition is not dividend yield accretive.

This acquisition makes the shareholders worst of, and increased the risk to the portfolio.

Financing with Higher Equity than Debt, with Income Support

LMIR may issue 2400 mil shares at $0.117 and borrow $150 mil.

The dividend yield before acquisition is 10.5%.

The asset yield of this acquisition is 3.93%, which is slightly higher (less interest expense). The yield on equity is closer to 6.0%, which is lower than the first scheme.

After the acquisition, the ex-rights price is $0.16.

The dividend yield fell from 10.5% to 8.87%. The debt to asset stayed constant at 34.28% to 34.39%.

Based on this financing, the acquisition is not dividend yield accretive.

This financing is more dilutive than the former in terms of dividend yield. However, it maintains gearing.

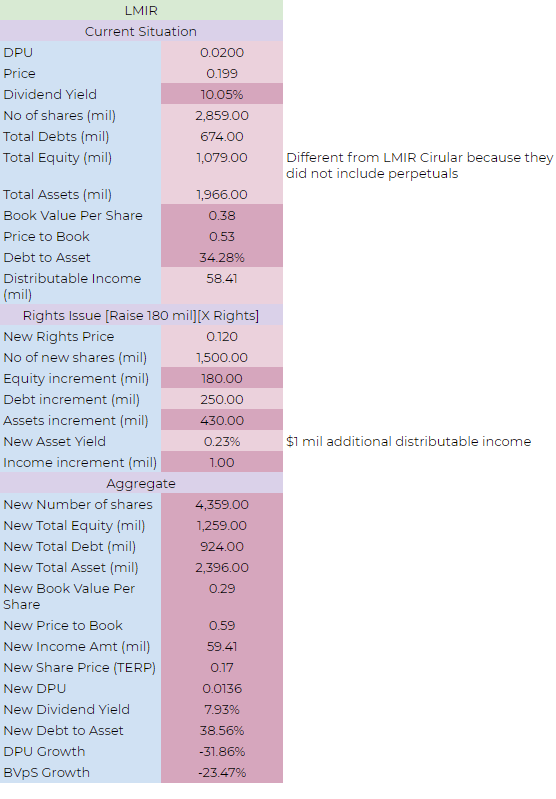

Financing with Higher Debt than Equity, without Income Support

LMIR may issue 1500 mil shares at $0.12 and borrow $250 mil.

The dividend yield before acquisition is 10.5%.

The asset yield of this acquisition is 0.23%. This is the increase in distributable income divided by the total purchase price of $430 mil.

Why is this so low?

This is even lower because without the income support, this asset barely adds to the distributable income! The yield on equity is 0.55%

After the acquisition, the ex-rights price is $0.17.

Based on this financing, the acquisition is not dividend yield accretive.

The dividend yield fell from 10.5% to 7.93%. The debt to asset went up from 34.28% to 38.56%.

Financing with Higher Equity than Debt, without Income Support

LMIR may issue 2400 mil shares at $0.117 and borrow $150 mil.

The dividend yield before acquisition is 10.5%.

The asset yield of this acquisition is 1.55%, which is slightly higher (less interest expense). The yield on equity is closer to 2.38%, which is lower than the first scheme.

After the acquisition, the ex-rights price is $0.16.

The dividend yield fell from 10.5% to 7.67%. The debt to asset stayed constant at 34.28% to 34.39%.

Based on this financing, the acquisition is not dividend yield accretive.

This financing is more dilutive than the former in terms of dividend yield. However, it maintains gearing.

Update: Is the current baseline dividend yield 10% or closer to 6%?

Here is an addendum to this original post.

Some readers have commented that LMIR’s dividend per unit have been dropping over the quarters. And based on the recent dividend per unit of 0.30 cents, the dividend yield should be closer to 6%.

I wrote a follow up post exploring this: Did I (and Lippo Malls Retail Trust’s Manager) used a Distributable Income that is Too Optimistic?

The conclusion is that well, perhaps I missed out on this, but if we look at the reason for the Q3 to Q4 fall in DPU it might be attributed to foreign currency exchange reasons then the business aspect of things. I am not sure how long that will last.

I think it will be safer to use Q3’s dividend per unit, which will work out to an annualized 2 cents. This is similar to this analysis.

Or we could work with an average of Q3 and Q4’s dividend per unit, which will result into a dividend yield of closer to 8%.

Either way, the reworked figure shows that the purchase is still not dividend yield accretive.

The Motivations Behind this Purchase

Why did I say this is obscenely not dividend accretive?

If we summarized the 2 kind of financing, you realize that they yielded very low asset yield or yield to equity after interest expense, without the income support.

So that is why the sponsor of LMIR need to provide rental support.

With or without rental support, if you are a shareholder holding the REIT before this announcement, you enjoy a dividend yield of 10%.

After this rights issue, if you subscribed to all the rights you are entitled, your dividend fell from 10% to a range of 8.87% to 9.30%.

Now why would you approve such a purchase?

As a shareholder, I would approve such a purchase if the growth of the rental is like in Hong Kong, where each revision can be like 20%. This means that we are purchasing a quality asset. This justifies why we have to buy it now.

The sponsor is providing rental income support and judging by the figures, its 17% higher than without income support. Based on the current distributable income of $58 mil, this means the rental growth within the next 5 years needs to be around 17% or 3.2% per year.

That looks like a pretty normal hurdle growth rate. If Lippo Mall Puri grows faster than this you got a good asset.

Still, with a dividend yield of 10%, you have to wonder why the manager would buy something that is not immediately accretive.

They could wait until the income stabilized 4 to 5 years later, before purchase.

I think for them, there is never a good time, because

- perhaps it will take a long time for the income to stabilized (that will be a worry)

- rental earnings will always be volatile (that will be a worry)

- the sponsor have to sell to someone, but without a stable income, no one will buy

#3 looks the most probable.

If this is a very attractive asset, they would have sold it to a third party.

The Sponsor need to provide income support, so they will hold back $70 mil. They will receive $354 mil for the sale and they won’t be getting the VAT, land acquisition tax, acquisition costs.

So its still a immediate cash flow of $284 mil. (just not sure what is the construction costs)

Why not Sell a Property and use the proceeds to Buy Back LMIR Shares?

If you look at the calculations the price to book is 0.53 times which is extremely low. But we have to bear in mind the book value includes the perpetuals.

If we take out the perpetuals the book value is $819 mil. LMIR current market capitalization is $569 mil.

The price to book is closer to 0.69 times.

Still it is a discount.

If their property is that undervalued, and they can sell at book value, or even higher, selling one or two properties would create enough cash flow.

Take that cash flow to buy back shares at 10% dividend yield.

That is better than any properties out there.

However, it is not intuitive for a REIT to do that, because

- that will reduce management fees, since what they earn is based on distributable income or AUM size

- those shopping malls may not be worth at book value, if its not operated by the Sponsor

So these are some of the things to think about if you are a shareholder.

Rights issues and Placement is a competency you need to learn if you purchase REITS.

I have more case study in my REIT Training Center in the Learning about REITs section below. It is free. No upsell. Just to get you level up.

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

- The LionGlobal APAC Financials Dividend Plus ETF Won’t Give Singapore Investors 5% Dividend Yield Always. Further personal thoughts (with some data). - April 13, 2024

Toh hong San Robert

Saturday 5th of December 2020

I refer to Lippo Mall Trust (D5IU) right issues, I opposed it proposal of 160 rights to 100 existing share. I have the following points:

1. The prospectus is based on 17/9/2020 closing price of $0.115, as of 1/12/2020, the closing price is $0.084 which 26.9% lower, so all figure quoted is out dated.

2. “Lippo Mall Puri acquisition would provide a steady stream of income during the current Covid-19 downturn while the rights issue would unlock the distribution restrictions currently imposed by the US-dollar Notes” I trust US-dollar Notes distribution restriction; it prevents Trust Management make excessive loan, it called for proper audit and protects Singapore investor.

3. Does Vendor support come under SGX purview? If not, it can be withdrawn any time, for such scenario, Trust performance is to be negative.

4. The Acquisition Cost of Lippo Mall Puri for S$391.0 million in cash is expected to be funded by S$271.0 million of equity from the Rights Issue proceeds and S$120.0 million of debt financing facilities comprising bank facilities and Vendor Financing, so shareholder fund is 2.25 times to bank loan, means individual investor are smarter than Investment Bank that access more data and market information; which is not true. Rights issue of 160 to 100 existing shareholding is equating to back door listing. Non underwritten means is not back up by bank, anyone can claim better than Indonesia bank for this issue, agree?

5. Does the Trust plan strategic move to delist from SGX and list it on Jakarta Stock Exchange? In AGM unit holder are asked to vote for The Unitholders’ approval of the Whitewash Resolution which enable the Sponsor (through its wholly-owned subsidiaries, LMIRT Management Ltd. and Bridgewater International Limited) and their concert parties to subscribe for its Allotted Rights Units and all remaining unsubscribed Excess Rights Units without incurring an obligation to make a mandatory general offer for the LMIR Trust in the event that the Allotted Rights Units and Excess Rights Units issued to them raise their aggregate unitholding to more than 49% of the voting rights of LMIR Trust. Singapore Investor understanding of the Whitewash Resolution is a protection measure; for SGX building a healthy stock market.

6. I am holding 350,000 units, I bought it recently for dividend collection as retiree. With the proposal, I need to invested another $33600, which is very high risk. For a stable market, a rights issues of up to 20% is prudent. A more stable market likely to attract more grow and further investment. I bought it at $0.144, without right subscription, I will have left with shares price at $0.081, not a good move for existing shareholder.

I refer to Lippo Mall Trust (D5IU) right issues, I opposed it proposal of 160 rights to 100 existing share. I have the following points: 1. The prospectus is based on 17/9/2020 closing price of $0.115, as of 1/12/2020, the closing price is $0.084 which 26.9% lower, so all figure quoted is out dated.

2. “Lippo Mall Puri acquisition would provide a steady stream of income during the current Covid-19 downturn while the rights issue would unlock the distribution restrictions currently imposed by the US-dollar Notes” I trust US-dollar Notes distribution restriction; it prevents Trust Management make excessive loan, it called for proper audit and protects Singapore investor.

3. Does Vendor support come under SGX purview? If not, it can be withdrawn any time, for such scenario, Trust performance is to be negative.

4. The Acquisition Cost of Lippo Mall Puri for S$391.0 million in cash is expected to be funded by S$271.0 million of equity from the Rights Issue proceeds and S$120.0 million of debt financing facilities comprising bank facilities and Vendor Financing, so shareholder fund is 2.25 times to bank loan, means individual investor are smarter than Investment Bank that access more data and market information; which is not true. Rights issue of 160 to 100 existing shareholding is equating to back door listing. Non underwritten means is not back up by bank, anyone can claim better than Indonesia bank for this issue, agree?

5. Does the Trust plan strategic move to delist from SGX and list it on Jakarta Stock Exchange? In AGM unit holder are asked to vote for The Unitholders’ approval of the Whitewash Resolution which enable the Sponsor (through its wholly-owned subsidiaries, LMIRT Management Ltd. and Bridgewater International Limited) and their concert parties to subscribe for its Allotted Rights Units and all remaining unsubscribed Excess Rights Units without incurring an obligation to make a mandatory general offer for the LMIR Trust in the event that the Allotted Rights Units and Excess Rights Units issued to them raise their aggregate unitholding to more than 49% of the voting rights of LMIR Trust. Singapore Investor understanding of the Whitewash Resolution is a protection measure; for SGX building a healthy stock market.

6. I am holding 350,000 units, I bought it recently for dividend collection as retiree. With the proposal, I need to invested another $33600, which is very high risk. For a stable market, a rights issues of up to 20% is prudent. A more stable market likely to attract more grow and further investment. I bought it at $0.144, without right subscription, I will have left with shares price at $0.081, not a good move for existing shareholder.

Bob

Sunday 17th of March 2019

The hurry is because the sponsor PT Lippo Karawaci Tbk is raising capital by selling off assets and pulling in another US$730 million by a rights issue. It has severe liquidity problems, in particular interest payments, rent to FIRST REIT, plus two loans that are due in the next twelve months.

Lee Wai Leong

Friday 15th of March 2019

They didn't price the purchase based on the current yield. If they did, they could never acquire anything. Except junk properties offering 10% or more yield.

LMIR price has been knocked down like crazy because of Lippo. Does that mean they should stop acquiring anything at all?

Kyith

Friday 15th of March 2019

Should they?

Bob

Friday 15th of March 2019

Thanks for the analysis.

1. "Selling off the rights, in theory prevents you from being diluted due to the enlarged equity base."

I don't quite understand this. By selling off the rights a unitholder has not only a smaller piece of the pie, but also, based on the calculations, will receive a diminished DPU on current holding??

2. It looks like LMIRT is planning on a rights discount of at least 40% to the current price. Unless they are very concerned that the market does not want to invest in the REIT, I can think of no good reason to discount this heavily. Surely a much less discounted issue of a smaller number of units would not result in the DPU drop and leave the yield relatively the same?

3. This action is almost certainly going to cause another lurch down in the unit price, as the market current requires a yield of 10% to cover the risk premium. If the new yield drops below this as shown in your calculations, then the TERP unit price will fall until a 10% yield is reached again.

4. Yep, the sponsor is having a few difficulties and trying to raise cash. I would have thought this would be a good opportunity for LMIRT to expect a higher discount for this underperforming purchase.

Looks to be a bad deal for the unitholders and a good deal for both the sponsor and the manager.

One hopes that the manager will revise the terms or the unitholders will vote down the purchase. With a 50% drop of the unit price in the last twelve months maybe a few dissonant voices can be raised?

Kyith

Friday 15th of March 2019

For #1 its because if you do not wish to subscribe, the rights will be priced at the different of 19.9 cents and 11-12 cents (in theory). by selling off the rights you get to take back the capital that you do not wish to subscribe for. so your average cost instead of at 19.9 will be at around 16 cents. the dividend yield at that 16 cents will be near to 9-10%.

This is in theory but it does not always work out like that. this is because usually the rights, when they start trading is at a discount so you already lost money. the best is if you do not wish to subscribe, sell off if there is no price fall.

i think my dividend yield data might have a mistake. the dividend yield might be lower. the asset addition might be accretive.