One of the questions that were recently asked on our Singapore Financial Independence Subreddit is on pursuing early retirement with a child.

The lady asking the question probably encountered enough articles online that if you have children, it is practically impossible to retire early.

I think that is a valid question.

Too often, whenever I write an article on financial independence or retirement, you will get comments like: “That is easy, just remain single! So easy to do!”

It goes to show how much this narrative permeates the financial world.

In general, it is not impossible. It is just tougher if you have more future expenses to take care of.

At the end of the day, a lot boils down to whether you can save up the resources to pre-fund your future expenses.

So let us look at the math today.

Mr and Mrs J’s Current Financial Situation

Let us call the couple Mr and Mrs J so that I have an easier time writing the article.

Mr and Mrs J (both 31 years old) currently do not have children. They spend their time building their career. They did indicate some childhood traumas and are close to sorting that out to be ready to have children.

Here are their financials:

- Joint Annual Gross income of $270,000 (before CPF deductions)

- Annual household expenses: $30,000 to $48,000 (exclude vacation travelling, includes an allowance for parents, not so sure about whether it includes the mortgage)

- Assets: Joint cash, equities and bonds worth $500,000

- Residential home: 4-rm HDB in the outskirts of Singapore. Pleasantly surprise they enjoy living there. $120,000 mortgage left outstanding with CPF.

Since we are not sure about their CPF, we can assume that their employee CPF contribution together will work out to be $33,600.

Thus their joint annual net income will be roughly $236,000. This income is likely to still go up over time.

Mr and Mrs J have two of the three main ingredients to successfully retire early math wise:

- They earn a relatively high income.

- Their expenses are rather low.

They may just have to learn how to invest well. If they do, they would be able to be financially independent pretty fast.

There is one thing that I wonder about. Given their high income, I wonder if they have omitted their income tax. The income tax should be a rather big feature and would definitely affect their savings rate. But I am giving them some benefit of the doubt that this is factored into their expenses.

It will be better if we have the net income to work with.

When would Mr and Mrs J be able to retire if they remain childless?

Before we answer if they can retire early with a child, it will be good for us to have a reference point to compare with.

If they remain childless, how long would it take for them to be financially independent, retire early? And how much would that cost?

One of the unknown is whether their $48,000 expenses factor in mortgage repayment. If it does, then there are some payments that will come to a stop in the future.

The couple is not going to pay their mortgage payment throughout their retirement and thus, we can capitalize that mortgage cost. In any case, given their income, their mortgage should be comfortably paid with their CPF.

Let us assume that their expense includes a mortgage. If we backed out an estimated $14,000 a year in the mortgage, then we can assume that their current lifestyle would cost $34,000 a year.

Net of their expenses, their net surplus, or savings rate is $202,000 a year.

It is kind of crazy that if they work 1 year, they can roughly take 4 years off in theory. And the salary may still be going up.

We can make use of my Coast FI / Barista FI Calculator here to compute when MR and Mrs J can retire if they maintain their current lifestyle.

While my calculator is meant for you to figure out a Coast FI configuration (you can read my deep dive on Coast financial independence here), it can be adapted to compute a full early retirement.

Given their current expense, at an inflation rate of 2%, with a conservative investment growth rate of 4% a year, with their savings rate, they should be able to be financially independent in 5 years time.

They may need to reallocate their portfolio into a more ideal allocation.

As they may need to live through a longer duration (64 years), we assume a conservative initial safe withdrawal rate of 2.5%. They would need about $1.5 mil at 36 years old.

What worked out for them is because their expenses are rather low and high savings rate.

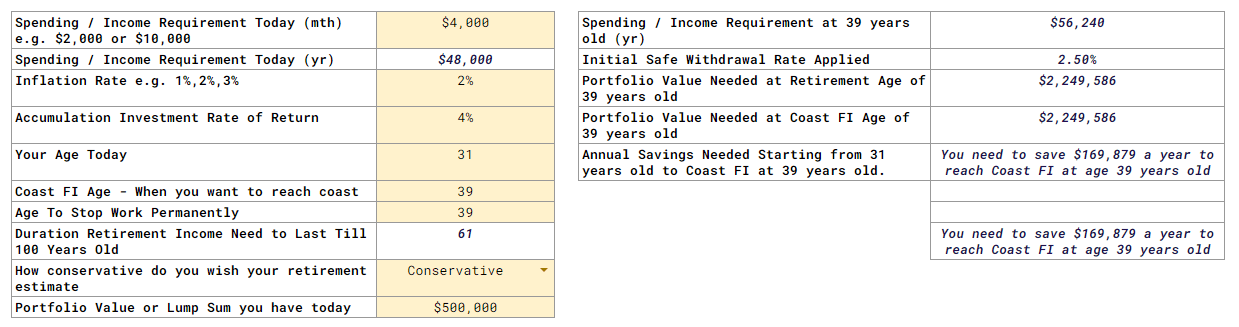

I decide to work out the math if their annual spending is $48,000 and their net surplus is $188,000:

Instead of 36 years old, they would need to stretch it to 39 years. They would need $2.25 mil instead as their inflation-adjusted expenses is higher.

But to be able to do it within 8 years is quite good.

The assumption here is that

- Mr and Mrs J maintain their lifestyle throughout this retirement. This is quite a challenge as it does not factor in vacation expenses.

- Inflation rate and investment rate.

- Depending on the economic outlook, Mr and Mrs J may not experience a poor retirement sequence and thus, they might not need to stick with such a conservative initial withdrawal rate.

How much to save up if you retire with one child?

The cost of a child is like a mortgage repayment.

It will be about 21 to 25 years.

You can estimate that you will pay for what they need up to university. After that, they are on their own. Strangely, that works out to about as long as a mortgage repayment.

The difference is that every year, the amount of payment is different.

We can compute for 1 child, how much we need to set aside on the retirement date, the future expenses for the child up to their university graduation.

If you are planning this when your child is 5 years old, some of these costs are avoided.

Someone pointed us to this Dollars and Sense article titled How much does it cost to raise a child in Singapore till age 18.

I think the article went through some pretty extensive line items. I was more disappointed that they don’t include university education costs. I guess that is rather subjective.

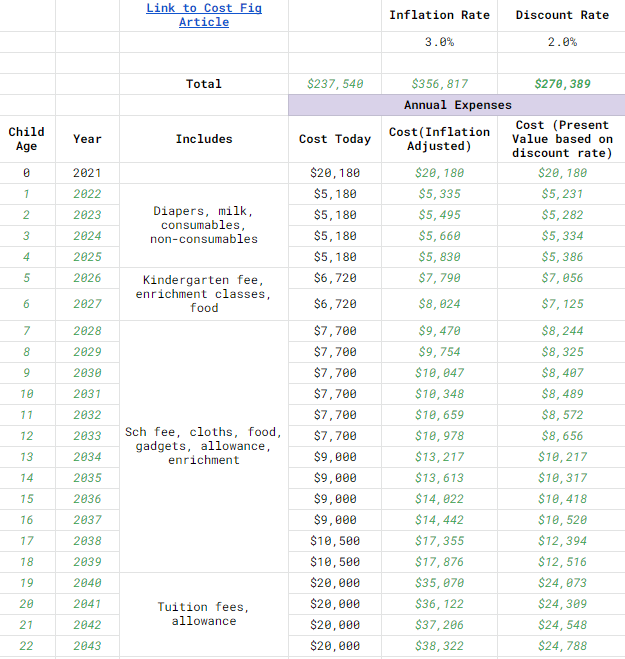

I took the list of expenses at every age, added some buffer and came up with a Child FI Expenses Calculator. You can access it here and make a copy of it.

Cost Today shows the expenses in today’s dollars. I followed the dearest estimation from Dollars and Sense but I added some more buffers for secondary to tertiary education expenses.

Cost (Inflation-Adjusted) shows the cost today in future dollars. A $20,000 a year university education with allowance will cost $38,322 in 20 years time at 3% inflation.

Finally, Cost (Present Value based on discount rate) adjusted the cost back to today’s value, based on a 2% discount rate.

The discount rate here represents the investment huddle rate you expect the money you set aside for your children’s expenses to grow at.

2% is rather conservative. You can imagine getting ready a lump-sum, put in a balanced portfolio that grows at 4-5% a year but expecting only a return of only 2% a year. Basically, you are over-buffering.

If you wish to be more adventurous, you could raise the discount rate. Changing the assumptions changes things.

The total cost over 22 years is $356,817, but if we invest it, and assume a discount rate of 2%, we need to set aside $270,389 today.

If you have more than 1 child, then you can adjust the figures accordingly.

Suppose your kid is already 10 years old, then the expenses you need to be prepared for is from 10 to 22, which will be $189,819.

Revisiting Mr and Mrs J’s Early Retirement Plan, with a Child

So now that we have a model for how much we need to save to bring up a child from 0 to 22, we can see how much Mr and Mrs J’s plan will have to adjust.

If they have their child at 32 years old, then

- Their net surplus per year will go down due to additional expenses.

- At their retirement age, we need to calculate roughly how much Mr and Mrs J need to set aside for their child’s future expenses

To be honest, their expenses may not go down much in real life. Given their salary, a 6% pay rise is nearly $16,200. That will more or less cover the cost of baby/infant and even include the cost of a maid if they so prefer.

But let us assume that their surplus a year is reduced by $6,000 a year. This will reduce $188,000 to $182,000.

Their net surplus barely got reduced.

This means that the amount they need to maintain their current lifestyle (for only the two of them) remains the same. Notice that in my calculator’s comments, I said that they need to save $169,879 a year for 8 years to be financially independent, retire early.

They have ample room to spend more.

Now when they are 39 years old, their child would be about 7 years old, so the expenses that they need to set aside, at 39 years old, is the expense for the child from 8 to 22 years old.

At 39, Mr and Mrs J would probably need to have $242,007 for the child’s expenses.

Given their surplus of $169,879, they may need to accumulate for 2 more years.

This is not too long of a delay. If they plan things well within 10 to 11 years from today, they could retire.

What are the considerations that could shift their plans?

What we provided today is a very linear way of planning. We assume enough assumptions so that we can have figures to work towards.

My experience tells me plans like this expire in 3 years because your life situation changes quite a bit every 3 years.

The way to think about planning is to come up with a plan, have an idea of how much you spend and how much to save, where to allocate your money, what should be your portfolio allocation.

Then we will periodically see how we are in our progress.

Mr and Mrs J’s plan would be ideal if they have taken care of the following:

- Build up the portfolio for financial independence for the two of them.

- Pay of the mortgage.

- Save up for the expenses of each child.

There is probably no need for some cash buffer to mitigate the sequence of return risk since our safe withdrawal rate is rather conservative.

Mr and Mrs J’s situation will change depending on:

- Their expenses. This is a big one. Expenses seldom stay constant. If they wish to accommodate an additional maid, that will change the picture.

- Child’s projected expenses.

- Portfolio allocation. This determines the investment rate of return.

- Inflation rate.

- Pay increment.

How much less do we have to accumulate by splitting out the child expenses?

If you look at my model, I treat the child expense as a finite stream and not perpetual.

But how much less do we need to accumulate by doing it this way?

I think it is rather mixed.

If you look at the child’s expenses over time, the expenses progressively become greater as the child grows up. In typical retirement estimation, they assume all your expenses to be the same.

How do you model that with fixed income knowing that expenses are bound to increase over time?

Basically, treating all your expenses as the same is the wrong model. And it leads you to have a twisted brain and think retirement is not possible with children.

But if you wish to lump all your expenses in one bucket and estimate how much you will need to retire, you can do that.

If we take the mid-point of expenses, having one more child will increase your annual expenses by $14,000.

And if you assume you need this for 60 years, just like the expenses for Mr and Mrs J only, then you will need $656,000 compared to $242,007 for the child expenses.

That is 171% more to accumulate.

If the child’s expenses are limited, then what you need is much less.

Can we do it with less income?

Mr and Mrs J’s upside is their high income at such a young age.

Even in a more optimistic case, if a couple has a combined income that is half of theirs, early retirement at 41 years old will prove challenging.

Mr and Mrs J’s superpower is also that they didn’t let lifestyle inflation happen. A couple with half income would likely only have $80,000 in surplus to work with.

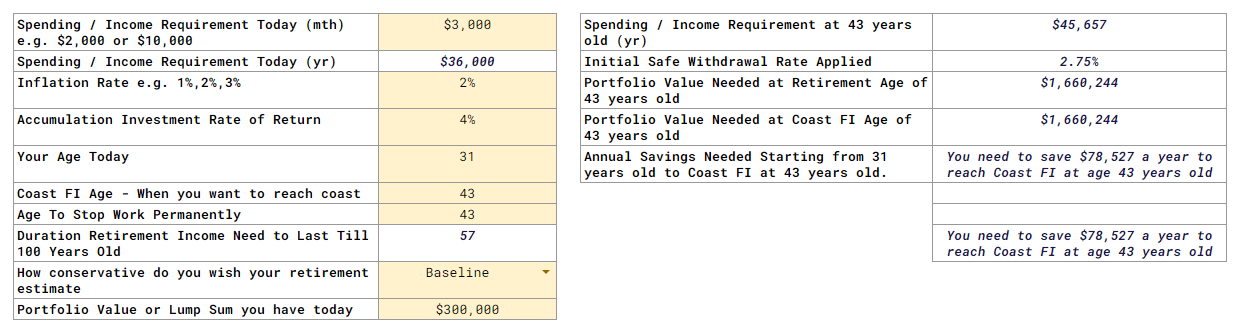

I made some adjustments to the two-person childless plan:

- Expenses for desired retirement lifestyle to be $3,000 a month in today’s dollars.

- Portfolio value of $300,000 at 31.

- Instead of a conservative retirement estimate, switch to a baseline. A 2.75% initial withdrawal rate is still rather conservative.

The couple may only be able to early retire after 12 years at 43 years old.

The additional amount that they need to set aside for the child’s expenses is closer to $212,000. That is 2.5 years more.

So a realistic early retirement age would be 45.5 years old.

Is that still considered early? Definitely!

Conclusion

Ultimately, whether we can retire with one child or two children is just math.

If you have the resources of Mr and Mrs J, you can do it faster. If you do not have the resources even half of them, it will be daunting.

But ultimately what determines a lot whether you can retire early or not seem to be:

- How your child expenses differ from Dollars and Sense profile.

- Your own lifestyle versus your income.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.