I opine in the past that, you do not need to track your expense or you do not need to budget if you have a good handle of your money.

However, not knowing how you spend your money, likely make you unaware of a key data that will make you realize you are closer to being financially secure or independent.

I been doing this budgeting and tracking for the past 12 years, so this is a glimpse of how I drain the money and its relation to how much wealth you need to build up.

My Past Annual Expenses Review

How different was this review from the past?

You can perhaps take a look at my commentary of my annual spending in the past.

- 2014: $23,798/yr – A review of my past year’s expenses

- 2015: $22,150/yr – How our family’s $22,150 annual expenses means for our financial security and financial independence

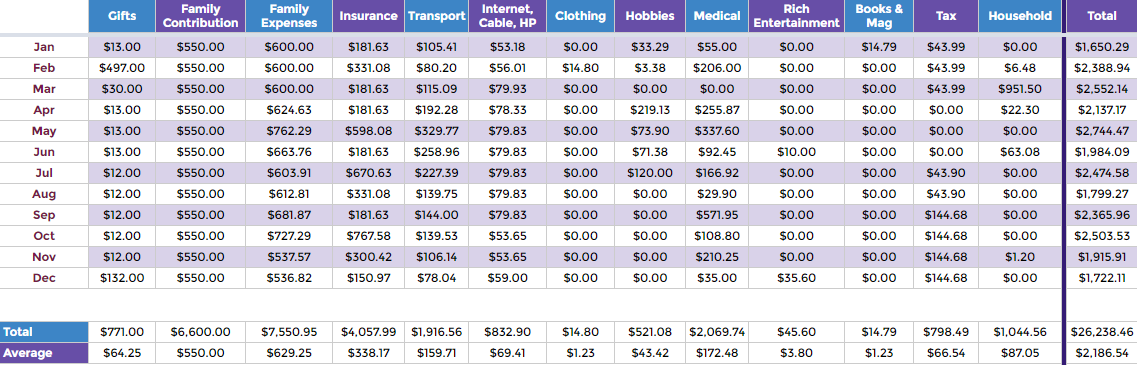

My 2016 Annual Expenses

My expenses went up but that is not much of a surprise. Our life changes and our expenses change accordingly.

Overall I spent $26,238/yr for a family of 3 adults.

This works out to be $2,186.54/mth.

I will go through some of the notable differences compared to last year.

Family Expenses went up from $5,773/yr to $7,550/yr

We prepare our meals for 3.5 adults at home. I seldom eat out so most of these spending are purchases from NTUC, Giant Shop and Save, Fresh Meat from the Market.

One of the reason why it went up was that, when my dad took over most of the cooking and purchases, he wasn’t about to optimize the quantity properly.

Add to the fact that, perhaps, last year my tracking is flawed, thus the difference looks big.

It took a few months of optimizing before we were able to push down from $700/mth to $550/mth. I think we will stabilized at $550/mth.

Is $700/mth a lot?

If we were to divide by 30 days and then 3 meals and then 3 person, then each meal costs $2.60 per person. That does not look like a lot, but the math is flawed, because Kyith eats roughly the amount equal to both his parents!

This means we spent $23.33/day as a whole.

When we stabilize at $550/mth this would mean we spent $18.33/day.

Before you say we should not be discussing the difference between $5/day, this is not always about how much we spent but how much Kyith is eating.

Over the past year, I embarked on some crazy binge eating and realize that perhaps I am eating too much for my own good. Just because things do no harm to health, I can eat as much as I want. However, that theory is flawed because, by right the excessive food brings little extra satisfaction and a waste of resources (if you read Bully The Bear’s 2016 reflection, he talks about his meal experiments and realization that we may not be as full as we think we need to)

I think I can do better. I will reduce my fruit intake to alternate days and perhaps try to reduce my breakfast.

Household went up from $605/yr to $1000/yr

Because the fridge eventually broke down. That alone takes $950 of the $1000.

Looking forward, when your home is 18-19 years, things will start breaking down.

The stove will be the thing to change this year, which will need about $300-$400. If you got a good vendor such as Goh Ah Bee, do let me know!

Medical Expenses Went Up

While I always cater $250/mth for medical needs, which includes supplements and experimental medical procedures, this year I spent $2000/yr compared to $444/yr.

I actually scaled down most of the medication that I tried. This time round, someone in the family got sick, and we spend a fair bit on hospital and outpatient treatment.

If not for health insurance and pioneer package, expenses will be more expensive.

I expected this to remain this amount if not higher in the coming year.

Transportation Went up 100%

Transportation went up nearly 95% as this was the year I consistently took numerous cab rides due to movement problems. Still, I felt Singapore is a very convenient place without cars.

However, I really feel the difference when Uber and Grab came into the picture. I didn’t take much rides with discounts but the increase in availability is such a pleasure compare to a real uncertainty of not getting any cab in the past.

A Very Controlled Rich Life Living

It is always important to form meaningful categories for your spending. This allows you to understand what are distinctly different in what you spend on, versus the overall goal that you sought to achieve.

I always have 2 levels of spending:

- Survival – What you need to make ends meet and sustain life as a human being in a place you live in

- Rich Life – The things you do so that you have moments that you feel life is good and worth living

Due to much challenges in 2016, I decided to practice being conscious that if there are people not enjoying themselves around me, I will also restraint myself.

My Rich Life consist of the following categories:

- Gifts – $771/yr

- Clothing – $14.80/yr

- Hobbies – $521/yr

- Rich Entertainment – $45.60/yr

- Books and Magazine – $14.79/yr

This gives a total of $1367.20/yr or $114/mth.

If I were to reflect whether I lived a poor life, I think I didn’t.

Living a rich life is living a life with a purpose. Working on things that you feel purposeful about, then sprinkle with some meet ups that do not cost a lot and light YouTube watching, Pocket reading is quite the rich life.

How is my Financial Security Numbers Shaping Up?

When we know our survival expenses, from our overall expenses, we will be able to work out how much we need our wealth machine to generate, to give us a financial security.

This to me is also what I term our self-funded unemployment insurance because if you are unemployed, you could go find some bare minimum job that pays you less than your last job, but enough to cover the costs of some of your Rich Life spending.

(click to see larger)

Compared to my 2016 average monthly spending, my survival expense work out to be $1,285.00/mth. The annual amount is $15,420/mth.

To arrive at this amount, I evaluated and reduce some of the categories realistically if shit hits the fan during unemployment and when money is tight.

I will still get by, but we won’t eat a comfortable $650/mth but cut to $500/mth (trust me still a lot of food), less transport, and still have to pay for some home and personal utilities, household breakdowns and minimal hobbies.

If I built up $308,400 in my wealth machine, at a 5% rate of return, I would be able to generate the $15,420 to maintain a very minimalist living.

However, if I were to be more conservative, and use a lower rate of return of 3% instead of 5%, I would need $15,420 / 0.03 = $514,000 in my wealth machine. You will need more wealth if you are conservative to shift to lower volatility and more predictable financial assets.

The amount needed is a far cry from the $524,769 needed in my wealth machines, to pay for my 2016 expenses.

It is assuring to know that my wealth machine, have the potential to provide this amount of cash flow currently. I am still employed, but based on the formulas and figures, I am in a financially secure state whether the rate of return is 3%, 4% or 5%.

What if I were Single next time, what would my Financial Independence figure be?

Financial Independence is define as a step up from Financial Security, where the Wealth Machine is able to generate a wealth cash flow to cover my current standard of living.

We have already seen how much I need to be financial independent if I were to retire tomorrow. It is that $524,769 figure.

What I tend to war game, are scenarios that in the future when my dependents are not around, how much would I need.

We see one more row added, and the annual expenses for a single financial independence is $1680/mth or $20,160/yr. My wealth machine will need $403,200 to generate this amount at a rate of return of 5%.

Some Inescapable Lessons

There are always some takeaways from my annual expenses breakdown:

Some expenses are inescapable. When you develop prolong illness, no matter how you try to avert, you will still need a higher expense to pay out. Insurance does cover to a certain extend, and do ensure that you do a good job covering them. These expenses become part of life.

Your annual expenses, the size of your wealth and the rate of return of your wealth machine are linked.

The more you need, the larger your wealth machine needs to be. We see that how much we need to build up for retirement, financial independence or security will depend on how much we spend.

Wargaming your spending presents you ideas how much wealth you need. The exercise of trying to vary your expenses might make you learn more ways of living. Some will be acceptable, others will be ridiculous. However, the exercise would train your mind to be aware that in a lot of times, you are in control of how much wealth you need.

Conservative rate of return means you need a larger wealth. If you are so rich and that your annual survival expense is $16,000/yr, you just need $1,600,000 to provide your survival. If we are not so rich, we need to learn to build wealth better, build a sustainable wealth machine to generate a higher rate of return.

So how is your 2016 spending, did you choose to be more conservative in your spending due to the challenging economy? Are you facing some challenge meeting your targeted annual expense?

To get started with dividend investing, start by bookmarking my Dividend Stock Tracker which shows the prevailing yields of blue chip dividend stocks, utilities, REITs updated nightly.

Make use of the free Stock Portfolio Tracker to track your dividend stock by transactions to show your total returns.

For my best articles on investing, growing money check out the resources section.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- Should I Take Less Risk in My Fixed Income Allocation by Moving Away from a Global Aggregate Bond ETF? - May 5, 2024

- Singapore Savings Bonds SSB June 2024 Yield Climbs to 3.33% (SBJUN24 GX24060A) - May 3, 2024

- New 6-Month Singapore T-Bill Yield in Early-May 2024 to Stay at 3.75% (for the Singaporean Savers) - May 2, 2024

Rayray

Sunday 8th of January 2017

What do you eat, Kyith? XD

Kyith

Sunday 8th of January 2017

hi ray ray, vegetables, sweet potato and chicken in the morning, cauliflower meal prep in the afternoon, vegetables and chicken at night. you may be able to find out more here > https://investmentmoats.com/lifestyle-redesign/frugal-life-how-do-i-meal-prep-for-7-days-lunch-in-half-a-day-in-singapore/

Cory

Sunday 8th of January 2017

Hi Kyith,you are rather frugal. I could spent like $2.5 K monthly in recent years just for myself ...

I would also say due to larger wealth base, investment has been conservative for me . Maybe I need to strike a balance in everything in life.

Cory

Kyith

Sunday 8th of January 2017

Hi Cory, it depends, maybe i am used to a miser lifestyle so anything a little more is a bit rich already haha. A larger wealth base is always good to allow more changes, testing and mistakes haha.

Xie Hong

Sunday 8th of January 2017

Hope your family members enjoy the same way as you do in this journey . 😄

Kyith

Sunday 8th of January 2017

Hi Xie Hong, thanks a lot. I hope you and your family have a good Year of the Rooster!

Jared - SMOL

Sunday 8th of January 2017

Kyith,

I wish you good health.

Life may not always deal us a good hand, but you are making the best of what you got.

Respect your attitude.

Namaste.

Kyith

Sunday 8th of January 2017

Hi Jared, thanks a lot. Yes life doesn't always give you a good hand. its just that we need to learn to be flexible and forward looking and constructive. Concepts will change over time, after we have more hard knocks in life.

My Sweet Retirement

Sunday 8th of January 2017

I am quite amazed how low your monthly expenses are. I think reducing food intake in unhealthy although we are bent to reduce expenses.

Kyith

Sunday 8th of January 2017

hi My Sweet Retirement, you mean you are trying to reduce your food expenses is unhealthy?