In my last article, I look at whether we can create a health sinking fund to pre-fund our health and wellness expenses in financial independence.

When we do not have income coming in, and we do not know whether we will be able to accumulate again, how much should be inside a health sinking fund?

How conservative or less conservative should it be?

The first article focus only on one area where we need funding: Funding our health insurance plans, which is more commonly known as our shield plans.

We learn that the nature of cash flow needed in health insurance is unique in that the premiums are low when we are younger, very expensive when we are older, and that this premium schedule does not stay constant.

If we lump our health insurance expense needs together with our other consumption needs, it will be tough to model. If we compute how much we need based on our health insurance premiums next year, most likely we will end up underfunding our future healthcare needs.

Health insurance is probably not the only necessary insurance premium we need to save up for.

A lot of us got used to having riders on health insurance that offset a large percentage of our outpatient and inpatient hospital expenses. If we want that in our retirement, we got to pre-fund it as well.

So in today’s article, we are going to explore how much to set aside.

What are Health Insurance Riders and how important are these riders?

If you have purchased a shield plan from your private insurance provider, your adviser will ask if you wish to purchase a rider that comes along with it.

Here are some of the private shield plans in the market and their corresponding riders:

| Health Insurance | Rider |

| NTUC Enhanced IncomeShield | Deluxe, Classic |

| AIA HealthShield | VitaHealth |

| Aviva MyShield | MyHealth Plus |

| PruShield | PruExtra |

| GE SupremeHealth | GREAT TotalCare |

| Axa Shield | Enhanced Care |

They go by different names so to source out the materials is a problem sometimes as well.

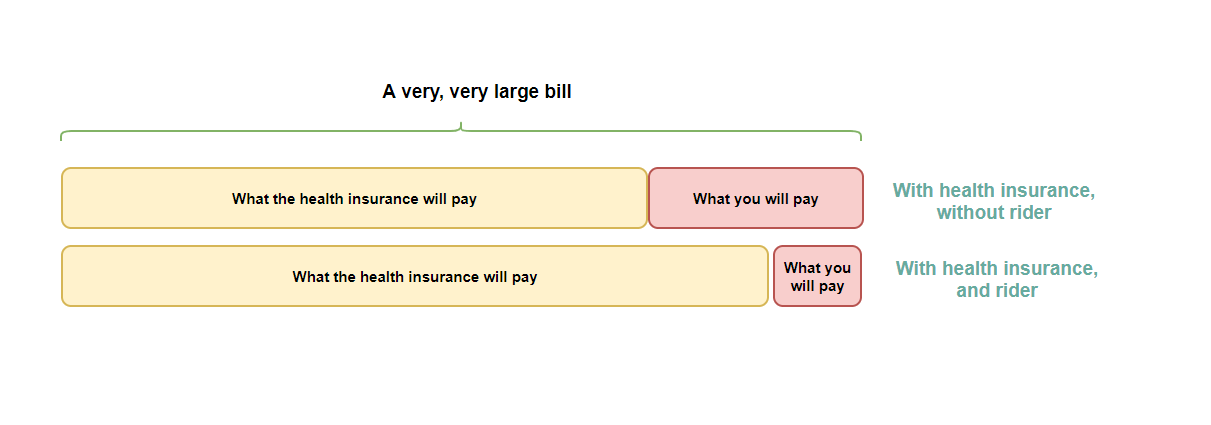

The primary role of your health insurance (your basic shield) is to ensure that if you get a catastrophically large hospital bill, it does not financially impair you.

So if the bill is $300,000, you would pay around $32,700 but paying $32,700 is far better than having to pay the full $300,000.

With a rider, it reduces the amount that you have to pay. Usually, these riders are able to reduce your out of pocket expense by 50% (in the example above, it would potentially cut your out-of-pocket expenses to $16,325).

For smaller bills that are less than your shield plan deductible (Say $1000), these riders can cut out-of-pocket expenses to maybe $500.

On top of that, each rider may have specific benefits that are different from other insurers.

These shield plan riders used to be very, very potent.

They are able to reduce your out-of-pocket expense to zero.

But this creates some perverse incentives such that the whole healthcare system became out of whack. Health care costs escalated, the shield plan and rider premiums escalated and there was much finger-pointing who is to blame for this shit that we are in.

So the government had it and mandated that everyone copay the bill. No more zero dollar out-of-pocket bills.

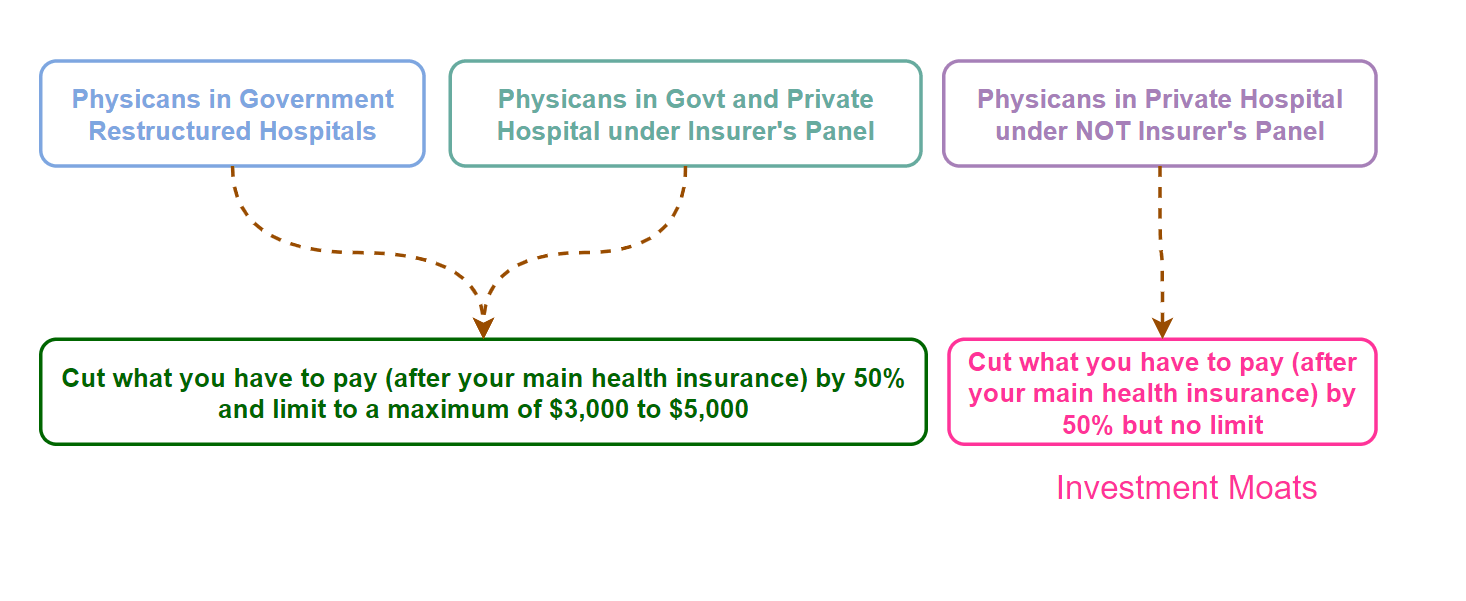

The amount of expenses these riders will offset depends on the quality of healthcare that you choose:

If you choose physicians in government restructured hospitals, specialists in restructured hospitals or private specialists that are under the insurer’s panel of approved private physicians, the riders can limit the amount of out-of-pocket expenses to $3,000 to $5,000 (depending on the plans chosen).

To do this, you would have to inform your insurer through each of their channels before you seek help from the hospital. This is so they can approve you and you will also have the peace of mind that your shield and rider will cover you well.

However, if you choose a private physician that is not part of the panel, while the rider will alleviate 50% of the costs, there will be no limit on the bill.

If we use the previous $300,000 before the health insurance bill example, the out-of-pocket expense would be cut from $32,700 to $3,000 if you have a shield, a shield rider, you have selected a doctor on the panel.

However, if the private doctor you choose is not on the panel, then the rider will still cut the bill to $16,325, but there will be no limit like the former.

Therefore, if your preference is for non-panel physicians, these riders are greatly nerfed (to the point I wonder if there is a valid reason to get them).

Certain private physicians and specialists choose not to be on the panel most likely because to be on the panel, you have to abide by a certain charge rate. Doctors with a great reputation and expertise may be underpricing their services this way. If the insurer includes the bill cost of these groups of physicians, the premiums would have to be more expensive.

Not just that, certain insurers like Great Eastern and AIA are practising claim penalties and no-claim discounts, similar to the prevalent system in the vehicle insurance world. This means that if you have claimed, your next year premium would be more expensive and if you did not make a claim, there will be a discount.

It all means that:

- The riders are more efficiently priced compared to the past.

- You need to be clearer about your healthcare preference.

If we go back to the role of the riders, it is to minimize out-of-pocket expenses. I would classify it as a good-to-have.

The Nature of the Growth of Health Insurance Shield Premiums Over Time

I wish to figure out how much in present value to set aside in a health sinking fund to pay for the rider.

In order to do that, we need to understand the nature of the premiums of these plans.

There are a few plans out there but I will use NTUC Enhanced IncomeShield Deluxe as an example.

Deluxe is the higher grade rider plan offered by NTUC.

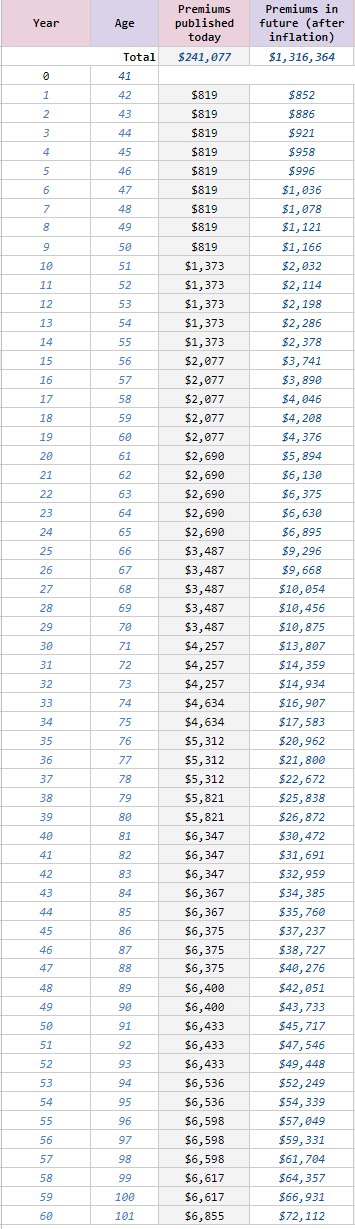

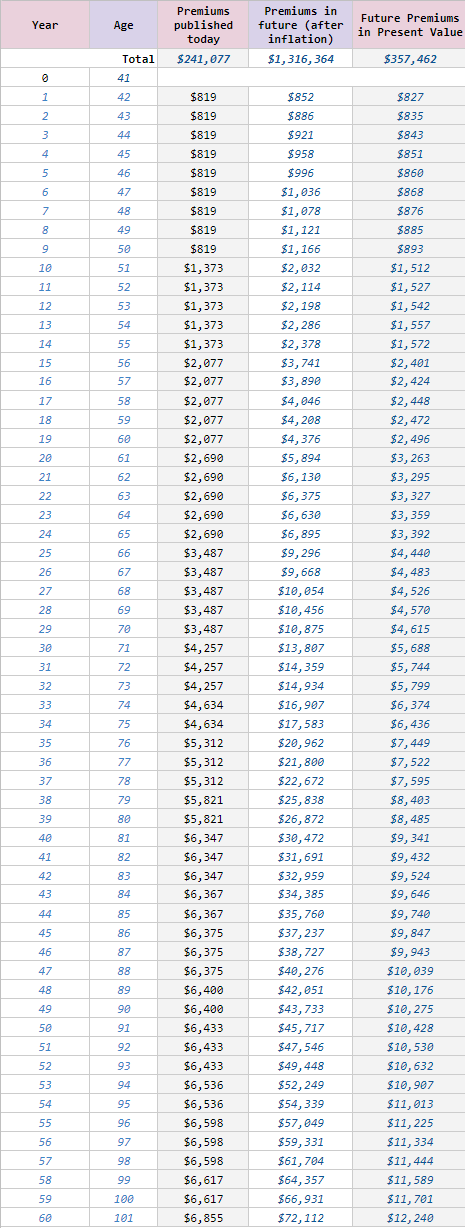

Here is the annual premiums taken from NTUC and the premiums growing at 4% a year:

The third column shows the premiums. As you can see, premiums are different for each age band.

And the premiums are damn fierce. For example, the annual premium for a 70-year-old is $3,487 a year. The premiums for the main health insurance at that same age is $2,241 a year.

It is more expensive than the main plan and if you add them together it’s $5,728 a year. The crazy thing is that paying this amount of premiums does not mean your out-of-pocket expenses will be very low if you choose a non-panel specialist. So it makes us wonder, is paying for the rider worth it at all?

Anyway, this premium does not stay static. In the past few years, certain parts of the tables are revised. The premiums go up at the whims of the healthcare system and insurers.

I have used a 4% a year compounded rate.

This means that when it reaches my 70 years old, instead of $3,487 in premiums, I may be looking at $10,875.

The total is a cool $1.3 million.

How much to set aside in the health sinking fund?

Similar to our previous article, we can assume a conservative 3% investment rate of return. We could invest in the same balanced or 70% equity 30% bond portfolio and drawdown from it.

Here is the table, including the present value of the amount needed in the sinking fund:

As a 41-year-old, I would have to set aside $357,462 in today dollars in the health sinking fund just to take care of the rider. If you think 3% is too conservative, and are more open to 5%, you will need $166k instead.

Here is the overview again:

If we were to summarize how much we need in our health sinking fund up to this point, it would be:

- Health insurance in Medisave: $45,300

- Health insurance in cash fund: $255,646

- Health insurance rider in cash fund: $357,462

The sum of money is becoming as big as our retirement fund!

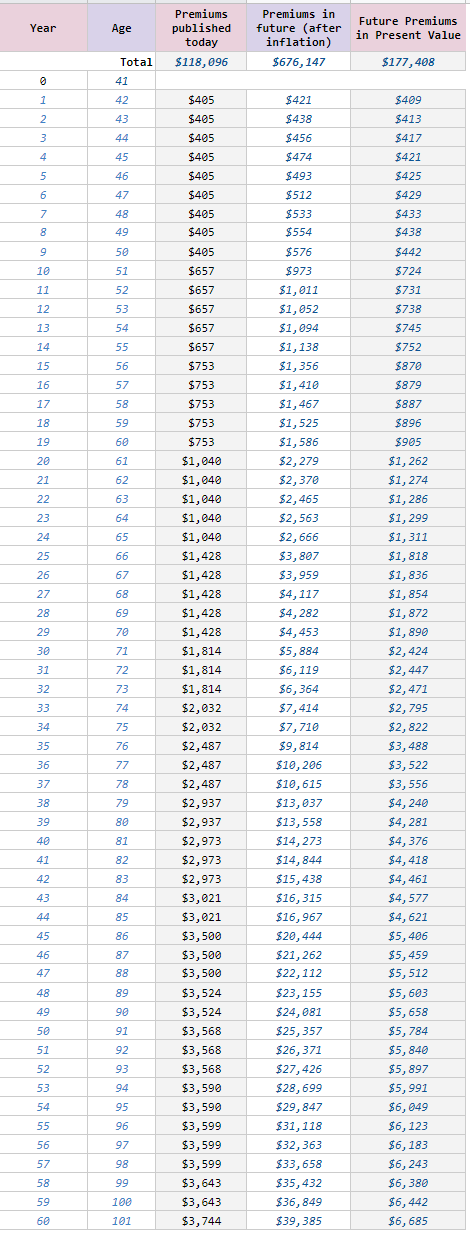

Reducing the grade of rider

For some insurers, you have the option to not choose the higher grade rider but the lower grade rider.

In NTUC’s case, that will be the Classic rider.

We can compute how much we need if we choose the Classic Rider:

Instead of $357k, your needs can be reduced by almost 50% to $177k.

Would it be a good idea to not set aside money for the health insurance riders?

I think this is an option.

And more and more, people need to ask what kind of healthcare scenario they are provisioning for.

If I have $377k, it begs the question would I be better using this to pay the premium, or just put in a balanced portfolio and use this to pay the out-of-pocket expenses if I need it?

In what world do we need to consistently pay for that rider? I think some people, need constant treatment, so this is valid for them.

But would all the costs be so uniformly big that it requires us to keep a constant rider? I am not sure.

You can let me know.

Conclusion

Just like my previous article on the health insurance sinking fund, the problem is less about the feasibility of early retirement.

The premiums that we need to set aside from 41 to 60 years old is not too challenging compared to the premiums after 60 years old.

Early retirement does steal precious years which you could use to build up the funds for health insurance.

The more I do this exercise, the more I realize that private insurance is a privilege. We can have a retirement, with our healthcare needs well taken care of.

We just need enough resources.

For most people, we would be struggling to accumulate enough just to pay for our expenses which exclude the health insurance premiums in retirement.

At some point, we will stop work, and we have to factor in these premiums so there is no running away from them.

More and more, we should encourage a conversation about our healthcare needs versus wants, the quality of our healthcare. It would allow us to optimize things better.

I think next up, let’s explore something simple, recurring medical needs.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- The Cheapest Way to Extend Your Laptop to TWODisplay that I Can Find. - April 29, 2024

- My Quick Thoughts on the Net Cash, 4% Yielding Boustead. - April 28, 2024

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024