Two years ago, a team of researchers from Lee Kuan Yew School of Public Policy conducted a set of research to figure out what is the minimum basic standard of living for older Singaporeans.

That study was great because the figures were put together in a very different manner, compared to what people try to infer from Singapore Statistics.

You can read about my commentary here.

The eventual report was useful to you for the following reasons:

- It gives all of us a glimpse of the priorities of folks that are going to retire.

- It provided a good trigger list for advisers to go through with their clients.

- Have a starting amount to begin a financial conversation with your peers or clients when discussing the topic of retirement.

Recently, the team of researchers sought to answer the same question but they expanded to target certain household configurations:

- A couple with two teenage kids.

- A single parent with a kid.

You can read the report here (which is better than the news commentary. The news commentary contain some errors due to how it is ported over)

I was intrigued to find out what would be the things needed as a basic standard of living for these two groups of people. And how much would that cost?

Like the previous study, the data, if done well, can act as a starting conversation about how much you need to accumulate for early retirement.

Parents with teenage children are the exact household configuration that we often get the most pushback on the blog every time we talked about financial independence.

When we can have a more accurate basic household budget of a couple with teenage kids, I can give a better estimation of the amount of money we need to accumulate for a leaner financial independence.

Even if early retirement is out of reach for parents with teenage kids, we can at least explain why it is so difficult to early retire.

In this article, we take a look at the budget, determine whether it is challenging for a couple with teenage children to retire early, and how much it costs.

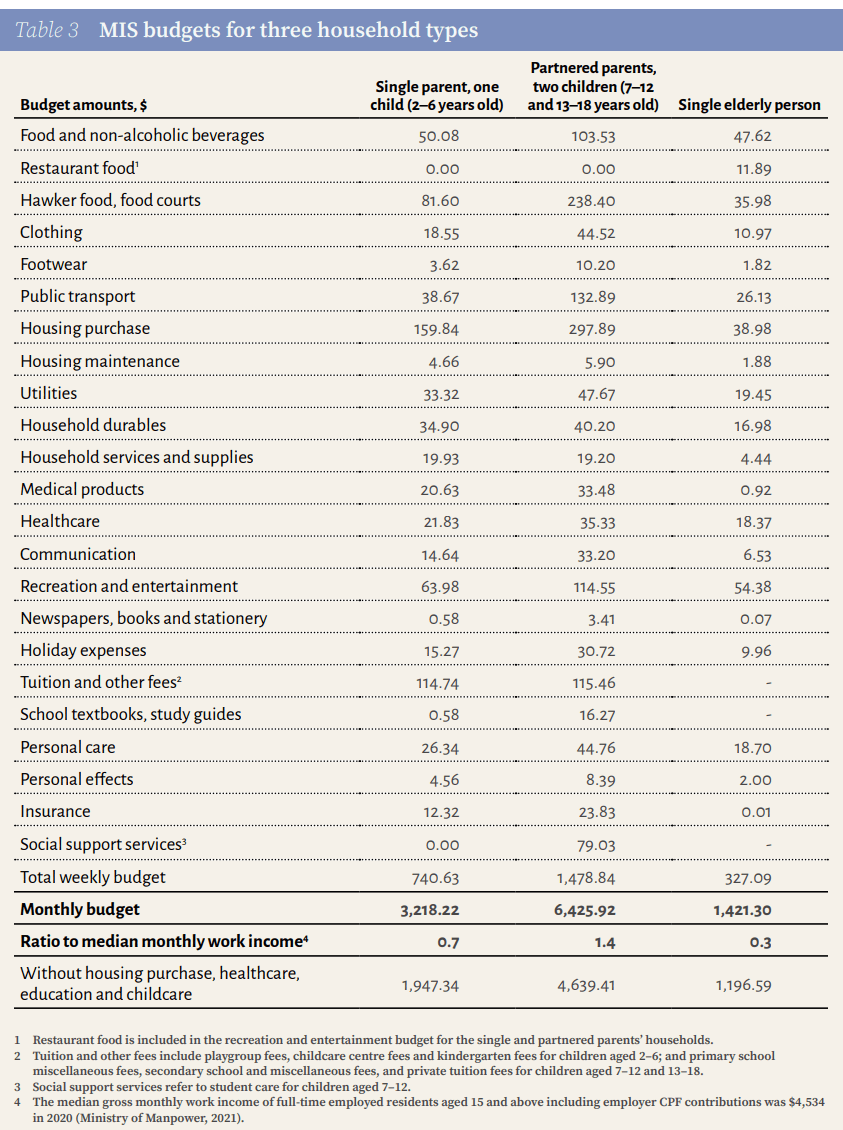

The monthly budget of a single parent partnered parents with two teenage children.

Here is the updated table of the monthly budget for three different household configurations:

The researchers included the single-elderly person they focus on in the last study. They updated the 2019 study with the latest figures.

So here we get the list of items considered to be basic for Singapore households and how much the lifestyle will cost.

A single elderly Singaporean will need $1421 a month while a couple with teenage children will spend $6426. If you are a single parent with a young child, your monthly budget will be $3218.

I will make my comment on whether the figures look too high or too low later.

Here are the revised numbers for the household configuration they did in 2019:

How much money roughly do we need to LEAN FIRE for a mature Singapore adult family?

Now let us estimate how much a couple like this need to early retire but based on the most basic living.

I consider this kind of living close to LEAN FIRE, a retirement early lifestyle choice where you accumulate enough wealth assets that can create a conservative income stream to pay for just your basic expenses.

(LEAN FIRE is one of the numerous financial independence lifestyle schemes that I introduced in the past. You can read this article to find out how much money you need to accumulate to be financially independent for the different desired lifestyles)

A couple like this should be around 45 years old and if we plan for immediate early retirement, the couple will need their money to last for about 55 years.

Due to the duration of income needed, we can use a conservative 3% initial safe withdrawal rate.

If a couple with to LEAN FIRE, they would roughly need: ($6426*12)/0.03 = $2.57 mil.

$2.6 mil sound like a crazy sum of money but if a couple is high earning enough and they control their expenses well, they can have a high savings rate. This may be possible.

We have heard of couples combining like $180k a year in after-tax household income and if your expenses are $80k, by 45-years-old is not out of the question by 45 you would have $1.5 million.

$1.5 million is not enough and most likely, Singapore couples will have their net wealth tied in properties. They will struggle to cash flow it for income.

This kind of LEAN FIRE is more possible if you have the same expenses but a combined household income after tax of $220k.

This is not out of the question, but it also means not all families can achieve this easily.

And not everyone wishes for a lifestyle that only caters to basic living.

How to Improve your LEAN FIRE outcome by adding some realism to the numbers.

In the past, I have explained that sometimes planning for a fixed amount of passive income might create more disappointment than reality.

This is because a few of your expenses today, is not perpetual:

- Children’s hawker food, restaurant food, public transport, social participation, clothing & footwear expenses

- Tuition and other fees

- School textbooks and study guides

- Housing purchase (if you are not renting)

For some, you would have paid off your mortgage by 45 years old.

Your children’s expenses may run for 7 to 12 years more. If we optimise this better, you would realize you might not need $2.57 mil to LEAN FIRE.

Let’s take a look at the table again:

Notice at the bottom, the group included a monthly amount without housing purchase, healthcare, education and childcare.

The group calculated the amount without these things because these are the items that are highly variable due to subsidies and state funding.

We cannot just say that for early retirement, we can exclude housing purchase, healthcare, education and childcare.

A better way would be to infer the following:

- Home mortgage paid off. This means we won’t have home purchases.

- All other expenses for children will last for a duration of 13 years.

- What is left after #1 and #2 is the basic need for the parents at about 55 years old.

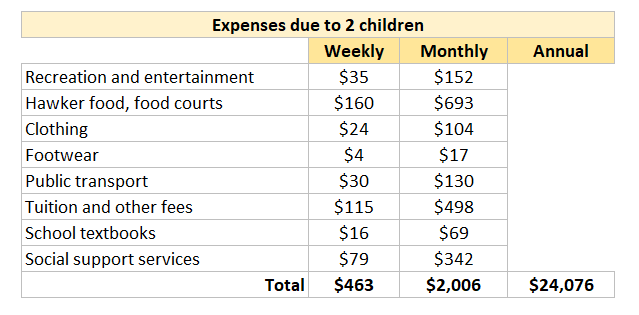

Here is my estimation (do note, this will not be 100% accurate because I will be calculating the difference in spending between some categories versus 2 times the expenses of a single elderly person.):

The home purchase will save about $1290 a month. We will deduct this from $6426 a month.

Here is my estimation of the difference between the expenses of parents with two teenagers and two times single elderly person:

Whoa! That is almost $2,006 a month. Let me be conservative and apply a 20% discount when deriving how much the two teenager will cost. That will come up to $1604 a month.

Let me summarize the LEAN FIRE configuration:

- Not renting and have paid off the mortgage.

- Capitalized 13 years of $1604 a month expenses upfront at 5% inflation rate. This comes up to a lump sum of $340,939. (Note this does not include university education cost)

- A LEAN FIRE Income need of $6426 – $1290 – $1604 = $3,532 a month for 55 years. At an initial safe withdrawal rate of 3%, you will need ($3,532 x 12)/0.03 = $1.4 mil

Instead of $2.6 mil, if we optimize how much we need, it comes up to $1.74 mil. That is almost $900k less.

In both LEAN FIRE examples, they do not include the future cost of university education. This means the cost probably will end up closer to $100,000 more (one child probably needs it soon the other one is about 8 years away).

If your household expenses today is $80,000 a year, then you would need roughly an average after-tax income of $190,000 a year to LEAN FIRE by:

- Paying off the mortgage of your HDB in 15 years.

- Saving $90,000 on average for 15 years at 4% compounded rate of return.

Most likely, you will need roughly an ending after-tax household income of $300,000 a year.

It feels to me at this point that LEAN FIRE at 45 years old is more for those who earns a good income and are able to control their expenses well.

A little insight on how the household budget is derived

I watched a Dr Wealth video titled What you need to know about marriage and money and realize that not many people read the actual report.

Due to that, many don’t have an idea how those budget were derived. They thought that its done by aggregating the responses of a wide survey.

The research team uses a UK Minimum Income Standard (MIS) methodology to go about deriving the budget.

The MIS approach gather both the views of experts and people on the ground.

Basically, the team gather those people on the ground and broken into focus group. Participants will try to discuss and create the needs of these few household configuration.

So it is less about what the participants spend, but tapping their aggregate real life experience, piece out the line-items and configuration what is needed. For example, what will constitute a survival meal? Is tuition necessary?

Then the team will consult experts such as dietician to firm up what should be a balanced diet and the team will individually sourced how much these line items cost.

You can read more here:

Forming a budget this way is less of what we are spending today BUT what should form the bare minimum, satisfactory household budget.

There were some assumptions to be made and as I guess, it is likely a process that is filled with enough frustrations.

The housing purchase assumptions may show us the level of details they go into:

MAS Response to the Household Budget Study

Apparently, MAS thinks this study is not an accurate reflection of basic needs. Straits Times have a commentary on this.

Here are some of the points:

- The researchers included discretionary expenditure items such as private enrichment classes, jewellery, perfumes, and overseas holidays in the estimates.

- They considered mortgage payments to be an expenditure. MAS think that this helps build housing equity.

- The 2017/18 report would have concluded that the figure of $1600 a month to be closer to the average household spending. This means that it is in excess of the basic needs of an average household.

- The amounts reflect more of a median earner, not low-income families receive.

If you ask me, I think the response is damn defensive.

The derived figure is based on line items Singaporeans think its basic. These are the stuff that they argue in not just one but a few focus groups.

Who do you think has the right to determine what is considered basic? The people sitting on their ivory tower or the people living through these kinds of lives?

To most of us, we are less interested in what is low income or high income. This is an exercise to determine what is the basic kind of life.

If the people say that this is considered basic and you need an average household income to be able to live it, then that means the lower-income is having a shitty life isn’t it?

As someone who tried to piece all these things together, I gain more appreciation for what this NUS and NTU team tried to do than what the government has put out in their stats.

Trying to deconstruct things from the SingStats is just pure bullshit sometimes. At least this one has more context.

Perhaps the most telling thing is: This study tries to focus on our living standards. MAS response keeps going back to low income. This is as if the only party that the government should care about is the low-income and if you belong to the upper quartiles, our quality of living is less important.

Cannot be right?

Conclusion

In these two studies, the people participating in the focus groups determine what is the most basic lifestyle for an elderly person, a couple of elderly people, a single spouse with an infant kid and a couple with two teenagers.

The monthly income that they determine is rough:

- Single elderly: $1421 a month

- A couple of elderly: $2450 a month

- Single parent, one young child: $3218 a month

- Two-parent, two teenagers: $6426 a month

Your fellow Singaporeans determine the type of expenses that is needed and the team cost it accordingly.

A couple with two teenagers can early retire at 45 years old. However, they would eventually need to accumulate closer to $1.84 million. You would have to pay off the mortgage of your 4-room HDB flat and also includes the tuition fee of the two teenagers.

The couple should have an after-tax income of between $100,000 to $300,000 between the age of 30 to 45 years old. This allows them to have an average savings rate of at least 45%.

It should be noted that the focus group determines a budget based on basic needs. If your desired lifestyle is more extravagant, the amount you will need to save up is higher.

This study shows that the elderly need to have at least the full retirement sum (FRS) in both their CPF so that they will eventually have a life-long income to cover their basic expenses.

It also shows how challenging it can be for a single parent to bring up one child.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

- The LionGlobal APAC Financials Dividend Plus ETF Won’t Give Singapore Investors 5% Dividend Yield Always. Further personal thoughts (with some data). - April 13, 2024