Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield

0 Comments

In BlackRock Chairman and CEO Larry Fink’s 2024 letter to shareholders, he highlighted potentially countries took a peep at the U.S. and wonders what they can do to make themselves more resilient.

And the key may be to have stronger capital markets:

Last year, I spent a lot of days on the road, logging visits to 17 different countries. I met with clients and employees. I also met with many policymakers and heads of state, and during those meetings, the most frequent conversation I had was about the capital markets.

More and more countries recognize the power of American capital markets and want to build their own.

Of Saudi Arabia, Japan and India:

In Saudi Arabia, for example, the government is interested in building a market for mortgage securitization, while Japan and India want to give people new places to put their savings. Today, in Japan, it’s mostly the bank. In India, it’s often in gold.

When I visited India in November, I met policymakers who lamented their fellow citizens’ fondness for gold. The commodity has underperformed the Indian stock market, proving a subpar investment for individual investors. Nor has investing in gold helped the country’s economy.

I think that if your stock market is doing so well, then India doesn’t have similar problems but Larry Fink expands upon this:

Compare investing in gold with, let’s say, investing in a new house. When you buy a home, that creates an economic multiplier effect because you need to furnish and repair the house. Maybe you have a family and fill the house with children. All that generates economic activity. Even when someone puts their money in a bank, there’s a multiplier effect because the bank can use that money to fund a mortgage. But gold? It just sits in a safe. It can be a good store of value, but gold doesn’t generate economic growth.

This is a small illustration — but a good one — of what countries want to accomplish with robust capital markets. (Or rather, of what they can’t accomplish without them.)

Of Japan’s move to NISA Savings Account:

Last year, Japan passed a demographic milestone. The country’s population has been aging since the early 1990s as the pool of working-age people has shrunk and the number of elderly has risen. But 2023 was the first time that 10% of their people exceeded 80 years old,6 making Japan the “oldest country in the world” according to the United Nations.7

This is part of the reason the Japanese government is making a push for retirement investment.

Most Japanese keep the bulk of their retirement savings in banks, earning a low interest rate. It wasn’t such a bad strategy when Japan was suffering from deflation, but now the country’s economy has turned around, with the NIKKEI surging past 40,000 for the first time this month (March 2024).8

Most aspiring retirees are missing out on the upswing. The country didn’t have anything resembling a 401(k) program until 2001, but even then, the amount of income people could contribute was quite low. So a decade ago, the government launched the Nippon Individual Savings Accounts (NISA) to encourage people to invest even more in retirement. Now they’re trying to double NISA’s enrollment. The goal is 34 million Japanese investors before the end of the decade.9 It will require the Japanese government to expand their capital markets, which historically had very little retail participation.

Larry Fink spent some time to explain about the capital markets and why it may be a reason US could have bounced back better:

In finance, there are two basic ways to get or grow money.

One is the bank, which is what most people historically relied on. They deposited their savings to earn interest or took out loans to buy a home or expand their business. But over time a second avenue for financing arose, particularly in the U.S., with the growth of the capital markets: Publicly traded stocks, bonds, and other securities.

I saw this firsthand in the late 1970s and early 1980s when I played a role in the creation of the securitization market for mortgages.

Before the 1970s, most people secured financing for their homes the same way they did in the Christmas classic It’s a Wonderful Life — through the Building & Loan (B&L). Customers deposited their savings into the B&L, which was essentially a bank. Then that bank would turn around and lend out those savings in the form of mortgages.

In the movie — and in real life — everything works fine until people start lining up at the bank’s front door asking for their deposits back. As Jimmy Stewart explained in the film, the bank didn’t have their money. It was tied up in somebody else’s house.

After the Great Depression, B&Ls morphed into savings & loans (S&Ls), which had their own crisis in the 1980s. Approximately half of the outstanding home mortgages in the U.S. were held by S&Ls in 1980, and poor risk management and loose lending practices led to a raft of failures costing U.S. taxpayers more than $100 billion dollars.2

But the S&L crisis didn’t cause the American economy lasting damage. Why? Because at the same time the S&Ls were collapsing another method of financing was getting stronger. The capital markets were providing an avenue to channel capital back to challenged real estate markets.

This was mortgage securitization.

Securitization allowed banks not just to make mortgages but to sell them. By selling mortgages, banks could better manage risk on their balance sheets and have capital to lend to home buyers, which is why the S&L crisis didn’t severely impact American homeownership.

Eventually, the excesses of mortgage securitization contributed to the crash in 2008, and unlike the S&L crisis, the Great Recession did harm home ownership in the U.S. The country still hasn’t fully recovered in that respect. But the broader underlying trend — the expansion of the capital markets — was still very helpful for the American economy.

In fact, it’s worth considering: Why did the U.S. rebound from 2008 faster than almost any other developed nation?3

A big part of the answer is the country’s capital markets.

In Europe, where most assets were kept in banks, economies froze as banks were forced to shrink their balance sheets. Of course, U.S. banks had to tighten capital standards and pull back from lending as well. But because the U.S. had a more robust secondary pool of money – the capital markets — the nation was able to recover much more quickly.

Today public equities and bonds provide over 70% of financing for non-financial corporations in the U.S. – more than any other country in the world. In China, for example, the bank-to-capital market ratio is almost flipped. Chinese companies rely on bank loans for 65% of their financing.4

In my opinion, this is the most important lesson in recent economic history: Countries aiming for prosperity don’t just need strong banking systems — they also need strong capital markets.

That lesson is now spreading around the world.

Many may wonder how digitalisation or fintech is going to weaken traditional bank but if the governments are thinking what Larry Fink is thinking, it is to successfully promote a secondary stream of economic lifeblood to ensure that the multiplier effect doesn’t get killed off easily.

Make the economies less reliant solely on banks.

To be fair, it is not like this isn’t prevalent. We are hearing lending from other sources but is it recognized or done enough to a certain degree that it thrives?

I have always view the stock market as a secondary market to exchange ownership and therefore, I cannot understand how the stock market can make people wealthy other than buying the stock at certain point and selling it, or being paid dividends. Indirectly, I always wondered besides the initial public offering, or the rights issues, placements, how does companies thrive.

Until I realize there is a very strong wealth effect if the stock market does well.

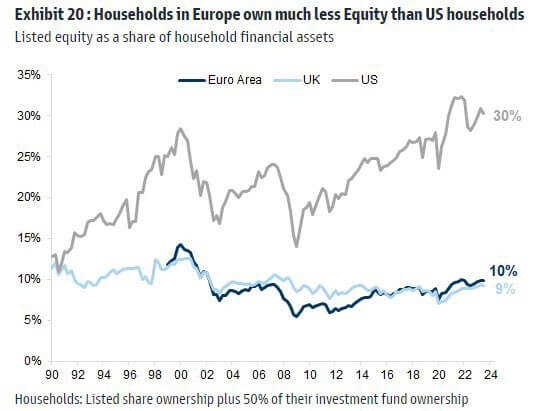

Stock Ownership by the population in the US is higher and thus when the market does well, the population spend more.

I happen to come across this illustration above that shows the US household ownership of equities as a contrarian indicator, but we can take the opportunity to see the different levels of ownership.

In Singapore, most of our money is in cash & savings, property and CPF.

As the US stock market is so thriving, even companies that were suppose to list in their home country is also listed in the US. You have companies like Sea Ltd, Spotify listing there because they can raise more money and have more attention.

Stock Market Reform in Japan

But to make your domestic markets thrive is no easy feat.

They may involve serious reform to your own public market.

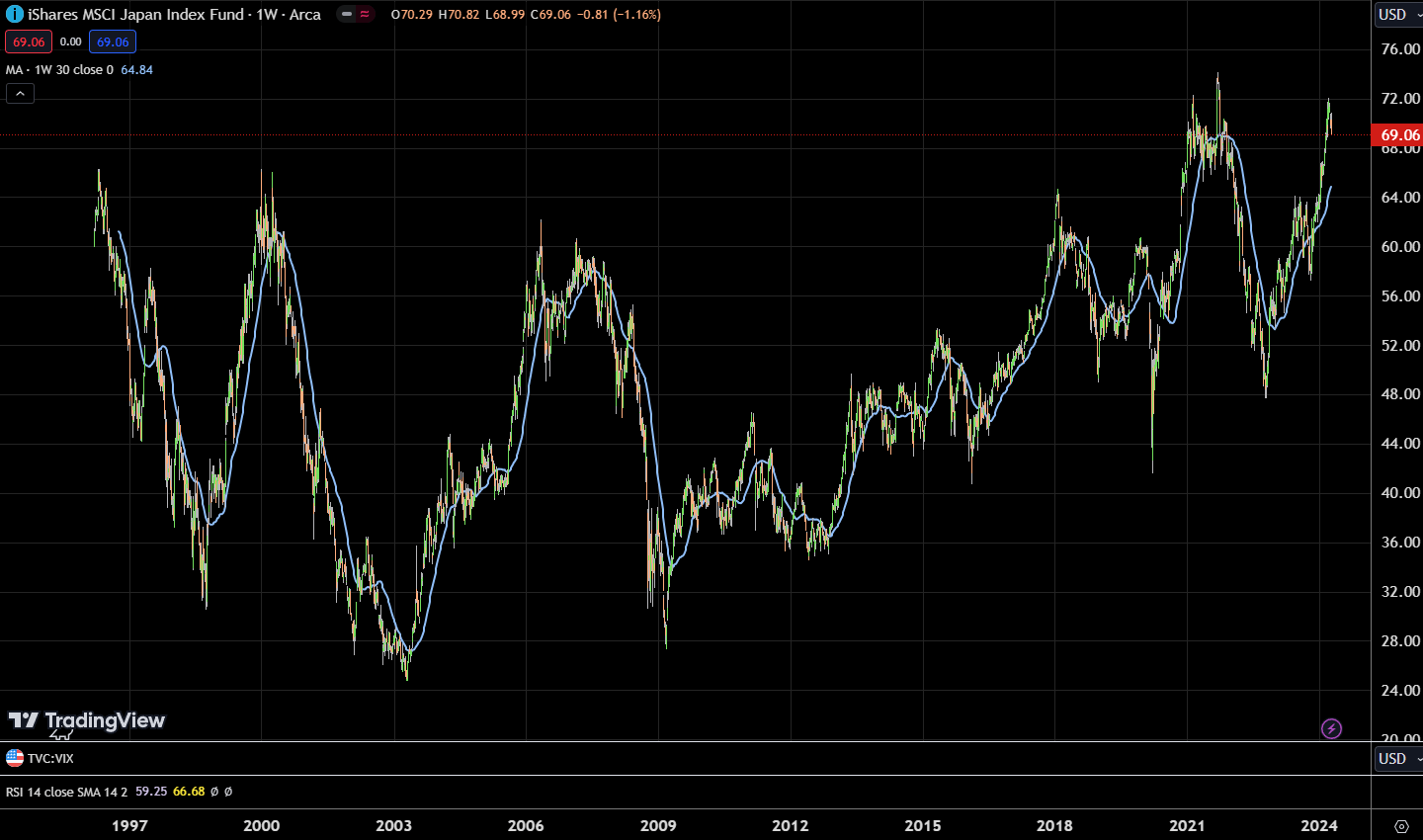

Japan may be the poster child. Their markets have been doing well in the past decade. Volatile but looks to be trending up:

Also playing a role is the Tokyo Stock Exchange’s push for companies to boost their value, urging leadershipto run their companies with investor expectations for returns in mind. Businesses that need to spend down their cash to boost capital efficiency are returning money to shareholders.

Trading house Sojitz, which targets lifting its market valuation above its book value by the end of fiscal 2023, announced a 16 billion yen share buyback as well as a 5-yen dividend hike in February. Osaka Gas has announced hikes to 72.5 yen this fiscal year and to 95 yen in fiscal 2024.

Several companies with price-to-book ratios below 1 have unveiled buyback plans. Honda Motor announced a 50 billion yen share buyback last month after already repurchasing around 200 billion yen in stock earlier this fiscal year.

“We’ll accelerate our efforts to improve capital efficiency with an eye toward raising our corporate value,” Chief Financial Officer Eiji Fujimura said.

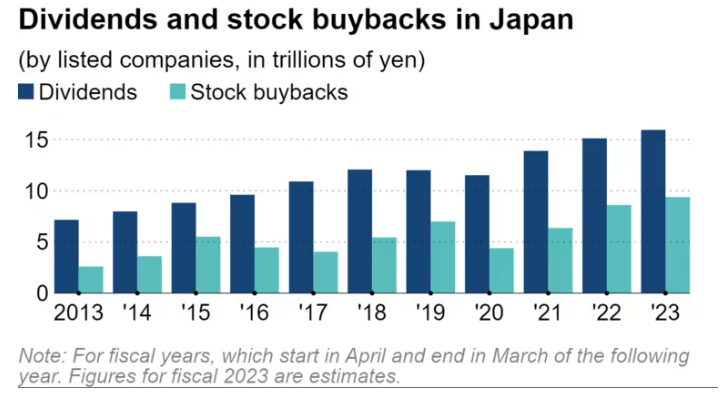

Total shareholder yield as a percentage of net profit looks set to hit 54%, down 2 points from fiscal 2022, as earnings are growing faster than returns.

Japan still lags the U.S. and Europe, with companies in the S&P 500 and Stoxx 600 returning nearly 100% and just under 80% of net profits to investors, respectively, QUICK-FactSet data shows. Nonfinancial companies in Japan had a record-high total of about 106 trillion yen in cash on hand at the end of last year, and may face pressure to use it for shareholder returns.

What is the right return to shareholders?

Kyith will argue it is free cash flow yield. But more and more, buybacks is being looked at as a form of return. Companies are more confident to pay out dividends and buyback their share if they feel that they have money to spend.

So the buyback + dividend yield, or what Japan terms as payouts to shareholders, is a good way to look at shareholder returns:

Payouts to shareholders by listed companies in Japan are expected to reach an all-time high of about 25 trillion yen ($165 billion) for the fiscal year ending this month, amid growing earnings as well as pressure to use capital more effectively.

The total, which includes dividends and share repurchases, was calculated by Nikkei from 2,300 companies that close their books in March. The dividends are based on QUICK Consensus analyst forecasts for companies that have not provided estimates, and account for stock splits and reverse stock splits. The buybacks cover tender offers and plans disclosed since last April.

Dividends are set to grow 6% to about 15.9 trillion yen, and repurchases by 9% to 9.3 trillion yen, both record highs. A total of 360 companies have raised their planned dividends since the end of 2023, adding about 200 billion yen to the total payout, and share buyback plans worth 1.42 trillion yen have been announced since January.

The rise in returns will benefit retail investors, who are being encouraged to participate in the stock market through channels such as the revamped Nippon Individual Savings Account tax-exempt investment program.

Individuals now own about one-fifth of all listed shares in Japan. Based on these figures, roughly 3 trillion yen in dividends alone would go to households, equivalent to about 0.5% of Japan’s gross domestic product.

In Arcus Investment Insights December 2023, Peter Tasker listed five fitting scenarios for the year of the dragon. They are Japan-oriented. One point talks about the NISA and how it may benefit Japan stocks:

I would argue that Japan is slightly behind time on this. The bigger impact is the reforms the exchange is pushing to make shareholder returns more appealing and, therefore, making participation higher.

This is what Japan is doing much better than Singapore.

What has this got to do with Singapore?

I can see some minister or some weird taskforce being created and some poor scholar is tasked to take a look at having a good second engine to the banking system. If they deem that this is needed and there is enough support, there may be a massive push.

There is network effects in a marketplace.

You will need the companies to be valued and traded efficiently. Public crowd needs to want the stocks enough.

But to do #1, you need to show visible shareholder returns, and usually that is in the form of buyback and dividends. Companies need to make them more attractive.

In Asia, there is a lot of traditionally family companies that have their own agenda other than the shareholders.

It is for the government and exchange to try and change that.

Equities if remain undervalue may be revalue to what they are worth eventually when that happens. The question is when that will happen and I am afraid impatient Millennial, Gen X or Gen Z investors would not bite.

Equities is a long game that to capture the value, you might need to hold 20 years. Thus, only those with deep pockets and with patience will be rewarded. But the companies must be worth something.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.