One of my readers asked me this question: “Kyith if you are investing for your own retirement, will I be concerned about the foreign exchange since you have invested in so many USD denominated ETFs? Would it be better to go with an SGD denominated ETF?”

This is a good question that is on the mind of many investors. Some of them were influenced by friends and the media to invest in say, the iShares Core MSCI World UCITS ETF (ticker: SWDA). SWDA is an ETF that allows you to own a basket of stocks (about 1600 of them) that mimics the MSCI World.

The ETF, listed on the London Stock Exchange, is domiciled in Ireland and is more dividend withholding tax and estate tax efficient (you can find out more about dividend and estate tax efficiency in my article here and here respectively).

These ETFs are denominated in USD or EUR and this could be a concern for some investors.

I wrote about whether there is a currency risk when you invest in funds denominated in other currencies for Providend before but I feel like I kinda fxxk up the article. Every time I need to write over there in a formal manner, I seem to fxxk it up more.

So let me try to answer this question the Investment Moats way.

The short answer is that currency risk does matter but it has got less to do with the currency your fund is denominated in. An investor needs to take note of the currency fluctuations of the assets they invest in versus were the currency of where they will spend the money.

Now let me see if I can expand further.

You need to have an idea of which currency you would eventually need to spend your money in

Currency exists in a pair:

- USD / SGD

- EUR / USD

- CHF / SGD

A currency depreciates or appreciates against another currency.

If the whole world uses one currency, then there is nothing that it depreciates or appreciate against. Well, technically, someone can come up with a digital currency and measure your currency against that.

If you are concerned about currency devaluation, you would need to be very surgical about what you are concerned about.

For most of us Singaporeans, we are building wealth and eventually retiring in Singapore, spending our expenses in SGD.

For some of you, you will be going back to Europe or Australia and will be spending your money in EUR and AUD.

You are likely concerned whether your investments grow well, in terms of the currency you need. That means SGD for Singaporeans, EUR and AUD for the respective expatriates.

Unit Trust and ETFs can have different currency denominations but the underlying assets are the same.

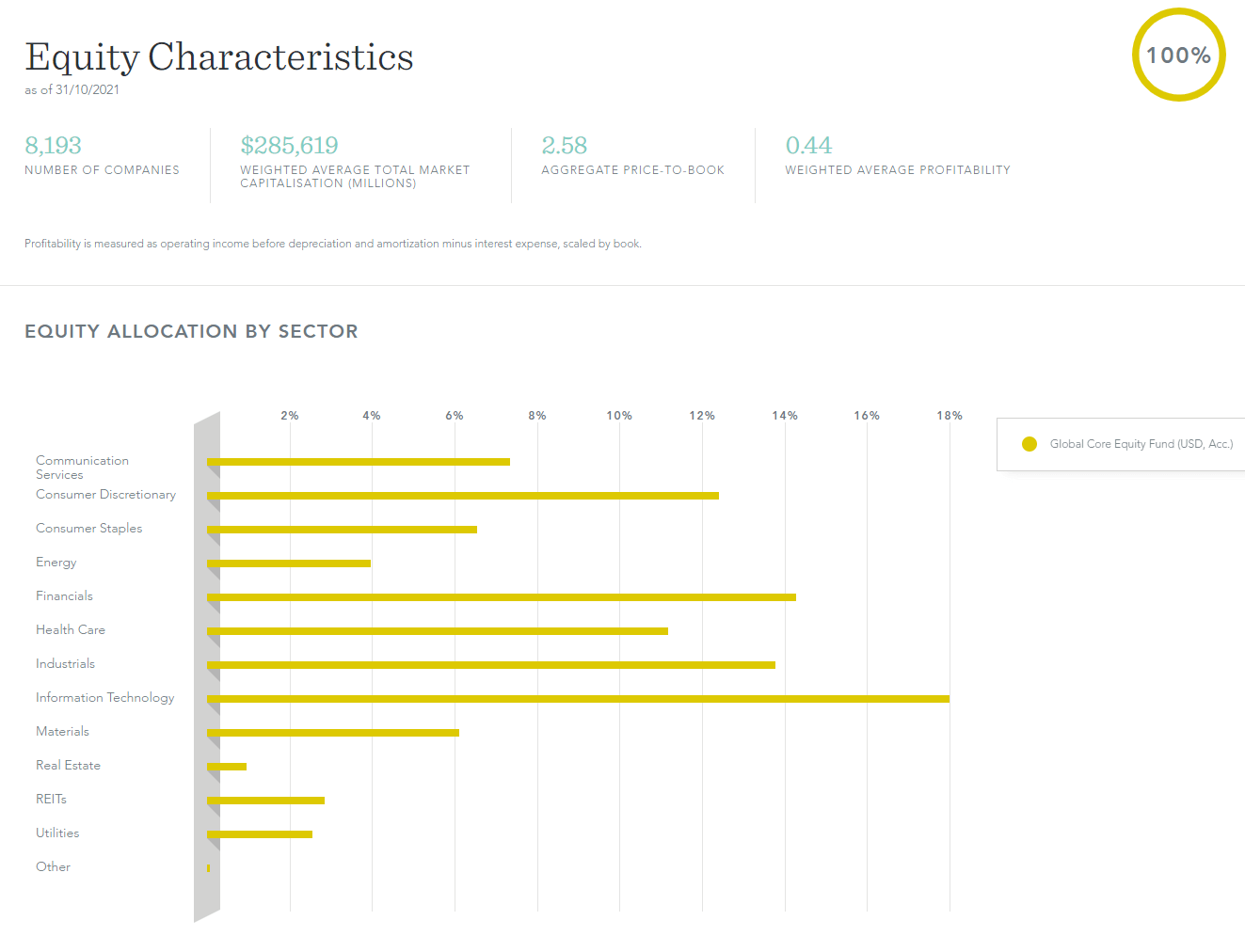

I think the best example that I can use to describe this is the Dimensional Global Core Equity. (You can read my comprehensive write-up about Dimensional Fund Advisers here)

The Global Core Equity is like the core equity fund that a few firms locally use to design their strategic portfolios for clients (Providend, MoneyOwl, Endowus).

By investing in the fund, you indirectly own more than 8,000 stocks diversified across the world.

Global Core Equity has a few different currency share classes. Let us focus upon EUR, GBP, JPY, USD and SGD.

Suppose you are a Singaporean investor who wishes to find the ideal fund to invest in, to accumulate towards retirement.

You decide to spread $1 million between these 5 different currency-denominated Global Core Equity Funds on 1st August 2017.

Your return for the 5 funds over roughly 4 years will be like this:

| Fund | Annualized Return | Cumulative Return |

| Global Core Equity EUR | 13.1% | 68% |

| Global Core Equity GBP | 11.5% | 59% |

| Global Core Equity JPY | 13.3% | 70% |

| Global Core Equity USD | 12.5% | 65% |

| Global Core Equity SGD | 12.3% | 64% |

The underlying assets are the same 8,000 stocks, selected with the same Dimensional factor algorithms, executed the same way.

The JPY fund reaps the highest return while the GBP one with the lowest return.

Assume that you decide to retire today and need to sell off the fund and convert it back to SGD.

Here is how these 5 funds performed, when denominated back to SGD:

| Fund | Annualized Return | Cumulative Return |

| Global Core Equity EUR | 12.3% | 64% |

| Global Core Equity GBP | 12.3% | 64% |

| Global Core Equity JPY | 12.3% | 64% |

| Global Core Equity USD | 12.3% | 64% |

| Global Core Equity SGD | 12.3% | 64% |

When you get the money in SGD, you will get back the same amount. The JPY fund, while earning more than 64% is now lesser in terms of SGD. The GBP fund, while earning less at 59% is now more.

End of the day, whichever currency-denominated fund you invest in, you get exposure to the same curated strategy.

Comparing your local investments against investments overseas

Many folks like to shit on Singapore stock investments but objectively it is not right to quote those returns in USD then compare them to returns in SGD.

Here are the returns of the MSCI Singapore IMI index and MSCI World IMI index in both USD and SGD from 2000 to today (Oct 2021) (Note: IMI stands for the investable market indexes which cover large, mid, small-cap securities in the region. It will cover more stocks.):

| Index | Annualized Return | Cumulative Return |

| MSCI Singapore IMI Index SGD | 4.6% | 167% |

| MSCI World IMI Index SGD | 5.0% | 187% |

| MSCI Singapore IMI Index USD | 5.6% | 230% |

| MSCI World IMI Index USD | 6.0% | 255% |

A common comparison would be a Singapore SGD index against an MSCI World or S&P500 USD index.

That comparison would yield 4.6% versus 6.0% or 167% versus 255%.

If we compare using the same currency, the difference is smaller. This is a period where when the MSCI World did poorly, Singapore did well, and when Singapore did poorly, the MSCI World did well.

If you have overseas property, ETF that is globally diversified, or which own a basket of stocks that earns in overseas currencies and you wish to evaluate against local investment, you need to do apples to apple comparison.

The Real Comparison is a Basket of Currencies Versus Investments Denominated in Singapore Dollars

An ETF owns a basket of stocks that earns and are individually denominated in different currencies.

The MSCI World is made up of about 64% US stocks and 36% in other international stocks.

If you are concerned about an ETF like SWDA, you are concerned about how a basket of 64% USD + 36% other currencies will do against SGD.

What if USD/SGD depreciate from 1.37 to 1.00?

Is that a real concern? Yes, that is a real concern.

But we have got to be clear about the concern. It is not so much the fund denomination we should be worried about but the underlying stocks.

If the cash flows of the business are paid in USD, all else equal, the business should be valued less. There is a real possibility that the investment will do poorly versus your Singapore investments such as your REITs which tend to average 6% a year in SGD.

So why do we invest in investments overseas?

For a few good reasons:

- After considering foreign exchange fluctuations, the expected returns are still better.

- You wish to mitigate single-country risks

Currency risk is real.

Case Study: The Investor Who Invest 100% of His Wealth in Turkey

Imagine you been in Turkey in 2000 and think that the economy will do well. So as a Singaporean, you decide to invest $1 million in the MSCI Turkey Index in 2000.

Here is your return:

| Index | Annualized Return | Cumulative Return |

| MSCI Turkey IMI (Try) | 12.1% | 1116% |

| MSCI Turkey IMI (SGD) | -2.7% | -44% |

If you view in the Lira, your 20-year investment would have been splendid. $1 mil in Lira would be worth a lot!

But as you are getting ready for retirement in 2021, you realize to your shock that after 20 years, you only get back S$560,000!

In SGD, you lost 44%.

How can the Turkey interested investor do better?

He could invest in an MSCI Turkey Index fund Hedged to SGD or USD.

When an index fund or ETF is hedged, the fund pays for some cost in exchange to eliminate the forex issues.

Investing in a fund that is hedged gives you exposure to the underlying businesses without the currency risk.

Most equity funds are not hedged. Only selective funds are hedged.

Most often, if a fund’s focus is in a region that historically has periods of big currency devaluation against where the fund is distributed, the manager should consider whether to hedge the currency of the fund.

Hedged funds are more prevalent among bond funds.

This is because bond returns are lower, and these currency fluctuations can just wipe off the return.

Conclusion

Singapore is one of the countries with the strongest currency.

Therefore, it means that your investments overseas have a higher hurdle rate.

When the S&P 500 was not doing well, the USD was depreciating against the SGD. Basically, the performance of your investment is doubly the worst.

We are not sure what the future holds, but foreign exchange stuff is something that we have to contend with.

Have an idea what currency you would eventually spend in.

Learn to measure your investments based on the right metrics. It should be less on what the fund or ETF is denominated in but more of the underlying investment performance versus the currency you would spend in.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Jaime

Sunday 28th of November 2021

Across a longer time period, it does appear that major currencies such as USD/EUR/GBP are depreciating against SGD historically.

Assuming this trend continues well into the future, does it also mean that Singaporean investors will actually be “worse off” in terms of return as time goes by?

Would love to hear your thoughts on this, thanks.

Kyith

Tuesday 30th of November 2021

In a way I think it does put the huddle rate higher. But for some, the expected investment returns might still make sense. if you can make 20% a year for 5 years, even if the currency is weaker, that might still be a better risk-adjusted investment. But i think sometimes factoring in this strong SGD, we tend to rate some overseas market return a tad too high.

retirewithfi

Sunday 28th of November 2021

For the sake of completeness, perhaps you should also mention S$NEER and how MAS manages SGD against the trade weighted basket of currencies of SG's major trading partners.