Back in the days when I was investing in funds, I had this problem of finding the ideal low cost unit trusts that I could invest in.

In Singapore, there was not a lot of solutions. Back in 2003, exchange traded funds was not prevalent yet, and have not developed into the mindshare that they have now.

The books and research that I had carried out leads me to conclude that for investing to work out well, we need to respect the cost that we pay for our investing solutions, and that it is damn tough for active fund managers to consistently outperform the benchmark.

What is highly recommended in books, the low cost Vanguard funds, was not available in Singapore.

We can however, invest in Lion Global’s Infinity Series. This is a wrapper fund that allows you to invest in Vanguard sub funds that follows the S&P 500 index, MSCI Europe index and MSCI World index.

The expense ratio is “low” at 1%+- but it is better than nothing. (You can check out my very detail look on the Infinity Global Stock Index Fund here)

In my research, I had often come across a unique company call Dimensional Fund Advisors or DFA for short. There is a lot of research pitting Vanguard funds against DFA funds.

What caught my attention, was that this was one of the loudest competition, that is not Vanguard versus active unit trust.

Also, the follow intrigued me:

- Their returns measured up to the Vanguard funds for a longer term basis

- This is despite them having an adviser wrapper fee

- Their fund’s expense ratio is low

- You could only purchase these DFA funds through a DFA trained adviser

Of course, to my disappointment, I could not access them as well.

Fast forward to 2019, we are swamped by exchange traded funds (ETF). We can now buy ETF through our brokers. We also have a few robo advisers such as Stashaway, Smartly, and Autowealth.

It is certainly easier to be a passive wealth builder in this age in Singapore than years ago.

In recent times, Vanguard, who had an office for higher net worth individuals have closed their office in Singapore.

To my surprise, DFA have, through their advisers, are starting to make their presence felt in Singapore.

As a finance blogger, I made it my personal aim to identify a fundamentally sound way for the average Singapore citizen to build wealth in a simple manner.

This is why I wrote the Infinity global stock index fund tear down and the POSB Investsaver one.

I think you should learn more about DFA funds. I think they are fundamentally sound enough.

This post is my tear down of what I know about their offering. And this post will show you how you can make use of DFA funds to build a rather passive wealth accumulation and de-accumulation machine for your financial Independence, or equivalent goals.

As this post is big, I will try to cut down on expansive description, and will try to keep it as short and sharp as possible.

I think if you are a general investor, or fund investor, parts of this article can be enlightening. If you want to, you can read the summary, then come back up and read through this.

This article will cover:

- The targeted market for a group of funds like this

- How do we build wealth, on a high level with DFA funds

- Introducing the Dimensional Funds

- Explaining Evidence Based Investing

- Examining DFA Results including rolling equity expected returns data

- Breaking down the Cost Stack and Comparisons

- Explaining the Adviser’s Alpha

- Breaking down Dividend Withholding Taxes and Death Taxes

- The Case to Invest in a Global Equity and Bond Portfolio

This is not a sponsored post. Unless you pay me $15,000, if not I will not exchange my free time to write a 10,000 word post. This post is for public education.

Executive Summary

- Building wealth is simple. You need capital from your work to build wealth. The more personal free cash flow you free up, the more capital you have. Learn to have a strategy to grow your wealth in a fundamentally sound manner

- You will encounter many strategies. They differ in the risk, volatility and return. They also have different levels of complexity. They also involve different level of upfront and recurring efforts. Investing in a portfolio of equity and bond funds such as Dimensional requires some upfront effort, but the recurring efforts are very low. It fits majority of wealth builders unless you like a second job

- Dimensional is not a new company. They been around for as long as I can remember. They are evidenced based in their investing approach. Many factors may work, but only those that show persistent and pervasiveness are implemented

- The historical results show the evidence of small caps over large, low price to book over high, high profitability over low. This is not just in USA but across other markets. However, the premium for the factors have noticeably narrowed over time. By implementing the factors in a cross sectional manner, it allows some factors to carry other factors when the factors do not do well, thus it smooths out the premium. The factors to me, have to be persistent enough. But you wonder if they just make up the company wrapper management fee that the companies charge. The out performance of the factors cover the management fees

- Cost matters. The DFA funds are low cost based on total expense ratio. To compare, we have to take a look at the cost stack. MoneyOwl and endowus’s offering is not the lowest. When stacked against unit trust they are low. When stacked against other robo platforms they are more or less similar. The lowest cost is DIY investing with a low cost broker like Interactive Broker. But in reality that is not for everyone

- There is an Adviser’s Alpha. Your mileage may vary. However, I believe that for most people, they need some form of hand-holding, behavioral coaching so that they can earn a decent return

- Where your fund is domiciled can have quite a high implication on the overall cost of investing. USA domiciled funds would have an additional 30% dividend withholding tax and if you do not structure well, a future 40% tax implication on your total wealth exposed. UCITS ETF and funds domiciled in Ireland are more optimized

- If you invest in a global portfolio, you mitigate the home country bias, or the home country risk or that, if a single country under-performs over your wealth accumulation period, it hinders your wealth building. You would also reduce your single sector, single asset class risks

- What you are paying for:

- The evidence investing approach giving the factor premium

- The tax advantages of the Irish domiciled UCITS funds

- The Adviser’s Alpha

- The ease of investing on a recurring basis

- The access to funds that are low cost, fundamental funds locally

This Way of Investing is Suitable for

I think most of my readers will have a lot of good takeaway from this post.

Specifically, those who are looking to augment their current way of building wealth, or shift their way of building wealth would get a lot of value from this post.

This post while its on DFA funds, is suitable for a lot of folks:

- Who wish to build wealth passively. That means they do not want a second job

- Who tried investing themselves, and gotten mixed results and would like to delegate much of these work

- Have great human capital (their potential for building wealth lies very much in their lucrative career) and would make more sense devoting their time to this rather than take on a second active investing job

- Who wishes for a fundamentally sound quantitative fund

- Who wishes for a solution that they can cash flow their wealth in financial independence or retirement, yet remains diversified

- Who both have large capital and low capital as a start

- Who have proved that they had been good at investing themselves, fell out of love with it, or believe that their future life lies more with family, career or other endeavor, but wishes to still invest by sticking to investing philosophies that are aligned to what they believe in

The Way Your Wealth will be Built

If we are going to talk about why we invest in a fund, then we are absolutely going to talk about the goal and purpose in the first place.

We invest in a fund because we want to build wealth. Why do we want to build wealth?

Because we have some financial goals.

Most notable what is on a lot of our minds are some longer-term goals:

- We want to build wealth for our retirement? (my retirement planning section)

- We want to not wait until 65 years old but retire earlier?

- We don’t need so much now, so we want to build up something, in case we need it (this is called financial security, which is explained here)

- We just want to build up money so that we can, maybe work on a childhood dream

Whichever goal you have, I think they require you to accumulate some money.

The next question to ask is how much money.

For a few of the goals highlighted above, they require your wealth to provide an annual recurring cash flow. The amount of the cash flow will depend on your needs.

Suppose you need $2,000/mth today in 10 to 15 years time. By then, due to inflation you would need $2,700/mth to $3,110/mth.

How much wealth do you need to cash flow this amount?

We can use the 4% withdrawal rate, which is a prevalent rule of thumb to determine how much you can safely spend down your wealth, so that your wealth can last for 30 years.

So if its $3,110/mth, you will need to accumulate ($3110 x 12)/0.04 = $933,000.

If you are more risk-seeking, you can aim for a less conservative withdrawal rate of 4.5%, you will need ($3110 x 12)/0.045 = $829,000.

If you are more risk-averse, you can aim for a more conservative withdrawal rate of 3%, you will need ($3110 x 12)/0.03 = $1,244,000.

Instead of telling yourself you are risk-seeking or risk-averse, build a wealth accumulation ladder of milestones so that you can see progress:

- 5 years of $3,110/mth: $186,600

- 10 years of $3,110/mth: $373,200

- Half of $3,110/mth at a 4% withdrawal rate: $466,500

- Half of $3,110/mth at a conservative 3% withdrawal rate: $622,000

- $3,110/mth at a flexible 5% withdrawal rate: $746,400

- $3,110/mth at a 4.5% withdrawal rate: $829,000

- $3,110/mth at a 4% withdrawal rate: $933,000

- $3,110/mth at a 3.5% withdrawal rate: $1,066,000

- $3,110/mth at a 3% withdrawal rate: $1,244,000

The higher you go, the more conservative your plan becomes. Every milestone translates to a financial utility that can impact your life.

In order to build wealth, you need to put in your own capital and grow it at an average rate of return.

If you do not have capital, it is very, very, very, very tough for the money to grow so fast.

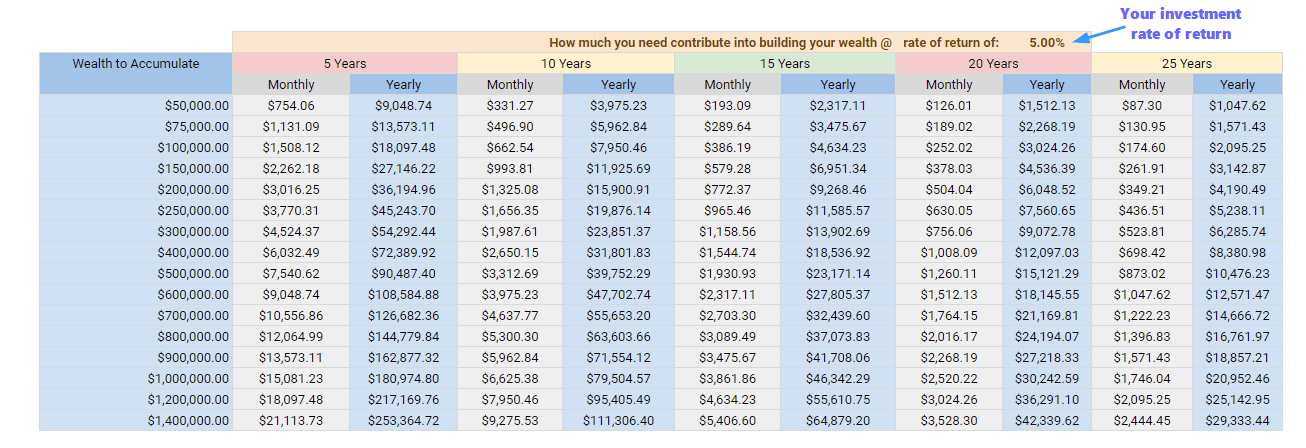

This is an easy look up table to show you that if you need to accumulate $X, if your time horizon is Y years, you need this recurring amount of funding monthly or annually.

For example, if you wish to have half of $3,110/mth at a conservative 3% withdrawal rate or $622,000 in 15 years, you will need to put away about $2,317/mth from your disposable income now.

If you do not need the money, by putting away $2,317/mth for 20 years, from this table you will see it grow to $900,000. This will imply you can build up a cash flow of $3,110/mth at a 4% withdrawal rate. If you still do not need it after 25 years, you will probably build up to $1.3 mil. This will give you a cash flow of $3,110/mth at a 3% withdrawal rate.

How do you get your capital? By doing this:

- Try to earn more

- Optimize your expenses well

- #1 and #2 will increase your personal free cash flow

- Put your personal free cash flow to building wealth

This is a well known formula. Different Gurus will tell it in a different way. But usually it boils down to this. If you would like to know more about these 4 points, I encourage you to read my post on my Wealthy Formula)

You will notice, that on the top right, one of the assumption is for an investment rate of return of 5%. The 5% used is an assumption.

You will need a rate of return that is respectable, yet consistent over time, so that as you add more capital, you can build wealth up.

How could we go about achieving a rate of return close to that, if not more?

And this is why we want to know whether Dimensional Fund Advisors funds can help us achieve that investment rate of return, to fulfill our wealth goals.

How you could build wealth with MoneyOwl

You could start building wealth even in your National Service, or when you graduate from university. That is when your pay is low.

Through MoneyOwl’s platform, you would be able to get started investing with just a lump sum of $100.

You can also regularly contribute on a monthly basis with $50 per month.

To move up the wealth milestone ladder, when your earning is less, contribute 25% of your personal free cash flow or $3600/yr.

As you move up:

- Control your expenses. Try to live as much as close to a student’s budget. This would allow you to put 50% of your disposable income of $3000/mth into MoneyOwl. You start by contributing $1500/mth. As you get raises, increase your contribution by 20%.

- Alternatively, you could spend 90% of your disposable income. As you get more raises, put 100% or 90% of your raises into a platform like MoneyOwl. This strategy is called saving for tomorrow. Then keep your spending as close to that first year 90% as possible. For example your disposable income is $3000/mth. Spend $2700/mth, which is quite comfortable for you. You start by putting $300/mth to MoneyOwl. Next year, your increment is $300/mth more. Put that entire $300/mth into MoneyOwl. Next year, your increment is $100/mth. Put entire $100/mth into MoneyOwl. So in 3 years you save $700/mth

- Read up on books, articles pertaining to portfolio investing, low cost evidence based investing, behavioral sciene

- Concentrate on your job, your family

Move from $700/mth to $1500/mth to $2000/mth.

From the table you can see that

- If you put away $700 per month at 5% rate of return for 5 years, you will build up $50,000

- As you increase to $1500 per month at 5% rate of return for 5 years, you will up it to $100,000

- If you are able to increase to $2000/mth as your savings rate is 50%, in 10 years you will build up $300,000

- If you keep to this for 15 years, it becomes $500,000

- When you get married and as a couple you can up it to $4000/mth, in 10 years that is $600,000

Visualize this: If you can on the initial year, withdraw 3% of $500,000, you get a cash flow of $15,000/yr or $1250/mth. For subsequent years, this $15,000/yr will be adjusted for inflation. This inflation adjusted cash flow can last for 25 to 30 years, if not more, and can cover your basic essential expenses to provide financial security. How appealing is that?

The Dimensional Fund Advisors Funds Available to Singaporeans

As a start these are the DFA funds that are available to Singaporeans, to be purchased through the various Singapore platforms.

From endowus:

- Dimensional World Equity Fund

- Inception in 2018 Mar

- Currency: SGD

- Benchmark: MSCI All Country World Index (net div., SGD)

- Total Assets: $2.4 bil pounds

- ISIN: IE00BF20L762

- Dividends: Accumulating

- Expense Ratio: 0.43%

- 10630 Global Stocks

This fund is newly created. It is available to retail investors and denominated in SGD. There is a GBP version which is started in 2011. So you can check out its history.

If you invest with endowus, you can have a lazy, passive portfolio made up of bonds and stocks, with a combination of Dimensional World Equity Fund and a Pimco bond fund.

From Providend and MoneyOwl:

- Dimensional Global Core Equity Fund

- Inception in 2017 Jul

- Currency: SGD

- Benchmark: MSCI World Index (net Div, SGD)

- Total Assets: S$4.5 bil

- ISIN: IE00BF20L879

- Dividends: Accumulating

- Expense Ratio: 0.35%

- 7776 Global Stocks

- Dimensional Emerging Markets Large Cap Core Equity Fund

- Inception in 2017 Jul

- Currency: SGD

- Benchmark: MSCI Emerging Markets Index (net div., SGD)

- Total Assets: S$706 mil

- ISIN: IE00BF20LB02

- Dividends: Accumulating

- Expense Ratio: 0.50%

- 922 Emerging Market Stocks

- Dimensional Global Short Fixed Income Fund

- Inception in 2017 Jul

- Currency: SGD

- Benchmark: FTSE World Government Bond Index 1-5 Years (hedged to SGD)

- Total Assets: S$4 bil

- ISIN: IE00BF20L549

- Dividends: Accumulating

- Expense Ratio: 0.29%

- 181 High Quality Bonds

- Yield to Maturity: 2.18%

- Average years to maturity: 3.67 years

DFA Global Core Equity Fund and World Equity Fund, is a basket of 7776 and 10630 global stocks. They are very well diversified and suitable for long term investing. The top 10 stocks makes up 8% and 5% of the fund respectively. This means that should one company or a segment of company collapse to zero, the majority of your capital is intact.

With these funds, you are able to dollar cost average, or lump sum invest into them over the duration of your wealth accumulation stage.

MoneyOwl and Providend’s offering is a little different from endowus. Instead of using a Pimco bond fund, they provide for their clients a full DFA solution with a bond fund that should be very safe.

Depending on your risk appetite, how far you are from your wealth building goal, you can set up different allocation with these 3 available funds for a lazy, passive portfolio.

At this time of writing, you should be able to purchase them through MoneyOwl, Providend, endowus and any DFA certified advisers like Wilfred.

DFA Funds are Low Cost Versus the Conventional Unit Trusts

One thing you would notice is that whether it is endowus’s offering, or Providend & MoneyOwl’s offering, the expense ratio for these funds are low.

This is in contrast to the typical unit trusts provided by Fundsupermart, Dollardex, Poems, the banks which are typically 1% to 3% per year.

If you look at the top funds, in terms of 10 year performance mentioned in my Infinity Global article, there are the corresponding expense ratio for these global equity unit trusts:

- Nikko AM Shenton Glb Opportunities: 1.57%

- AB SICAV I Sustainable Global Thematic A SGD: 2.00%

- Stewart Investors Worldwide Leaders Sustainability A Acc SGD: 1.93%

- HGIF-Economic Scale Global Equity AD SGD: 0.95%

- United International Growth Fund: 1.26%

- DWS Global Themes Equity A SGD: 1.71%

- Nikko AM Global Dividend Equity Acc SGD-H: 1.72%

- FTIF- Templeton Global A Acc SGD: 1.84%

- AB FCP I Global Equity Blend A SGD: 1.60%

- Schroder ISF Global Dividend Maximiser A Acc SGD: 1.88%

The expense ratio for these funds are higher because, there is an active fund manager and his team behind it.

Most of all, these expenses encapsulates trailer fees.

These trailer fee are paid from the fund manager to the distributor like Dollardex, Poems and FSM. So they have zero platform fees but you are indirectly paying for the fees through the high cost fund you are buying.

The Lazy Strategy to Build Wealth with 1 to 3 Diversified Funds

So after you have identified some reasons why you want to set aside your money to build wealth, how do you get started scaling this wealth ladder?

In a lot of investing strategies you come across, they would usually tell you about risk and returns. To have more returns, you need to take on more risk. You take on more risk, with the hope that due to market beta, higher volatility, you are rewarded with higher return. This is true for most financial assets. If you purchase a property, there are higher risks because you took on leverage which is a credit risk event to you, there is uncertainty over future property prices, future rental growth rates, future supply and demand. As there are more risks, you hope by investing this way, you earn a higher return. This relationship is always there.

What is less talked about is effort.

Different wealth building strategies have different volatility, returns but also entails different effort.

I do active stock investing, and some of you do too. And touch your heart, tell me that to do it well, it is not a second job.

It is a second job. There is a lot of effort that goes into having our attention spent monitoring, paying attention to news, prospecting new stocks, thinking about whether to buy, hold and sell.

Those are effort.

The Simple Lazy Portfolio is a concept that got popularize when low cost index funds/ETFs got popular. You are able to build wealth by just putting money into 1 to 3 funds, which are diversified and then rebalance annually.

For most part, you get on with your life!

As it is simple and not overly complex, people tend to stick with it easier.

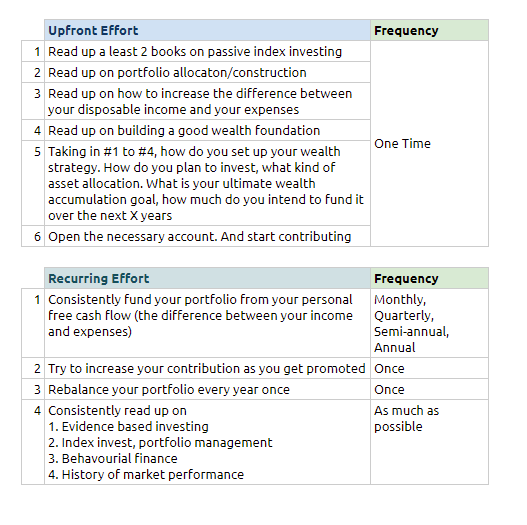

The effort you need can be broken down to 2 categories: Upfront and Recurring:

Before you get started investing, you have to build up sophistication and competency. Why?

You are going to sink like at least $500,000 of your future hard earned dollars into it!

The most you could do is to ensure that:

- the strategy and financial instrument you choose to build wealth is fundamentally sound

- you know the benefits of the strategies and financial instrument

- you know the weaknesses

- you know the effort it requires

- you are aware of the nuances of the strategy and financial instrument

So a large part of the upfront effort is on education. And I believe for most they can get more sophisticated, provided they put in some effort.

Part of the upfront effort is to open the account. And I believe the local robo platforms and the companies that I mentioned such as MoneyOwl and endowus make this part much simpler compare to some of the lowest cost DIY method.

The recurring effort will take place periodically. This is where most of the efforts take place for other strategies.

You will be:

- Screening for things to buy

- Monitoring your existing holdings and the news & information surrounding them to ensure that if there is potential negative events you need to pull out, or if positive add on more

- Do deeper work on potential things to buy (because that is the fundamentally sound thing to do)

- Get more educated by reading. A lot. Warren Buffett and great investors like himself spend a large part of their time reading so as to build up their mental models. Also, because you need to be real sophisticated so that you can do well in the long term, and you are not there yet, you need to read more

Contrast this to the Lazy Portfolio Strategy:

- Consistently do well at work, increase your personal free cash flow

- Consistently fund your portfolio. Try to increase your funding if possible

- Rebalance probably once a year

- Read more on the subject, and those 4 subjects highlighted above. The more you read, the more you know what you are doing, the greater likelihood you will stick to it. It builds conviction. It also tunes out the noise. (Also, this article is nearly 10,000 words. While the actions are simple and short, to make this strategy work and for people to stick to it, they might need to get to where I am, to be able to write something like this, so they have greater conviction in the way they build wealth this way)

For most people, they might not need that second job. Even if you have that second job in active investing, you might not do better than the lazy portfolio strategy as well.

The Origins of Dimensional Fund Advisors

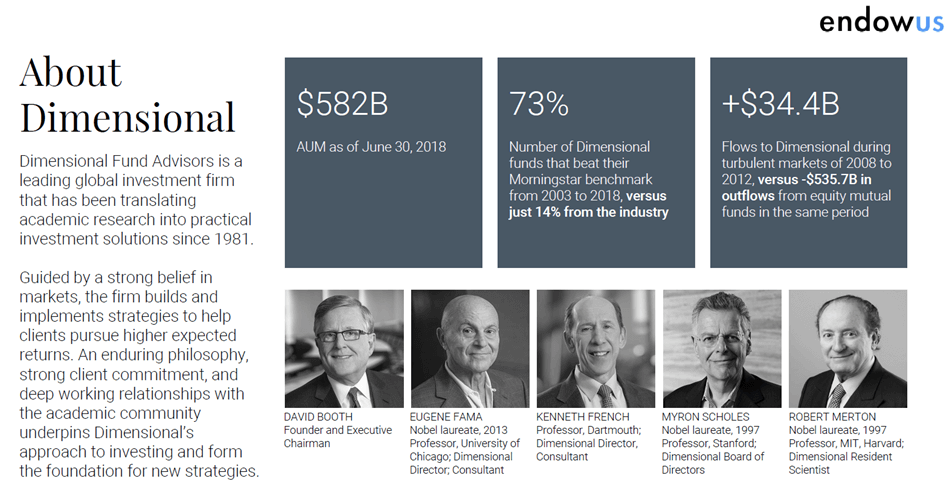

DFA was founded in 1981 by David Booth and Rex Sinquefield. Both Rex and David was graduates of University of Chicago’s School of Business, which is now renamed as Booth School of Business, after David Booth.

When they started the firm in 1981, they decided that their philosophy towards portfolio strategy, and structure should be based on evidence research. Back then in 1981, it was based on the single factor, which is that small cap out performed large cap issues.

Then in 1992, Eugene Fama and Kenneth French published the research on what is now known as the Fama-French Three Factor Model, DFA launched funds based on this framework.

Since then DFA have continued to based their investment philosophy on research, and evidence based investing.

They brought on both Eugene Fama and Kenneth French as directors, but also Nobel Laureate Myron Scholes and Robert Merton (who became famous for their Black Scholes options pricing model and as part of the founders of the infamous Long Term Capital Management), Yale professor Roger Ibbotson.

DFA is owned by their employees, board members and outside investors.

Currently, DFA manages nearly $580 billion in assets.

You can only buy DFA funds from their trained advisers. They have trained thousands of advisory firms. To be approved by DFA, the adviser must attend a conference that reviews the DFA philosophy and academic research in support. If the adviser is still interested, a regional DFA director will then discuss the investment philosophy with the adviser. There is then a lengthy approval process and once accepted, the adviser can purchase DFA funds for their clients.

What this means is that if MoneyOwl, Providend, Wilfred Ling and endowus can distribute DFA funds, they went through the same rigorous process.

DFA funds are used by many financial advisory firms who are certified to recommend DFA funds, amongst the many other funds that they can recommend.

There are some firms that are pretty famous that have put out research on DFA funds.

The biggest names in this space have been Larry Swedroe from Buckingham Strategic Wealth and Rick Ferri of Ferri Investment Solutions (formerly of Portfolio Solutions).

Both have written a lot over the years on evidence based investing, index investing, and implementing DFA funds as part of their solutions to clients. Due to how long they been around, it is not difficult to find out more about Dimensional.

A simple way could be Googling “Larry Swedroe and DFA funds” and you would have a lot of recent and past research on it.

The Case for Evidence Based Investing

The way I looked at DFA funds is that you take a strategic, systematic, quantitative, low cost approach to fund management.

- Strategic: They research on the ideal structure, based upon factors to set up their equity or bond portfolio, and stick to it, rather than make tactical shifts

- Systematic & Quantitative: As an individual “portfolio manager”, we often look through our watch list based on certain factors we think makes certain companies outperform other companies. Then we do our qualitative prospecting and analysis, discard or select a subset of the prospects. When we say DFA are systematic, they take what we do in stock selection, systematize which stocks/bonds meet the factors that over time provides alpha to the portfolio performance, and select them without as much human biases

- Low Cost: It is good to have a winning edge in #1 and #2, but if you are not able to keep the fund expense low, your performance is likely to suffer as well

For the past 38 years, DFA have based their portfolio construction and selection on evidence backed research.

We can look at them as looking through the research out there, back test which factors work, and incorporate them into their funds. Some critics will call this flipping and being reactionary, but we can also say that when you invest with DFA funds, you are also buying into their process of improving/correcting the performance for you on a proactive basis.

What Active Stock Investors will Appreciate about Funds like DFA

The biggest contrast between the prevalent passive index funds or ETF is that passive index funds track index benchmarks created and license by certain companies.

They are mainly capitalization weighted. This means that it is the survival of the fittest. Tencent grow from a very small company, to become a main component of the index. So did Apple and Microsoft in the past. Companies who got into trouble such as General Electric will shrink accordingly. In a capitalization weighted index, the majority of the fund is dominated by the largest capitalization companies.

When we purchase in, it is like voting that while the basket of companies are not cheap, but I will still buy into them. (It is also true that if the basket of companies are cheap, I will still buy into them).

I am not sure if you agree with buying companies that are not cheap.

Which is why there are some of us who have our own investing philosophy and decide to pick stocks ourselves. We believe that we can do better.

We have our own factors that outperform the index.

This can be:

- Value stocks based on price earnings

- Value stocks based on consistent or growing free cash flows

- Value stocks based on low debt, high dividend yields (the 80th percentile instead of the highest)

We run through our own screens. Then from the screens, we select the companies that looked better to do further research. We do both qualitative and quantitative research. Then we decide to buy or not buy. When selling, we have our own methodology. It may be gut feel, it may be markets sentiments, it may be quantitative measures.

The very best outperform the index over time, the mediocre ones keep pace with the index.

If you understand what you do, then you would appreciate factor funds such as the DFA funds.

They have done the research on which factors works, and incorporate in their funds. Overtime, they also build up a systematic way of rebalancing the stocks/bonds based on factors.

- Some of you, enjoy this stock investing process.

- Some of you, enjoyed the process in the past. However, life has become tougher and you cannot spend as much effort on active investing. However, you still believe some of these philosophies.

- Some of you do not like these active prospecting process!

Factor based funds such as DFA is a way for you to

- Resolve and keep close to your investing philosophy

- Drastically eliminate a large part of this “second job” of active stock investing

- Instead of slogging and getting mediocre results, have someone implement it in a broad diversified way

- You pay a certain percentage fee to get the value of #1 to #3

Only Persistent and Pervasive Factors which are Cost Effective to Capture will be Selected

Currently, DFA Equity funds are built upon 4 factors/dimensions (hence their name Dimensional Fund Advisors):

- Overall Market (Beta)

- Company Size (Small Cap over Large Cap)

- Relative Price (Low price to book over High price to book)

- Direct Profitability ( High profitability over low profitability)

For DFA Bond funds, they are build upon the following factors:

- Term (Maturity)

- Credit Spread (Quality)

There are many factors out there. In one article, Larry Swedroe said that there could be as much as 600 factors!

DFA’s methodology is to be stringent in what is considered a dimension.

To them the they only consider it a dimension if:

- Persistent: The factor have worked over time, and not just a selected period

- Pervasive: The factor worked not just in one market but various markets

- Cost effective to capture

- Consistent with an equilibrium view of investing

The following shows how DFA have evolved, due to their work on evidenced based investing:

- They started in 1981. They discovered the “Size effect”. Small cap stocks had higher average returns that can be explained by a single factor model. So they launch a small cap fund because the result was persistent and pervasive

- The did not have an explanation for higher returns but their deduction is that smaller firm have higher costs of capital. The return to an investor is the company’s cost of capital

- Don Kelm discovered “the January effect”. They see no sensible equilibrium explanation for this effect so they did not use it. They also discover that when they increase the data set they tested upon, this factor disappeared

- In 1991, after Fama and French presented the 3 Factor Model. People were concerned about data mining so Fama and French did 2 out of sample tests. they analyze the data from 1926 to 1962 and developed & emerging markets around the world. They found the return patterns consistent with what they observed in the US returns from 1963 to 1990. So they are confident to base upon them

- Then there were more research put out on profitability which met their criteria. The metric that was used is gross operating margin. DFA was able to replicate the findings

- Some were concerned that with higher expected returns, means higher risks. This might not be the case. Higher expected returns is equal to either Higher Expected Cash Flows or Lower Prices. In this area the two factors, profitability is tied to expected cash flows, and relative price is tied to prices. The intersection of these 2 factors can improve the portfolio structure

- Momentum have been a very popular factor recently. DFA finds that momentum does not meet their criteria as a dimension but it impacts portfolio returns. Stocks that have underperformed in a past period are more likely to underperform in the next period; stocks that have outperformed have a tendency to continue to outperform. If the momentum effect were large enough to trade on profitably, then it would be evidence of market mispricing. DFA finds that momentum is too small and sporadic to actively induce trading. Momentum is stronger in small cap stocks than in large cap stocks. Momentum also fails the test of all time periods

Low Cost, Passive but Not Indexed Portfolio

Based on what I explained till now, the best way to describe DFA funds is that of low cost, passive but perhaps quantitative.

If you look at their returns, and if you do not know them, you would think of them as index funds.

That would not be the right term to describe them because they are not.

If you do not understand them, then you will be alarmed:

- when in some time frame they underperform the benchmark they are measured against

- their returns veered far from the benchmarks

#2 happens if you think their objective is to track the index like a passive index fund / ETF.

Examining the DFA Results

There is some difficulty in examining the results because almost all the retail funds are newly created in 2017 or 2018.

It should be noted that past performance does not equal to future returns.

We could, however, evaluate the performance of some similar DFA funds, and project that these new funds under endowus, MoneyOwl would perform as well.

Since Dimensional wants to be evidenced-based, I will let the evidence tell the story

The Rolling Returns of Dimensional Funds If You Invest for the Long Term

We do not have a lot of actual fund returns because the funds that were available to Singaporeans was incepted recently.

However, the selection of these funds are based on systematic rules based on a few financial dimensions, investors can take a look at the results from an index created using the same methodology to see how are the returns like.

Rolling returns is a good way to give you an idea of the range of long term returns a fund or a Dimensional-based portfolio can get you.

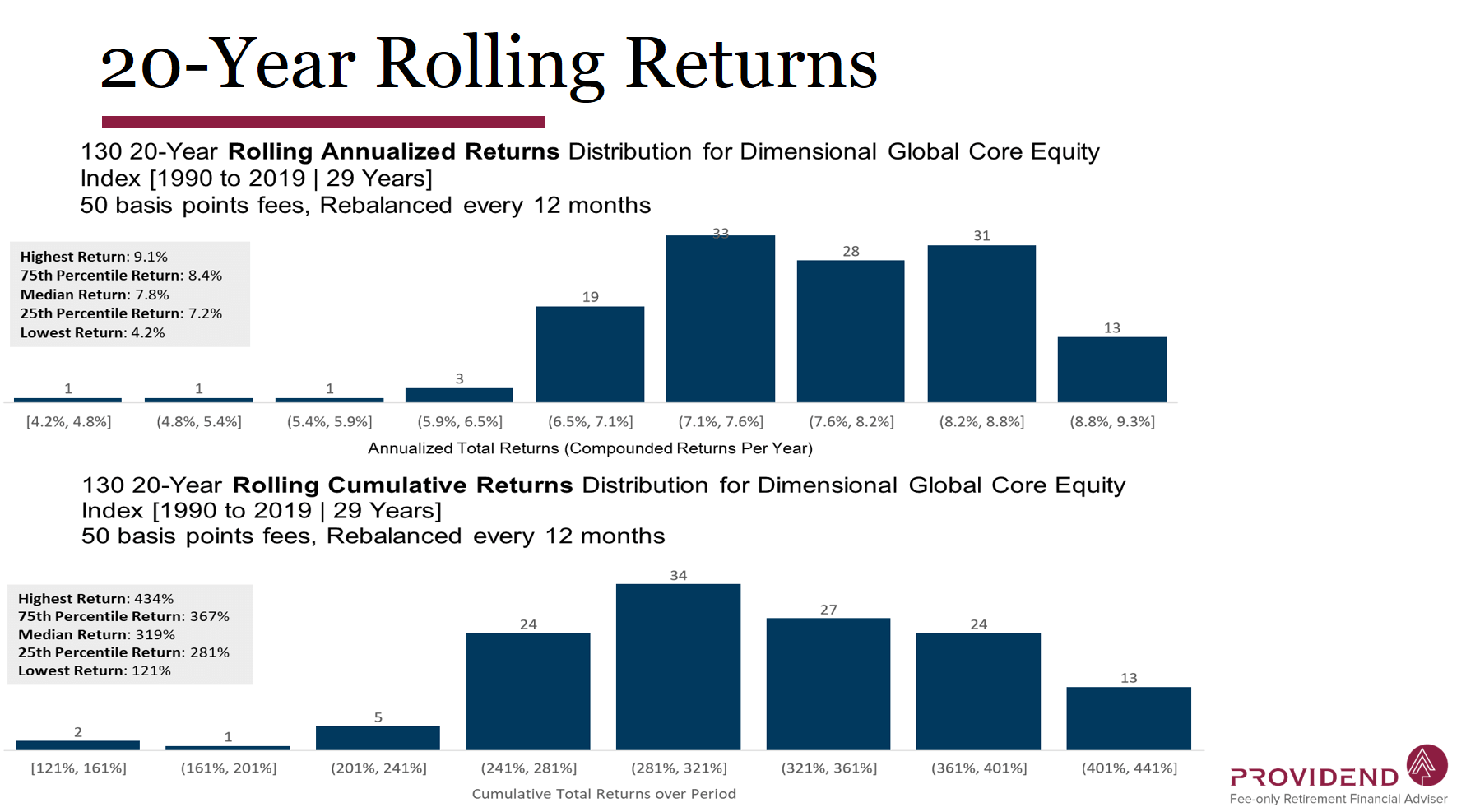

For example, the following histogram shows all the 20-year returns an investor can get if she invest in a Dimensional Global Core Equity Index at various points from 1990 to 2019:

The top histogram shows the annualized compounded returns while the bottom shows the cumulative returns. Each count indicates a 20-year period in history.

It lets you visualize what if you invest $100,000 in a particular month and held it for 20 years. We observe that all the 130 20-year periods were positive. The lowest 20-year return was 123% or 4.2% a year.

In some years, your money gain 200%, 300% or 400%.

This is the effect of sticking with a fundamentally sound investing methodology and fund for the long run.

You can review this Providend article which will show the 1-year, 5-year, 10-year, 15-year, 20-year rolling returns of the Dimensional Global Core Equity Index more here: Rolling Returns of Dimensional Global Core Equity Index >>

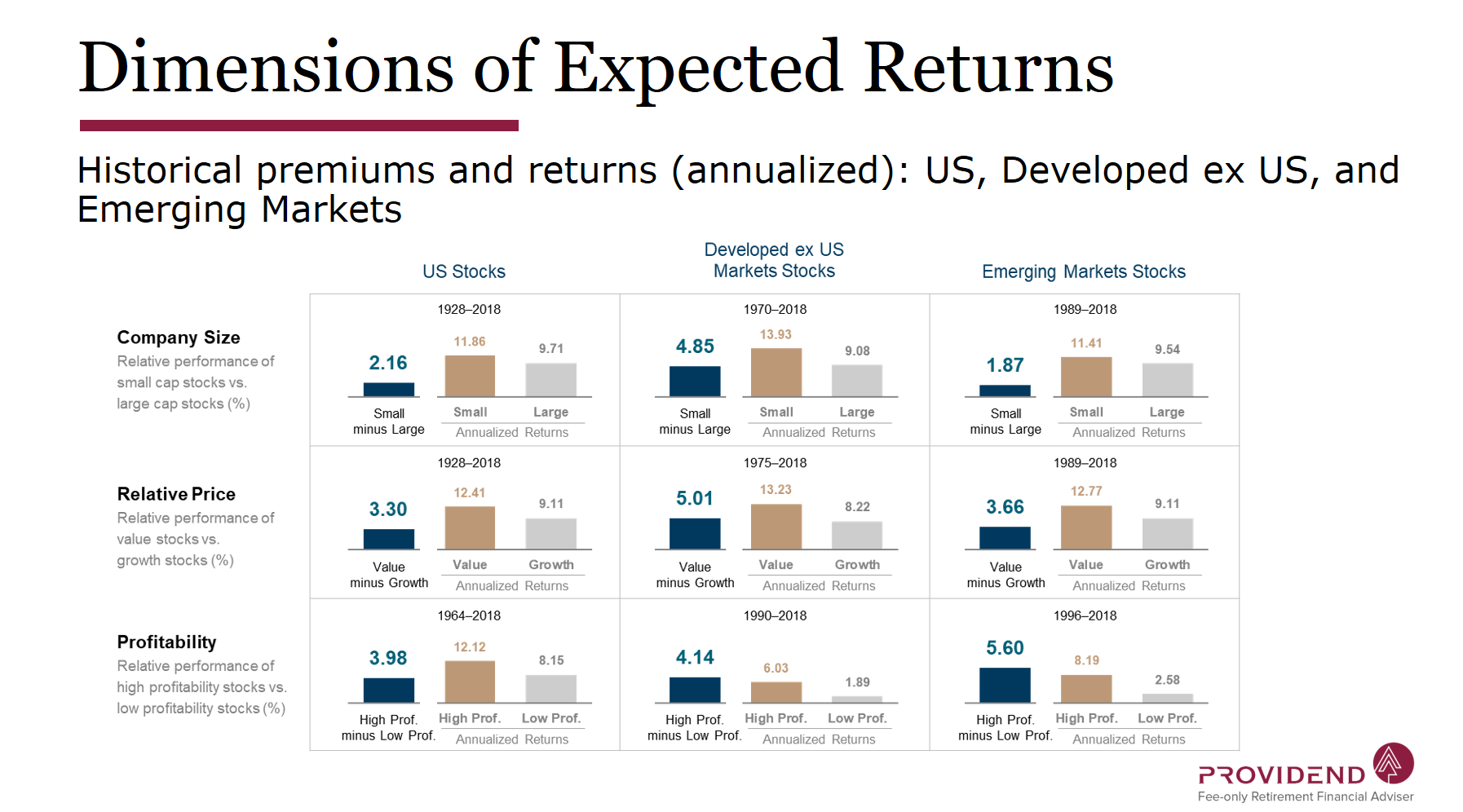

The Persistence and Pervasiveness of Small Cap, Value and Profitability

If DFA says that these factors should be present across different markets, and over different periods then it should be shown in the evidence.

In the illustration above, they break down whether there is outperformance by factors and by 3 different geographical regions. We have 47 years of Developed Markets EX US, 28 years of Emerging Markets data.

If we look at the size in the first row, it compares the Dimensional US , International, and Emerging Markets Small Cap Index against S&P500, MSCI World ex USA, and MSCI Emerging Markets.

Do note that these indices are for research purposes (those Dimensional Indices, Fama/French Indices) and not available for direct investments.

Across all three markets, there is at least around 1.8% in difference in having small caps.

In the second row, we see the Fama/French Value Index against the Growth Index in different countries. This is to contrast value versus growth.

There is like at least 3.3% difference for all three geographical regions between value and growth.

Finally, in the last row, we contrast high profitability against low profitability.

There is nearly a 4% difference between high profitability and low profitability.

This does seem very compelling.

However, my gripe with this is that this shows the result across the whole period.

As investors, we do not live the whole period, but perhaps 10, 20, 30, 40 years of our lives. It is also difficult to trust the fund to stick with it for so long.

So as much as I hate to say it, investors need to see the results.

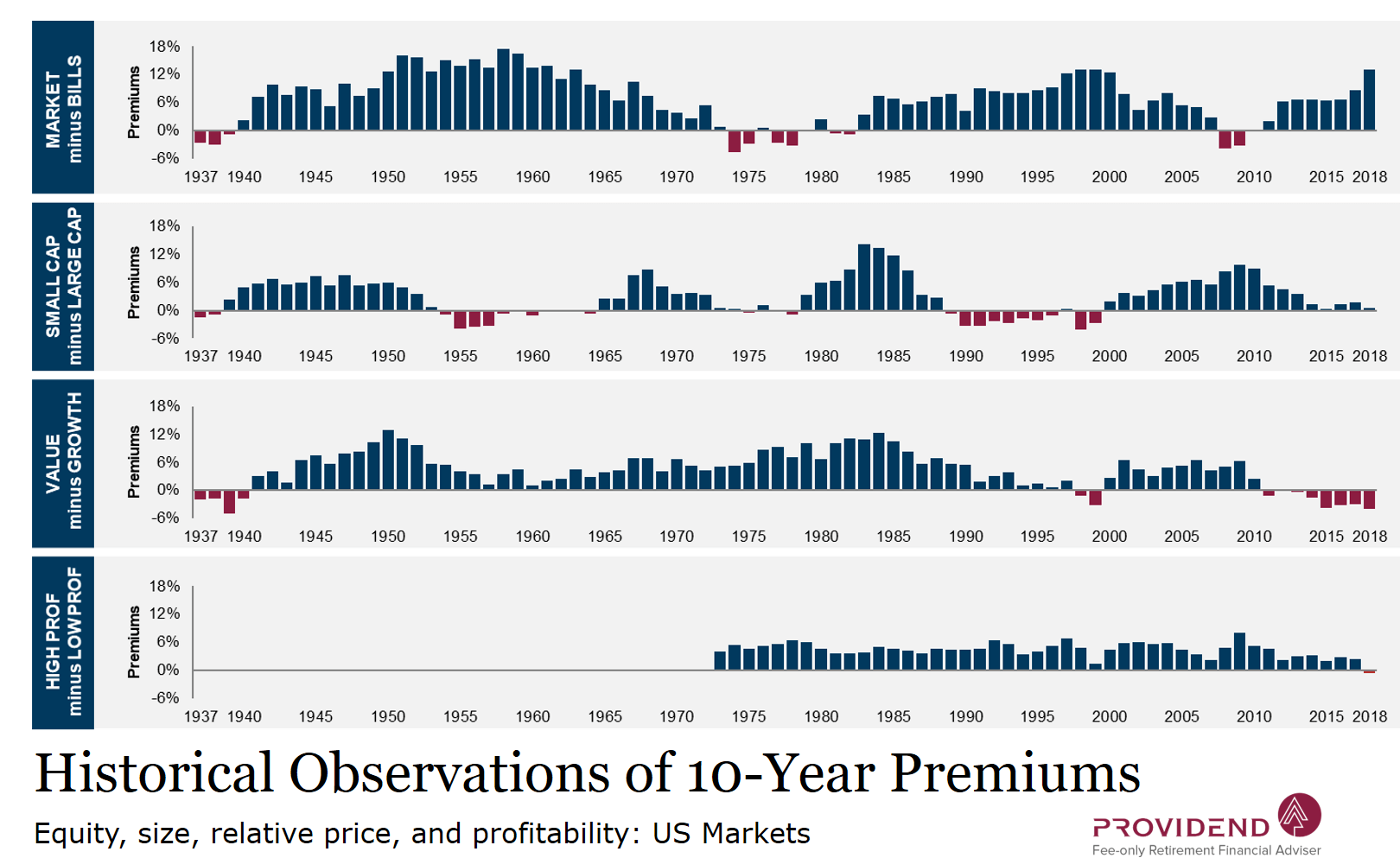

The Persistence and Pervasiveness of Small Cap, Value and Profitability over Rolling Periods

If we can analyze how these factors performed over rolling periods, then we might be able to answer the question of whether we are able to see results over a shorter duration.

While investing in the short term can contain much noise, or widely high/low results, with some data, perhaps we can have a better idea what we should be expecting when investing in quantitative funds such as DFA

The chart above shows the performance of the 4 premiums over time. Each bar on each chart is a 10-yr period.

If the bar is blue, it shows that equity outperform bonds, small outperform large, value outperforms growth, high profitability outperform low profitability.

You realized for all 4 there are more blue bars than red bars.

This indicates over rolling 10-yr periods, the dimensions showed up more often than not. If you have invested in DFA funds, you would benefit from them.

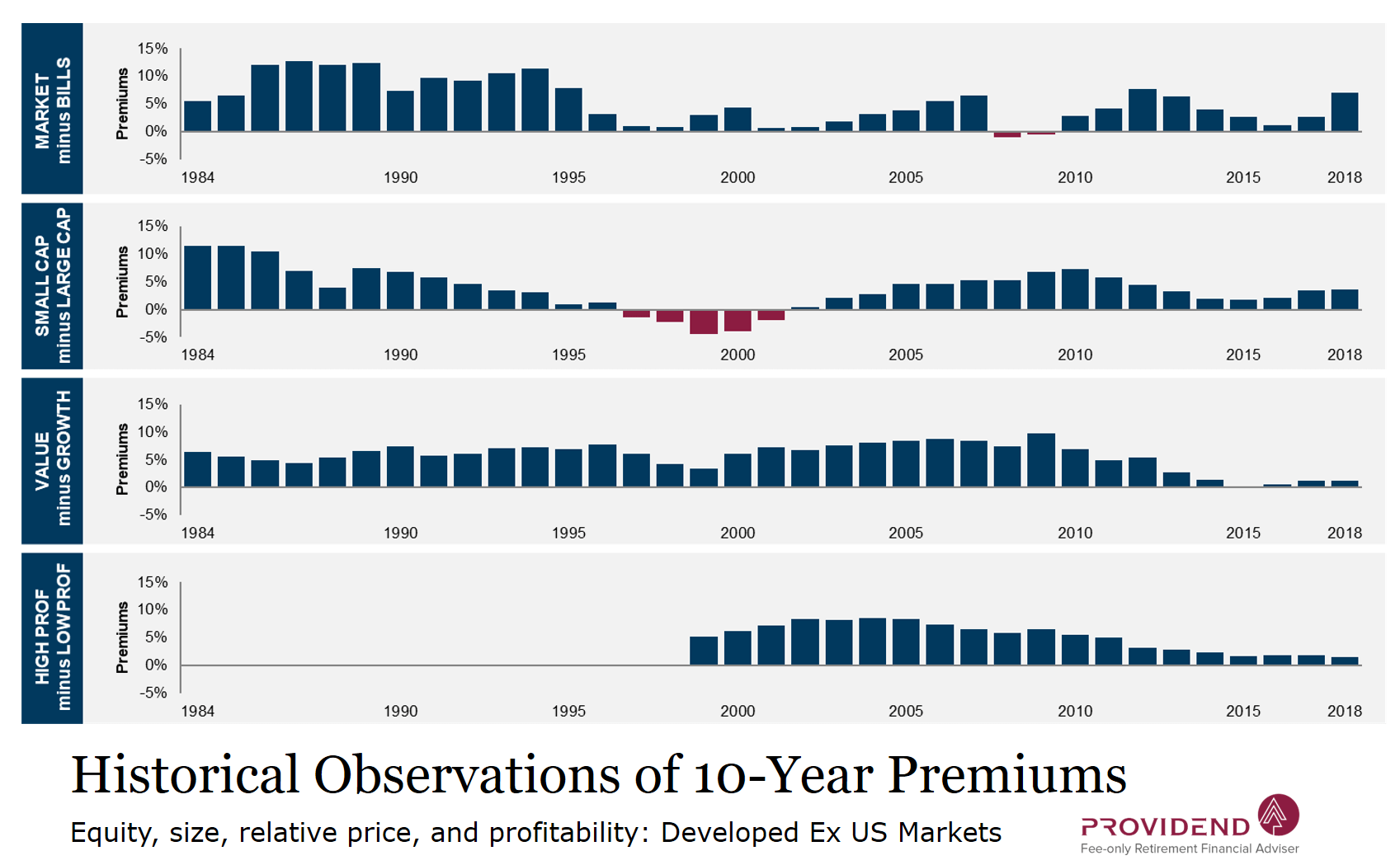

In contrast over a rolling 10-year period for developed markets ex-US, we see higher historical evidence that the factors are persistent.

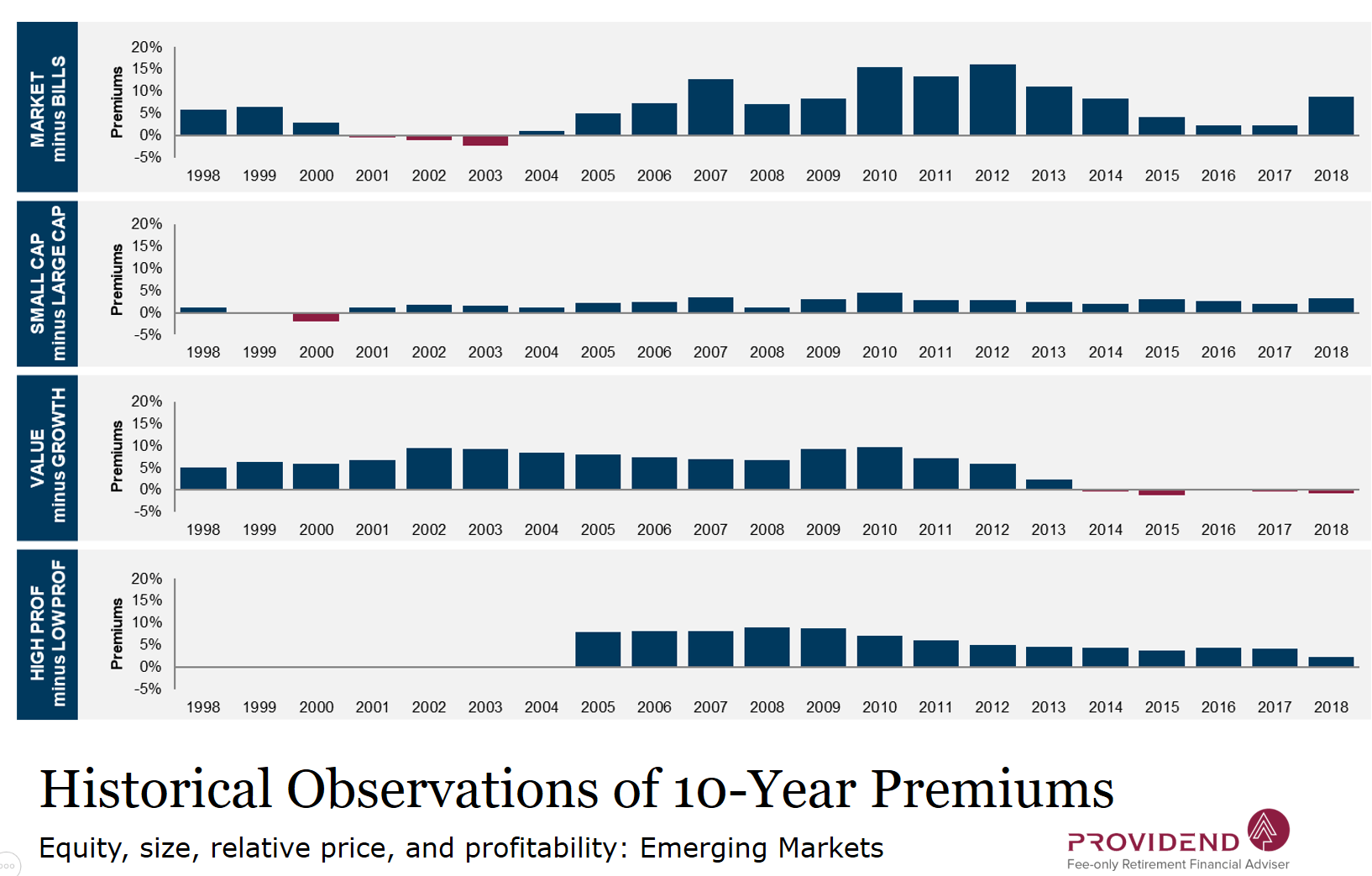

The result looks consistent with the emerging markets. However, we do observe in recent years, the underperformance of value over growth for the emerging markets.

And these are 10-year rolling periods.

10-year rolling periods is damn powerful.

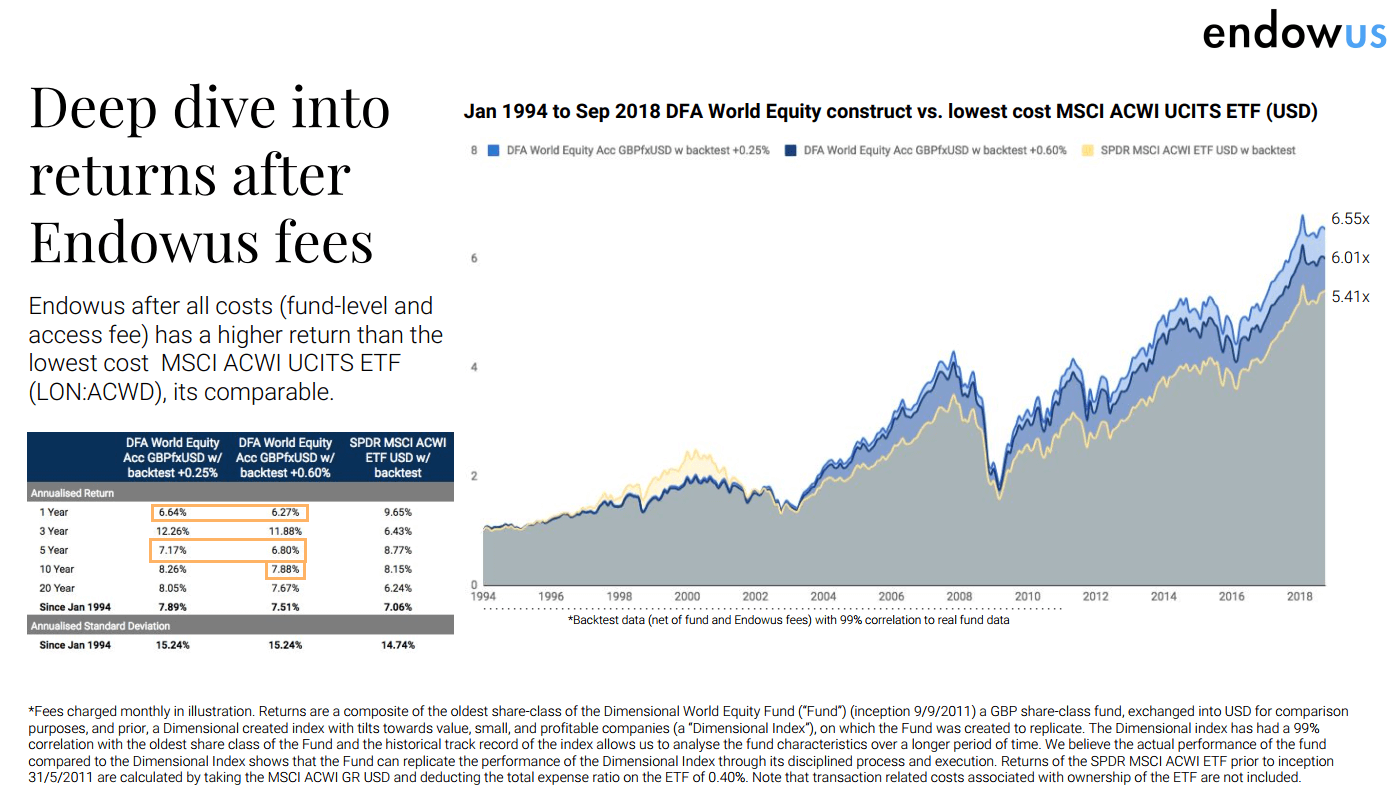

The Simulated Back Test Returns of the DFA World Equity Fund

As I have said, the fund that you will be investing in, is started in 2018. So there is not a lot of data to say.

However, in order for DFA to put out such a fund, they would have to have backtested results. Basically, they can reconstruct with high correlation, the returns of the fund, if it was started some years ago.

So they can give you the returns of a combination of a factor tilted index from 1994 to 2011, and the DFA World Equity fund in GBP, which started in 2011, from 2011 to 2018.

This is compared against SPDR MSCI ACWI ETF, which has an expense ratio of 0.40%.

Now you may notice they backtest with a 0.25% and 0.60%.

What are those?

endowus want to see the returns that the fund gets, including the endowus company wrapper fee that they charge to the highest and lowest tier of customers. This is so that they can be rather transparent about it. Which is great.

Overall the 2 DFA fund, with different costs, outperformed the MSCI ETF. However, you can also make a case that you could just invest in the MSCI ETF.

There are periods such as 1-year and 5-year, where the DFA funds underperform the index.

And you could draw the conclusion that investing in DFA is not worth the effort.

My job here is to present you with the data. You may conclude that way, and then for the next 3 year, 5 years, or 7 years see the factors working out and deliver the outperformance.

The reality is that you really need to know:

- What you are buying

- How it works in your favor

- When you observed the fund, what is considered normal and what its not

Sometimes I get people telling me that Stashaway or Smartly’s portfolio did this % and an index did that % over 1 year. And I wonder if that is really the right way to look at things.

There is no magic pill to the DFA funds. They are not supposed to be the god level fund that won’t give you negative returns.

We have shown here that the factors go through periods of underperformance but if your time horizon is long enough, the combination of the factors should result in outperformance.

Unfortunately, you need some time in order to conclude that.

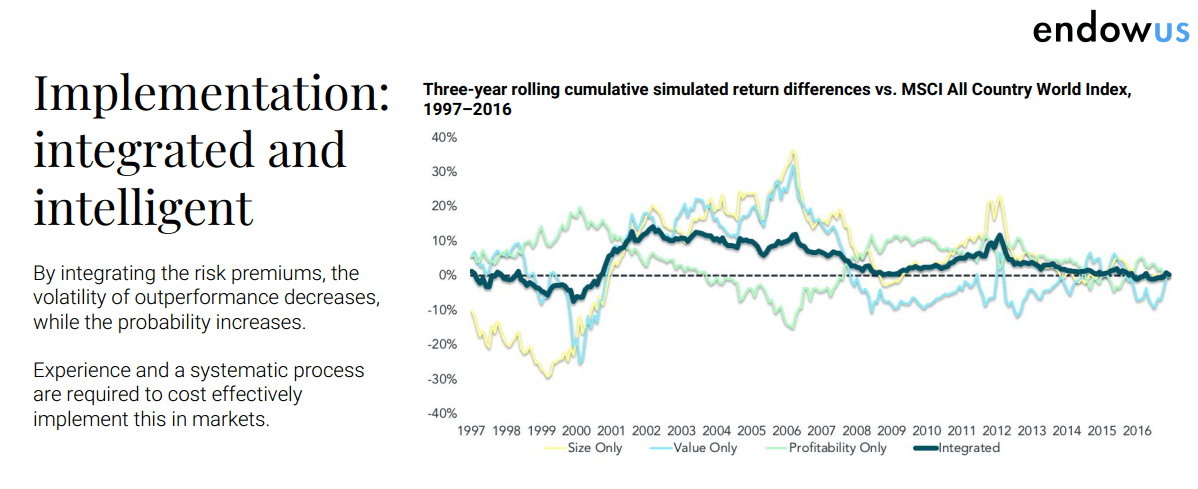

The Advantage of Implementing the Factors Together

In the last section, we see how each factor performed individually. It would be rather difficult for an individual investor to have the resources to find the selected stocks or bonds that meet all the factors. Thus, we need a good implementer for this.

While some factors may underperform, if we integrate them appropriately, there is a higher likelihood that this would result in an outperformance over a plain index.

In the illustration above, we do see that there seemed to be periods where the integrated factors result in less and less premium. Even in the 1990s, when growth and tech stocks did very well and value did poorly, we see that the integrated factors did underperform over at least 2 years.

In recent years, we seen the integrated line going so close to zero.

I do not think the factors do not exist or will stop to be persistent. I do believe as investors, we can be unlucky to be in a period where these factors do not work as well. And we may be in a period now. And here is where the proponents of investing in a passive index will gain a lot of strength.

Vanguard versus Dimensional Funds

Vanguard has always been the mutual fund company that is held in high regard by investors. One of the reason is due their philosophy to investing, which translates to their products. The other reason is due to their management structure being own by their own funds. This puts the objectives of the Vanguard manager aligned with the fund holders.

A lot of Singapore retail investors wishes for funds or ETF from Vanguard to be in Singapore.

Singapore is perhaps too small of a market for Vanguard to justify their presence here and this does make wealth builders who are fans of their simple fund products disappointed.

The advantage of Dimensional Funds here is that, they have always been put to a duel by thought leaders with Vanguard.

I look at this very positively because even if Dimensional fall short, they cannot be too far off from Vanguard’s solution.

And since Vanguard is not in Singapore, Dimensional becomes a very viable solution for Singaporeans.

The best way to read more about this is to Google “DFA Dimensional Funds versus Vanguard”

There are a bunch of articles overtime written on this subject.

One good one is by Larry Swedroe, the director of research for the BAM Alliance, a community of more than 140 independent registered investment advisors.

You can read it here 2018 Aug Dimensional versus Vanguard: A Test of Simple Factor Investing.

What kind of Expected Returns?

So if you are building wealth, you need to have a rule of thumb what kind of returns over the long run you can get.

The funds are just incepted so there are no data that we can use.

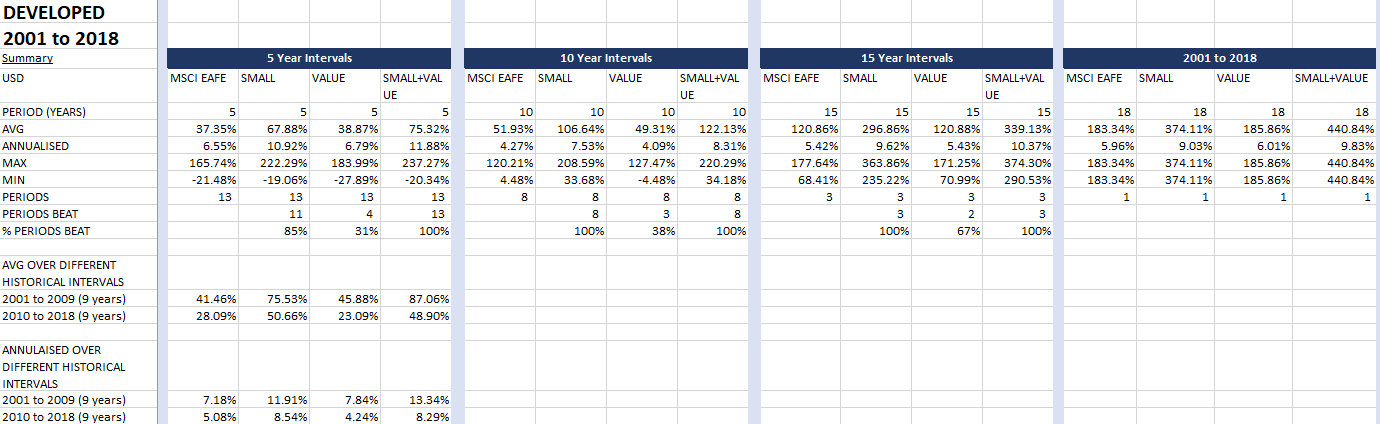

However, we can take a look at some of the returns data of the indices that the DFA funds are benchmark against.

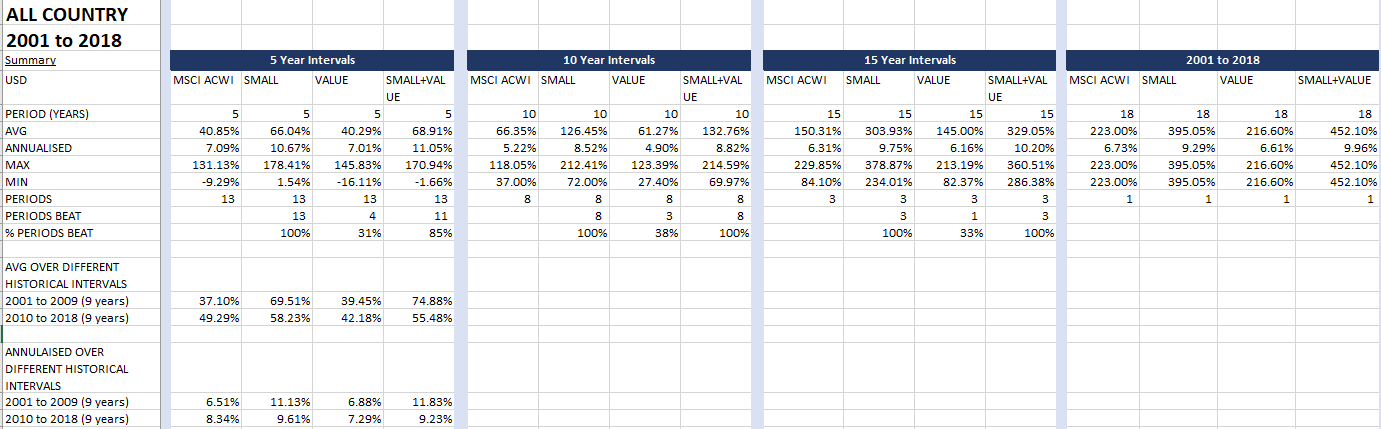

The table above shows the summary of the MSCI ACWI index performance against the MSCI ACWI Small Cap, MSCI ACWI Value and MSCI Small Value Index.

This is probably closer to the DFA World Equity and DFA Global Core Equity Fund by endowus, Providend and MoneyOwl

Do note that there are no fees involve.

The Profitability dimension is not in the equation.

The data let us see whether over the 5, 10, 15 year time frame there is a value premium. The sample size is small since they only have 18 years of data.

We can see the annualized returns for 5-year intervals is 7.09%, which outperformed the value index of 7.01%. However, when you factor in the cross-section of small + value, the annualized returns is 11.05%. If we go to the 15 year time frame it is 6.31% versus 10.20% for small + value.

The annualized data for the rolling periods show:

- 13 5-year periods: average annualized return 7.09% versus 11.05% in small + value

- 8 10-year periods: average annualized return 5.22% versus 8.82% in small + value

- 3 15-year periods: average annualized return 6.31% versus 10.20% in small + value

At the bottom we can see 2 different 9 year periods 2001 to 2009 and 2010 and 2018. The returns are pretty uniformed.

But we can see two things pretty coherent is that

- small caps tend to outperform

- value really struggled in the second 9 year period

Do note also: The MIN shows the lower bound of the different rolling years. In a 5 year period, you have some 5 years where the returns will be negative.

It is not all good. However, the small + value cross sectional combination improved the returns a lot (notably the small cap dimension)

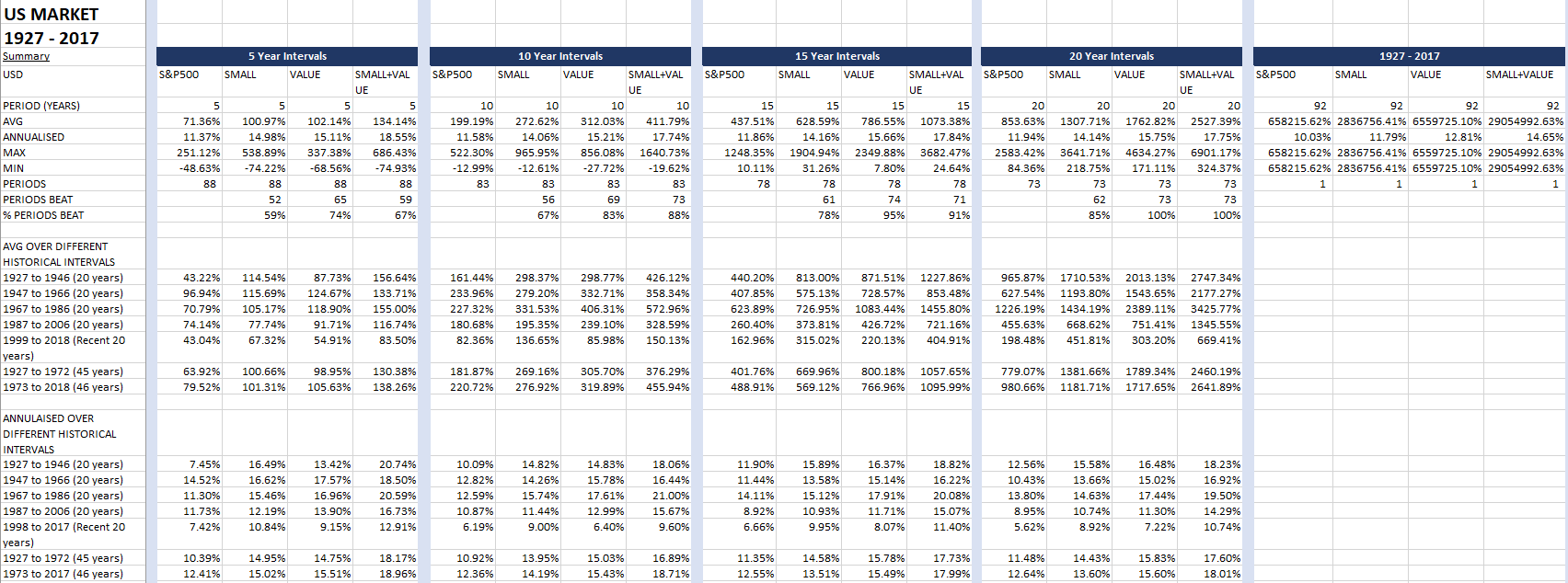

In contrast, we have more data for United States. There are like 73 period of 20 year data.

The annualized data for the rolling periods show:

- 88 5-year periods: average annualized return 11.37% versus 18.55% in small + value

- 83 10-year periods: average annualized return 11.58% versus 17.70% in small + value

- 78 15-year periods: average annualized return 11.86% versus 17.84% in small + value

- 73 20-year periods: average annualized return 11.94% versus 17.75% in small + value

The USA data is just a bit crazy. I have to double check again to see if I am interpreting correctly.

The data above is for MSCI EAFE.

The annualized data for the rolling periods show:

- 13 5-year periods: average annualized return 6.55% versus 11.88% in small + value

- 8 10-year periods: average annualized return 4.27% versus 8.31% in small + value

- 3 15-year periods: average annualized return 5.42% versus 10.37% in small + value

The returns of MSCI EAFE lag that of the MSCI ACWI, which means United States have been picking up the slack. This drives home the point of being globally diversified.

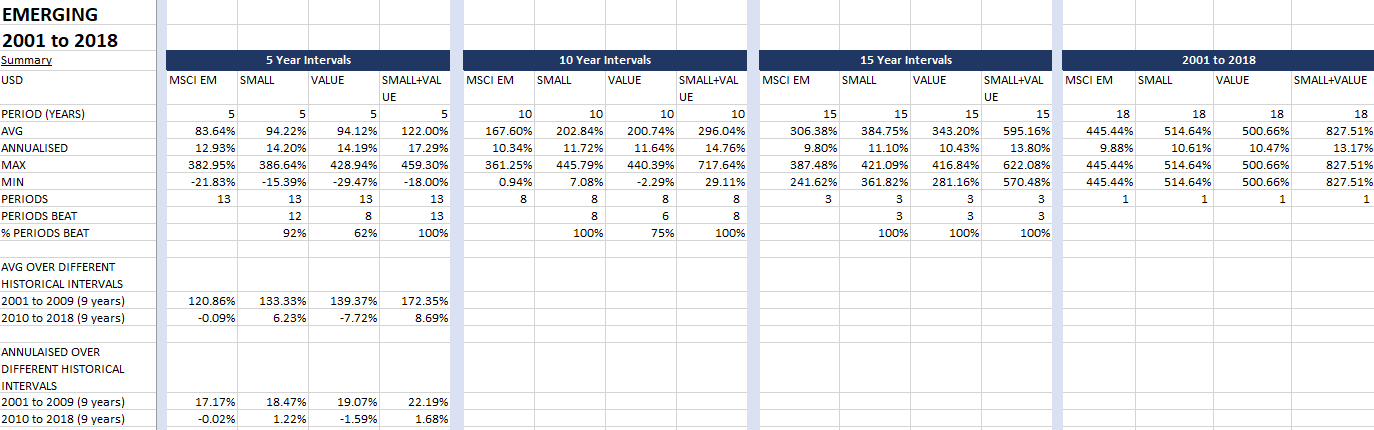

The data above is for MSCI Emerging Markets.

The annualized data for the rolling periods show:

- 13 5-year periods: average annualized return 12.93% versus 17.29% in small + value

- 8 10-year periods: average annualized return 10.34% versus 14.76% in small + value

- 3 15-year periods: average annualized return 9.80% versus 13.80% in small + value

This is probably closest to Dimensional Emerging Markets Large Cap Core Equity Fund by MoneyOwl and Providend

The returns are good, probably factor in the great performance from 2001 to 2007.

But do note the MIN in the 5 year returns. There are 5 year periods where the index look pretty bad.

These are past returns. In the future, the returns might look rather different.

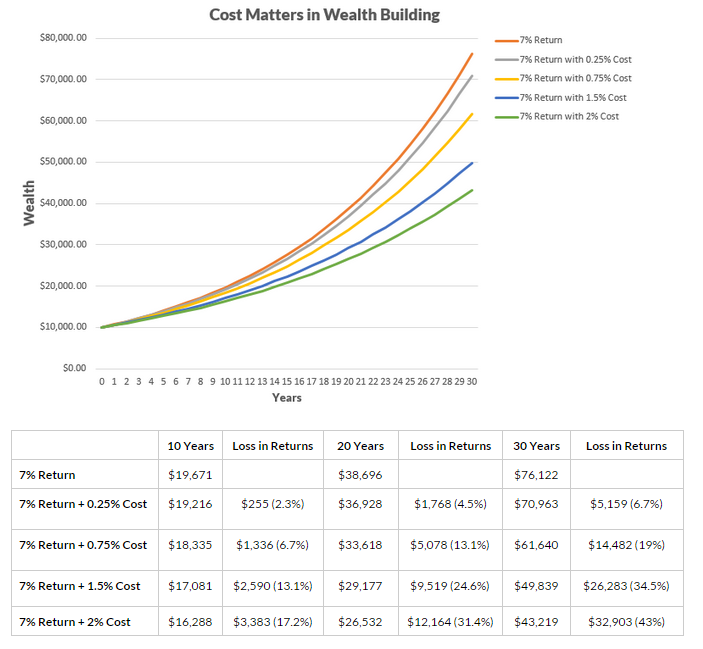

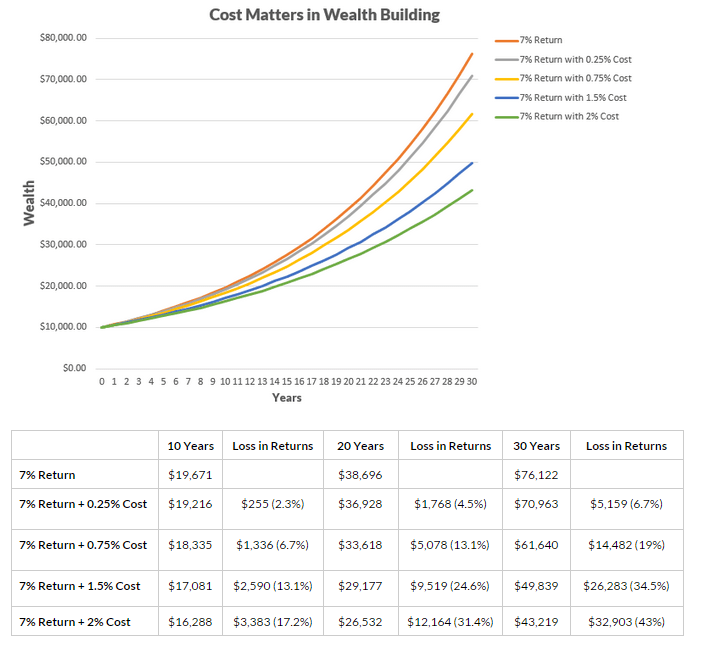

Cost Matters – Comparing the Dimensional Fund Provider’s Total Cost versus Competitors

After reviewing the returns, you would notice that in some of the back tests, endowus illustrated the results with different costs.

It lets you know the impact on cost on your returns.

The illustration above shows how much $10,000 will grow to in 10 years, 20 years and 30 years, if the compounded average rate of return is 7%.

If you add a little cost of 0.25% to it, we start losing some returns. If we add 0.75% cost to it, we start losing more returns. The longer the horizon, the greater the cost compounds.

You would not know whether you will get 4% to 10% over the long run, but you know your costs will always be there, and the cost is compounding. Returns are uncertain, cost is not, cost is certain.

The morale here: You need to minimize your cost, unless you know that the returns you are investing in for sure will make money.

Explaining The Cost Stack for Fund Investing

A lot of active investors I spoke to do not like to invest in unit trust because they say the costs is prohibitively high. And they may be right. However, we cannot run away that there are a set of costs that we incur as wealth builders if we want to build wealth more passively.

Investors are less informed about what are the costs they are subjected to because some of the costs are hidden.

Generally, I see 2 distinct passive portfolio investing models out there:

- DIY Passive ETF Portfolio Investing

- You have to transfer funding to your brokerage platform

- You have to initiate the purchase and sale transaction

- You pay a one time sales charge / commission. If you are in your accumulation phase, this will be frequent. If you stop, you do not pay the sales charge / commission on the transaction

- However, do remember that a fundamentally sound tactic is to re-balance your portfolio, and doing this the DIY way in retirement, would incur sales charge / commission

- There are no recurring company management fee

- There are sometimes custodian fee that your brokerage charge for giving you the service of holding your shares in their care, dividend handling charges, corporate charges. Some brokers

- For example buying Vanguard and iShares ETF listed in UK and USA through UOB Kayhian, DBS Vickers, Standard Chartered Online Trading, Interactive Brokers

- Managed Portfolio Solutions

- You transfer funding into the platform used by a managed solutions

- You have to initiate the purchase and sale transaction. For some platforms you can set up a standing instructions to recurring purchase more investments which makes this even more passive

- There are no sales charge / commission

- There is a recurring company management fee

- There is sometimes a platform fee. Platform fee differs from company management fee in that the company doing the management solutions leverages on the broker solutions of the platform to execute seamlessly. Thus you have to pay a charge for it. For example, MoneyOwl and AutoWealth both charges a platform fee. MoneyOwl makes use of iFast and you have to pay 0.18%. For AutoWealth you pay a flat S$18 platform fee. For endowus, they make use of UOB Kayhian but the platform charges are waived

- For example purchasing the passive ETF and funds solutions from Stashaway, MoneyOwl, endowus, Autowealth, Smartly, CIMB eWealth and OCBC

The main differences between the two category is that #1 there are less recurring charges. Your cost ends usually after your transactions. So I can imagine once you retire you save up on these. However, when you are retired, you may still re-balance your portfolio, to bring the portfolio back to its targeted weighting. So you would sell part of your portfolio to buy another part. Typically, we can assume you will buy and sell like 20-30% of your portfolio.

In contrast #2 is the distinct recurring AUM model. The company tries to let you know there are advantages to them managing your portfolio than you. They do the rebalancing. They re-allocate your ETF at the certain time without your instructions. They handle a lot of the background work of wiring money to a broker at the most optimum costs, which for #1 you do it yourself.

Which is cheaper in the long run? The DIY Passive ETF Portfolio Investing option. This is within your control. You can read my article AUM Fees vs Commission Sales Charges – Which is Cheaper?

However, that is only one side of the equation.

What is less mentioned is that there are some hidden fees that will be incurred on both kind of investing categories. They can be one time only or recurring.

These would be

- foreign exchange spread

- bid/ask spread

- fund tracking error

#1 This will depend on the ETF or the funds that you invest in as well as the platform. For example, when you want to invest in iShares Core MSCI World UCITS ETF (IWDA), you transaction to your DBS Vickers broker in SGD. The broker converts your SGD to USD to eventually purchase IWDA. There is a foreign exchange spread there. Typically, it is 0.50%. For those who use Interactive Broker it is very low like close to 0.02% from what I heard.

#2 If you chose to purchase IWDA on the London Stock Exchange or other ETF listed there, depending on the liquidity, you might be paying the market maker a slight cost. This depends on the liquidity of the ETF. Some ETF is more popular, or during certain more euphoric markets, the liquidity is better. The liquidity is observed to be better in the USA, so you can say that the bid/ask spread cost is lower.

#3 For the ETF that tracks a certain index (for example the IWDA tracks the MSCI World), there is a fund tracking error or the difference between the ETF’s performance versus the actual index. We do not have this problem for the DFA funds because the benchmark index is use as a reference to observe performance. There is no mandate to track it.

So this is the whole cost stack. If you do not know when you purchase your unit trust, or invest in your robo advisors, I summarized them below:

So a little cost here and little cost there and they add up.

There are 2 sets of costs that I have not explained:

- H: Dividend Withholding Charges

- I: Estate Duty/ Death Taxes

This deserves another section and I would explain below.

In general I would aggregate 2 figures: the Total Overall Cost and the Total Recurring Cost. The Total Recurring Cost is to give a realistic comparison of running cost on a recurring basis. I have included sales charge/commission in it which might be controversial but I do see re-balancing as an important component and it is not like you buy and you will not sell.

The Total Overall Cost do not include the Estate Duty.

Now we can do some comparisons.

Comparing MoneyOwl and endowus solutions to DIY Investing and Unit Trusts

Doing comparisons is always going to be frustrating because these stuff are often not all apples. So we cannot do an apples to apples comparison.

I hope everyone can takeaway from this, the cost stack and the range of cost in each category. Ask questions and debate upon them.

Most of all see which are the bigger costs, the longer lasting costs.

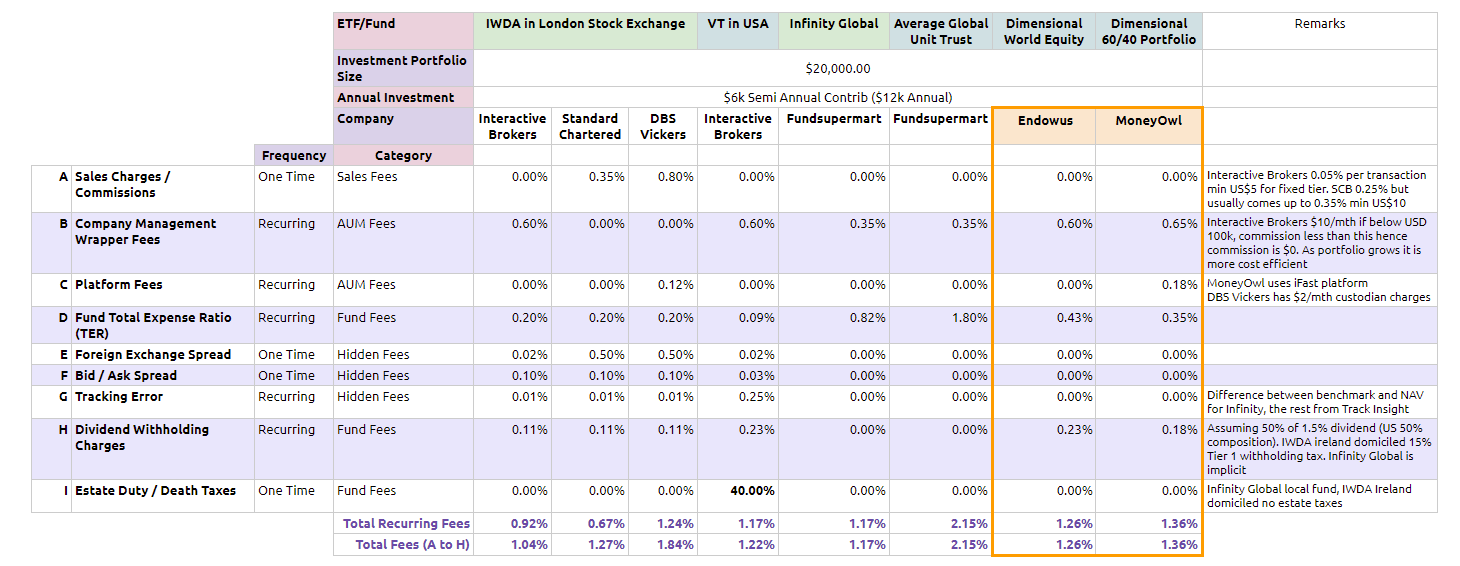

In this first section, I present this comparison for the client with $20,000 currently under management. This client will inject $12,000/yr into his portfolio. To optimize his cost, he would do it semi annually in batch of $6000.

In this first comparison we present how the cost of Dimensional funds under endowus and MoneyOwl will compare against:

- DIY ETF Portfolio in London Stock Exchange (IWDA)

- DIY ETF Portfolio in USA (VT or Vanguard Total World Stock Market ETF)

- The Lion Global Infinity Global Stock Fund, which is a wrapper to Vanguard Global Index Fund

- An Average Global Focus Unit Trust

For IWDA, I have presented three different brokerage solutions so that you can see some realistic differences.

Here are some observations.

Little cost here and there adds up. We get total recurring fees in the range of 0.92% to 2.15%. The average cost is 1.24%. While expense ratio gets a lot of the limelight, the rest of the hidden costs, dividend withholding charges more or less equates things.

If on average the expense ratio of the fund is 0.30%, then we should factor in roughly 0.90% as management cost that is not reflected in a fund’s factsheet.

VT has the lowest expense ratio. Vanguard have a history of trying to bring down the expense of their funds as much as possible. While its listed at 0.09%, I might have made a mistake and it is closer to 0.10% (which is not a whole lot different). VT being listed in the US, is likely to have very low bid ask spread (0.03%) versus the UK listed ones (0.10%).

I can’t reflect a lot of the costs of Infinity Global. As a fund, it should not have bid/ask spread but they should have dividend withholding charges at the portfolio level (will be explain later) and tracking error. But since tracking error is not announced and I cannot find it, its tough for me to present here. My sensing is that the cost of Infinity Global could be 2.17% reflecting perhaps a 1% tracking error or some hidden cost. We can also see this as poorer performance versus the index while the overall cost is at 1.17%

Interactive Brokers is the Solution for Large Portfolio if You DIY. Many DIY investors who wish to keep costs extremely low uses Interactive Brokers to purchase Irish Domiciled ETFs like IWDA, VWRD and EIMI in the London Stock Exchange because:

- No management and platform fee if your size is greater than US$100,000

- Absurdly low commission (0.05% to 0.12%)

- ETFs are low cost

- ETF are optimized with regards to dividend withholding tax due to Ireland Domicile

- ETF for non resident should not subject to estate duty/inheritance tax

- Investor is sophisticated enough

While the recurring cost is 0.92% and total fees is 1.04%, a main bulk of the cost is the 0.60% company management fee. There is a US$10/mth charge if your account size is less than US$100,000. If you wish to work towards say a $500,000 portfolio, this US$120/yr will work itself out over time.

But since you DIY, you need to ensure that:

- You probably understand this whole article and more

- How to proper portfolio manage yourself

- Ensure that when the volatility increase, you do not do stupid things

- You are able to continue to purchase when the market is down

- How to use the Interactive Broker platform ( there is a whole long Hardwarezone thread that act as “support” for this. This shows how not normal is the usage process. However, I think it gets better over time)

The Global Unit Trusts are Simple but they are Just more Costly. If you buy the Global focus unit trust that I have highlighted in my Infinity Global article through Fundsupermart, there is just the quarterly company wrapper management fee and the total expense ratio. Very clean.

However, the total expense ratio alone averages 1.80%!

If you use POEMs, and Dollardex, they do not have the 0.35% platform fee. However, you still have to live with the high expense ratio.

DFA Portfolio through MoneyOwl and endowus do not have a cost advantage over DIY Portfolio. But they do have over the typical unit trust. You probably save around 50% of the costs.

Since I list out Passive ETF Portfolio with Interactive Brokers as the best solutions, lets see how they measure up:

- Management + Platform fee of 0.60% and 0.83% (endowus can be lower if your fund size is large, but really much larger)

- No commission

- DFA funds are low cost

- DFA funds are optimized with regards to dividend withholding tax due to Ireland Domicile

- DFA funds for non resident should not subject to estate duty/inheritance tax

- Investor have access to advisory when they are less sophisticated (MoneyOwl)

So they lost out probably in #1 and gain in #6 (MoneyOwl). For sophisticated investors, you know which of the solutions to pick.

For those that, touch their heart, know they are less sophisticated, that access to behavioral coaching, clarification may be the difference between earning 2%/yr compounded returns versus 7%/yr compounded returns (we explain more in the Adviser’s Alpha).

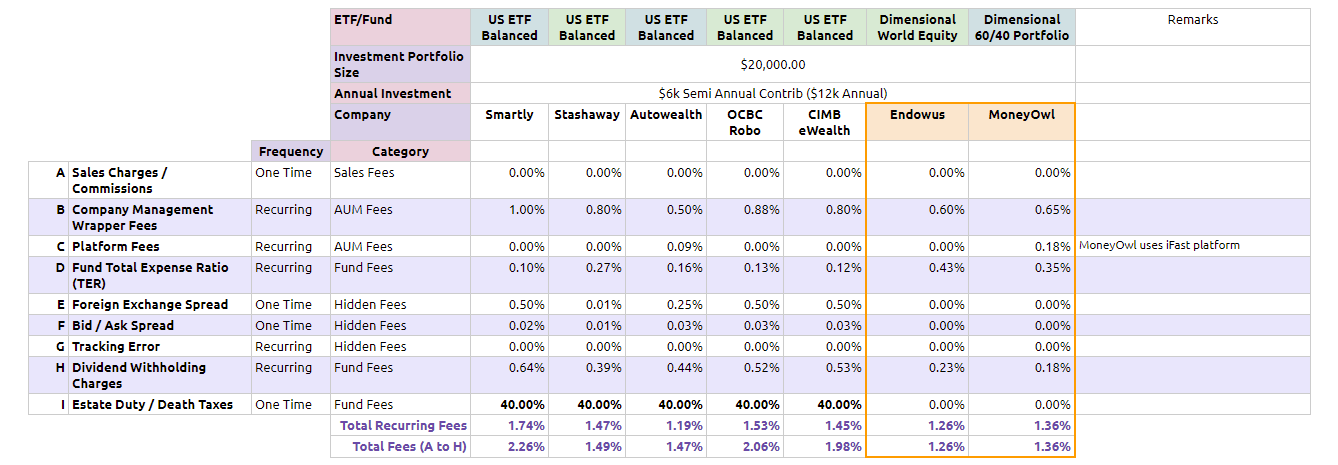

Comparing MoneyOwl and endowus solutions to Other Robo Platforms

The next cost comparison is to ascertain whether endowus and MoneyOwl’s solution is competitive versus the robo platforms out there:

If we look at the recurring fees, Autowealth is the most cost competitive. Yet majority of the robo platforms, including the 2 houses that is able to manage DFA funds, will have a total recurring fees of 1.3% at least.

Two things stood out for the other robo platforms.

The first is that the dividend withholding charges are higher. This may be likely because the platforms give you access to NYSE listed exchange traded funds which are domiciled in USA. However, on the portfolio and fund level, if you invest in USA listed ETF, you may be taxed twice (refer to the withholding tax section below to see the explanation).

The second is that because they are using USA domiciled funds, if you do not take care of it well, the estate duty / inheritance and death taxes would mean that you might not be able to passed on 40% of your accumulated assets to your next generation.

I tried my best to estimate the foreign exchange spread for the robo platforms but in truth it can be rather hard, so don’t take those high foreign exchange spread seriously. It is a reason why I aggregate 2 different total cost, one for a more meaningful recurring fee and one total fees. If you factor in total fees the solutions from OCBC, Smartly and CIMB looks costly.

The Bid/Ask spread for the robo is very low, likely due to the greater liquidity for the exchange traded funds listed in the world’s most popular exchange.

The DFA funds in endowus and MoneyOwl, do not have this issue because they are open ended unit trusts that tabulate their net asset value together with new funds that come in at the end of the day, instead of being daily traded, so there is no spread there. The typical spread in unit trust tend to be sales charges, charged by a platform say Dollardex.

Since there is no sales charge on DFA funds, the bid/ask spread is effectively zero.

We also notice that the average total expense ratio for portfolio of the robo platforms are lower than those in DFA funds, and those UCITS ETF listed in London Stock Exchange like VWRD, IWDA, EIMI.

This is a good thing definitely, if we are looking at expense ratio alone.

However, if we look at it in totality, as a portfolio ownership cost stack, there are some costs not accounted:

- higher company management wrapper fee

- more inefficient dividend withholding tax

- estate duty and death tax uncertainty

Why do you pay a Higher Cost for – the Adviser’s Alpha

Since I have time and again said cost matters, what do we make of these offerings with a company management fee?

This is in contrast if you purchase it DIY through the lowest cost platform such as Interactive Brokers. What are we paying for then, and is it worth it?

What you are paying for is

- The ease of access, to review your investments

- The ease of investment. The platforms make investment process much easier instead of navigating tough processes. In some DIY case, you need to wire the money to the account, then know how to exchange the SGD to USD/GBP. Then you can purchase. And you did not automate it. If you do not automate it, you might not buy when prices are falling.

- A one stop shop for not just investments but also protection

- Behavioral Coaching

I think it can be quite easy for a financial planner to justify why you should pay them more. A lot of them are trained to throw smoke bombs at you.

But I think if you have access to someone competent to ask, it might stop you from making mistakes.

When you make less mistakes, you lose less money. You made money where you otherwise wouldn’t have invest. A lot of times it is clarification of doubts.

If you make an investment decision with a train of thought, you better hope that trained of thought is sound.

If you have a conflict free, high integrity adviser, this validation and clarification is probably worth that 1%.

This is probably the famous Dalbar study.

It shows the 20 year annualized returns of various kinds of asset class.

Notice the worst performer. It is the Average Investor.

Why did the average investor do so poorly? Dalbar cites a few reasons:

- Panic selling during market downturns.

- Exuberant buying at market highs

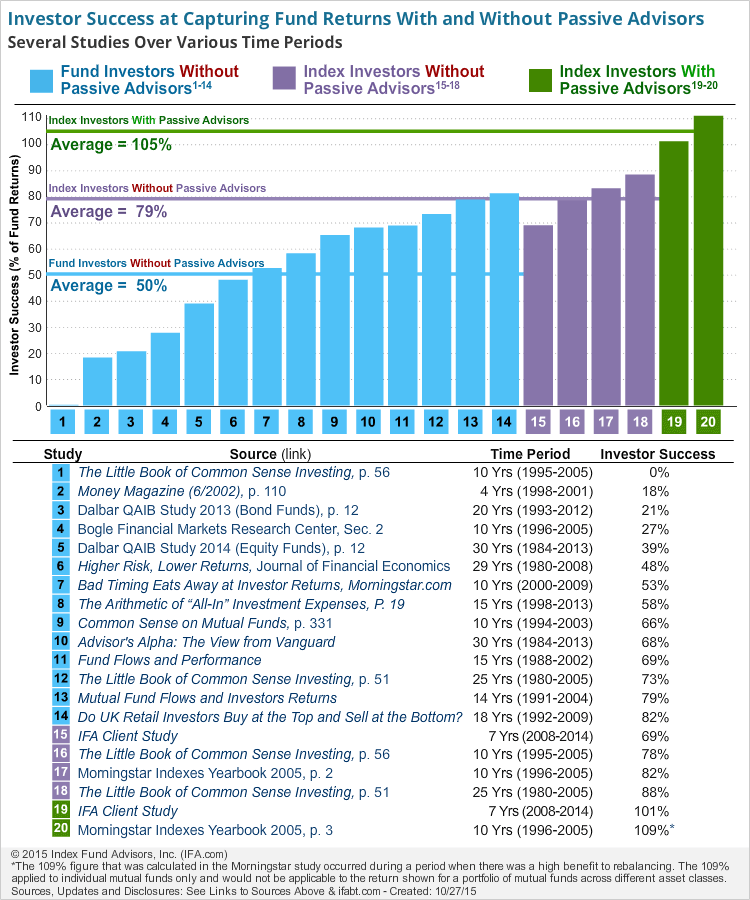

I found the following illustration from the very good website IFA.com which further emphasize the role of advisers in enhancing your final returns:

This is a compilation of 20 studies which depict the varying levels of investor success with or without passive advisors:

- the average fund investor without passive advisors captured only 50% of the returns

- indexers without passive advisors capture only 79% of the fund returns

There is 2 studies, one by IFA client study (themselves) and another by Morningstar which shows that those investors with DFA advisors was able to capture 105% of the returns.

How true is this? I think it would be how close you are to the adviser. If the solution is a robo platform which provides you an access to a fund, which otherwise you could not get, and not advisory service, then you are on your own to navigate this volatile and confusing wealth building world.

Those who paid money to have a person to hand hold, would see better results by virtue of sticking to the principals.

A large part of investment success is determine by you overcoming your behavioral issues. This is why a lot of the upfront and recurring efforts that is require for this form of investing involves reading up and reflecting on your past or future potential behavioral tendency.

If you are not going to spend effort doing this, I recommend you to find a good wealth coach, pay him or her, or them, so that you can stick to it.

I do not think you want your DFA portfolio to earn 8% on average but the past 15 years you only get 3% due to you being too confident about yourself.

DFA Funds are Much More Optimized for Dividend Withholding Tax and Death Taxes

2 of the costs mentioned in the cost comparison are dividend withholding taxes and estate duty/inheritance taxes/death taxes.

When you invest in financial assets that are cross border, you have to contend with this.

Let us tackle dividend withholding taxes.

- A global fund owns a basket of companies and these companies are in different countries. These companies are incorporated in their own country, or another country such as Cayman Island, Singapore, Bermuda, Hong Kong, Ireland for tax efficient purpose. We call this country where the stock is domiciled

- The fund itself needs to be incorporate in one country. We call this country where the fund is domiciled

- When dividends are paid by the stock to the fund (such as DFA Core Equity Fund or a Vanguard World Stock ETF), and the dividends leave the country where the stock is domiciled, the country will have a withholding tax

- The amount of withholding tax depends on country to country

Some countries have withholding taxes, some do not. For example, Singapore do not have withholding taxes for non resident individuals. However, if you are a non resident corporation or partnership, there is a 10% withholding tax.

For the larger countries, here are the withholding taxes:

- United States: 30%

- China: 10%

- Australia: 30%

- Germany: 25%

- Japan: 15%

- UK: 0%

- France: 30%

A lot of countries having 30% withholding taxes on dividends. If a country has a tax treaty, then the taxes are reduced.

For example, Ireland have a tax treaty with the United States, so for the businesses domiciled in Ireland, if they have a subsidiary in USA, the withholding tax on income is only 15% instead of 30%.

Now, when the fund pays the investor after receiving the dividends from the underlying stocks, depending on the domiciled location, there may be further taxes!

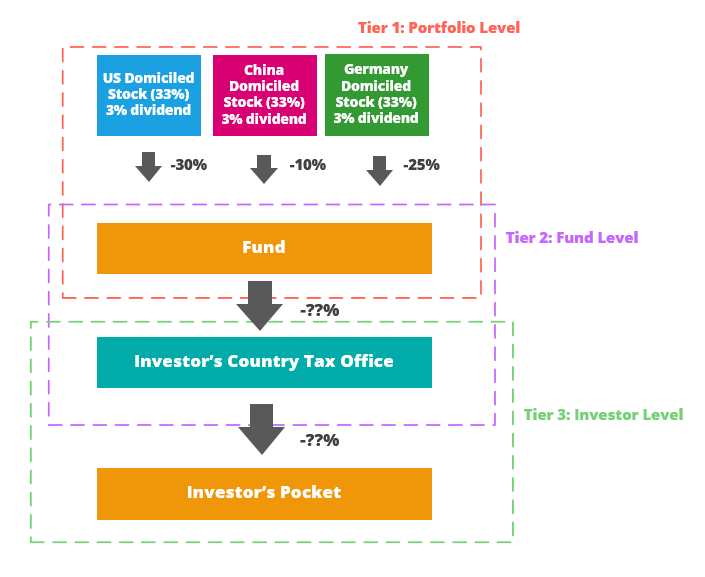

This is a bit complex so I think it is better to explain through a diagram. In general, there are 3 tiers where the dividends can be taxed. Each tier will tax the net amount from the previous tier:

- Tier 1: When the underlying stocks pay to the fund

- Tier 2: When the fund pays to the investor’s tax office

- Tier 3: Before the investor gets the money, some country may have a further tax on the dividends from foreign sourced

Our typical scenario is a world equity fund that owns 3 stocks, one in US, one in China and one in Germany. All pay out a 3% dividend. (Just bear with me. It is to explain a concept. I know the composition of a world equity fund should not be in only 3 stocks)

Let us take a look if this is a

- DFA world equity fund, which is domiciled in Ireland. Ireland have 0% dividend withholding tax

- iShares Core MSCI World UCITS ETF (IWDA), which is a Ireland domiciled ETF

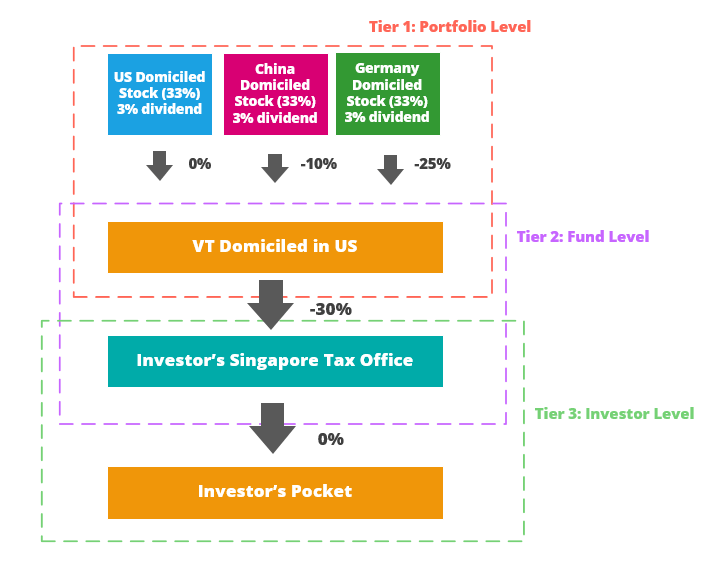

- Vanguard Total World Stock ETF (VT), which is a US domiciled ETF

Vanguard Total World Stock ETF (VT)

The illustration above shows the taxation at different levels. Since VT is domiciled in US, when the dividends from the US stock is paid to the fund, there is 0% withholding tax. There are however 10% and 25% withholding taxes for the China and Germany stock.

At the fund level to the investor’s tax office in Singapore, there is a 30% withholding tax.

Since Singapore currently do not tax on investor’s foreign sourced income, there is 0% tax when the investor receives the dividend finally.

So this works out to:

- US dividend: 3% x (1- 0.0) x (1-0.30) x (1 – 0.0) = 2.1%

- China dividend: 3% x (1- 0.10) x (1-0.30) x (1 – 0.0) = 1.89%

- Germany dividend: 3% x (1- 0.25) x (1-0.30) x (1 – 0.0) = 1.575%

- Overall dividend: 1.836%

- Dividend withholding tax cost: 3%-1.836% = 1.163%

The mileage would vary depending on the size of the average dividend, and the composition.

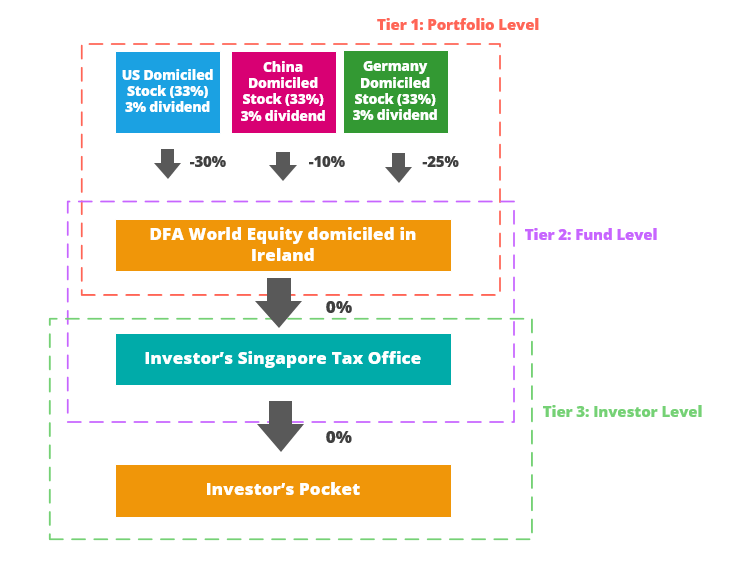

Now lets see the DFA World Equity Fund’s situation

DFA World Equity Fund

The illustration above shows the taxation at different levels. Since DFA funds available for Singaporeans is domiciled in Ireland, US withheld 30% of the dividend, China withheld 10% of the dividend, Germany withheld 25% of the dividend.

At the fund level to the investor’s tax office in Singapore, there is 0% withholding tax, since Ireland currently do not have withholding taxes

Since Singapore currently do not tax on investor’s foreign sourced income, there is 0% tax when the investor receives the dividend finally.

So this works out to:

- US dividend: 3% x (1- 0.30) x (1-0.0) x (1 – 0.0) = 2.1%

- China dividend: 3% x (1- 0.10) x (1-0.0) x (1 – 0.0) = 2.7%

- Germany dividend: 3% x (1- 0.25) x (1-0.0) x (1 – 0.0) = 2.25%

- Overall dividend: 2.326%

- Dividend withholding tax cost: 3%-2.326% = 0.6735%

You can see how much efficient Irish domiciled funds are. The difference is like a 0.50% recurring cost there (which might offset some of US domiciled fund’s advantages). Of course it would depend on the size of the dividend.

DFA funds available to investors are UCITS funds and they have certain advantages to guard investors interest.

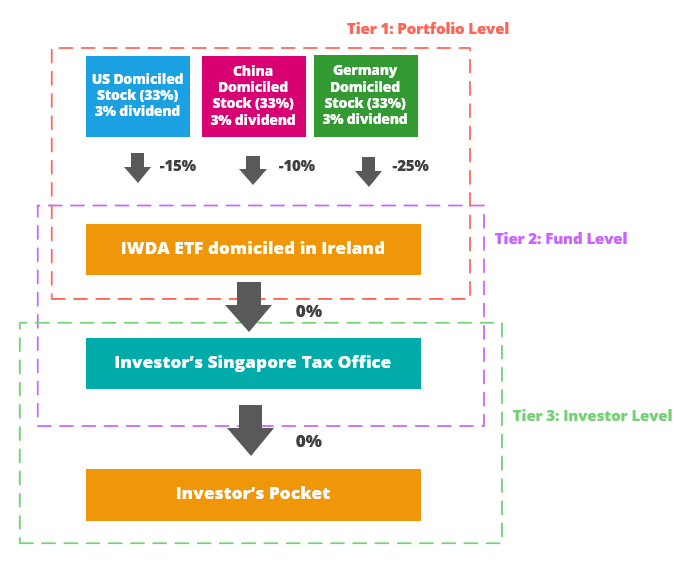

Now lets see IWDA’s situation

iShares Core MSCI World UCITS ETF (IWDA)

IWDA’s situation is very much similar to the DFA funds, except that they have a double taxation treaty with the US in activation.

Thus on US, they only withheld 15% of the dividends for taxes. Why is there such a difference? I have no idea. I guess that is how its treated. To the best of my knowledge, we do know that the withholding tax for the Irish domiciled DFA funds should be 30%. (Note: Still checking. It might be the case the Ireland domiciled funds and ETF has the tax treatment)

So this works out to:

- US dividend: 3% x (1- 0.15) x (1-0.0) x (1 – 0.0) = 2.55%

- China dividend: 3% x (1- 0.10) x (1-0.0) x (1 – 0.0) = 2.7%

- Germany dividend: 3% x (1- 0.25) x (1-0.0) x (1 – 0.0) = 2.25%

- Overall dividend: 2.475%

- Dividend withholding tax cost: 3%-2.475% = 0.525%

IWDA in this regard, and for the Irish domiciled ETFs, should be the most tax efficient.

The handling of Interest Income Withholding Tax on Bond Funds Such as Dimensional Global Short Fixed Income Fund

So if there are dividend withholding tax on equity what about the tax on interest income on bonds?

Since the Global Short Fixed Income Fund is a fund which invest in a basket of bonds around the world, domiciled in Ireland. In contrast, the other popular route for investors is to invest in high yield, or general bond funds domiciled in the USA.

How much interest income withholding tax the fund is subjected to depends on the withholding tax on interest income in each country.

In the USA, exchange traded funds that generate qualified interest income and short-term capital gains, may be exempted from United States withholding tax when distributed to non-US holders. The US Tax law permits a regulated investment company (“RIC”) to designate the portion of distributions paid that represent interest related dividends (normally known as qualified interest income) and short term gain dividends as exempted.

- you need to be a regulated investment company and provide proper documentation to qualify. Thus, DIY investors would not be exempted

- bond interest income from USA bond generally are exempted from dividend withholding tax

Here are some examples:

- for US Government Bond ETFs, typically 100% of the interest income qualify as Qualified Interest Income. One example is the iShares 10-20 year Treasury Bond ETF (TLH) used by Stashaway

- for US Corporate Bond ETFs, perhaps only 70-80% of interest income qualifies as Qualified Interest Income. One example is the iShares IBOXX Investment Grade Corporate bond ETF (LQD)

- for international bond ETF domiciled in USA, the Qualified Interest Income may not be applied at all. One example is the iShares International Treasury Bond ETF (IGOV) used by AutoWealth

For those funds or ETF domiciled in Ireland, the USA bonds are subjected to withholding tax and that could be 30% or 15% depending on whether it is a fund or ETF.

Do remember, while USA have been a popular discussion, the withholding tax treatment for other countries will mean that there may be withholding tax incurred there, which might be more or less than the United States withholding taxes.

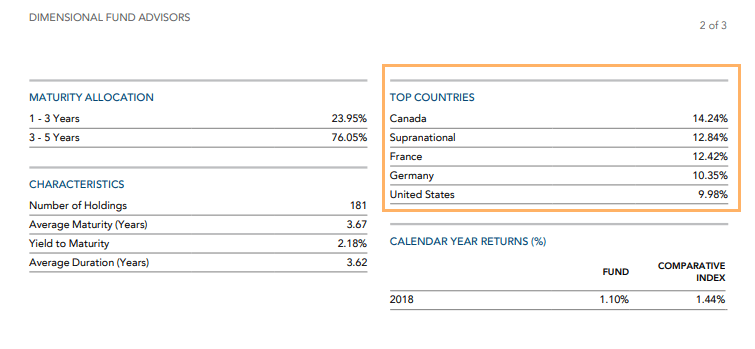

If we look at the latest factsheet for the DFA Global Short Term Fixed Income fund, US bonds constitute about 10% of the fund. The USA withholding tax costs is largely minimized, but does bring about the tax efficiency in relation to the other countries.

Does the DFA Funds Pay out a Dividend to DFA Fund holder?

While we are on the topic of dividend, you might be curious whether, if the underlying shares pay out dividends, does the DFA funds pay out to you periodically as well?

If you look at the description of the funds I put far above, you would see that I put them as accumulating.

This means that instead of paying out the dividends, the funds accumulate the dividends and reinvest them back into the fund.

If they do not pay out the dividends (accumulating), does that mean we avert the dividend withholding tax? From what I gather, this is not the case.

The underlying company will still have to pay out the cash, and unless there is a local entity where the cash is kept and reinvest back into that country, it is likely the cash will be repatriated to the domiciled country, and taxes will have to be paid. I doubt the fund will create like tens to twenty sub companies to be tax efficient.

So short answer is no, your dividends will flow back into the funds.

Avoiding the Estate Duty / Inheritance Tax Issues

Prior to 2008, there is an estate duty levied on the estate of those who passed away in Singapore. This means that above a certain concession amount, there is a tax on the net worth of the person that passed away. One justified reason is to ensure that the wealth is not concentrated.

This estate duty was removed in 2008 for Singapore. However, in other parts of the world estate duty, or inheritance taxes are pretty common.

One of the popular countries where ETF is domiciled is in USA. They have a 40% estate duty above US$60,000. There is an inheritance tax of 40% above 375,000 pounds. These are hefty shaves off the net worth for your next generation.

So for example, you invest with a local brokerage that has access to USA and you accumulate by purchasing the Vanguard Total World Stock Market ETF (VT) listed in US over 30 years.

You have accumulated SG$900,000 or US$666,666. The first US$60,000 is not subjected to estate duty, so US$606,666 would be subjected to it.

A 40% tax would mean US$242,666 will go to the US IRS!

If you are non resident investor investing in a USA ETF, would you be subjected to this?

Some say no, some say legally yes. And it is something that you need to think about if you are investing in USA based ETF.

A lot of the robo platform in Singapore are using the USA ETFs, so this is something to check with them.