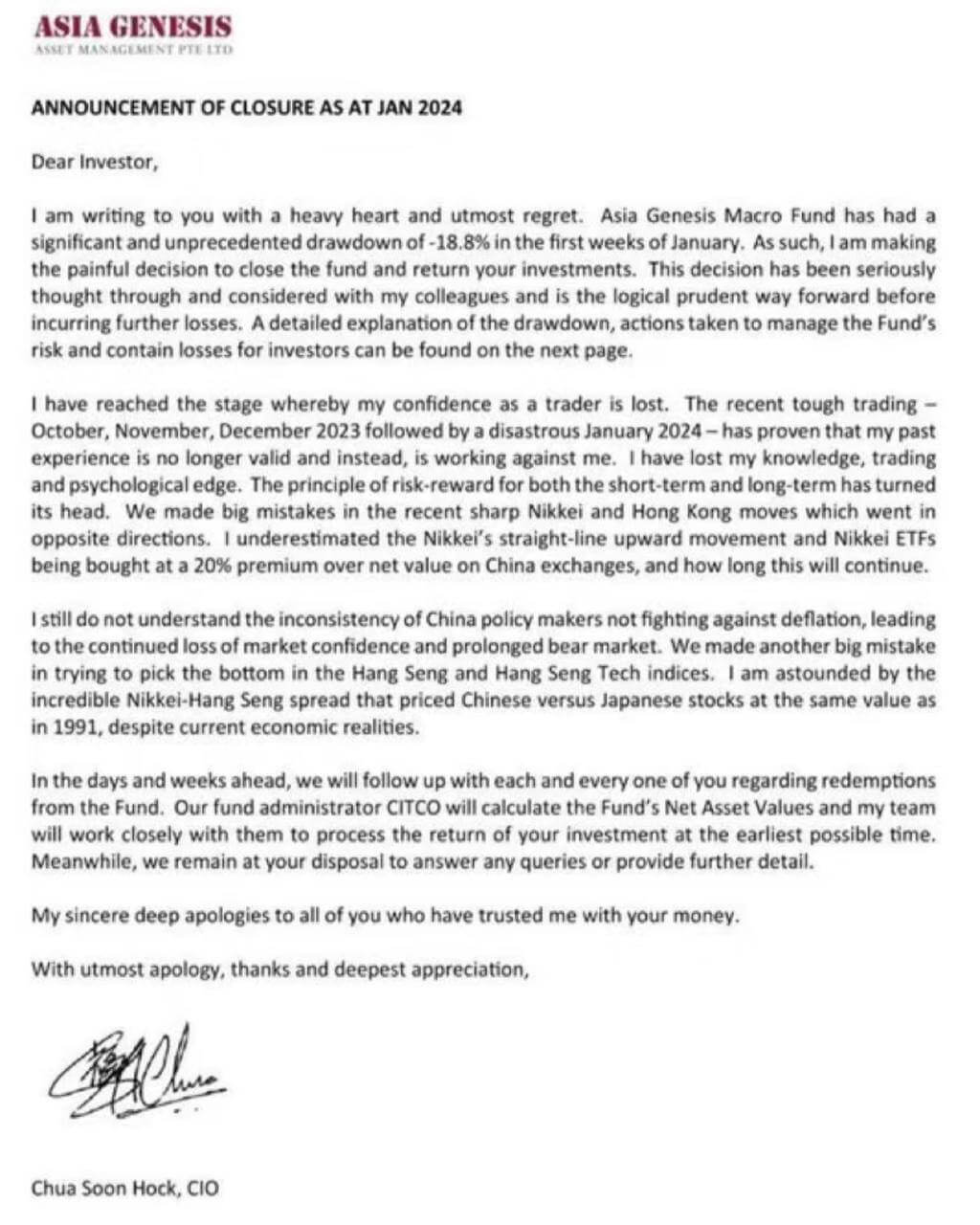

In recent news, local fund manager Asia Genesis put out a succinct letter to shareholders to explain their recent performance for their Asia Macro fund, what happened and their decision to close down the fund:

The fund was incepted not too long ago in 2020. From the Asia Genesis website, we can derive the following information:

The fund’s goal is to seek capital preservation and positive annual compounding. That message is meant to appeal to many of us because this is the goal we all seek:

- Don’t lose money

- Don’t lose out to inflation.

#1 and #2 are hard to achieve together because most strategies that do very well in each will do badly in the opposite.

Chua Soon Hock, the CIO, is a trader. There is no masquerading that they have some magic formula but that if you invest with them, you are tapping upon their sophistication in trading.

The fund has been positive even in a year like 2022, where most strategic buy-and-hold portfolios have been negative. Since inception, the fund’s 31% cumulative net returns is half of the 62% return of IWDA (which tracks the MSCI World), but similar to the performance of EIMI, the MSCI Emerging Markets IMI ETF. The fund is keeping up with the index that they measure against as well.

Unlike many (including ourselves), Soon Hock did not beat about the bush, such as lamenting about the poor performance of our selection, things turning out unexpected from what we anticipated; in normal situations, this would not happen, but it did happen.

His post admits that what I mentioned is, in fact, THE OPERATING ENVIRONMENT.

Both unexpected and expected outcomes of different aspects in investments should be expected.

Soon, Hock’s post also gives us a glimpse into something different regarding trading and buy-and-hold investing. In a buy-and-hold strategy, a 20% drawdown in the value of your portfolio is to be expected but a multi-month 35% to 60% move up is to be expected.

Within a trading strategy, this may be very different.

The more I read about such things, I think volatility drag is an area traders try to avoid and in this case Soon Hock admitted they messed up.

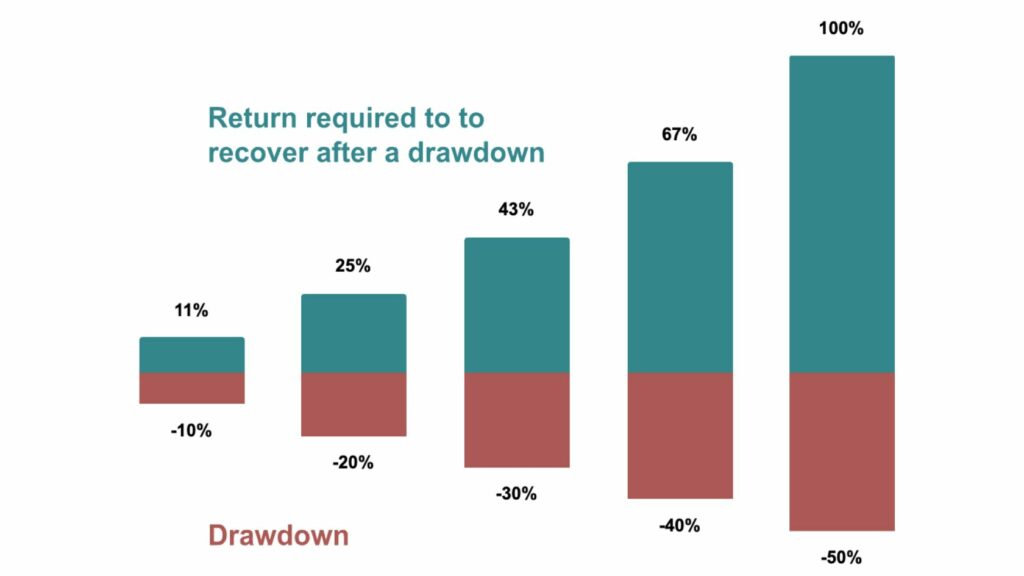

The Macro Fund probably needs a 20% return to recover and if you look at recent monthly trading performance, the highest monthly return was 4.8%, which is far from this amount.

The easy conclusion is trading doesn’t work or this fund sucks.

The average wealth builder is most often not too different from a portfolio manager with a trading mentality, just even much less sophisticated.

We all consider whether to deploy the incoming capital from work to Treasury bills, savings account, this investment, or that property.

Making investment decisions is not too different from trading. It is just that our time frame is different, and the nature of our investments is different.

I am a wealth builder, attempting to allocate my own capital, and have been a personal investor trying my hands on my individual stocks portfolio. There are times, in both roles, when I had a confidence crisis as well.

I am sure some of you would have encountered this crisis in confidence as well.

An index buy-and-hold strategy may look simple, but it’s greatest flaw is that it requires you to hold through some great volatility periods. Those periods will generate enough episodes of “Crisis of confidence” or the “do I know what I am doing (really!)” moment.

All strategies, low volatile or high volatile, will have these moments.

This crisis in confidence is a phase of investing we should all have at some point if we are successful. How we overcome it is another matter.

I wonder how many of us can write such a “I know I fxxked up” letter out to the world.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- The Cheapest Way to Extend Your Laptop to TWODisplay that I Can Find. - April 29, 2024

- My Quick Thoughts on the Net Cash, 4% Yielding Boustead. - April 28, 2024

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

lim

Saturday 27th of January 2024

"An index buy-and-hold strategy may look simple, but it’s greatest flaw is that it requires you to hold through some great volatility periods. Those periods will generate enough episodes of “Crisis of confidence” or the “do I know what I am doing (really!)” moment."

Having a large 'warchest' is useful. A large amount of reserve liquidity when volatility strikes gives you the confidence to keep on holding whatever you already have. You might even have confidence to start spending your warchest to average down.

Even having dividends are useful, because you tend to feel reassured if the dividends still keep on flowing in during volatile periods, because you know that you have bought shares in companies that have quality earnings, since they pay dividends from earnings, not share prices.

Sinkie

Saturday 27th of January 2024

This will fall under the low volatile strategies Kyith mentioned above. The main crisis of confidence for such will be when one is in the accumulating phase in a long multi-decade secular bull when one sees his peers far outstripping him in networth in growth assets.

This can only be negated by: One already reaching the portfolio / networth size that he's contented with (usually retiree stage by then);

or

One has a high income career where simply annual cash savings provide a high CAGR to his networth, and he's not dependent on investments.