One of the most common questions I observe out there in the chat is

What do you think of this product/strategy/solution? Is it good for income?

Usually, the question is phrased in this manner, and frankly, I don’t know what to say.

This is not just in chats but… I heard from our client advisers that clients will ask them about their opinions of these products. Prospects mention them or compare our retirement income solutions against these products from time to time.

It is easier for my colleagues to explain to their clients because we understand their financial situations better. After finding out what they know about these products and why they are drawn to them, we can share our perspectives about the product/strategy or solution better.

For everyone else asking, it is a struggle.

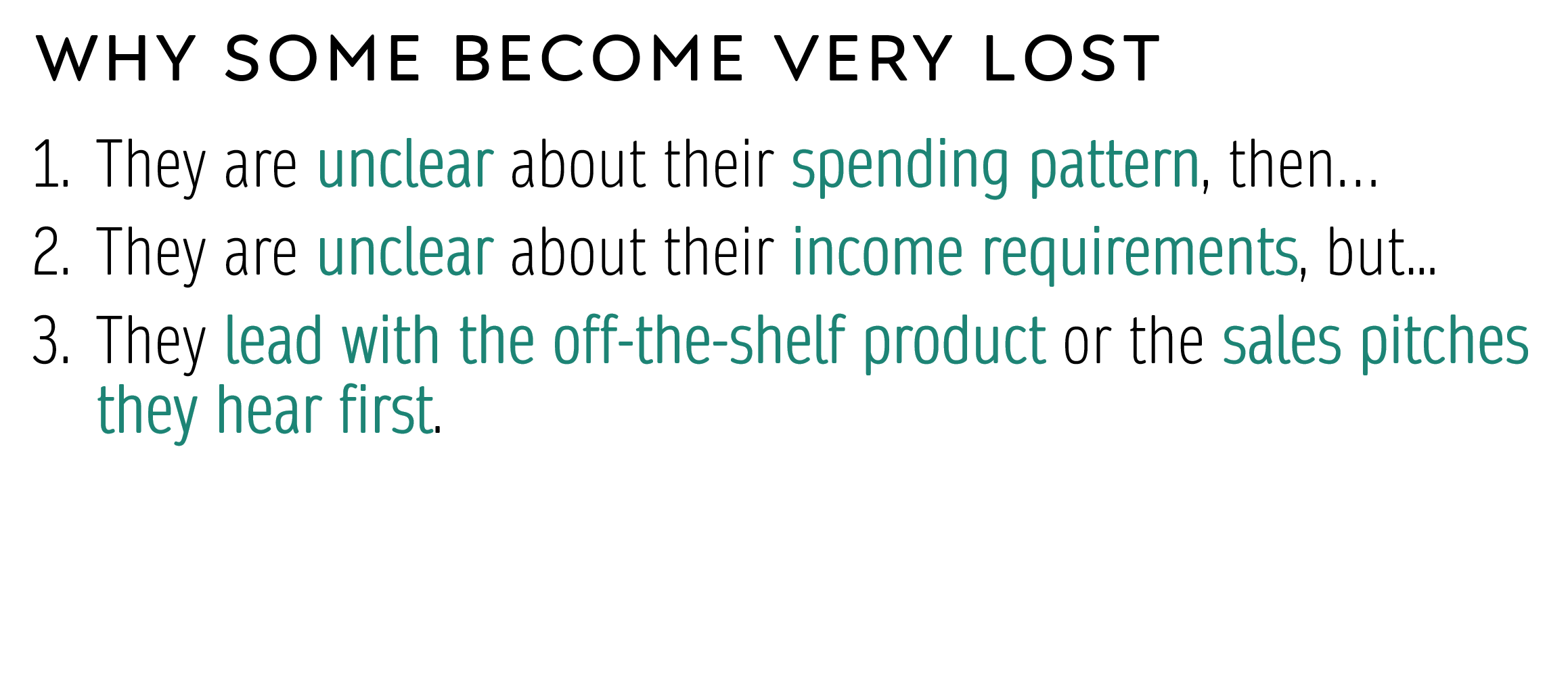

Investments and insurance are typically sold.

We don’t wake up one day with the idea that we need these things in our lives.

So we were pitched these products or investment ideas.

Then, our thinking is led by these products and investment ideas first.

We then think, and also HOPE that these products and investment idea is the holy grail to provide passive income to get me out of the rat race.

I have taken enough look at all this stuff.

Insurance endowment market as retirement income plans. Universal life plans that is flexible enough to provide income. I was a DIY individual dividend stock investor. Probably wrote a whole series, which many find really good on Real estate investment trusts (REIT).

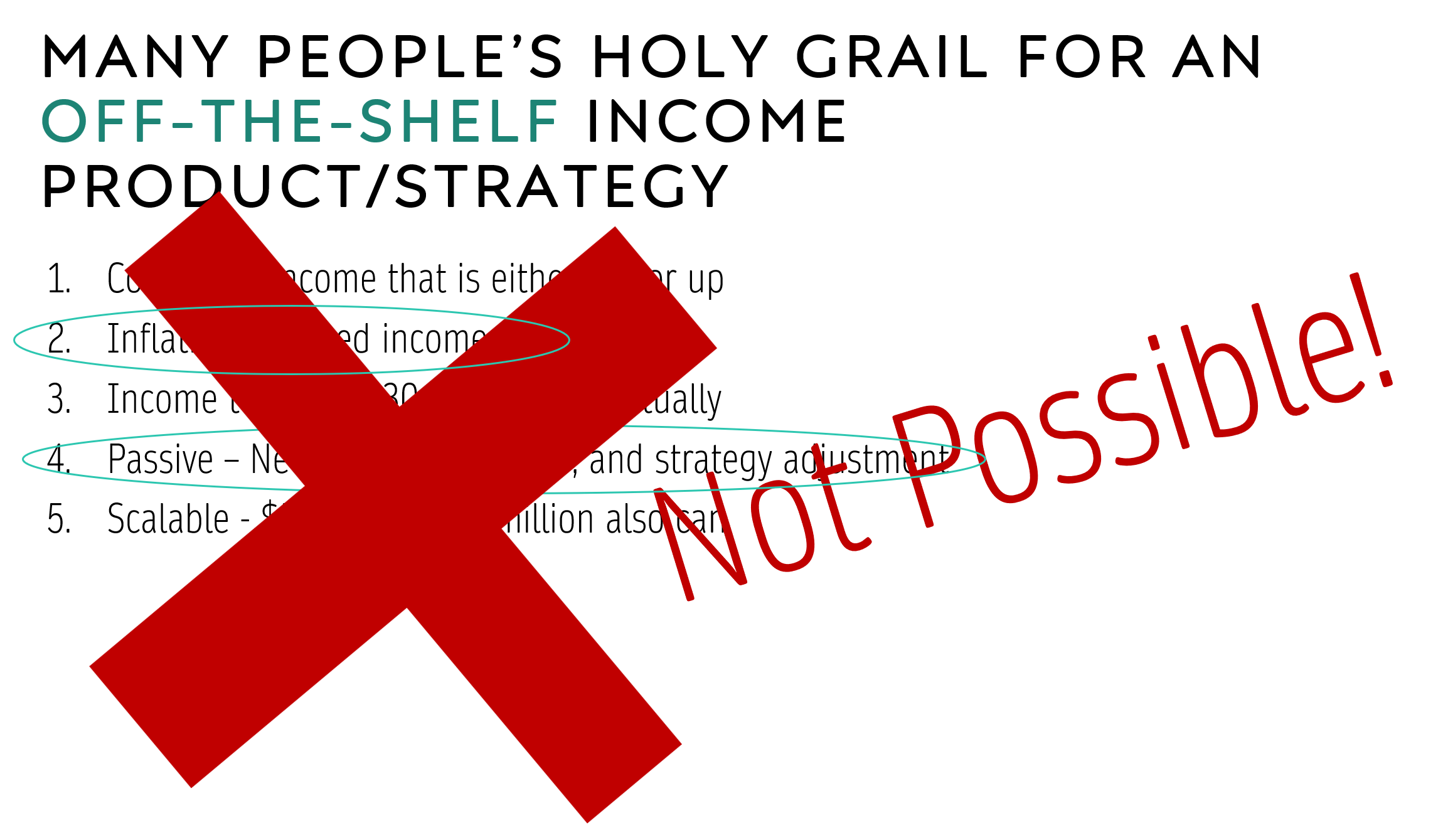

There are no holy grail off-the-shelf income products that will satisfy what you want.

Investment ideas should be seen as investments with clear compounded returns that come from their asset allocation and their manager’s skill (usually not much).

This doesn’t mean the products are shit.

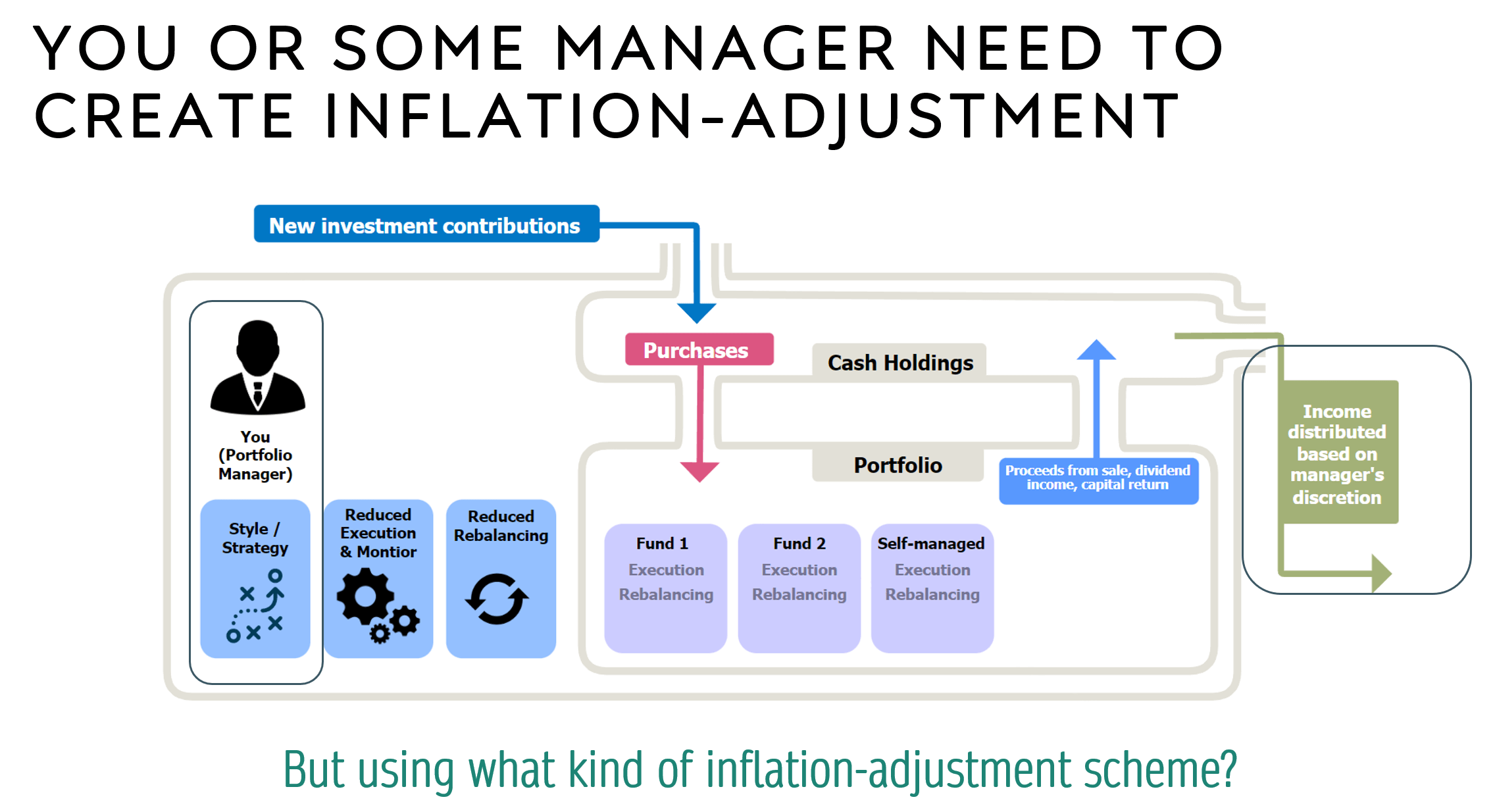

If all the products and strategies have flaws, if we think of them from the income perspective, we (as the portfolio manager) needs to do something about it.

Usually. we need an income strategy.

But many don’t really have those.

Having said that, I think is healthy to evaluate more products with an open mind.

When you evaluate more products, but bearing in mind what I said that there is no holy grail income product out there, you start seeing their uniqueness easier.

You can use a fix set of wealth planning characteristics and an investment characteristic to review these products to see if they are closer to your needs:

- income consistency

- inflation-adjustment

- how long will the income last

- effort needed

- scalability

- are there empirical evidence the income strategy gives you what you want?

- investment total returns –> asset allocation

In this podcast video that I did, I explain all of these, with some examples why most off-the-shelf products tend to disappoint your expectations:

Let me know if you have further questions.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- The Cheapest Way to Extend Your Laptop to TWODisplay that I Can Find. - April 29, 2024

- My Quick Thoughts on the Net Cash, 4% Yielding Boustead. - April 28, 2024

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

Sinkie

Monday 28th of August 2023

Lol 20 years after MAS started changing the financial sales/advisory industry to move away from product-focus to client needs-focus & we're still the same as in 1970s & 1980s.

Fundamental problem for many sinkies is that they want to still be treated like school children, with 10-yr series model answers, no fail/sure pass, 1-time straight As in A-levels or 1st class honours degree and future is set mentality. Salesmen, banks & insurance companies are more than happy to treat sinkies as school kids.

Figuring out future spending needs & budgets is a basic retirement foundation.

As example, a basic need like healthcare can estimate based on the current elderly premiums for various classes of medical insurance, together with healthcare inflation from Singstat. Singstat also provides 5-yearly updates on various household spending on different categories like food, utilities, leisure, medical etc. For specific healthcare treatments/procedures, MOH also has their "hospital bills & fees benchmark".

Is whether people are motivated to help themselves or not.

FC

Monday 28th of August 2023

Kyith, just wondering if you have the version in written blog post format? old unker here (and maybe some others) , prefer to read while drinking kopi-o-kosong.

Sinkie

Monday 28th of August 2023

1. Click on the word "Youtube" at bottom-right corner of the video to open the video in Youtube website.

2. Click on the 3 dots at bottom-right corner of video & select "Show transcript".

3. Enjoy your kopi-o-kosong (the transcript is auto-generated by youtube so some errors here & there).