The biggest debate recently happens to be between those who think they know a lot in the area of finance and those who wishes to market the Astrea IV Private Equity Bonds, in the hopes that it will sell well.

If you wish to read more about my thoughts about the Astrea IV PE Bond Class A-1, which was made available to retail investors, you can read my article here.

In one corner, you have those that are pro opposition or finance trained people saying this is a bad idea, primarily because this will be made available to the mom and pop investors.

On the other corner, you have the standard mouth piece of the government, be it the news paper agency and those platforms that were paid to talk and market this bond. (Disclosure: I wasn’t paid to talk about the bond in the link up there)

So you can consider this Saturday article a lounge article of some of my thoughts, the side show involving this bond issuance.

Shifting the Wealth Building Mindset Away from the Property Based Mindset

In recent months there were so much discussion on the reality of a limited land lease HDB flat.

Almost every week there was some discussion either during Parliament discussion or a BIG READ from Today.

There was some revelation that took me by surprise. The most surprising was that there are people with 50-60 year old land lease flats that are struggling to get a good valuation.

Current property markets looked to have recovered a little, sentiments are also better, but in one of the big read by Today or Channel News Asia, the price proposed by buyer is much less than 4 years ago.

In some of my past articles, I have laid out how over time the government, media and ourselves create a facade that HDB will appreciate or retain value well.

Thus, a big problem faced in Singapore is that for the majority, other than properties, most people do not know how to build wealth in other ways.

The government seem to recognized this.

What they are doing now is to manage the expectation that HDB might not enjoy the same privileges as the private non-landed properties.

However, the problem becomes: If we cannot retain or grow our wealth in our most concentrated and expensive asset, how else do we build wealth?

Singapore can be seen as a wealth management hub, but for the citizens who tends to be less sophisticated, versus the higher net worth people, other than property, most things are:

- speculative

- volatile

- hard to deploy a large sum of money confidently

By focusing the narrative that the safe way to build wealth is through HDB and private property, the incumbent have shifted the narrative away from finding out other ways to build wealth.

As a society, we have not matured in that aspect.

We tend to not look for solutions ourselves because majority are very dependent on what the government says. The government drives a lot of the narrative in a lot of aspects of our lives.

Given the choice, they would wish us not invest our CPF OA and SA in CPF Investment Scheme. It would be better to keep money in their hands. Hence a large part of the narrative was to top up our CPF SA to upgrade a return from 2.5% to 4.0%.

For most that do not save, CPF is our largest capital and if you present that all investment options pale in comparison to CPF SA, people give up looking for anything else that is more risky.

At some point, you have to sell the idea that we have to look for other ways to save for our retirement, that has less to do with property.

If there is a time to do it, it is now.

While Singapore has institutions like CPF for retirement, “we think we need to supplement it and companies can participate in this“, she said.

“One of the things we decided to do is to try and make use of our skills and strengths to create new products for individuals to invest for their retirement,” said Ms Ho who was replying to a question from the audience following her speech

“As you know these funds are open and accessible to many of you but not necessarily to the broad masses.”

“But by creating a product which is diversified and therefore provides a better risk adjusted return for the individual, we can bring a new category of product to the market for the retail investor,” said Ms Ho.

“So quite apart from things like housing this is another way that we as an institution, …try to bring our skills and knowledge to create products in the future for those who want to invest for their retirement,” said Ms Ho.

What Ho Ching said, gives us clues that providing options for wealth accumulation is on the government’s agenda.

Why Unit Trust and Index Funds Will be dead on Arrival

The obvious solution to this is to rely on the existing fund management products that have exist for the past few years.

Unit trust while provide variety and something people are familiar with, tends to have higher expense ratios, survivor-ship bias and selection problem.

The government could just study some white paper and realize that a lot of people don’t advocate for the average folks to build wealth this way.

The sensible solution is to encourage an index fund house such as Vanguard or Dimension Fund Advisers to come in. Else encourage low cost exchange traded funds as a way to build wealth.

However, it is likely only the more savvy and sophisticated wealth builders would devote a large amount of their net worth to these low cost fund solutions.

One of the main reason is that the typical average person cannot take volatility in their capital.

There is a lack of understanding how funds really work, how to invest in them, as well as how we should manage the behavioral part of wealth building.

Some of the most common questions that I get about the Astrea IV bond is whether its guaranteed, whether there are any risks.

These are valid questions. But they also show how risk adverse we tend to be.

Most of us would suffer from availability bias in that we remember how some relatives did really badly with some funds, or get scammed by some unscrupulous agents that they lost a large part of their net worth.

While index funds, quantitative exchange traded funds, index exchange traded funds are the right things we should develop and move towards, most would not be receptive over this due to them being more volatile and the future being unknown.

Unlike funds, property is predictable. Prices will always go up because economy tend to have a positive bias over time.

Why Bonds Make Sense

Bonds make a lot of sense because, it is easy to sell the story that these debt instruments are backed by good companies, have a fixed coupon and guaranteed if held to maturity.

There is very little uncertainty, unless the bond defaults.

The problem with bonds is that, the typical denomination of $250,000 minimum puts a single bond out of reach for the average person trying to build wealth.

Thus, if you reduce the denomination, a wealth builder can build a diversified portfolio of bonds that they enjoy predictable returns.

In order to enable citizens to be accustom to this option of building wealth, they probably need to seed this idea.

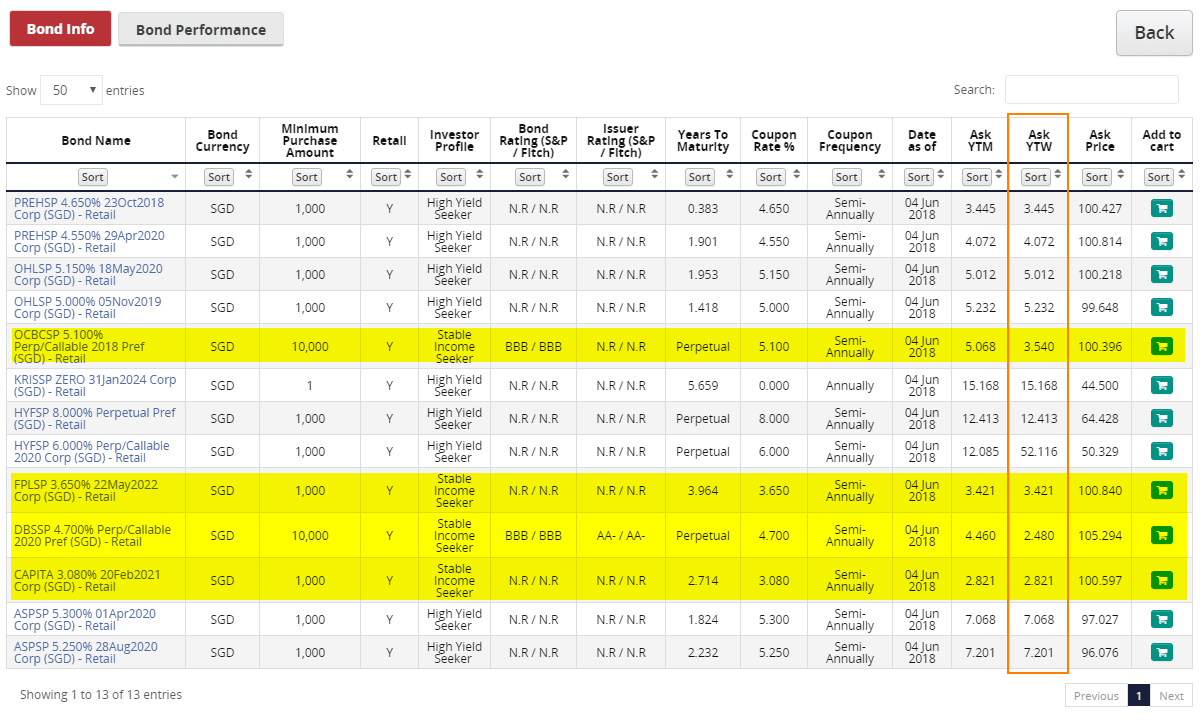

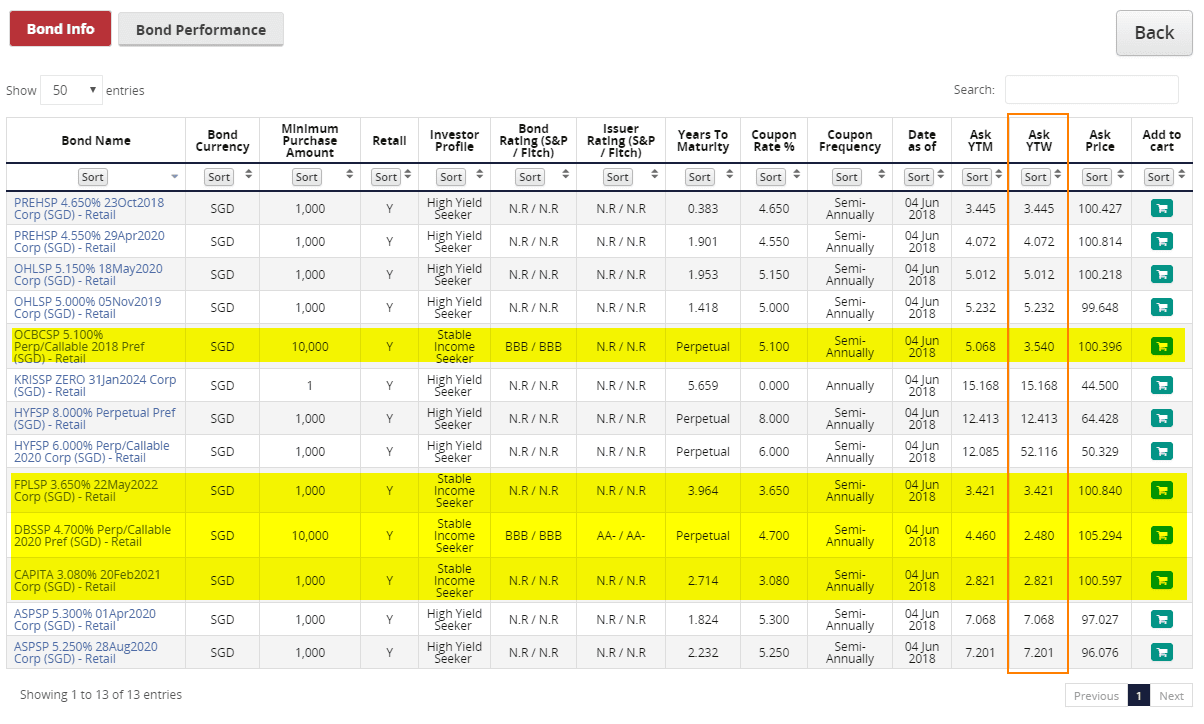

Now this is not the first time list companies were encouraged to do this. If you look at the table above Capitaland a Temasek Linked company, did issue retail bonds of small denomination.

However, the frequency that companies of the standing of Capitaland put out retail bond issue is few and far between.

I am not sure here, but I think the process of raising debt through retail means versus institutional is much tedious (and might be more costly). So unless they have an incentive to do it, most likely they won’t.

They will raise more from institutional means with less effort.

Astrea IV Class A-1, while technically not your normal bonds have the advantage:

- diversified

- predictable returns

- low volatility

- a known brand name

Thus, this is the best instrument to test the market if the general people likes to build wealth this way.

Some may ask the question why not issue debt instrument directly from Temasek? Why come up with something that is related to private equity?

My sensing is that if they issue a bond directly, with their credit rating, the yield on the bond would be low.

Probably as close to the Singapore Government Bond rate.

If that is the case, why not just buy government bonds or Singapore Savings Bonds?

Singaporean’s tend to treat bonds like fixed deposits.

They can sense whether somethings are attractive or not.

If you look at the subscription of the Singapore Savings Bonds, it is highly reflective of this.

Initially, I thought that not many average folks know about the Singapore Savings Bonds.

But in recent months, the short term 1 year bond rates shot up to above 1.4%.

Then we start seeing the savings bonds to be oversubscribed.

Now people are complaining they applied for more but get filled with less!

So it seems people know about this Singapore Savings Bond, but they did not invest because they are waiting for the yields to be attractive.

If you offer something straight, with the low yield, people would rather put their money in NTUC, FWD, Great Eastern 3-6 year endowment plans!

Thus designing something that the average folks would bite is not so easy.

Why not get a government affiliated, Temasek linked entity to issue bonds?

These bonds could possibly be lower in grade, thus they require a higher yield to compensate potential investors to put their money into it.

I won’t be surprise if there is something top down driven to ask them to issue a retail tranche.

I think for some they would bite those bonds or perpetual if its issued from say Capitaland Commercial, Mapletree Commercial Trust.

People were interested in LTA Bonds, and HDB Bonds in the past.

So it is not out of the question, but it takes time and someone needs to re-ignite the engine.

The Numerous Safeguards Put in Place for Astrea IV Class A-1

There is that debate about how exposed we are to low probability 100% losses of the Astrea IV Class A-1 bonds.

The risk is always there but in general I see a lot of signs that this might turn out OK.

1. Underlying Assets Should be Cash Flow Generating in Nature. This might not be confirmed but when I based my experience from what I know, and what my peers tell me, the firms that are subjected to buy outs tend to exhibit some characteristics that we like. These can be businesses that are predominately cash flow generating that have some problems or inefficiencies. The private equity buy them out with leverage, then sought to improve the margins or expand their distribution channels through their contact. With that in mind, if you have 36 funds and 500 plus companies mostly of these nature, things should be alright.

2. Private Equity funds held by Astrea IV are also held by other pension funds. If I can get performance data from CALPERS and public pensions in Washington, it means that these are not the obscure funds that is bought only exclusive by Temasek linked firms or firms in this region. A lot of the funds are widely known. If one of these funds would suffer, which is highly probable, a lot of the pension investors with private equity portfolio are likely to suffer as well.

3. Various Safety Measures and Assurance Provided to the Class A-1 Bond. Azalea went out of their way to ensure that the Class A-1 Bond looks “Safe”. Only the A-1 Bond is rated A(sf) by both Fitch and S&P. The other tranches was only rated by Fitch.

There is the large equity ownership from the sponsor.

There is a reserve account to ensure that cash distribution after paying debt interest is kept to build towards calling back the bonds on the 5th year. If the NAV of the underlying funds fall, the reserves are also used to deleverage.

Private Equity might not make timely distributions, thus credit facility were also arranged in case there is a need to manage liquidity.

This PE is bond is meant for retail take up, and if it doesn’t work out, there are a lot of reputation risk on the line for Temasek, even though based on obligations they are not directly liable.

Failure would be a rather black mark, after all these talk about their ability to use their expertise to push something sound and good for people to accumulate wealth and de-accumulate wealth with.

Refrain from Having the Fear of Missing Out

If you are unsure if this will eventually suffer from the same fate as those higher risk, unrated, poorer quality bonds, do not have that fear of missing out.

If this conjecture is correct, we will have some other bonds that come out.

If interest rate are still rising, the yield might even be higher.

Take some time to understand about bonds, how do they work, how to create a portfolio with them, and what are their weakness.

Don’t rush in and buy something you do not know well.

If you are uncomfortable investing in something like this, find something comfortable to invest in. If you are uncomfortable with everything, then its difficult.

You can only build conviction from within yourself.

To get started with dividend investing, start by bookmarking my Dividend Stock Tracker which shows the prevailing yields of blue chip dividend stocks, utilities, REITs updated nightly.

Make use of the free Stock Portfolio Tracker to track your dividend stock by transactions to show your total returns.

For my best articles on investing, growing money check out the resources section.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Sinkie

Sunday 10th of June 2018

I would say the main risk for Astrea iv is if we have a global recession in the near term and we need to liquidate for whatever reason. Coz likely market price may be below par during bad recession as this is backed more by equity rather than balance sheet net tangible assets.

Operational performance & earnings cashflows from the 500+ investee companies will be important.

So probably not a good vehicle for warchest if idea is to utilise during bear market to buy stocks / property.

That being said, if have 5-7 yrs timeframe, most likely will get paid back in full by then due to the capital structure & safeguards.

As usual, consider your position sizing & asset allocation lah. Although it's a cliche, there's a reason why 5% for a single counter especially if it's something new.

Kyith

Sunday 10th of June 2018

Hi Sinkie fully agree

Sgdividends

Saturday 9th of June 2018

Well I think this bond might be well received but even more well received if not for the hyflux fiasco..I think the hyflux fiasco could be a damperner if what you say about the government narrative is.

Kyith

Sunday 10th of June 2018

They cannot control something like that. for us, we have to see if more of these gets to the market. the good thing is that if we dont subscribe or dont get it, might not lose out so much.