Since I came out of university, I have been mainly accumulating wealth through active stock investing.

The topic of how concentrated should your stock portfolio be, or how diversified is a question that have been asked a lot. By both those who wish to learn and those who are experienced.

When we are experienced, we want to understand how others do it, versus how we ourselves do it.

So here are my personal rules.

- I am at the tail end of the accumulation stage, which means there will be limited capital being injected

- I am to be diversified holding at least 10 to 15 individual assets/stocks

- There can be asymmetrical positions, where some are larger than others, this will depend on conviction

- My Psychological Fail-Safe Point is about 10-13% of my net worth. I don’t wish to see more than $100,000 loss due to a single impairment that happens suddenly and I have no control over them

This article tries to explain some of my thoughts on the subject of diversification and concentration.

The above may work for me. But you are likely different, and you need to know the thought process behind this.

So this article will go through:

- The Role of Diversification

- It Depends on Your Investment Strategy

- It Depends on the Level of Effort You can Afford to Put In

- It Depends on How Far You Are from Your Financial Goal

- It Depends on Your Conviction In Individual Stock/Assets

- Concentration is Entrepreneurship

- You can Hold an Asymmetrical Sized Portfolio Provided….

- You need to Figure Out Your Psychological Concentration Fail-Safe Point

Let’s get into it.

1. The Role of Diversification

Firstly, why do we diversify?

I have stolen the image above from my friends at Dr Wealth.

In theory, there are 2 kinds of risk:

- Systematic Risk. This is the risk that generally affects all stocks, regardless of geographical, industry. It explains why a bad stock still goes up in a bullish market and good stocks get punished even though they have good results, in a bear market

- Unsystematic Risk. This is the kind of risk that affects particular stock or particular industry. For example certain manager’s sudden scandal only affects that particular stock, not the others. A downturn in the oil & gas industry only affects the oil and gas stocks or complementary industry.

As you increase the number of stocks in your portfolio, you reduce the #2 Unsystematic Risk. However, you cannot eliminate the Systematic Risk.

Thus if you invest in an exchange traded fund (ETF) which mirrors the FTSE All World Index, you are essentially investing in an equity allocation that almost mirrors the world, by market capitalization. If a single stock falters, the allocation is small such that it does not impair a large amount of your capital.

So How Much is Diversification Enough to Diversify Away these Non-Systematic Risk?

This is the subjective part. You can read this article from the balance that gives you the history:

- Evans and Archer Calculated 10 Stocks Were Enough Diversification In 1968

- Meir Statman Believed Evans and Archer Were Wrong, Arguing in 1987 That It Took 30-40 Stocks To Have Enough Diversification

- Campbell, Lettau, Malkiel, and Xu Published a Paper in 2001 Insisting Increased Stock Volatility Required an Update to Evan and Archer Because 50 Stocks Were Now Required

- Domian, Louton, and Racine Changed the Definition of Risk to a Better Real-World Metric and Concluded, in April of 2006, That Even 100 Stocks Weren’t Enough

- Why Benjamin Graham believes 15 to 30 stocks is enough, with some caveats

You can see it is a hell hole to into. If its 50-100 stocks, it makes active stock investing difficult.

“I decided to run a concentrated portfolio. As Joel Greenblatt pointed out, holding eight stocks eliminates 81% of the risk in owning just one stock, and holding 32 stocks eliminates 96% of the risk. This insight struck me as incredibly important. It is hard to find long ideas that are ones or twos or shorts that are nines or tens, so when we find them, we decided that Greenlight would have a concentrated portfolio with up to 20% of capital in a single long idea (it had better be a one!) and generally would have 30-60% of our five largest longs.” – David Einhorn

I sit in the camp that if you hold more than 20-25, you are going to have serious problem if you are a retail investor. If that is not enough diversification, its time to abandon the job of an active investor.

2. It Depends on Your Investment Strategy

Certain investment strategy requires you to be effectively distributed in order for the whole strategy to work.

If you do not abide to this aspect of that investment strategy, it may impact your results. However, the likely consequences is that it affects the magnitude of your upside or downside.

The typical strategies for active stock investing taught to you by investing course providers, won’t ask you to have more than 30 stocks.

The main reason is that they are afraid that you will blow up in an overly concentrated portfolio and that you will go and find them, or leave a bad review.

There are some strategies that requires you to be diversified enough, else you will have a problem.

A lot of the times, these strategies are very quantitative strategies.

These are folks that does pure screening based on the data with very little qualitative inputs.

The folks at Dr Wealth used to run their CNAV, teaching folks a very Benjamin Graham net net style of investing.

Former Business Times Correspondent Teh Hooi Ling, who now runs inclusif value fund, used to show us the kind of outperformance we can achieve by just focusing on a portfolio of low price to book, low price to earnings, high dividend strategies.

Diversification is an essential part here. Usually, a lot of really low valuation stocks or assets, screened this way, have a incidence of blowing up and closing shop.

As an overall portfolio, it should achieve the outperformance on the benchmark market index talked about. However, if you select a few, say 6 from a basket of these screen stocks, there run a probability 2 out of 6 ends up to be one of those extreme duds.

Suppose you have $100,000 and you are diversified across 6 stocks screened the same way, and 2 of them turns out to be utterly wrong due to their qualitative fundamentals, where they fall 50%, your overall portfolio will be down $16,666. Your performance will be determined by how well the other 4 stocks outperformed based on this strategy.

In another example, I learn that Motley Fool in the USA teaches a certain form of growth investing. It focus on companies with the potential to be multi-baggers, or stocks that go 200% to 4000%.

You learn that by studying the qualitative aspects of fundamental analysis, such as the business model, outstanding managers, you can find stocks like this.

However, if you only listen to half the strategy, it might kill your capital.

A lot of potential multi-bagger companies are in the infant stage, or the entrepreneurial stage. They might fulfill their promise, or they might not.

Thus, it means that you will also get a lot of them who fall on the way side, have atrocious stock price falls. Even when they have atrocious stock price falls, it might not mean they are duds.

Amazon, Netflix, the FANG darlings we see nowadays, had -40% to -75% draw downs! Look at the gains you would have if you stick with them.

However, there are some potential darlings who fall -60% and they never fulfill that promise.

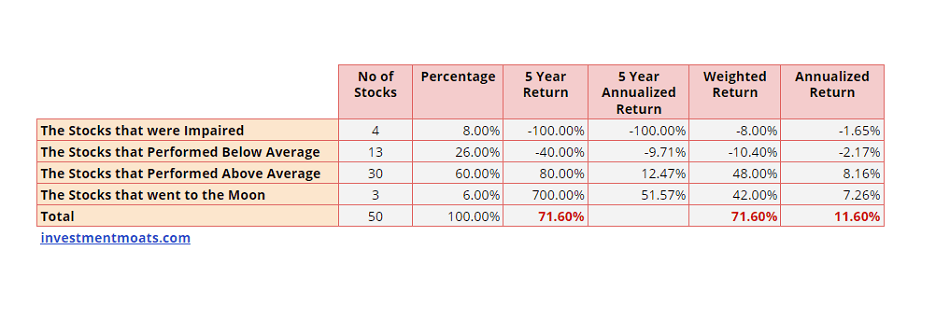

Thus the right size for such a strategy might be that you are diversified across more than 50 stocks. So on a $100,000 portfolio, each position is almost $2,000.

The strategy curates a basket of 50 stocks with the potential to be really good, and you are hoping that on the average a small number of them goes 500%-4000%, a number of them goes -80% to -100%, the average of them delivers the average -10% to 10% per year result.

In the illustration above, 4 of the 50 stocks in 5 years time was irrecoverable or we suffer some bad losses, 13 of them lost 40% in 5 years or 9.7% annualized. But on the average 30 or 60% of the stocks did very well, and 3 of them went to the moon.

Overall, the returns were an annualized 11.60%/yr over the 5 years or a total of 71.60% in total.

On the opposite end of the spectrum, you have folks like Joel Greenblatt, who wrote the delightful book You can be a stock market genius, and manages Gotham Capital, where he started with $7 mil in 1985 and have a compounded 40% per year return from 1985 to 2006.

At some point during the great financial crisis he has one pick that forms greater than 70% of his portfolio. The reason for that is that through his quantitative and qualitative analysis based on value investing philosophies, he has a strong probability that the particular stock is trading below the cash position of the company and he was able to validate to an extend the cash is there, and that in some worst case scenario, even if the business goes belly up, equity stock investors would do pretty OK and not lose much of their capital.

To do that, you have to be competent enough, and know the level of deep work that you need to do for that strategy.

Most qualitative value investing strategies require a certain level of rigor in prospecting.

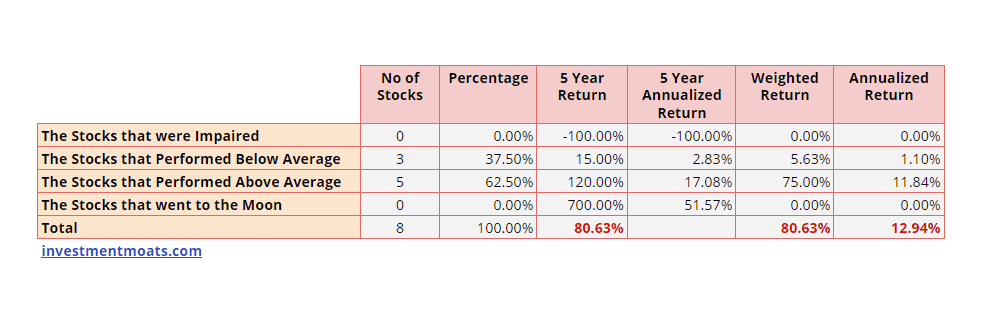

The table above shows a very highly concentrated portfolio of only 8 stocks. The investment strategy follows a particular theme and aims to earn greater than 15% per annum.

Since it is highly, focused, and very focus on identifying adequate margin of safety, the investor should not be expecting any impairment, nor stocks that go to the moon.

The question is how many stocks performed up to expectations.

If 3 out of the 8 stocks do not perform accordingly, and 5 do, which earns an average of 17%/yr over the 5 years, the overall annualized returns is 12.9%/yr or 80% over the 5 years.

It is pretty similar to the example before in terms of returns, but the implementation is very different.

Most of the gods in this area would tell you not to diversify too much.

Here are some of them:

“Two things should be remembered, after purchasing six or eight stocks in different industries, the benefit of adding even more stocks to your portfolio in an effort to decrease risk is small, and overall market risk will not be eliminated merely by adding more stocks to your portfolio” – Joel Greenblatt

“We strongly believe that the supply of great businesses is severely limited and to engage in broad diversification is dilutive to the implicit purpose of earning above-average longer-term returns” – Frank Martin

“There is one thing I can assure you. If good performance of the fund is even a minor objective, any portfolio encompassing one hundred stocks is not being operated logically. The addition of the one hundredth stock simply can’t reduce the potential variance in portfolio performance sufficiently to compensate for the negative effect its inclusion has on overall portfolio expectations” – Warren Buffett, Partnership letter 1965

“A key component of our investment strategy is sufficient but not excessive diversification. Rather than own a little bit of everything, we have always tended to place our eggs in a few dozen baskets and watch them closely. These bargain-priced opportunities are selected one at a time, bottom up, which provides a margin of safety in case of error, bad luck or disappointing business results. However, we are always conscious of whether these different investments involve essentially the same bet. If each of our holdings turned out to involve similar bets [inflation hedges, interest rate sensitive, single market or asset type etc], we would be exposed to dramatic and sudden reversals in our entire portfolio were investor perceptions of the macro environment to change. Since we are not able to predict the future, we cannot risk such concentrations” – Seth Klarman

So the moral of the story is: Don’t just listen to part of the strategy. Position sizing in the strategy is also an important area to figure out about the strategy, and not understanding, or figuring it out can greatly affect the performance.

3. It Depends on the Level of Effort You can Afford to Put In

A lot of the times, investors become too overly diversified because they see that if a fund can have 50 different stocks, they could also do the same.

The difference is that these folks are full time fund managers.

Their job is to manage and ensure the performance of this portfolio.

You are not.

You are an investor with a day job, or a day business to run.

You could be starting to learn this on the side. You could have a very hectic day job that requires you to spend enough mental effort such that when you reach home, you are mentally drained from doing any more brain work.

When you run a concentrated portfolio of 6 to 8 stocks, you have to ensure that these 6 to 8 stocks do not blow up, and that their growth story is still intact. (As a gauge, other than work, family, most of us spend our spare time thinking about these stock position. Its basically a job)

You need to check up on their business, environment and trajectory consistently. For someone who is rather competent, 6 to 8 might be enough work to monitor.

For some, 6 to 8 might be too much.

This is because for the prospecting of each stock, they really spend a lot of effort to ensure that they will not lose a huge amount of their capital on it.

These are usually those who uses strategies that require them to be very thorough in their prospecting.

Now, if you do this same strategy, but with 20 to 30 stocks, you are going to run into problems because you cannot give enough attention to each of these stocks.

When you cannot monitor, some of these stocks would slowly and subtly rot. And then before you know it, you will ask yourself how did that happen!

Sooner or later, you will end up with a portfolio of a mix bag of winners, losers and average stocks. And you will ask yourself, what am I going to do with a portfolio like this?

A lot of active stock investing requires pruning.

This means that you review consistently the prospects, weed out the poor performing ones, or those that have run its course, and add on to those that its prospects became clearer to you, and you have higher conviction. Over time, you have a “nicer garden”.

This requires effort.

And not just this. You need to prospect and find new potential businesses, so that is another set of qualitative and quantitative work to do.

Might not be very fun for a lot of people!

On the other end of the spectrum, if the strategy entails less of individual stock prospecting, then it might require less effort.

The more diversified, the less impact of a few particular blow ups.

You can see the appeal of a portfolio of index exchange traded funds.

This is definitely at the opposite side of the spectrum.

You practically own like thousands of stocks or bonds.

Your returns are diluted, but your non-systematic risks are very much reduced as well

4. It Depends on How Far You Are from Your Financial Goal

The strategy that you apply to your active portfolio, will have to take respect of the goal of your portfolio.

There are some goals generally for folks:

- Wealth accumulation. Lean towards growth

- Wealth preservation. Lean towards ensuring the net worth is there

- Wealth de-accumulation. Lean towards spending down your money

The level of concentration, or diversification will affect the portfolio investing strategy you take, which affects the level of concentration or diversification.

This is what they say, and there is some truth to that. When you are diversified, you spread out the risk of capital impairment in active stock investing from a few stocks.

You will need more picks to form your portfolio, but you might be able to reduce the risk of something really go wrong.

However, when you are in the wealth accumulation stage, you spend effort on your portfolio, watch over it, and work on the portfolio to do well.

Concentration + good processes + high competency might make sense.

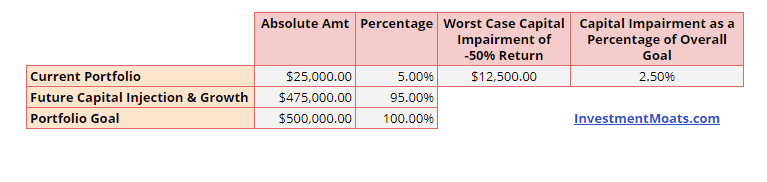

For example, suppose you have worked 3 years and have a portfolio of $25,000.

You are not going to be happy with that amount, and likely are hoping to get to $500,000 in X years, through stock investing and injecting capital.

So you have $475,000 more to go.

Now suppose, you are still learning and you are concentrated in 2 stocks.

Now one of those stocks got suspended due to fraud and likely, you are not going to get anything back. That will be a -50% return on that portfolio at least.

This looks catastrophic, until you think about it and $12,500 is just maybe 70-100% of your 1 year capital injection. You are going to work for 15 to 20 more years, so this sum is not going to be really significant. It is probably 2.5% of your overall goal of $500,000.

The more important thing is to learn through that blow up.

It might make sense for those who are de-accumulating or preserving their wealth to switch to a more passive strategy of holding a portfolio of exchange traded funds.

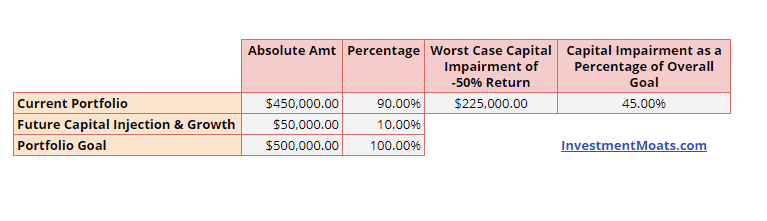

Since I am leaning closer to the wealth de-accumulation stage rather than the wealth accumulation stage, I tend to be more diversified rather than concentrated as well.

This is a situation closer to what I am in. Suppose I become concentrated in 2 stocks, but my capital is $450,000 instead of $25,000.

The same blow up in one of the stocks will set me back $225,000. This amount is 45% of my overall goal.

Suffice to say, this is a big psychological blow and I will have to recollect myself, and most likely need to extend my working life.

Can you be concentrated during wealth de-accumulation stage?

Yes you can.

This is provided that you are cognitively strong, enjoy this job of active stock investing, retired from your day job to focus on living life and active stock investing.

If you are able to grow your portfolio even more, give your wealth de-accumulation plan more certainty, isn’t that even better?

However, it is better to have a level of diversification, in that scenario as a fail-safe, just in case things do not go your way, and you do not suffer from large capital impairment.

Each of our circumstances are different.

5. It Depends on Your Competency in that Investment Strategy

I used to have the following picture in my depiction of what are wealth machines:

You only have wealth machines if you develop enough competency to build wealth in a certain way sustain-ably.

Each of us starts off from the novice level and some of us do progress to be really good at it. But a lot of us are “halved past six”.

For active stock investing, the required competency to do well is subjectively near the tail end of being intermediate.

However, for most people, they would think that they are equipped but in actual fact they are still pretty far off.

How does this relate to concentration or diversification?

Concentrated portfolios, with large capital, are suited for those who have adequate competency to build wealth with sustained success.

If you have a large capital, yet close to the end of your wealth goal, but assessed to have a short fall of the required competency, it is better not to be too concentrated.

If you are building up your net worth, yet have a short fall of the required competency, you can learn to be concentrated, even if you are not there yet.

Lastly, if you are building up your net worth, feels that you do not wish to put in the effort to learn this competency, please be diversified enough.

The very problem with what is written in the media: That all of us can become the Buffetts and Drunkenmiller overnight, by doing this minimum entry level of work to achieve the level of competency to be at the same level as them.

And this might be killing a few people.

6. It Depends on Your Conviction In Individual Stock/Assets

Some folks can be very concentrated because they really believe in their deductive work on the stock. So much so that they overweight their position on it.

Some folks, while having done the work, still have reservations about certain stock they initiate the position in. They tend to not have a high allocation to it.

Conviction is your belief in a stock. This can be real or falsely attributed.

However, it does affect whether you concentrate into a few stocks, or be very diversified.

“Diversification is always and everywhere a confession of ignorance” – Andy Redleaf

“Diversification covers up ignorance.” – Bill Ackman

“Diversification is a protection against ignorance. It makes very little sense for those who know what they’re doing.” – Warren Buffett

To a certain extend, these guys are right. You don’t hold a larger position because you are unsure.

If you are sure something is really a good thing, you would be pilling in to it.

Even this, it is better to have a fail-safe level of diversification, because even the most sure thing, there is a chance that it will blow up.

I wrote about why conviction is important in greater detail in this extensive article here.

7. Concentration is Entrepreneurship

“Charlie Munger considers that a portfolio of four stocks is a well diversified portfolio. He says, you don’t even need a 5th stock. He goes on to say that if you lived in a small town, and if you owned the best apartment building in town, if you owned the highest quality office building in town, if you owned the McDonalds franchise in town, if you owned the Ford dealership. if you owned this collection of assets, even though they’re all geographically concentrated, his perspective is that you will do very well. You will not need to do much else beyond that to have an interesting investing career.” – Mohnish Pabrai

I have a few friends that holds concentrated portfolio.

They tend to manage their own money to grow. Seldom you see this in funds.

I think the issue is that there are much career risk if something doesn’t go the way you want. You cannot manage money anymore, due to the small community.

However, if you are managing your own money you have certain advantage.

You are not shackled.

Some I know hold 70% of the portfolio in one stock or asset. A lot of them hold 3-6 positions only.

The thing you need to understand is that doing it this way is really like running a business.

It is not hands off.

They practically work, family and the rest of their time breath these 3-6 positions.

Maybe include 2 to 3 more for those they are looking to buy into.

In business, you cannot enjoy the “passive income” before getting the business up.

And real business is damn tough.

A lot of business ended up closing down and losing large amounts of capital.

The returns are great, but the volatility, and success rate is also very wide.

Running a concentrated portfolio requires certain level of competency.

You need to figure out the investment strategy, the details of it to a high degree. Then you need to execute the process a few times so that you roughly know you can do it this way.

You are basically buying 3-4 businesses and watching over them like a hawk. And you do not have time for much other things.

Thus, its not always going to be your cup of tea.

But because their processes are good, they are good critical thinkers, they are damn hardworking, that concentration also see them earn those kind of 20-50% XIRR in a year, if not for the past 5 to 10 years.

This is not the 1% to 10% returns we are talking about.

This is the Buffett level returns.

It is doable.

But it is not simple and honestly if you ask them they don’t look at that return as a badge of honor but just trust the process.

Some of the very concentrated folks:

- Musicwhiz (stopped writing)

- Invest Moolah

- Chris Susanto

- Brian Halim

- Thumbtack Investor

- zzxbzzinvesting

8. You can Hold an Asymmetrical Sized Portfolio Provided….

You may ask, so if I wishes to be at least 20 stock diversified, are they all equal weighted?

It depends.

Based on conviction, competency, there would be stocks that you have higher conviction in. These can be larger in individual sizing.

There will be those stocks that you have less conviction in, the individual sizing an be less.

The thing to understand is that perhaps you have 2 strategies in one portfolio:

- One is a high conviction, well researched one. To be effective, you need to watch over them more, spend more time on them. These are like your main business.

- One is a high potential one which you are still seeing the story unfolding. These tend to be volatile, some might blow up upwards, some might blow up downwards. How fickle you are with selling them, adding on to them will depend on how the story unfolds.

#1 tends to be larger in individual sizing. Due to that, your capital might really be impaired, so the level of rigor, and how trigger happy you are, might be very different from #2, which might afford you to be less anxious over them.

The key thing to note is that which strategy it is.

In some cases, I could have 10 high conviction large sized position ones and 40 really small ones that I am trying to figure out.

9. You need to Figure Out Your Psychological Concentration Fail-Safe Point

There is a difference between percentage and absolute amount of money.

We usually measure in percentage but we lived with, or use the absolute amount.

Our net worth provides us a real utility, in that we can spend down, or used to purchase something we like, or we need.

It also take us some time to accumulate your portfolio by injecting capital.

Because of all this, each of us have a different psychological attachment to the money.

For some, if they lose 50% of $500,000 it’s not too big of an issue because their annual capital injection is $80,000/yr and they can see themselves doing this for the next 10 years.

There are also folks who can see a 50% capital impairment on $500,000 because they have so high conviction in their own ability, and have seen that they can achieve sustainable 50-100% returns on their picks.

Then, there are also folks who cannot see a $40,000 absolute impairment of their money.

This is your psychological concentration fail-safe point.

If you are doing active stock investing, you should not invest more than this in a single position.

For some that are more experienced, or choose stocks that are more matured, they can estimate a worst case 50% capital impairment and can’t afford to lose more than $30,000, then their individual sizing could be $60,000.

No one can tell you what to do. We are here to put this in front of your to let you think about it (as oppose to you living in a dangerous blissful state)

My psychological concentration fail-safe point is that, if there is a sudden impairment of a single stock that catch me unaware, if it’s more than 10-13%, it will set me back quite a fair bit considering the stage of life I am in.

I will have to go back to work to earn that portion back, or I have to double down on investing in the hopes of making up for that impairment.

Thus the maximum that I would go to is $100,000 to $140,000 for each individual stock. $140,000 if I see that I have time to react and get out with losses but not more than 50% losses.

Lastly, on a related note, you might monkey see and monkey do by following some others portfolio allocation.

Do keep in mind that for some, their stock portfolio is just a small subset of their overall net worth. For some, If you include their future net worth, the portfolio is less important.

Their psychological concentration point is much higher, because in the worst case it will not affect their future quality of life.

However, if you copy them without understanding your situation is unique to others, you may run into problems next time.

Summary

I hope this is clear enough on the level of diversification that might work for you.

The focus here is on active stock investing, and you can see the appeal of having others to manage your fund for you if this is not your cup of tea.

If you are a trader, the strategy might be different, and some of what I mentioned might not be entirely applicable.

However, if your capital is dear to you, your individual position sizing might need to respect the same kind of psychological concentration fail-safe limit, the competency perspective, and financial goal perspective.

If you have any questions you can ask below.

I do consolidate all my more structured thoughts on active stock investing in my active investing section here.

There are still some tickets from Investors Exchange 2018. You can know more about the event and get the tickets here.

To get started with dividend investing, start by bookmarking my Dividend Stock Tracker which shows the prevailing yields of blue chip dividend stocks, utilities, REITs updated nightly.

Make use of the free Stock Portfolio Tracker to track your dividend stock by transactions to show your total returns.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

Sinkie

Monday 4th of June 2018

Hi Kyith,

Kudos for the insightful treatment as always!

Regarding the psychological fail-safe point, was wondering if 10%-13% might be too low for equities? Even a strong company can drop by 15%-20% within a multi-year bull. Unless you're intending to do some timing or trend following to get out / get in again?

From personal experience with trend following, even a -15% threshold may be too tight. I use a dumb 200 day SMA and sometimes this means being willing to accept a large percentage drop before I start to pare down or sell off. Especially if the stock or ETF has gone up aggressively within a relatively short time (that's where I'll take some off the table beforehand, but that's another topic).

Also in a bear market, there's good chance for many if not most stocks to drop over 30%. Do you envision selling all or most of your equity holdings? Or adopting a more balanced equity/bond/cash portfolio?

I think it's good to have some of these things codified & rules based. Especially if backed up by backtesting for both dot.com recession (long drawn scenario) and GFC (vicious but shorter).

Kyith

Tuesday 5th of June 2018

Hi Sinkie, I think you might have been mistaken. My 10-13% is the amount of allocation as a % of the portfolio i would allocate to a single asset/stock. This is perhaps to prevent a single catastrophe linked to one company.

Using a moving average could work well but even if a stock goes down 20-30% on a 13% position it is still manageable. of course my exposure could be greater than that if a bunch of stuff move down 10%, if I own a lot of one sector.

Hope this explains.

Divy123

Monday 4th of June 2018

Thanks for sharing Kyith. The article talks about the fail-safe limit for each position. How would you consider this with respect to the entire stock portfolio? Since there can be correlation between stocks even from nonidentical, but possibly correlated industries ( eg banking and O&G ). Do you have guidelines on the number of stocks you allow yourself to invest in for each industry ( and correlated industries?) How do you manage overall portfolio fail-safe limit?

Kyith

Monday 4th of June 2018

Hi Divy123, good question and something i felt i might forgot to address in the article. I would say i let one rule override it is that if each position have a positive expected return. This means that we need to analyze to see if the sector going forward will have a realistic positive growth or it has value.

given this, i am ok to be overweight on it. it is like if you hang out in an extremely nice neighbourhood, should we sometimes hang out in a dangerous neighbourhood just to diversify?

I think sometimes the best example is what if Kyith have 80% in REITs, which is one sector. Then perhaps Kyith needs to see if there are some secular danger in that one sector. To be honest, i most likely wont do something like this. Last year I was pretty heavy in the manufacturing sector, and it worked out but we can see in another situation it could get me into trouble.

I am more afraid of single company blow up. if the whole reit sector goes into a tailspin, i could probably get out and suffer losses and i got to live with that my analysis was wrong.

Alan

Monday 4th of June 2018

Great article Kyith .

Another downside to diversification is the transaction costs for retail investors. Imagine the accumulation and transaction numbers for a portfolio of 50 stocks.

Also , the effort for a concentrated portfolio is huge. I once got the report from the Avid Hedgehog (Gannon and Hoang). A single report ran over a 10k word count with very detailed analysis.

Kyith

Monday 4th of June 2018

Oh! you subscribe to that! Their analysis was super detailed as always. but i think they really go deep into it. i think the transaction cost will depend on portfolio size and we should just be aware not to pay too much but i feel it is less of an issue.