I don’t know if she meant it but Cathie Wood of Ark Innovation really played this ETF marketing game better than anyone we know.

Ark has created an omnichannel communication engine unlike any other we know. The media create residual stories from what they say afterwards.

Recently, she explain why she thinks a lot of these companies that their fund invest in is in “deep value” territory and that the fund will deliver 40% compounded growth a year for the next 5 years.

She has since then, corrected what she says a couple of times.

I dunno but the deep value in my dictionary is quite drastic.

Usually, if we take all the cash or those assets that can be sold in a very conservative manner and deduct all the liabilities and the net asset value is higher or near the current share price, I would use deep value.

But what would be considered deep value when it comes to these growth companies, with not very sturdy earnings to no official GAAP earnings, which trade at valuations much higher than book value?

One of the podcasts that I listen to was The Razor’s Edge which is a podcast hosted by an ex-Seeking Alpha employee and Akram who is an ex-propriety trader.

Akram single-handedly changed my perception of what a “trader” does. The deep-dive research work that he does on a single company is very deep and makes me question one more time whether I have an edge in this game or not.

I also learn through Akram that there is a price to pay for these companies if you would like to get a good outcome. So he is not the sort of “buy-at-whatever-cost-as-long-as-its-a-potentially-wonderful-company” guy.

Akram tried his hand on answering if these growth companies are in value territories.

A Backtest of Great Tech Investments

If we want to find winners, we should try and “model” long term trades on tech companies of the past.

Akram thinks it is better to narrow down the characteristics of the companies we look into:

- Make sure we pick companies that were growing rather steadily over a 10-year sample period. This should be available in enterprise software. Goal: avoid companies with pivots/turnarounds/distress situations that skew the data.

- Focus on established businesses that had some sort of scale as public companies. A good metric is to find companies with at least $1 billion in revenue. This avoids venture-like public companies that generally don’t have customers, profits, consensus.

Akram then did an exercise to profile some of the venture-like SaaS companies that turned into category killers in the past.

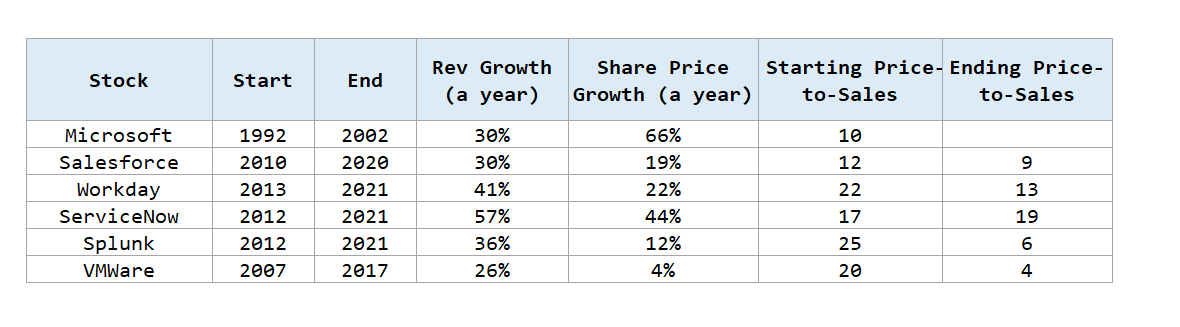

I have summarized in the table below:

We can see these are familiar names that have operated for between 7-10 years period and the subsequent share price annual compounded growth rate.

Microsoft was in an infancy stage and buying a company at 10 times PTS looks like a shrewd investment, even accounting for the Dot Com Bust. The rest are the OG of the tech space.

At one point, ServiceNow and Workday were the Zoom of today but because there weren’t so many SaaS then, they were the poster child that was subjected to a debate whether these no income, a venture like companies were worth it for you to pay 17 times to 22 times PTS.

The compounded revenue growth over 7-10 years was very high, but there were a couple of notable companies that could not keep up with their original growth rate. Splunk stepped down its growth rate in the last two years from a high of 45% while VMWare slowed down in the last 5 years from 40% to 10%.

Profiling these businesses in their early listed stage allows us to compare how much we pay for them initially on a price-to-sales basis versus the return that we get.

We can also see whether they could sustain a high growth rate or not.

It is interesting to see their ending price-to-sales at the end of the 7-10 year periods.

Notice that many did not trade as high of a price-to-sales as when they IPO or started.

This review will give us some idea of how vulnerable some of our thesis is regarding what kind of price-to-sales a company should trade at.

Businesses do slow down, even for wonderful companies.

The data also show that we would get reasonable return outcomes if we pay at 10 times sales for steady “wonderful” business. (This also means that there are a lot of companies that are excluded that are not so wonderful businesses)

But Akram wonders how much should we be willing to pay for the next-generation software tech business that will become wonderful.

What if we pay a much, much higher amount for these historically great tech investments?

Akram mentioned that we could pay a lot more for Microsoft in 1992 and the investments will be decent.

But what if we pay Snowflake valuation on Microsoft in 1992? If we pay 100 times the price to sales for Microsoft in 1992, this will make Microsoft 3 times the most valuable company with a market capitalization of $200 billion.

But if we look from a 20-year perspective (2012 end), your returns on Microsoft would be flat.

If we pay 45 times price-to-sales for Salesforce at end of 2010, our 19% a year compounded return will dwindle down to 4% a year.

Akram said ServiceNow is an example that will make valuation easier because investors would be able to better profile how it will scale over the next 10 years through the first year of operation.

But if you pay 100 times sales, your 44% a year return will go down to 12% a year.

This part is a way for Akram to tell us that sometimes we can pay more for a company and get a reasonable outcome but if we pay crazy valuation, it doesn’t make a good risk-vs-reward.

The Sweet Spot

As an experienced, detail-oriented market participant, Akram feels that when the old school software names transit from on-premise to the cloud, they made great business roughly 8 years ago.

They were not growing, and trading at 2 to 4 times enterprise value-to-sales.

Their returns have since 10x but likely partly due to the fact that they were cheap and there was a catalyst for change.

He reminded us that:

- Adobe was at negative growth.

- Nvidia was trading at 2 times sales with 4% growth in 2015 before it grew 40% for the next 3 years.

When the business undergoes such a big turnaround, the price multiple likely will overshoot and look overvalued on the short term, but if a not growing business starts growing at 20-30% a year, it is likely going to get re-rated (if it continues to grow!)

But how much in terms of price-to-sales should we draw the line for great companies that can become great investments?

Akram puts the magic number at 40 times.

Akram’s benchmark is that if we hold the S&P 500 for 10-years the annualized compounded return is 10%. If we pay more than 40 times sales, even the most profitable steady growth in tech history will not beat the market over a 10-year window.

And a key assumption is that during that period, there is no slowdown in the growth rate. If we take more companies growth like an ‘S’ curve and that these companies IPO when growth is ramping up, this assumption becomes weaker and weaker.

Akram has already given the answer.

The backtests were great tech-focus business, compounding at great rates, at different points of the past 30 years.

The range of price-to-sales is not more than 20-22 times.

If we are able to identify a great business (got to do the qualitative work) and pay that range, then we may have an investment that has a good outcome.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.