Shortly after the Singapore Budget 2024, CPF put out a short FAQ regarding some commonly asked questions and their responses. Out of all the responses, this response was quite intriguing to me:

Math is quite unique in that if we exercise our brain power a little more, we can become clearer in something. But the math might not come naturally to us. We might not know that we can easily calculate something.

I always wondered how much money in CPF Special Account (SA) we are discussing that CPF members can potentially shield so that they can have a High Yield Saving Account of 4% p.a.

CPF stated here that 99% of members aged 55 and above today would have an equivalent of less than 4 times their cohort CPF Basic Retirement Sum (BRS), or the equivalent of two times their CPF Full Retirement Sum (FRS) in their CPF SA at 55.

So with Shielding, members have roughly two four-percent per annum accounts instead of one currently. Naturally, most Singaporeans will feel unhappy.

I wanted to test whether that 99% math is accurate and remember that we have a CPF Projector which we use internally to estimate the account values in CPF at certain junctures.

I set the following parameters:

- A member can hit CPF FRS in their CPF SA at 20, 25, 30, 35, 40, 45, 50, 55-years-old.

- Upon hitting CPF FRS, their money will grow on its own, regardless of the higher annual revision of the CPF FRS limits.

- Then, this member can earn a high income that would have an equivalent annual CPF Contribution of $37,740 p.a. He or she will have additional money flowing into their CPF SA accounts.

- We want to see the estimated value in their CPF SA account whether it will be two-times of their cohort CPF FRS.

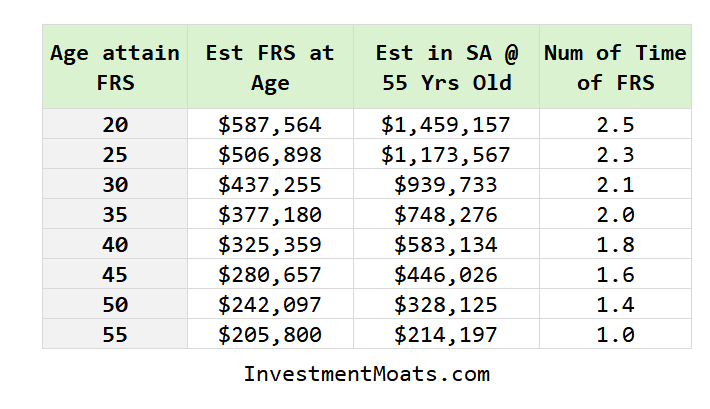

The results is in the table below:

I have listed the age the member attained CPF FRS, the estimated CPF FRS for that cohort and the estimated money they would have in their CPF SA.

We can see that the 4 x BRS, or 2 x FRS gauge is quite alright.

There are very motivated working adults between the working age of 25 to 35 who strives to attain the CPF FRS. The number of times of FRS is about 2 times.

If you attain CPF FRS earlier than 25-years-old AND earn a great salary, you can possibly have a much higher SA amount relative to the CPF FRS.

Either:

- Well, inform the young person who started a business and drew a good salary and early top-ups to their CPF SA account.

- Young person whose parents help fund their CPF SA account to the maximum and give them a high-earning job that allows high CPF contribution above the CPF FRS limit or

- Their parents somehow make Voluntary Contributions (VC3A) up to the annual limit of $37,740.

Here are some CPF Rules to consider when thinking about whether the CPF SA cannot be more than this:

- Below the age of 55, members cannot top-up more (via Retirement Sum Top-up or RSTU) than the prevailing CPF FRS. The growth of the account (4% p.a.) should outpace then growth of the annual CPF FRS limits.

- We already account for a maximum salary contribution via either a high salary from work or VC3A contribution.

- Members cannot transfer more than the CPF FRS from their CPF OA to CPF SA before age 55.

So this is how the math works out.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Lee

Monday 26th of February 2024

Hi. If the aim is to have FRS but let interest contribute as much of it as possible, at 55 we choose to transfer the full ERS (2x FRS) to RA and at 65 or 70 before CPF Life starts withdraw till only 1x FRS remains in RA, would that be a good strategy? Thanks.

Kyith

Friday 1st of March 2024

Hi Lee, you should note that the money transferred into CPF RA after 55, is considered as top up monies, cannot be withdrawn even after property pledged. Is this your intention?