Prime REIT. Prime REIT. Prime REIT.

If you say it fast enough, and repeat it often enough it becomes Prime Rib, Prime Rib, Prime Rib.

Not too long ago, Keppel Capital partnered with Peter M. Bren and Charles J. Schreiber, Jr’s KBS Realty Advisers to list a Grade B Office REIT called Keppel KBS in Singapore.

Keppel Capital and KBS Asia Partners (KAP) have lodged their prospectus and will go ahead to list their Grade A Office REIT called Prime US REIT.

This article will go through what I think about this REIT.

The Offer

From what we understand, there will be a Placement and public offer at a price of US$0.88.

There will be a total of 923 million units.

The breakdown:

- Placement and Public Offer: 335 mil units

- KBS REIT III: 228 mil units

- Cornerstone Investors: 360 mil units

- AT Investments Limited: 8% of REIT

- KCIH: 6.8% of REIT

- The Schreiber Trust

- Credit Suisse AG, Singapore Branch

- DBS Bank

- Hiap Hoe Investment Pte Ltd

- SPH: 6.7% of REIT

This will give Prime US REIT a market capitalization of US$812 mil.

The sponsored wanted to list Prime US REIT sometime ago since last year but the volatility last year and all the negative USA tax situation have made listing very challenging.

From what we understand there were some changes to the configuration of the REIT listing:

- Mainly SPH becoming a new cornerstone investor

- SPH (Times Properties Limited) also took a 20% stake in the manager

- KBS REIT III ramp up their stake from 16% to now 24.7%

- The offer size (cornerstone + placement + public offering) got reduced from US$705 mil to US$612 mil

- Gearing going up from 35% to 37%

The challenge for a REIT that wishes to enjoy Portfolio Interest Exemption (PIR) and not pay the 30% withholding tax on dividend is that each non USA resident shareholder cannot own more than 10% of the USA REIT.

And that might be a reason why each shareholding is rather small. The sponsor won’t be a substantial shareholder.

It is interesting that Prime US REIT’s largest shareholder is the fund that it bought its asset from. I am not sure how I should conclude here. I think the sponsored originally do wish to realize more of the asset sales from KBS REIT III to this entity and not hold so much units.

However, in light of the difficulty in drumming up interests, or their anxiety of how poorly Prime US REIT will do after seeing the lukewarm response of ARA Hospitality REIT and Eagle Hospital Trust, they decide to pivot.

At this point, we should really talk about who owns the manager:

- KBS Asia Partners (KAP): 40%

- P Bren KAP I, LLC, which is owned by Linda Bren 2017 Trust – 33.3%

- Schreiber KAP I, LLC, which is owned by Charles J Schreiber Jr – 33.3%

- Rana KAP I, LLC, which is owned by Rahul Rana – 16.66%

- R Bren KAP I, LLC, which is owned by Richard Bran – 16.33%

- SPH – Times Properties Limited: 20%

- Keppel Capital Two Pte Ltd – 30%

- Experion Holdings – 10%

- AT Holdings, Sai Charan, own by founder Arvind Tiku

You will realize that, the majority cornerstone investors, major shareholders and the managers, are almost the same people. DBS has been actively trying to bring these oversea players to come and list on our bourse.

It is as if they listed a vehicle that is primarily owned by themselves, or their partners so that minority shareholders can ride together with them. I think more likely they were unable to find the cornerstone investors that are interested and thus KBS REIT III would have to take up more. If it is for their own khakis, they could very well let this entity be unlisted and manage themselves.

A Concurrent Listing

On 8th of Jul, after the final prospectus is announced, we got news that the placement and initial public offer will take place concurrently.

Usually, these IPO placements and initial public offering are done sequentially. It is VERY RARE that this is done together.

When an IPO and placement are carried out together, if there are weak public demand, the book makers can shift the public offer to the placement. In this way, the underwriters will not need to swallow a large chunk of the IPO shares (like what happened to Eagle Hospitality Trust where the IPO was lukewarm)

If the demand is weak for the public offer, the IPO will not be priced and the applicant’s funds will be refunded and the IPO will not take place.

This is a rare move by a listed company and usually the company doing the IPO would have pulled the plug. However, since Prime US REIT have tried a few times trying to list, they decide to take this challenging route.

My sources tell me that the placement was less well received, so perhaps that is why they are taking this route.

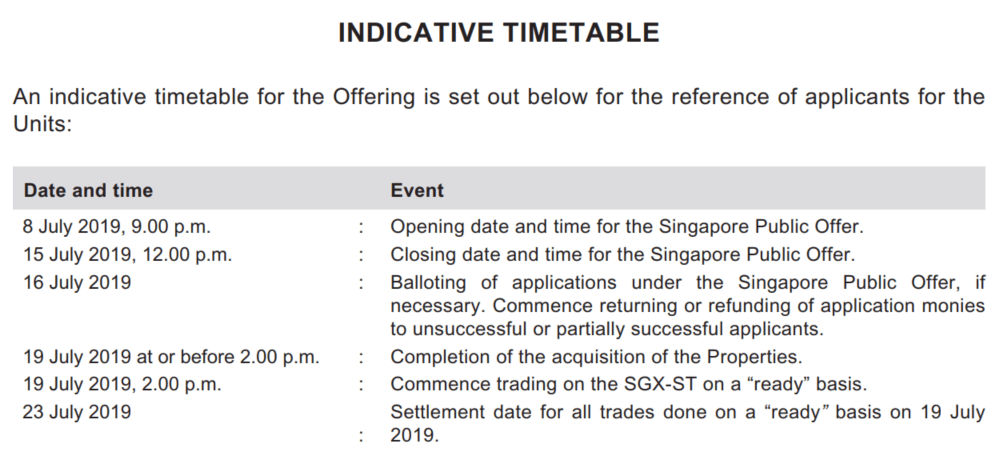

The Time Table

The Portfolio

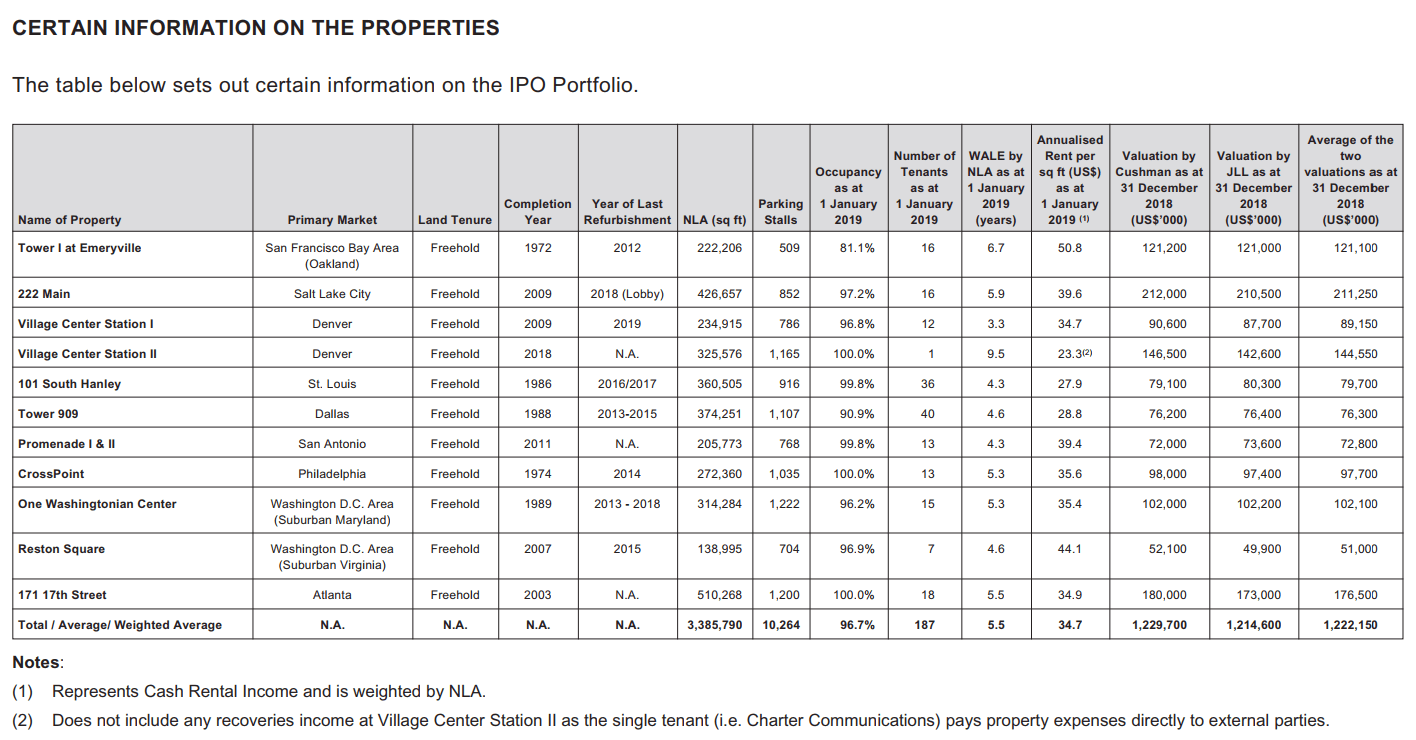

Prime US REIT consist of 11 Class A Office Properties. Singapore investors should not be so unfamiliar with the office property scene in the USA as Keppel KBS was listed a few short years ago.

Its closest peer is probably another Class A Office REIT Manulife US REIT. I have written enough content on Manulife US REIT, the characteristics, the withholding tax situations, the nature of the leasing in that country.

I think if you are investing in Prime US REIT, you should at least read through what I have to say about it (especially if you are still not so sure about the tax shield stuff):

- My Manulife US REIT Analysis

- Manulife US REIT Reaches a Dividend Yield of 7.80%. Here’s More Insights about the REIT

- 11 Deeper Things I Learned about Manulife US REIT

- Manulife US REIT and Keppel KBS Announced Minimal Impact from Section 267A Regulations and Barbados Tax Rate Changes

- More High Yield Certainty from Manulife US REIT FY 2018 Result

- Thoughts on Manulife US REIT’s Accretive Acquisition of Centerpointe I & II

One thing I realize is that majority of the portfolio are sub-urban Grade A properties. That can explain the attractive CAP rate for the portfolio.

This is not a slight on Prime US REIT. About 50% of Manulife US REIT’s offices are located in sub-urban locations. They believe that there is a trend towards moving out closer to where the employees live, so that there are more work life balance.

Class A office can be found in the CBD or sub-urban. Cushman defines Class A as the most prestigious, high quality standard, well-located buildings, typically steel and concrete construction, built or renovated after 1980 and competing for premier office users with above market rents.

- 4 properties are in Tier I cities – 28.7% of Net Property Income

- 4 properties are in Tier II cities – 35.9% of NPI

- 3 properties are in Tier III cities – 35.3% of NPI

The properties are in good state of upkeep as the current management has systematically made necessary improvements to the building systems and added or refurbished common areas as needed over the years to enhance their appeal. (for more information on Class A, Class B and Trophy, refer to my past Manulife US REIT articles)

- Based on the listing price of US$0.88, the dividend yield in FY2020 is 7.6% and FY2019 is 7.4%

- All 11 properties are Freehold status

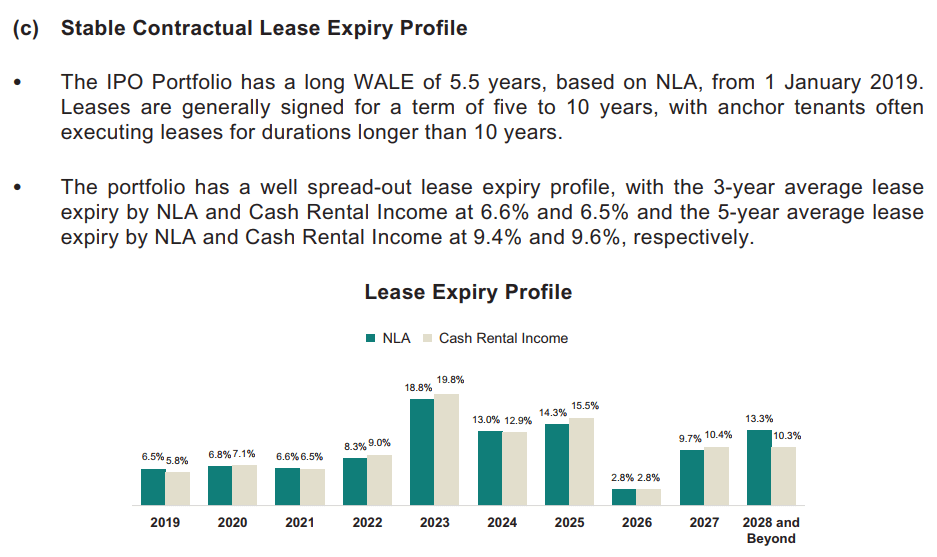

- The Weighted Average Lease Expiry (WALE) is 5.5 years.

- The average occupancy is 96.7%

- 10 out of 11 either are LEED Certified, Energy Star Certified, or LEED Gold, LEED Platinum, signifying their energy efficiency

- Average 2.1% annual rental escalation

- Management fee: 10% of Annual Distributable Income and 25% Performance fee based on the improvement in Dividend per Unit

The WALE is relatively long, the yield is attractive and the gearing is reasonable. I think some investors would like this portfolio if the managers is able to grow this portfolio.

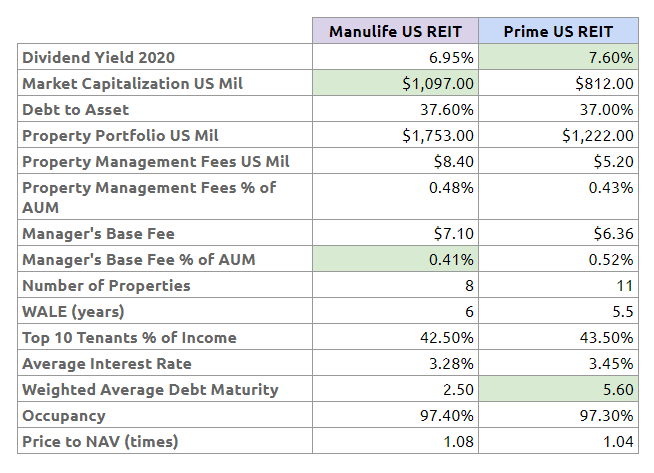

Prime US REIT versus Manulife US REIT

Investors here have about 1 year plus to be acquainted with the manager’s capabilities in acquisition and ability to renew existing leases, leased out new leases.

Depending on how comfortable you are with KBS, your other question is how Prime US will measure up against another pure Class A portfolio.

The table below shows how Prime US and Manulife US compared against one another:

Prime US REIT looks more attractive in terms of dividend yield. What is not reflected in this comparison is that both REIT is paying 100% of their manager’s fees in units, so that is a rather fair comparison.

The property portfolio value for Manulife US REIT is lower than the latest figures because I want to gauge the property management fees and manager’s base fee as a percentage of the property value. Both REIT is paying roughly the same percentage in terms of property management fees. Manulife US REIT, surprisingly have a lower base fee as a percentage of AUM compared to Prime.

One comparison that I missed out, and I would include it in writing is that both Class A office REIT average 2.1% in annual rental escalation (if you combined organic rental escalation and mid term review)

If we were to compare the profile of properties, 75% of Manulife US REIT’s properties are in Tier I cities, while the rest are in Tier II. Whether that matters or not is another question all together.

Many businesses see Tier II and Tier III cities as desirable destinations, particularly in times of economic strength. These areas present opportunity for growth and development and allow businesses to expand and provide employment to people in growing cities. Additionally, the cost to operate in prime Tier I real estate is expensive, and companies often see underdeveloped areas as a way to expand and invest in future growth.

In contrast, businesses tend to focus more on the established markets in Tier I cities when the economy is in distress, as these areas don’t require the investment and risks associated with undeveloped areas. Though they are expensive, these cities feature the most desirable facilities and social programs.

Investopedia

While Tier I tends to be more developed, they also tend to have lower CAP rates. I tend to think that much of their value is in their perceived lower downside volatility in property value while in other Tier cities, there are more for rental yields to grow, but also more volatility in property demand and supply.

The rest is almost the same except that the weighted average debt to maturity for Prime US REIT is vastly higher.

Given the size of Prime US REIT’s portfolio, and the ownership structure, I think there might be a rights issue coming our way in the future.

The possible lack of liquidity might work against the REIT in raising non-renounceable rights issue or placements, which are typically to institutional investors, family offices.

Manulife US REIT are starting to reach the size where they can carry out acquisitions, finance by equity raising that are at slight discounts. Prime US REIT can place out as well, if they place it to some very rich individual or entity, and the current shareholders are willing to subscribe to even more of Prime US REIT’s units.

The possibility of future rights issue might put a ceiling to the share price of Prime US REIT.

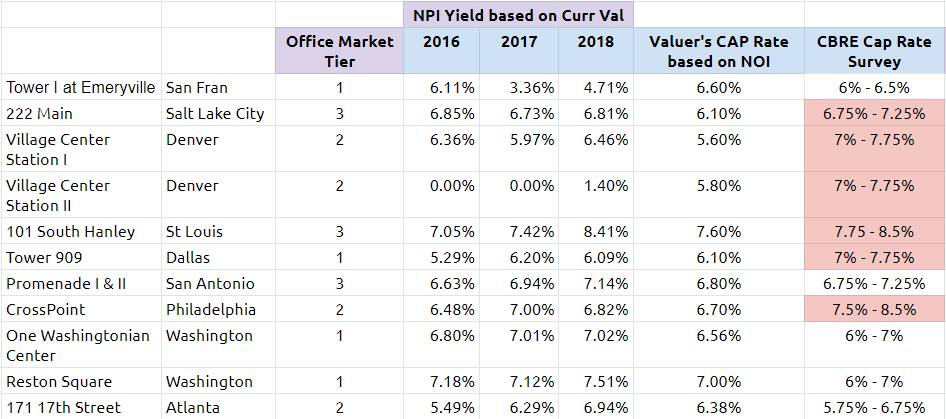

Reviewing the Past Revenue and Profit Performance

Prime REIT presented some data regarding the properties’ past revenue and net property income figures.

I thought the data will at least enlighten us how well the properties have been performing.

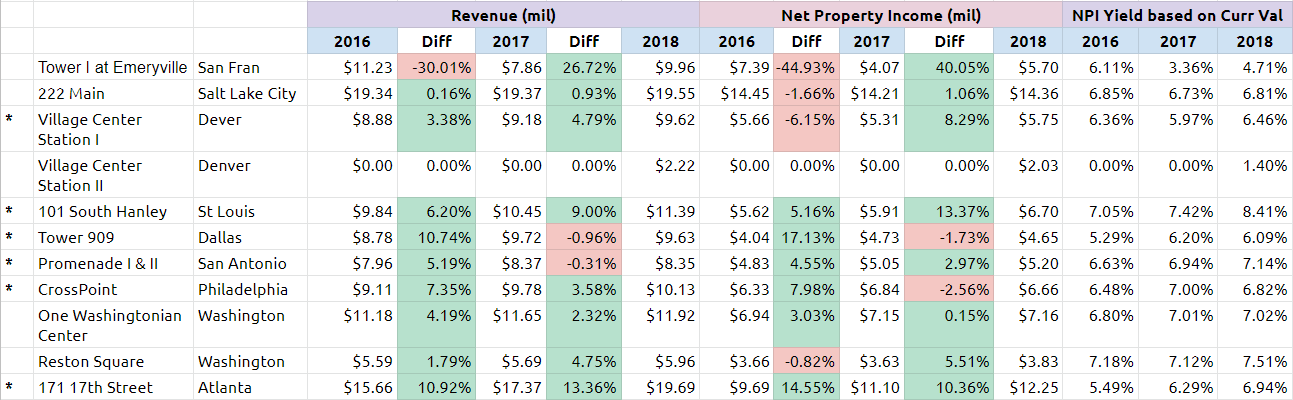

In the first table, I compare the year on year performance of the revenue. There are some properties that have interesting results:

- Village Center Station I: despite a drop in occupancy recently, revenue growth was strong, which may indicate strong leasing

- Promenade I & II: despite a drop in occupancy in 2017, revenue was up

- 171 17th Street: This property shows some improvement in occupancy but the revenue revision is very good

I wanted to see if there are some real operating leverage for the properties.

In theory, the cost of operation should not increase proportionately as rent increase via organic escalation (in Prime US REIT’s case, it is an average of 2.1% a year increase).

Majority of the leases, I suspect are on modified gross rent. We keep seeing in the prospectus recoveries income, which is likely the expenses that the REIT was able to recover from tenants. So these leases should be something rather close to like double net leases at least.

We can analyse this by looking at the difference in growth year on year between the revenue and net property income.

It is not always a one to one relationship. For Village Center Station I, in 2017 to 2018, the revenue went up but the NPI went down. Same for Reston Square.

However, in a lot of cases, we see majority of the revenue increase directly passed to the bottom line (net property income):

- A 400k rise in revenue in 2018 at Village Center I resulted in an almost 400k rise in NPI

- A 1 mil rise in revenue in 2018 at South Hanley resulted in a 800k rise in NPI

- A 1 mil rise in revenue in 2017 at Tower 909 resulted in a 700k rise in NPI

- A 1.7 mil rise in revenue in 2017 at 171 17th Street resulted in a 1.4 mil rise in NPI

The conclusion is that in terms of income, it is not a 100% pass through from revenue to NPI, but baring any exceptional costs, a large portion should be passed to the income.

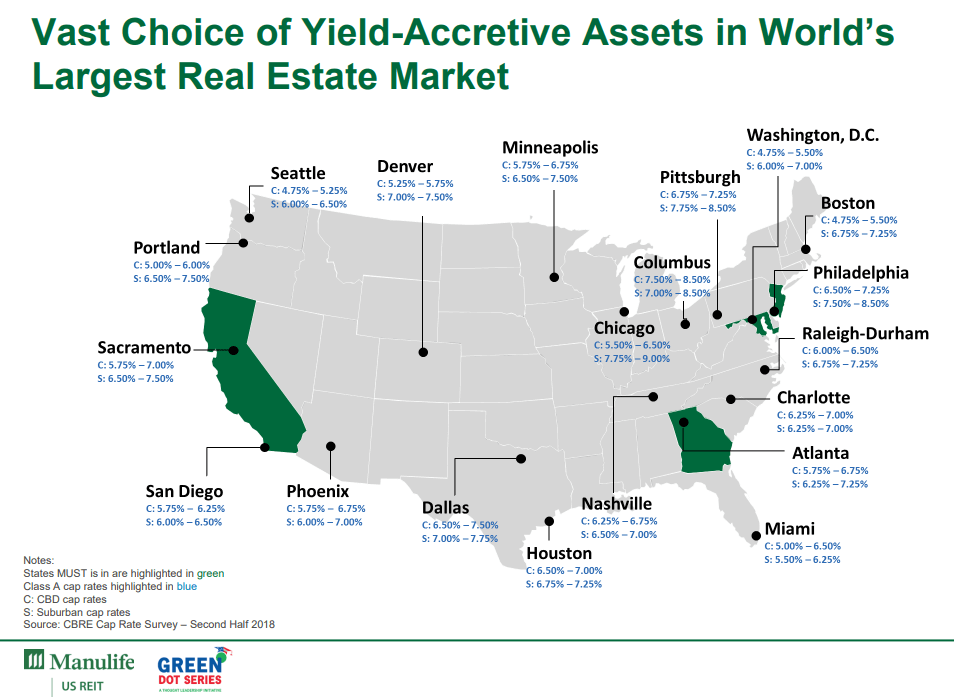

To the extreme right of the table above, you can see the net property income yield progression over the 3 years. They are measured against the latest valuation of each individual property that Prime US REIT’s shareholders will be acquiring it at.

You can compare it against the CAP rate published by CBRE CAP Rate Survey for the second half of 2018.

I have tabulated for easy comparison:

Those rows market in red are the buildings where the Valuer’s CAP Rate, based on their Dec 2018 Net Operating Income, is less than what CBRE surveyed in 2H 2018.

Do note that the surveyed CAP Rate is based on properties whose income is stabilized and with a certain level of occupancy.

Emeryville occupancy was rather low which explains the low yield versus market, Village Center Station II just completed not too long ago so the data is incomplete.

If you take out Village Center Station II, 36% of the portfolio seemed to be bought below market rent. You can look at it two ways:

- The shareholders purchased assets that are below market performance

- There are opportunities that the results can be improved upon

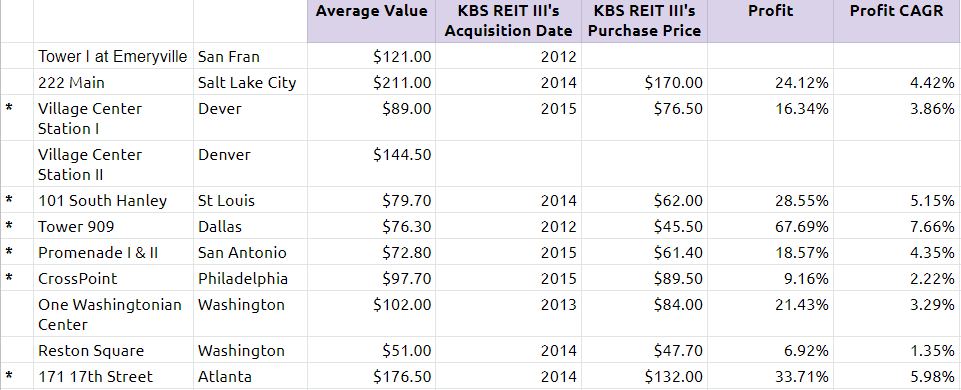

KBS REIT III’s Profits

The properties that were sold into Prime US REIT were from an unlisted REIT KBS REIT III. KBS REIT III would still own 24.7% of Prime US REIT.

If we look at some of the presentation of KBS REIT III we can get some information such as the purchase price of these properties, how much work was put into them, and when was the purchase.

The table below presents some of these information.

I am rather puzzled why I cannot find the data on the latest valuation of these properties. It is as if the unlisted REIT did not revalue the properties.

My hunch is that to minimize taxes, the properties are treated as plant, property and equipment and are accounted at cost minus depreciation. Thus, I cannot find that information there.

I did tabulate the CAGR for some of those properties since their purchase. The Atlanta, Dallas, St Louis property have some pretty good CAGR.

However, I don’t think it is fair to say these properties are not cheap. A fairer comparison would be the appraised value of these properties in 2018 versus the price shareholders buy it at. I could not find this information.

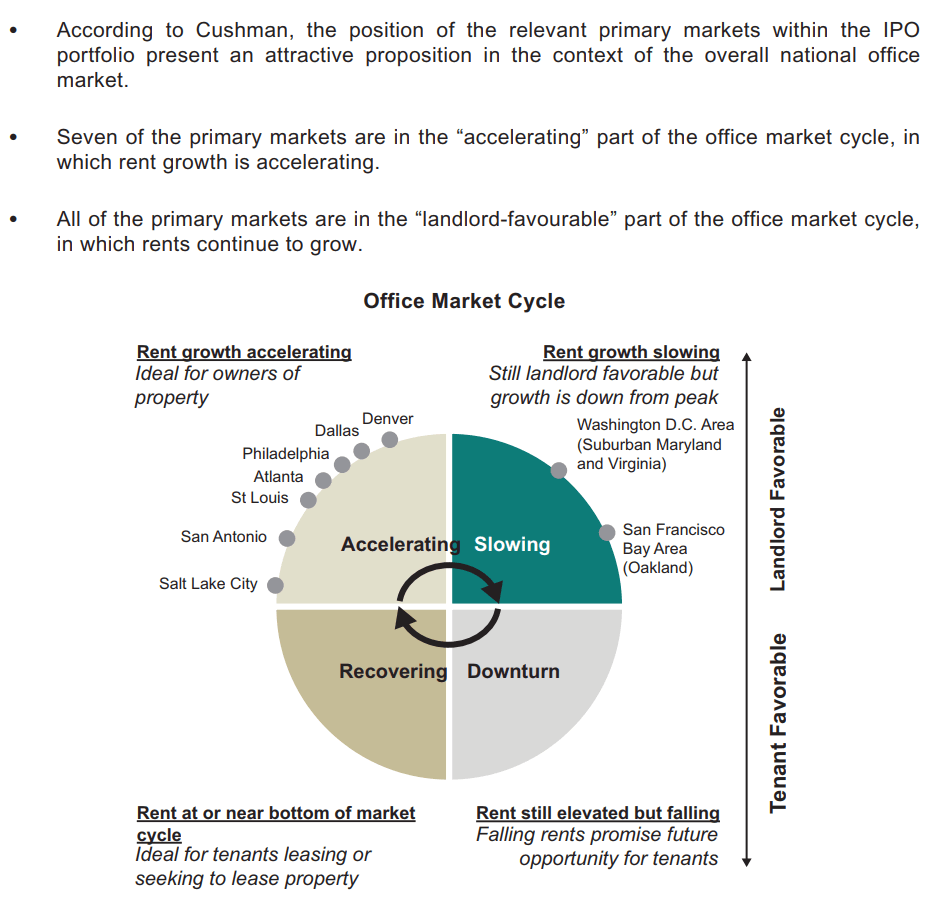

The Growth Potential of Prime US REIT

Prime US REIT do look like it has an organic growth angle.

There is this rough office market cycle clock, which is to help the investors visualize where in the property cycle, the various markets are in.

Somehow, majority of the properties, are in cities that are in accelerating growth. Graphics like these are always subjective and should be taken with a pinch of salt.

From the residential property podcast that I have been listening to, things are getting extremely cautious over there.

The opportunity for Prime US REIT is good if the growth is really there. Prime US REIT’s lease expiry is well staggered like a bond ladder.

In this way, the risk that the leases are expiring in a year where the market is in a downturn is diversified away. On the flip side, as the expiry is well staggered, it allows the manager the opportunity to lease out or renew leases at higher rents.

This is something bonds do not have, which is the ability for your dividends to grow.

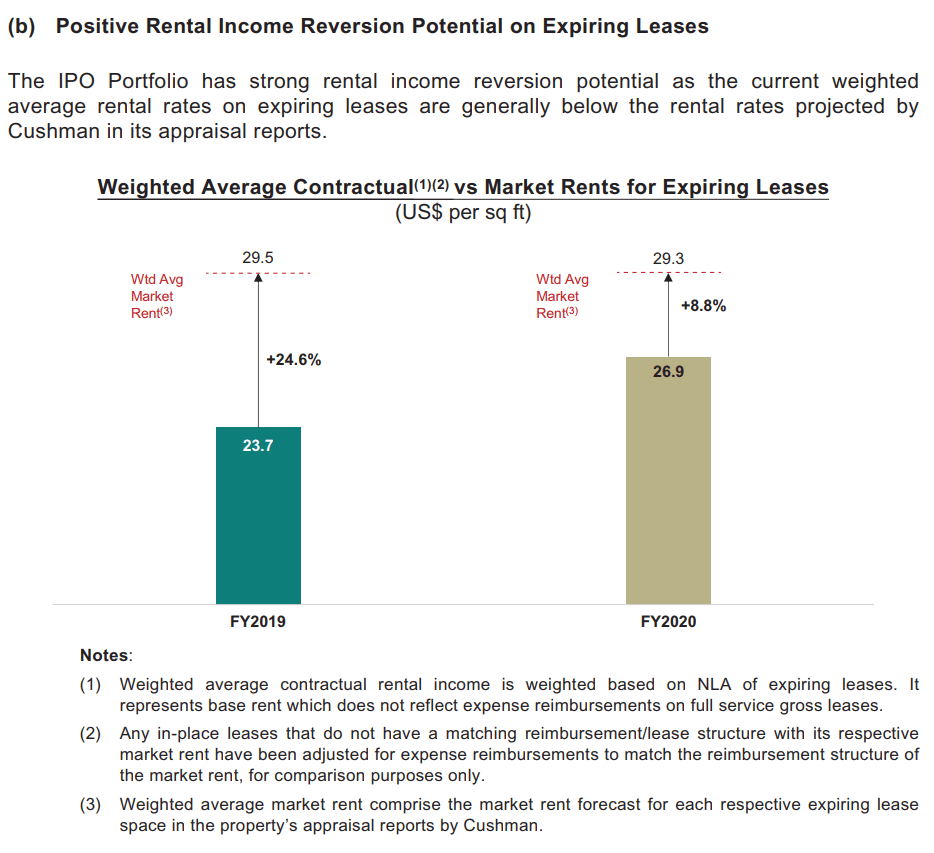

In the illustration above, Prime US REIT average market rent is below that of the market rent.

My friend, Caveman, will say that perhaps some properties are so difficult to rent out at market rate, thus they are forever somewhere below market rate.

However, at least there are some potential of organic growth from a low base (low occupancy, low passing rent, expiring rent), compared to their competitor who have less of it.

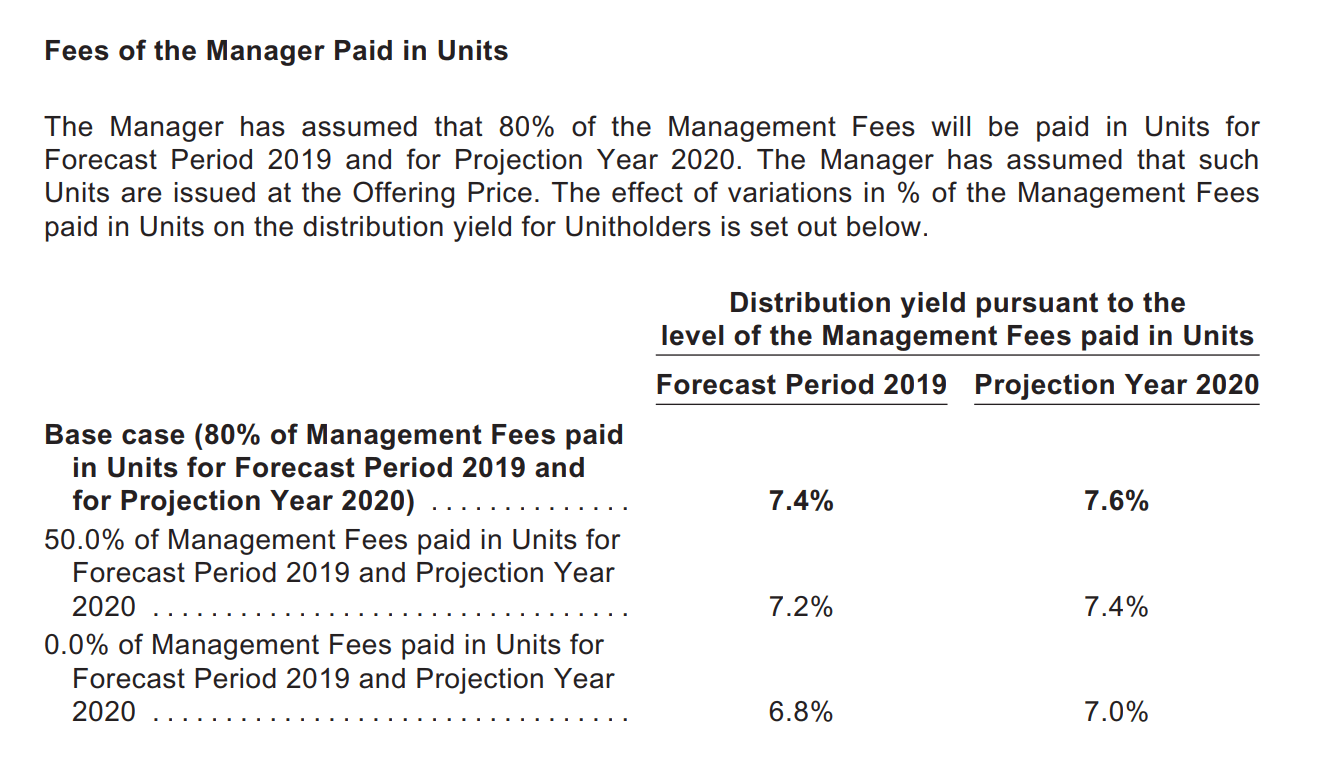

Room to Pull Back Paying Management Fees in Units

Prime REIT presented a section where they show the sensitivity analysis, if the manager do not take their management fees in units. For a lot of the REITs, the dividend yield is attractive because they paid out all their fees in units. This increases available distributable income and thus dividend per unit.

In the case of Prime US REIT, we can see that if they do not pay any management fees in units, their dividend yield will be the same as Manulife US REIT now.

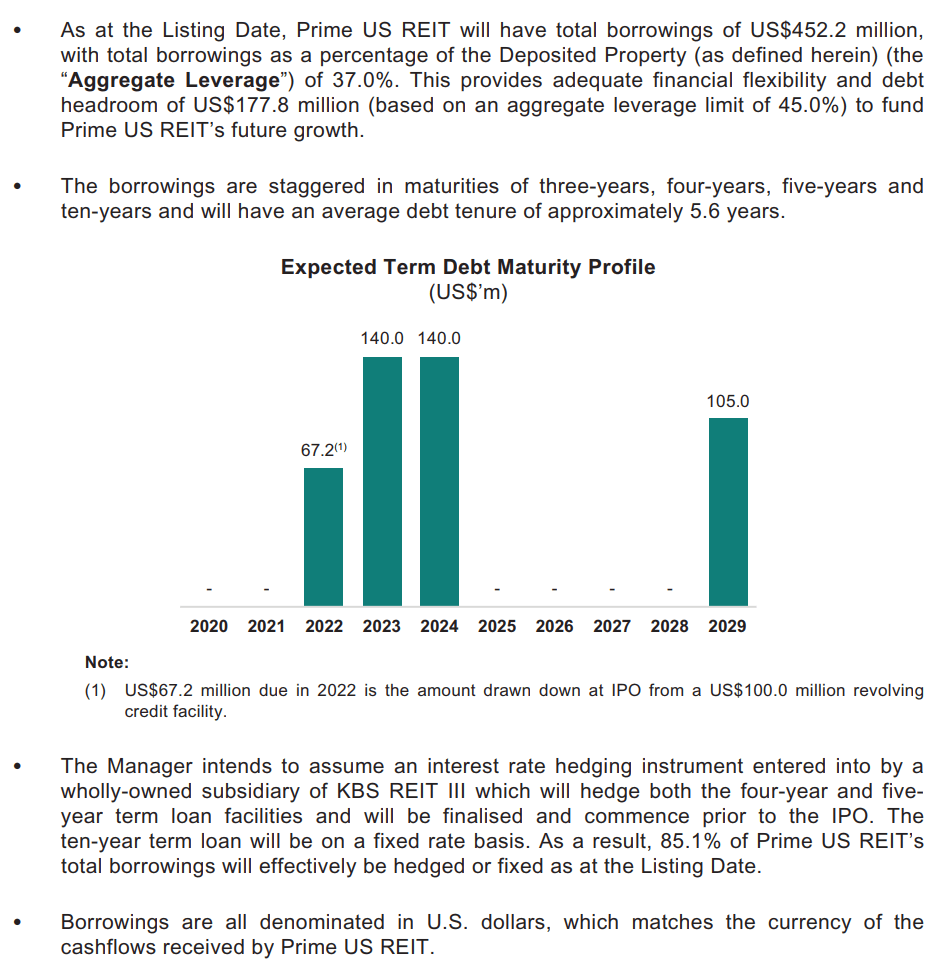

Long Average Debt Expiry

What I noticed about the debt structure is that their debt are concentrated firstly, but not too different from when Manulife US REIT start off at IPO. Overtime, these REITs should be trying to “ladder” out their loans to minimize refinancing risks.

The second thing is, man, the average debt maturity is 5.6 years. That is very long! Which is a good thing as it minimizes uncertainty there.

I think shareholders will appreciate this, especially when their debt interest is reasonable at 3.45% and 85% fixed by hedging.

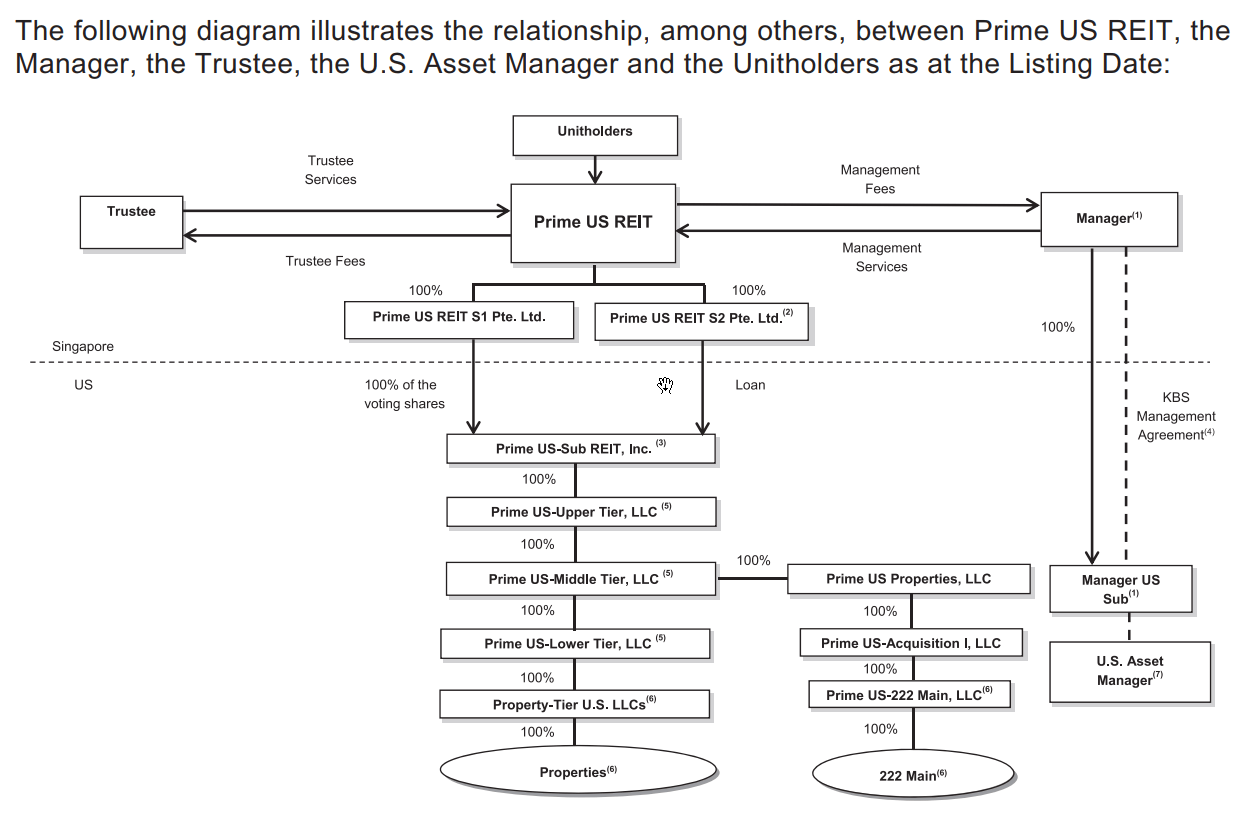

Tax Structure and Risk

The following illustration shows how the REIT is set up.

If we compare to Keppel KBS and Manulife US REIT, the main difference is the lack of a Barbados intermediary company, which both of them have.

The Barbados structure is to address some of the potential tax complications brought about by the major tax change in the US in 2017 called the Tax Cuts and Jobs Act (TCJA). By having the Barbados entity, the two REITs tried to address the problem that they will be classified as a “Hybrid Entity” (the Section 267A). If they are, then they cannot use the shareholder loans, loan from the parent in Singapore to the child company in USA as a tax shield, to minimize the taxes.

Without the tax shield, this means the shareholders potentially is going to get a 10-15% cut in their dividend. That is massive.

However, since end Dec 2018, the clarification to the TCJA do not show that Manulife US REIT and Keppel KBS’s structure will be classified as a Hybrid Entity.

The final all clear is suppose to be announced some days ago, but it seems that it has been delayed.

Nevertheless, with the way Prime US REIT is structured, which is similar to how KBS and Manulife US REIT originally structured during their IPO, it more or less means that management strongly believe that there are no issues there.

This tax stuff is rather cheem, but if you are putting your money in, perhaps you are interested to read about it. You can read my two articles:

- 11 Deeper Things I Learned about Manulife US REIT

- Manulife US REIT and Keppel KBS Announced Minimal Impact from Section 267A Regulations and Barbados Tax Rate Changes

If you are a shareholder, you need to submit your W8-BEN form.

This is to firstly identify you as a non-resident USA citizen, so that you can qualify for Portfolio Interest Exemption (PIR), that your dividends will not subject to a 30% dividend withholding tax.

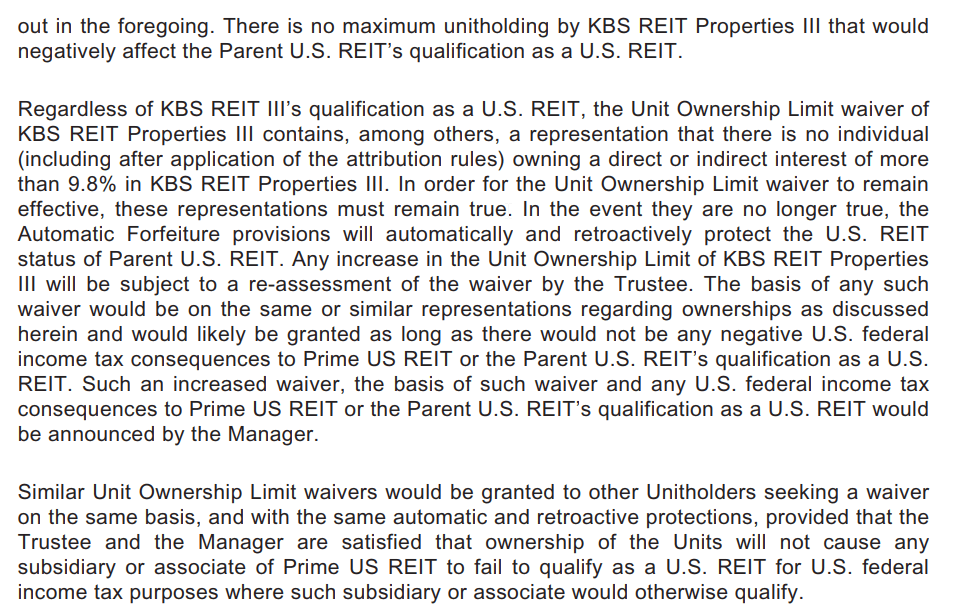

Secondly, it is also for the REIT to track the level of shareholdings of each shareholder to be less than 9.8%, so that they will not be in violation of the PIR.

One thing that is interesting is that, to not violate the PIR, each shareholder holding cannot be more than 9.8%.

Then how come KBS REIT III can own 24.7% of Prime US REIT?

This is answered in the Prospectus, and it was explained right at the start of the prospectus:

Fxxking wall of text.

No wonder no one reads the prospectus.

I think the general idea is that while KBS REIT III owns 24.7% of Prime US REIT, the manager have obtained an Automatic Waiver such that it will not disqualify Prime US REIT’s USA Subsidiary from qualifying as a US REIT for federal income tax purpose as long as it is advised by an independent tax adviser and let the shareholders know of the risk that this Automatic Waiver may be forfeited in the future.

This Automatic Waiver provision protects KBS REIT III from losing its US REIT status. A US REIT cannot be held by more than 50% by less than 5 or fewer individuals

Prime REIT have put in place the process of identifying substantial shareholders. The moment that a substantial shareholder crosses the threshold, the shareholder’s units will be transferred out so that the shareholder will not violate the PIR.

If you think about it, the unlisted KBS REIT III, probably are made up of shareholders that, each have smaller shares that would make up less than 9.8% of Prime US REIT if they directly own it. So this waiver probably make sense.

The risk is if this structure (as advised by an independent tax consultant) is not recognized or illegal, then the manager might be looking for at least 3 substantial shareholders!

Conclusion

I think with the recent run up in REIT prices, with the yield compressing, and the recent IPO of USA hospitality REITS ARA Hospitality and Eagle Hospitality Trust, many are thinking this is a bubble.

Sentiments wise, a sponsor will not bring a REIT to the market if they cannot get a good showing out of it. So IPO are usually released when the times are better. It will not be cheap.

However, there are REITs where it makes sense to buy at IPO because of the potential for growth. Not just that, they are recognized by the larger funds, investors as a REIT that is under good management, good growth potential, less risk (in terms of surprises), good quality assets. They will do well.

I just think that right now there are 2 REIT market, the blue chip larger capitalized ones and the smaller ones. The first market has been running, the second one, not as much.

My sensing is that due to its initial IPO size, it might be languishing for a while. Acquisitions will come in. And likely using debt and rights issue to grow it to US$ 1.2 bil. Without it being big enough, there should be limited price appreciation.

The recent lukewarm REIT IPO response certainly worked against them.

But the portfolio is not too bad. The portfolio is mainly sub-urban based Class A office, which explains the higher dividend yield, and so it looks attractive to investors. From what I see, they are all located with recreational and retail amenities.

I am still thinking about getting IPO assets with some below the market CAP Rates and what I should think about that.

There are potential for yield improvement for Prime US REIT in the future and that is where we can access the competency of the manager and their potential to organically improve the portfolio.

I also like the longer average debt expiry as this reduces some uncertainty.

I write more about REITs in Learning about REITs below:

Here are My Topical Resources on:

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- Should I Take Less Risk in My Fixed Income Allocation by Moving Away from a Global Aggregate Bond ETF? - May 5, 2024

- Singapore Savings Bonds SSB June 2024 Yield Climbs to 3.33% (SBJUN24 GX24060A) - May 3, 2024

- New 6-Month Singapore T-Bill Yield in Early-May 2024 to Stay at 3.75% (for the Singaporean Savers) - May 2, 2024

Retailahbeng

Wednesday 17th of July 2019

1. After close of IPO - Prime reit issued announcement in evening that Stabilisation/over-allotment is 22,727,000 Units (6.8% of offering). Prospectus has a different number for stabilisation/over-allotment option of 46,193,000 units (13.8% of offering). This is almost 50% reduction. There should be an explanation how this affects investors, is this a reduction in stabilisation/over-allotment option. As an investor, I think a bigger amount available to stabilise is better. 2. Another announcement says the public offer or retail tranche has increased from strong demand. Public tranche went up to 40,909,000 Units, above original size of 16,761,000 Units. Where did the extra 24,148,000 units for this increase come from. The announcement does not say. Guessing: a. 23,466,000 units came from reducing the stabilisation ability/over-allotment option for the IPO; and b. 682,000 units are unaccounted for. It is good for issuer to clarify where the units from the public tranche demand comes from. The prospectus does not say that over-allotment option/stabilisation can be reduced to satisfy extra demand from retail investors. 3. If the over-allotment option is reduced, the issuer should clarify the resulting difference to information in the prospectus. There are many pages that use the original over-allotment option figure. EG: page 87 the shareholding of major shareholders assumes the over-allotment option is exercised in full, are based on original over-allotment option size of 46,193,000 units (not 22,727,000 units). KBS REIT Properties III’s final shareholding is not 182,216,000, but 205,682,000 which is 22.3% (not 19.7%) of the total unit capital.

4. There is no announcement on the placement tranche demand. Also no announcement whether placement agreement was signed (supposed to be 15 July according to prospectus). Since Demand = Placement tranche + Public tranche + over-allotment option. If the over-allotment option is reduced, does that mean that total demand is reduced? In this case it seems to have been shifted to public tranche, and it is unclear why. They issuer should clarify whether the over-allotment option demand was originally intended to be from the institutional placement and whether that demand now is no longer there but only in the retail tranche and is that the reason for the change?

5. Can the issuer or banks change the offer structure stated in the prospectus so drastically after the close of the IPO? Retail investors rely on the offer structure stated in the prospectus when they apply. Would a retail investor still have bought if they knew the stabilisation/over-allotment option would after close be reduced by almost 50%. Eagle REIT stabilisation amount was also 6+%, but share price went down. Does reducing the stabilisation from 13.8% to 6.8% mean like Eagle a lesser ability to stabilize, and greater risk to share price?

6. Does the change in offer structure mean that the bankers do not have to underwrite? There should be an explanation, why the change, and if it affects underwriting by the bankers. If the IPO is not underwritten, this must be clearly stated in the prospectus.

Kit

Thursday 18th of July 2019

As an investor - i think I would want the public tranche to not increase - create more demand, and keep the stabilisation, so that unsatisfied demand and the unreduced stabilisation would help keep the price up. Also this is all very confusing, that things can change from what is stated in the prospectus after the ipo close

Aa

Tuesday 9th of July 2019

So are you buy this ipo

PR

Wednesday 3rd of July 2019

hi - excellent summary - should have saved my time going through the prospectus and just read this first..

As per the assets Prime is buying from KBS III. See the blow presentation (9 mins 11 seconds mark). you can see their cost basis as on 31st march 2019.. If my rough calcs are correct. . assuming that KBS III is holding these properties on their balance sheet at a cost basis the sale will generate something like $342MM profit, which will more than pay for the stake they are purchasing in prime..

https://gcs-vimeo.akamaized.net/exp=1562151647~acl=%2A%2F1354544922.mp4%2A~hmac=448b48c7f10c153bceb159b857b505c74f6811a5d6efe2cf02f3ab1314114cc7/vimeo-prod-skyfire-std-us/01/3010/13/340050735/1354544922.mp4

Kyith

Wednesday 3rd of July 2019

Hi PR, i cannot view this.

BlackCat

Sunday 30th of June 2019

Can I ask a dumb question...Where did you get the prospectus from? I was not able to find it on the SGX website?

Kyith

Monday 1st of July 2019

Hi BlackCat, it can be a little hard to find. I got to thank a friend who asked what I think of it. If not I couldn't find it as well

https://eservices.mas.gov.sg/opera/Public/CIS/ViewProsDetail.aspx?prosID=cd36d1026fa14937991d551839667be5

TruthJeff

Sunday 30th of June 2019

A lower cap rate means the property is more expensive than comparable properties within the same vicinity. To interpret your table on valuation and cap rates, most of the properties in the REIT now are "over-valued" relative to the market cap rate, not below market rate.

Kyith

Monday 1st of July 2019

HI TruthJeff, i interpret that they are not performing as well. Or that their properties are not stabilized yet. In any way, not stabilized may mean they might not have the characteristics of stable Class A properties