Emergency fund exists because some scenarios cannot be quantified

In project management, we always build up our budget, what we want to get from the sponsor in a certain way.

We need to justify for how much we actually need. For each work package (sub division of work), there are cost to it.

And then there are risks. There are usually 2 kinds of risks:

- Known risks: You go through a systematic qualitative and quantitative analysis to determined that

- Unknown risks: The shit. Things that, after putting a group of subject matter experts together, you still cannot anticipate everything

To a certain extent, risk management is similar to the way we do it, when evaluating risks while prospecting a business we invest in.

The known portion you can assigned a dollar value to the probability. The unknown is the difficult one.

A standard way is to assigned a percentage amount to the final cost figure. Say 15%.

Now, I wonder, would I want to save on this 15% and say, I am a bloody good project manager and recommend to my sponsor that I only need 5%?

It depends, I may deemed I am experienced enough to have less of this. But, if I am that experienced, I would have know that shit happens, and not save on this amount.

That’s probably a career suicide.

The similarities to planning a personal / family budget

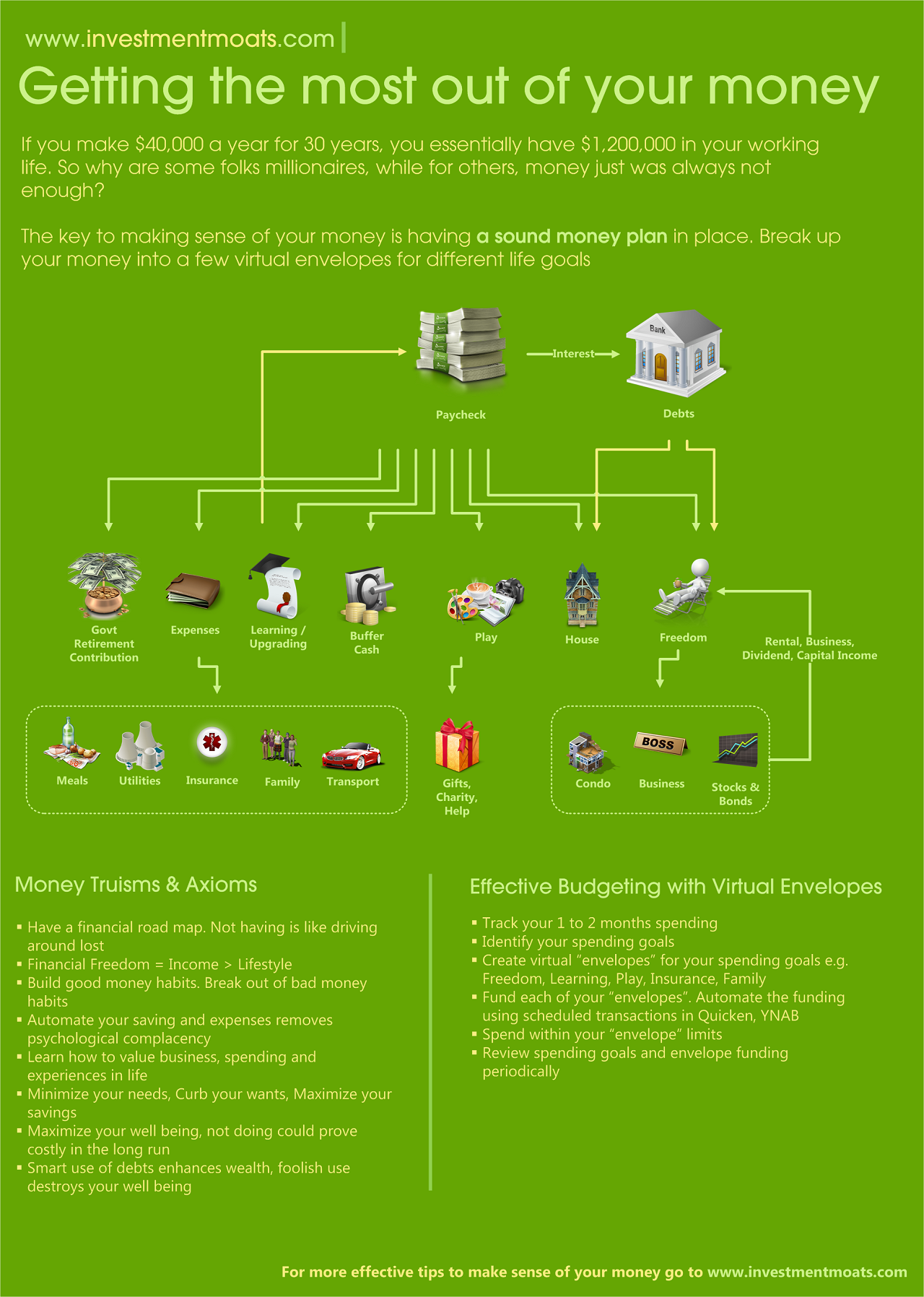

There is a reason why choosing an amount for your emergency fund / buffer fund / rainy day fund is similar to creating a project budget.

If you plan your budget well, using a methodology such as a zero-based budgeting / envelope budgeting method (read here and here), each envelope / bucket / virtual account is assigned for a certain purpose.

If shit hits the fan, you are probably going to deprive yourself from spending on something, be it critical or not.

We hope its not critical, which is why a standard rule of 3-6 month is what the experts recommend.

Your budgeting planning is not comprehensive

I gave an example where known risks are identified qualitatively and quantitatively. Where you need to spend your money on can never be very quantitative unless you keep track of what you spend on at a very granular basis.

Due to that, you missed out on

- Infrequent transactions

- Annual transactions

- Transactions you think don’t amount to much

- Costs you have yet to experience in your young adult life

All these creep into your emergency fund, because if you budget nicely, you shouldn’t have to touch the other accounts!

Budgeting is a fluid process and its on-going. By right, the more you adjust your overall budget, the more you identify these transactions as you get more experience, you should see less tapping into this fund.

Paradigms shift. So does your emergency fund needs

While 3 to 6 months is a good estimation, your lifestyle needs may change drastically such that this standard amount may not be conservative at all.

I would think it will be better to expand the fund rather than shrink its size.

Memories scarred by experience

I guess I appreciate such a fund better due to the context where I started working.

That was in 2004. We just came out of SARS and a very deep recession.

It was not fun looking for a job. I would say I had it better. My previous batch really felt the full blunt of it.

I got a starting salary of $2400. My university mates told me that was one of the largest amount they heard a graduate got.

Pay and hiring freeze everywhere.

To make matters worse, mom doesn’t work, the construction and housing scene was so bad that dad couldn’t find any work.

We were living on fumes.

Just like investing, you tend to be scarred by traumatic situations. A previous project management fault causing a huge f*** up, felling to psychological investing errors.

You never want to be in that situations again. In this case, you plan with this scenario in mind.

Mom and dad depends on me now. Better don’t f*** this up Drizzt.

The difficulty in building up an emergency fund

Its good to have a diary in the form of my Quicken. You get to reference and share how you did it last time.

There are many ways to build a 3 to 6 months emergency fund, and I was privileged that I learnt this from the more experienced investors.

The difficulty is how to go about building it.

I still have to pay back my parents on student loans of 15k odd. I also want to build up my investment warchest.

Looking back, I guess more of us get overconfident and would think its bloody stupid to let the money rot at such a low rate of return. I was like that as well.

You can choose to quickly hit the goal of saving this emergency fund first, before saving for wealth building or other saving goals, making it the top priority.

Else you can save for many goals at the same time like me. You tend to spread yourself thin, and you may lose your focus.

Back then, I considered what I left over after diverting to my virtual accounts as the emergency fund.

Because it so freaking slow, I barely hit 3 months. It took me like 2.5 years to get to that amount.

Hindsight, I probably divert too much into wealth building. I should have diverted more into building this.

Too young and too brash.

The present situation

I thought taking 2.5 years to build up 3 months of paycheck worth of emergency fund wasn’t an easy thing. Let alone 6 months.

Folks have a lot of saving goals

- Wedding

- Student loan debt

- Photo shoot

- Wedding Ring

- Housing down payment (Perhaps from CPF?)

- Renovation

My reasonably well paid civil servant friend settled after marriage and home without kids was telling me he has zero savings at age 30.

That is the stark reality facing us.

We have a long period where Singapore have not faced a heighten unemployment situation, the primary reason for an emergency fund.

Recency bias may lead us to postpone building this up, even though folks are aware the need for rainy day savings.

The sensible way perhaps is to cut out a part of your savings if you have build it up as your emergency fund or start saving a sizeable amount monthly.

Suze Orman recommends 8 months of expenses

Thanks to my friend Winston for linking me to this. Suze Orman explains why she feels 8 months of expenses is right but also dispense some wisdom on why you need it.

2 Callers called in on getting a better rate or return and exhausting his emergency fund in unemployment to pay down mortgage.

To get started with dividend investing, start by bookmarking my Dividend Stock Tracker which shows the prevailing yields of blue chip dividend stocks, utilities, REITs updated nightly.

Make use of the free Stock Portfolio Tracker to track your dividend stock by transactions to show your total returns.

For my best articles on investing, growing money check out theresources section.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Singapore Man of Leisure

Sunday 20th of October 2013

Kyith,

I must compliment you on your recent writings!

Weaving in your personal story provides the context and perspective and helps your readers understand where you are coming from.

Makes it more real and personal.

A person who has never been retrenched and a person who took 2 years to get a job after being laid off will have different perspectives on the need for emergency fund.

Hey, we have something in common, we both project managers ;)

Kyith

Sunday 20th of October 2013

I am not technically one haha but as all, we are all project managers because we take small projects in life.

have to improve the writing, else SMOL wont come and read.