I had written a lot of articles where I used the terms savings rate, or your level of savings and I think many readers may be confused about what savings rate mean and what goes into savings rate.

So this article is to try and make sense of it.

At the same time I will introduce 2 terms that we typically use in our articles:

- Your Savings Rate

- Your Spending Rate

- Your Personal Free Cash Flow

With this, it will make my other articles more understandable. I would also go through some discussions so as to help you understand these 3 terms better.

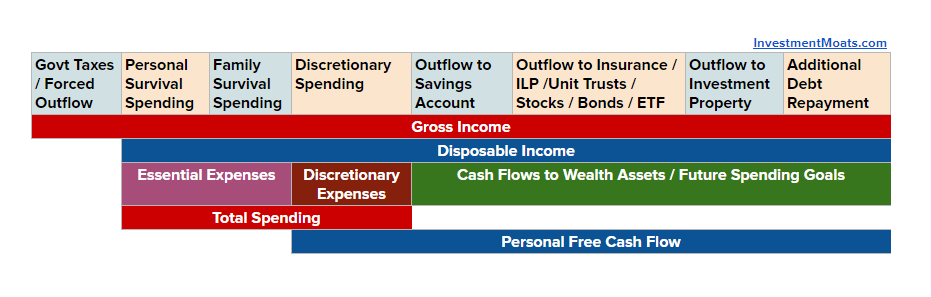

What is Your Spending Rate?

For the majority of you, you have a day job that you earn income.

Your income is made up of the portion where:

- You can touch and

- The portion that you couldn’t.

The portion that you couldn’t touch is the mandatory government pension plan system, such as the CPF in Singapore.

The income that you earn before all these deductions are called Gross Income.

Your take-home pay or disposable income is the cash flow that you get to make decisions upon that is unconstrained. So we use these 2 terms take-home pay or disposable income interchangeably.

For those of you that have a business, you are likely to get a workers income out of your company, for the work you do in your business, or a dividend income.

So overall take-home pay, disposable income, dividend income are incomes that is unconstrained for you to make decision upon.

We will all have cash outflow from our income to buy things that

- ensures we continue to function as human beings (food, housing, transportation, paying off student loans, credit card debt, personal loan)

- for our family to function (household, children’s education, mortgage payment)

- for other discretionary purposes (going to the bird park, charity donation, eating at the cafe)

What is not included is money that we channel to help us achieve future spending requirements. This may be obvious or not obvious to us.

We compartmentalize this and call these our cash flows to build our wealth assets.

Examples of cash flows to build our wealth assets include:

- cash channel to a savings account

- cash channel to a high yield savings account

- premiums on insurance endowment

- premiums on ILP

- cash outflow to purchase stocks

- cash outflow to purchase bonds

- cash outflow to purchase exchange-traded funds

- cash outflow to purchase unit trust

- mortgage on investment properties

- cash outflow to purchase managed investments

The objective here is to

- put part of our disposable income into these wealth assets

- these wealth assets grow at a higher rate of return to compound in value

- eventually, withdraw partially, or fully your wealth assets for your future spending goal or requirement

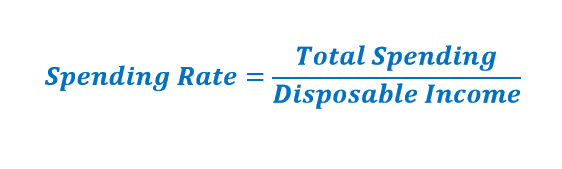

So your spending is the cash outflow from the former, less the money we channel for our future spending requirements

Your spending rate is calculated as the percentage you spend divide by your disposable income.

So for example John and his family earn $75,000/yr before deduction by the government. The government has a mandatory forced savings of 20%.

So his disposable income is $75,000 x (1-0.20) = $60,000.

In the last year, John and his family have had a cash outflow of $55,000/yr.

However, out of this $55,000:

- $12,000 is the total amount put into a portfolio of exchange-traded funds and stocks on a recurring basis

- $4,000 is the total amount put into premiums paid on their insurance endowment plan

So John and his Family’s total spending is $55,000 – $12,000 – $4,000 = $39,000/yr.

The family spending rate = $39,000 / $60,000 x 100 = 65%.

For every $1 John and his spouse earned, they spend $0.65.

What is Your Savings Rate?

Your savings rate is the percentage of cash flow that you do not spend, according to our definition in the spending rate.

The idea is, what you do not spend, you are not put into the system of cash outflows, so you are actually saving.

In financial planning, your savings rate is also called the surplus rate.

Your savings is the surplus of your money after spending.

Very often, I use both terms interchangeably.

Thus the formula for your savings rate is:

Savings rate is really the cash flow that you can allocate to your wealth assets.

Going back to the previous example, John and his family spent $39,000/yr out of his $60,000/yr in disposable income.

Thus his savings rate is = ($60,000 – $39,000) / $60,000 = 35%.

John and his family have a pretty good savings rate.

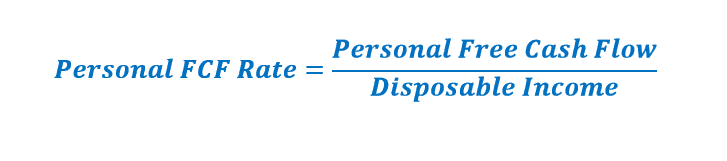

What is Your Personal Free Cash Flow?

Personal free cash flow is a term, derived from the business.

In our financial analysis, we wish to find out what is the amount of cash a stock/business has, after its necessary cash outflow, to use at their own discretion.

So for a business, the free cash flow is something like this:

Leveraged Free Cash Flow = Revenue – Cost of Goods Sold – Operating Expenses – Taxes – Interest Expense – Maintenance Capital Expenditure

Once you are done with this you can use this free cash flow to:

- reinvest in investments and property that expand your business capability

- pay down debt

- retain in your business

- payout to your shareholders

Thus a healthy free cash flow is vital. For more of the different cash flows in business, you can read my comprehensive article on cash flows here.

You can look at your personal free cash flow to be similar to business free cash flow.

Your personal free cash flow is the cash flow that you can:

- improve the lives of your family

- improve your ability to earn more

- improve the ability of your spouse or children to earn more

- the build-up to ensure financial security

- reduce your existing mortgage

- pay off more than your minimum debt repayment to speed up being debt-free

- donate for charity

In other words, your personal free cash flow forces you to decide whether to give your family a better life today versus setting yourself up so that you have great future spending power.

To compute your free cash flow, we need to revisit what considers your spending:

- Ensures we continue to function as human beings (food, housing, transportation, paying off student loans, credit card debt, personal loan)

- For our family to function (household, children’s education, mortgage payment)

- For other discretionary purposes (going to the bird park, charity donation, eating at the cafe)

#1 and #2 are considered essential expenses.

These expenses are essential because without them we will in deep trouble. You cannot cut away essential expenses if things are tighter as well.

#3 are your discretionary expense.

These are spending that give your family a better life today or set them up better in the future.

Different families will see what is considered as essential and discretionary differently.

Here is the formula:

This formula looks simple enough but the difficulty or the subjective thing is figuring out the essential spending (in this diagram it is shown as Mandatory spending. I updated this recently but did not change the graphic.)

Do we include all those spendings that you have to pay month by month such as cable television?

I don’t think cable television is mandatory, but that is me.

John and his family spend $39,000 per year but out of these probably $28,000/yr is essential.

So his personal free cash flow = $60,000 – $28,000 = $32,000.

With this you could also want to calculate your personal free cash flow rate:

Thus John and his family have $32,000/$60,000 = 53%.

With this, we can go into some deeper discussions.

Your Savings Rate versus Spending Rate

There is an inverse relationship between savings and spending rate.

Many people may not realize that deducting one from disposable income gives you the other.

The main contention is that they do not have much money saved up. So they conclude that they do not have much savings.

This, to me, is not true because most of them have

- money with their company options, shares

- premiums for insurance savings plans, investment-linked policies

- contribution to unit trust

Investments and insurance to them are not savings. And perhaps that is the growing frustration with the term savings.

If we group them up and say their overall objective is meant more for not spending now but in the future, the mindset should shift.

If we clearly break these savings cash flow masquerading as spending, you can see the distinction better.

Your Savings versus Your Personal Free Cash Flow

Your savings rate and your personal free cash flow look pretty similar.

The difference between them is how you segregate your expenses, essential or discretionary.

My co-worker, always says she does not have savings because all her expenses are essential.

A lot of us disagree with that.

I think that if you are used to your current standard of living, and cannot imagine you ever stepping down to a lower standard of living, even if you lose your job, then your saving rate will equal your personal free cash flow rate.

For those who are more intentional, they would be able to classify different grades in their spending. Thus, what is mandatory and discretionary can be identified.

Why Disposable Income? Why not Gross Income?

This is the formula that I use, but if you can choose to communicate with gross income, it is OK.

The important thing is that you communicate the parameters across.

Personally, I don’t think if you have a large amount of CPF or pension currently, it constitutes free cash flow.

However, housing mortgage, which is a large spending, is blurred as it can be considered as partially paid by disposable income, partially by your CPF.

In this case, it might make more sense to group them together. The problem with that is that your savings rate and free cash flow will be very high, as your CPF Special Account and Medisave are considered future spending objectives, or meant for the future.

The CPF is one of the reasons why we are said to have a 20% savings rate as a percentage of our gross income.

However, could we make use of it if we wish to upgrade ourselves or for medical needs? I don’t think you could do it with your Special Account, but you could for your Medisave.

So this is up to your discretion.

Summary

I think to recap, the table above gives you a good idea of how I classify things. And it might help you make sense of some things in your personal planning as well.

After I get this out of the way, I can then link to a deeper conversation on this topic.

Let me know if you have a different way of seeing things.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

GreenDollarBills

Sunday 30th of September 2018

I think that you need to focus on the savings rate. Every time you get a salary rise put a large proportion of that automatically into savings each month (via standing orders or automated bank transfers). This will ensure that your savings rate will continue to increase. Additionally, without the money available to spend then you will naturally reduce your spending as a proportion of your total income.

Kyith

Monday 1st of October 2018

That is making things look too simple. If you are lower income, all your spending are mandatory (that you have finish reducing) then how do you focus on saving rate?