Growing up, I used to have some relatives and friends telling me not to buy 4D.

It is one Singapore lottery that seems to be less popular as I grow older. My parents used to buy it. Strangely, non of my colleagues, or co-worker mention buying it.

Now TOTO, which is another form of lottery, that is another story all together. During Chinese New Year, when the pool of money snowballs to a large million, it is a must purchase for many.

I guess a common gripe about 4D might be that, people don’t commit a lot to buying 4D or TOTO.

With the amount, you will win perhaps $2,000 to $10,000 with 4D. With TOTO, the winning is much more. However, strangely, I thought the odds that people win 4D is much higher.

I think the problem is that people do not think a $2,000 to $10,000 windfall of money is going to change their lives.

And that they are not going to win so frequently that it will matter to them.

And this is one of the problem that I ponder about.

How useful is $10,000 to $200,000?

I wrote an article explaining how you should look at wealth building as a series of milestones. It is called the 11 Stages of Wealth.

You identify where you are. And then you take a look at what is the stage next and try to aim for it, if its compelling enough.

At each stage, you realize that the wealth that you build up has a functional use for it. (you should check it out. its a good conversation starter to circulate among friends. At most they will say how ridiculous these stages are)

At some stage, it provides a cash flow to pay for your current expenses. At some stage, it fortifies you against negative monetary surprises. At some stage, it reduces financial anxiety.

The difficulty is that after paying off all your high interest debts, leaving you with perhaps your mortgage loan (Stage 3), there is a wiiiiiiiiiide gap to reaching a level of wealth where your wealth assets are able to provide a cash flow to pay for your annual basic expenses (Stage 7)

So I inserted 3 stages in between. These are building up lump sum of wealth that can be rather useful in life.

You could cash flow them by just spending them like this.

But the question is, what is so useful of these lump sum?

These lump sum, might not be very big (not my opinion. Its what a lot of you think. Purely because we lived in such a high income and expense place).

In order for me to tell you to put them away, and not spend them now, I got to give you a compelling enough reason.

It is not that I cannot come up with one, but that writing them would be rather bland.

Until I read this article in The Topic that I thought explains what this amount of wealth is useful for.

The Topic asked how gifts, insurance payouts, the MacArthur Genius Award, book deals—ranging from $8,000 to over $1 million—were spent. So these are like windfall of money, that people get from winning a competition, winning a lawsuit, from an insurance payout, winning a prize, doing a side hustle. While they are not very famous people that you would know, some of them are rather accomplished in their own fields (including a long term HIV survivor).

And I pick out some of the case studies that illustrate what kind of utility a lump sum of money, that is not outrageous, can give you.

1. Giving it Away. Because Relationships provide more Financial Security than Money

Maddy inherited $250,000 when she was 18 years old. Her Jewish ancestors passed these money down so that their next generation can have a comfortable life.

Maddy discovered Resource Generation, a multicultural organization of young people with wealth and privilege, who are organizing to reinvest the money back into the communities that they were taken from.

So she decided to give away $160,000 of it.

Most adults told her that she should “keep some money for herself”.

What I like was the way she said about financial security:

I take it into account, but I also know that I want to try something different than what the generation before me has primarily done in my socioeconomic group. I’m still figuring out what financial security looks like for myself. But so far it’s meant working, and it’s also meant building relationships, because to me relationships have a lot more security than wealth.

Most of all she doesn’t like to be a gatekeeper of wealth. That means she gets to decide where the wealth goes.

I think out of all the accounts, I feel I admire Maddy the most. I always say that I know what is enough looks like.

However, if I have enough, then why do I keep those excess? Why don’t I give it away?

If I don’t give it away then do I really have enough?

If $XXX is really enough for financial security, and you are not giving that away, it seems that we are always chasing a moving wealth target.

As a 39 year old looking at Maddy’s situation, I felt that where you come from drives the way you look at money. She probably came from a background where money was less of a problem and that allowed her to weigh money versus other things of value in life.

And she thinks that relationship is a stronger security.

I am not sure.

I came from a situation where money is more scarce, so money will always take a central place in my decision making. I gave money more power than Maddy did.

And since no one helps you, you always try to be as self sufficient as possible because, no one will help you.

It is a totally different way compared to a privileged background where help is always around. Thus, we look at relationships very differently.

I always think money will be a better bet than relationship. Except that over time, as I do Investment Moats, BIGScribe and my day job more, I can see how relationships and network can buy you financial security.

2. Buying Joy for Herself and Other People

Joy is a moment of great pleasure. Usually, as they say, it came about because of something you do or something that came along with an experience.

Like Maddy, Heather McHugh came into possession of a large sum of money ($500,000).

Heather is the second person in this article who won the Macarthur “Genius” grant, for her work in poetry. This grant is from the John D and Catherine MacArthur foundation for USA individuals who demonstrated “extraordinary originality and dedication in their creative pursuits and a marked capacity for self-direction”

Heather took part of that money and founded the nonprofit Caregifted. Heather never had children, but the child she was closest to had his first child, who was microcephalic and needed a lifetime caregiving.

Heather used part of the money to get them the care they needed to find new work nearer to the wife’s parents, so that they can create a local support system (perhaps this is what Maddy talked about that relationship is a better financial security than money)

With Caregifted, Heather worked with caregivers of the most severely disabled family members, caregivers who had been at that devotion for 10 years or more:

We asked what their dream vacations would be if they could choose, given the locations we had lined up (on islands, mostly). Some simply wanted to sleep late. Some wanted a meal out. Some read a book for the first time in years. Some brought a spouse for a much-needed recharge of strained relationships. All wanted to see new territories, visit the ocean, visit gardens, wineries, fishing, markets, tourist excursions.

People who heard about Caregifted often came to us because of my life in the arts—many were artists who had not been able to reflect or catch their breath since giving birth to a child who had to battle severe challenges. All of them recovered some perspective on their own choices, chances, and changes in life. Some person they’d not been in years began to start a conversation with their futures.

And Heather explains the intangible feeling of joy that came with giving the money away:

It was a jolt of joy to give away that money—the kick of actually materializing a dream for someone who unquestionably needs it. No fancy home or golden furniture or vacation indulgence of your own can ever give you back the gift this gifting does.

McHugh was elected a Chancellor of the Academy of American Poets in 1999. She taught for some 40 years at American colleges and universities, including the University of Washington in Seattle; and she still takes some students through the low-residency Warren Wilson College MFA Program for Writers.

In 2009, she was awarded the MacArthur Foundation “Genius Grant” for her work and in 2011-2012, she started the non-profit CAREGIFTED ( http://caregifted.org ) to provide respite and tribute to long-term caregivers of the severely disabled and chronically ill. For her work there she received notice from Encore.org’s Purpose Prizes.

3. Reinvest into Capital Expenditure for the Business. And Buying some Financial Security

Tony Hightower won $250,000 on Who Wants to Be a Millionaire?

So what he did was to take the money and reinvest back into his small trivia business in NYC. The trivia business hosts one trivia night a week at a bar.

The business was doing fine, but Tony was living month to month. Without money, he cannot expand it.

When he won Jeopardy! and earned $23,000, he put it into a nice lounge and some nice things. With this bigger winning, he hired 2 people.

And he finally go a retirement account.

Two hundred and fifty thousand dollars felt like I should do something meaningful with it, because I didn’t want to wake up one morning and have it be gone.

I was in my late ’40s, and I had never been anything other than a subsistence worker my entire life.

I’ve always lived as if I were two bad weeks away from sleeping in a cardboard box. This is the very first time in my life where I feel like that might not be the case.

His trivia business is now doing well.

Was it the business that gave the financial security or was it the retirement account?

I think the retirement account assured him that he is not doing stupid things with his money. In the event that if something goes wrong with the business, at least he has the retirement money.

But it has to be the thriving business that provided that financial security.

4. Gifts and Worry/Guilt Free Spending

Danielle Henderson works as a story editor for Maniac. She shares about what her first script fee which is estimated around $27,000, mean to her.

Danielle grew up poor since her parents were on welfare. Thus, financial security was an issue.

So even with a job, and small windfalls such as this, she still does not trust it.

Danielle spoke about what having a larger budget brings to her life:

My grandma’s getting older—she’s 86—and she’s starting to exhibit signs of dementia, and I’m able to send groceries and not think about it. I’m able to send her a little bit of extra money so that she’s not stressed out about paying for things. I set up automatic payments for a lot of her accounts through my accounts.

That’s the best feeling of all. It is kind of nice to be able to go to Trader Joe’s and just go HAM on snacks and not worry about it. But more than anything, I feel better about my life and my career when I’m able to give that back to other people. I cannot understand how a single person can have a million dollars in this world and feel like they need it all for themselves.

Some times we get so comfortable in Singapore’s affluent middle income life that we failed to notice that some of these spending that we could easily afford is a luxury that gives others very high job and satisfaction.

5. Buy Household Help

Astrophysicist Sara Seager’s first husband got cancer and died in 2011. She was working 60 hours a week and she had a child.

She is a professor at the Massachusetts Institute of Technology and is known for her work on extrasolar planets and their atmospheres. She is the author of two textbooks on these topics, and has been recognized for her research by Popular Science,Discover Magazine,Nature,and TIME Magazine. Seager was awarded a MacArthur Fellowship in 2013 citing her theoretical work on detecting chemical signatures on exoplanet atmospheres and developing low-cost space observatories to observe planetary transits.

A lot of the money is spent to exchange for time and help.

If you have kids, or a person who relies solely on you, not only do you have to take care of them and want to spend time with them, but you have to make their breakfast and their lunch, if they’re really little. And then clean up after them. There’s this endless series of chores. I got tons of responses from people saying, “I can’t believe you said that,” because people won’t admit that. People don’t want to admit the price you pay for working.

Because I was having to get up and go to my job and be at work, get my work done, and come home. You can’t have the job I have as a single mom without a lot of extra support. Maybe you have your parents living with you, or you happen to have extended family who live on your street, but you just cannot do this alone.

Then when she won the MacArthur “Genius” grant ($625,000), she spent the money on baby sitters, bringing the family on conference.

Without the MacArthur money, all my time was spent thinking about household problems, things I had to do. When you’re driving in your car, or you’re walking outside, or taking some time off, what are you thinking about? “I’ve got to get the laundry done.” Or, “I’ve got to get groceries.”

And this is what you would do if your windfall is on an insurance policy against your spouse.

The money is meant to cover the living expenses for the years before your child becomes productive.

If you have saved up a lump sum, you could view it as providing a cash flow so that you can get your family over the hump for 3 to 4 years.

Like Sara, Lydia Kiesling saw the windfall wealth that she got as a way to offset her daily living.

Lydia sold her book in 2018, The Golden State (2018) in San Francisco and got a low six figure amount. A six figure income might look big (debatable for the Investment Moats audience), but she got it in 4 separate payment over 3 years.

And each year, she has to pay 35-40% in estimated quarterly taxes.

She would put a portion of it into her SEP IRA, or her retirement account.

The way she looked at this lump sum, is as if suddenly she became a middle income six figure worker.

It just goes to her expenses:

So for three years I have a salary of some kind. It works out to having a job that pays $15 an hour, which is a minimum-wage job in San Francisco, where I live.

I was able to sell the book, so I was like, “Thank God I did it, I did the thing,” but basically we had been paying for childcare for my daughter in that time, and my Millions thing didn’t even totally cover that. My husband has a full-time job that covered rent and expenses; my freelance income mostly covered the daycare, but we had been kind of operating at a loss.

She explains how expensive it is to live in San Francisco (she described $117,000/yr as low income for a family) and how much childcare was pivotal in her writing another book.

6. Buy into a Wealthier Social Circle. Firewall against Financial Anxiety

We all fantasize about taking small bets, and those small bets giving us a pile of money.

Well for Bill Wasik, the deputy editor of New York Times Magazine, that happened.

In 1996, Bill was out of college. He didn’t know what he wanted to do. So he took on a low level research job that made investments in start-up tech companies. One of the advantage is that the firm allows you to make investments in companies the firm was investing in, up to $5,000 per company, per investments.

As he does not have any money, he have to take from the little money he made that time. So he would put $250 to $500 into companies.

3 years later, he moved to New York and worked as an unpaid intern at a magazine. It is during this point where those small investments started paying off. A $300 investment became $10,000. A $500 became $50,000. In total that came up to about $100,000.

$100,000 may not be super, but we have to see the context where Bill was. The people around bill was scrounging and making very little money.

Bill let us in on the money culture in New York during that time, and how $100,000 can be life changing:

At the time I came to New York, everybody pretended they had the same amount of money. Even people who you knew or suspected were very wealthy would act like they didn’t have wealth, and people who really were living close to the bone would still feel like they wanted to or had to come out and get beers, get a drink, and do things socially to the same extent as everybody else. Because of the money I made, I was able to live in a very expensive city and do the things that people around me were doing, without the feeling of anxiety that so many people had hidden—or didn’t hide—about money in an industry where nobody gets paid very well.

Bill was able to get access and network with people. If he didn’t have money, he would have to do what his peers did, pretend that he could afford it and put drinks on credit card debts to network.

You are not going to show it on the outside, but deep in the night, you are going to get haunted by that financial anxiety.

This networking allowed Bill to realize the real truth in this “bubble” as he called it:

Americans love to tell themselves lies about class. And of course, wealthy Americans like to tell the biggest lies about class. And I feel like having this money, it was like I was a secret trust-fund kid. I hadn’t grown up with that kind of money, but the fact that I got it in this weird and unexpected way wound up giving me insight into the bubble that people who have a lot of available money live in. I’d like to say that it made me realize how soulless it is inside that bubble. But in fact, it’s super nice inside that bubble. And I only wish that my own version of the bubble had been bigger, such that I feel like I could still be living inside it. But it doesn’t quite feel that way.

I would contend that this amount of money buys Bill a perspective of what people spent their whole life chasing early in life, let him see it as it is, and so that he do not spend his whole life chasing.

This is what some of my friends who grow up wealthy, or those that mixed with those more wealthy friends said. They are not like those you see on Instagram and such. They try to remain as grounded as possible, even though there are times they didn’t know their privilege.

Because they have access to a lot of what a lot of us is chasing all our lives, they discount those stuff massively because they know people overvalue them too much.

Bill also explained that the stream of cash flow generated by that lump sum windfall was able to let him patiently wait for the spot of editor to come up:

After I did the unpaid internship, I got a job as an editorial assistant at a magazine. And about a year into that, the other magazine that I had done the internship at said that there was an editor there who was going on maternity leave, and if I was willing to quit my job, I could come and be an editor there. I’d be on the masthead and get to do my own editing, but with no guarantees that when the other editor came back three months later, I would have a full-time job. And I did it. I think I never would have done that if I wasn’t sitting on a nice big bank balance. And lo and behold, that did turn into a permanent job. And it put me on a career track working at magazines that I don’t think would’ve happened otherwise.

This is the privilege of the more wealthy:

An external stream of cash flow to cover large part of expenses ==> You can focus on your craft/technical competency with less financial anxiety and distraction ==> Part of the process to get better to eventually earn a higher income ==> Greater and more valuable human capital.

7. Medical Help and Creating a Business at the End of Your Life, then Realizing Your Life Might not End

Perhaps one of the most fascinating sharing was by Sean Strub.

Sean was diagnosed with AIDS in 1985. And he is still around today. He survived HIV for 34 years. His case study will show you how you look at money when you do not have time left, and then realizing maybe you have more time left.

Sean got around $500,000 via settlement of viatical life insurance policies. Basically you know you are going to passed away soon, so you name another person as a beneficiary of your life insurance. In return, the person give you a sum of money that is much smaller than the payout.

It works for the other person because you are going to passed away soon. It works for you because you get the money needed for medical aid and enjoyment.

Sean took the money and started Poz magazine. He was tired of the information provided to people living with HIV that was invariably cheaply printed on newsprint not in color. He wanted to write about friends he are affiliated with.

His loved ones thought he is risking it by putting all his resources into starting a magazine that had a very uncertain future.

Sean reveal something that I seldom read about money: It is a different feeling :

- When you are going to die

- You do not have to worry of old age

- You do not need to think about long term financial security

- Don’t have a direct responsible to support people

Sean lasted longer than he and a lot of people expected. Combination therapy came out in 1996 and he got better.

By 1997 he realize he has been around for much longer than he anticipated, how long could he last.

I realize that had he been spending that money away frivolously to enjoy his end of days, he might not have the financial ability to live an even longer life.

Money can be an Enabler for Sensible Living

You can buy a fair bit of things with $10,000 to $200,000. In Singapore, you could top up a bit and buy a rather nice car. Great clothes, nice vacation can be purchase with this sum of money.

However, we can group what these folks do with their money into the follow categories:

- Taking care of the essential expenses. For themselves if not for others. This frees them up to focus and do the best work. And this builds up their human capital

- Buy experiences and education. Enables them to participate in activities that otherwise they cannot. Think 1 semester overseas study program. What they learn builds their human capital

- Capital expenditure for their business. Enables them to execute their plans to take their business to the next level

- Buying Joy for themselves or others

- Eliminate Distress

I reckon a lot of us would do 2 to 4 well. What we are less aware of are #1 and #5.

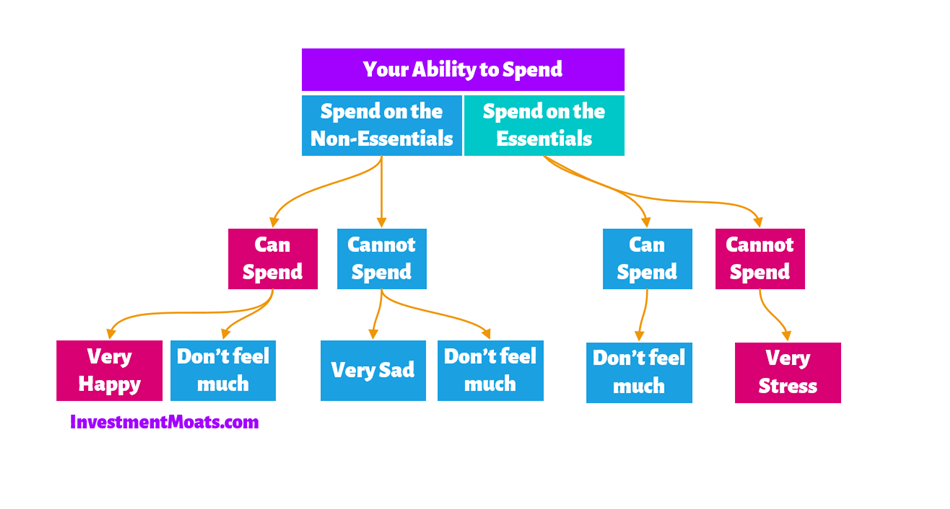

For each of us, every $1 can be used to be put away to some other delayed goal, or we can spend on essential expenses and non-essential expenses.

If we spend on each, we can be very happy, or not feel much. If we could not spend, we will feel sad or don’t feel much.

Due to the affluence of this place, we seldom do not realize that a lump sum of money is able to eliminate extreme financial distress or increase joy. The boxes marked in red is where we should allocate the money to.

Solve someone’s problem of not being able to spend on the essentials. Because this probably give them enough stress.

Help someone who couldn’t get some non essentials that you know will make them very happy.

There are some more windfall case studies that were not mentioned and you could check out the article to read more about it.

Now it is your turn. If you came across a story, or you have spent $10,000 to $200,000 and have benefit in unique ways from it, let me know in the comments below.

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

- The LionGlobal APAC Financials Dividend Plus ETF Won’t Give Singapore Investors 5% Dividend Yield Always. Further personal thoughts (with some data). - April 13, 2024