I received 2 questions on dividend investing and cash flowing for financial independence question and I would try to address them here.

These questions were sent to me as part of my organizing Investors Exchange 2018. And while I am not always in the best position to answer, I will try my best where I can.

Its even more awkward when the questions are on my friend B‘s The Evolution of Dividend Strategy presentation.

So here are the questions:

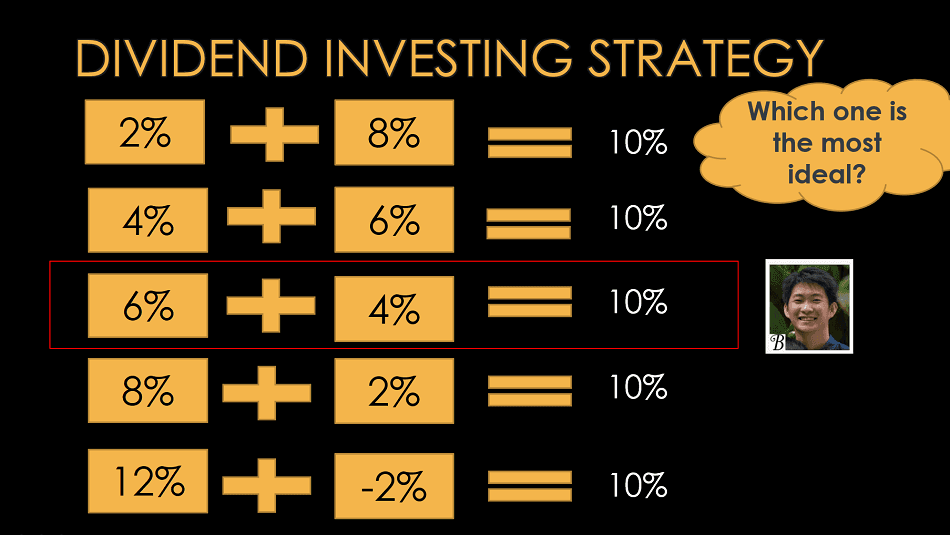

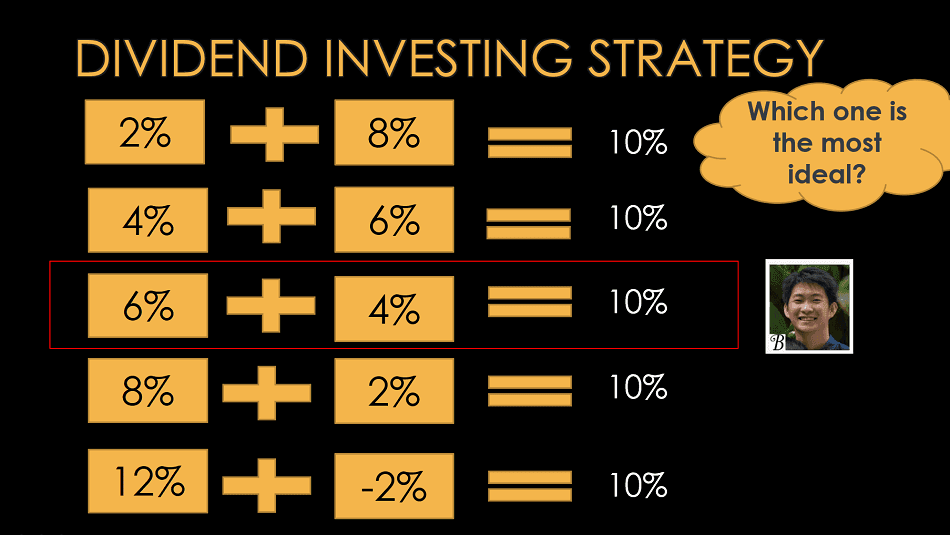

- Brian Halim’s strategy is to buy stocks with 6% Dividend and 4% Growth. Over what period is the 4% growth measured? That 4% will be past performance right?

- Brian Halim achieves FI when his dividend income matches his expenses. However his portfolio is 100% stocks. During an economic downturn, dividends might be affected. How can we handle that? If we switch to safer assets like bonds, the yield might not be high enough to match expenses.

I have answered the first question here in Expanding on the Growth in the 6% Dividend Yield + 4% Growth Dividend Strategy, so you might wish to take a look.

Here is the continuation to answer the second question.

Dividend Income Will be Volatile

We cannot run away from the reality that businesses will go through cycle where their earnings is going to look better, and their earnings is going to look worse.

When earnings are better the dividend per share is higher, and when earnings are not good, some companies will try to maintain the dividend, if the payout ratio is lower (meaning they do not pay out all their earnings as dividends).

Some companies will cut the dividend.

Part of B’s 5 dividend strategy, is for you to identify the nature of your dividend company.

If you look at those 2% dividend + 8% growth ones, 4% + 6% and 6% + 4%, these companies might not be so willing to cut dividends.

The payout ratio is low, the CEO have factored in the business will be volatile thus it is more conservative to pay out less, so that they are not going to cut it.

In contrast those that pay out more, like REITs who pay out nearly 100% of their cash flow, are subjected to cut.

Can you make a 100% Stock/Equity Solution and Make it Work in Financial Independence?

I think it is possible that you do not need to invest in bonds to have something like this.

1. Buy Low Dividend Payout Stocks, Covered by Sustainable Free Cash Flow with Good Fundamentals

There are some Legacy stocks, or stocks which we classify that can passed down to the next generation. They are likely to be manage by owners with vested interest, who happens to be good capital allocators as well.

These stocks could only pay a 3% dividend yield. However the dividend payout ratio is low at 30%-50%.

During recession, the share price might tank, or it might hold up.

But there is a high probability the dividend is not going to be cut.

Thus if you find 6-8 of these companies to form the back bone of your 100% stock portfolio.

If you need $25,000/yr in annual expenses, you will need $25,000/ 0.03 = $833,333 in your Stock Wealth Machine (What are Wealth Machines).

If you wish to be a little risk seeking, you could sell a little of your shares and boost your wealth withdrawal for your financial independence by 0.50% more.

How risk seeking will depend on the nature of the stock.

But if you analyze that these are indeed Legacy stocks which tend to lean towards more conservative, you could do something like that as there is a high likelihood that their asset value, or cash flow nature will bounce back in the near future.

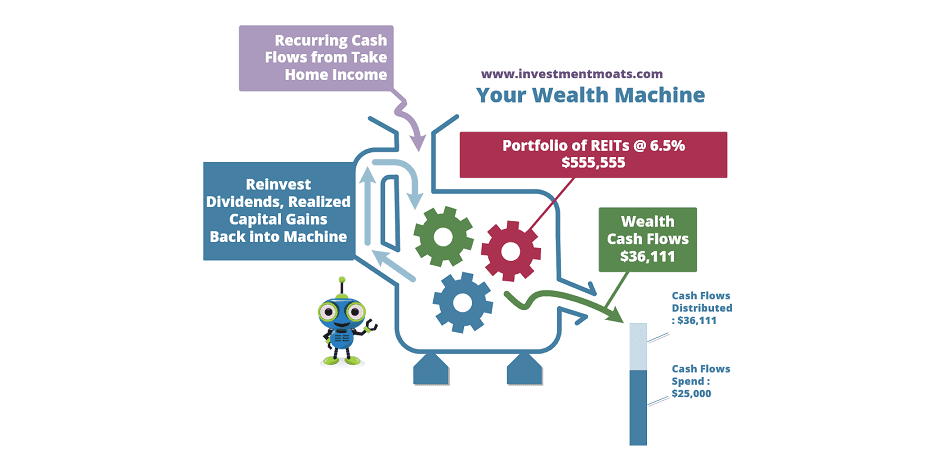

2. Big High Dividend Payout Stocks, but Ensure Your Spending is Well Below the Full Cash Flow Payout

If you prefer to choose stocks that pay a good dividend, you have to recognize that when the main street business is challenging, the business earnings get cut and so is your dividend.

Your way to shelter this is to be conservative in your planning.

Suppose you need $25,000/yr again.

Typically, your portfolio of 8 REITs give you an average dividend yield of 6.5% (you can take a look at my dividend stock tracker to know what is the average dividend yield you can achieve from common Singapore dividend stocks).

So how much you need?

A typical investor who wishes to make use of his portfolio to cash flow will assume that he needs $25,000/0.065 = $384,615.

That looks like an easy sum to build towards.

Unfortunately, if you been investing in REITs during this 3 to 4 years, you would have experience a situation where there are more supply than demand, falling rents and rising vacancy. The REITs have seen their rental income take a hit, and so have your dividend.

If you are planning this currently, when the operation condition is poor, assuming you could spend all of the 6.5% might be OK because the situation now is poor, and while the conditions could be worse, there is every probability the future would be an upswing. Your average REIT dividend yield might expand from 6.5% to 7%.

If you are planning this when the operation condition is good, and the average dividend yield is 6.5%, then its better to be conservative and assume a down cycle will come, and to spend perhaps 4.5% instead.

In this climate, you might need $25,000/0.045 = $555,555. That is $171,000 more.

You Need More Money

According to B’s model, which is not to spend capital, in the midst of increased downside volatility, don’t assume your dividend will not fall.

The reality is your dividend will explode downwards and also likely your dividend will exponentially increase.

By spending half of your dividends or 60-75% of it, it means to maintain the same standard of living, you need more money.

Your Spending May be More Variable

If your cash flow from portfolio is variable, you might be able to circumvent this by knowing that they can be flexible in their spending.

This is not very doable if all your expenses is being paid by the portfolio.

If your expenses is provided by a tiered system of an annuity + stock portfolio, you can be more flexible.

If you are flexible, you could spend all 6.5% of your portfolio.

If your average yield drops to 5.5%, you reduce the spending accordingly.

Switching to Bonds Reduces Volatility

And as the reader said, it reduces the yield.

The rate of return of your portfolio (dividend + capital growth) determines how much you can spend.

If bonds on average earns a lower rate of return, it means your average rate of return gets pulled down.

To be conservative, it means that you need more money.

Ok this concludes my answer to the second part.

Let me know if you have any queries.

My consolidated resources on:

- Wealth Foundation

- Active Investing

- Investing in REITs

- Dividend Stock Tracker

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money

Here is a small announcement.

My friend Christopher Ng would be speaking at a Kim Eng event on 18th Aug Saturday Afternoon. The topic would be on his take on financial independence, and how real estate investment trust augments your path to fulfill financial independence. The event is free and if you wish to sign up, you can do it here.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Lim

Tuesday 7th of August 2018

Hi,

Instead of merely looking at 'expenses' as a single monolithic number, you should divide it between stage 4 basic expenses, standard of living expenses stage 5, and life goals spending stage 6.

Achieve stage 4-4.5 Financial Security by ensuring that stage 4 is funded by cashflow from lower volatility assets like bonds and diversified ETFs. The average yield on these assets may not be that high (eg: 3%), but diversification should provide more stable cashflow and provide "security."

With a high degree of confidence in your stage 4 - 4.5, you can take more and more risk in seeking to reach stage 5 and then 6 for example, by investing in REITs and picking individual dividend stocks, so that you can reach stage 5 Financial Independence quicker.

(stages refers to your original stages of wealth, I find your new 11 stages too messy/complicated, and why would I want to quote a wealth model that says "F-U" to explain financial concepts to my loved ones and relatives?)

Kyith

Thursday 9th of August 2018

Hey are you the limster from hardwarezone? Didn't know you had a blog. Will follow it from now onwards. Thanks for coming over to leave your thoughts!

Thanks for explaining about the stages and the subsequent instruments that would work out. However, I do have reservations about whether we can break it up this way. If i read you correctly, it is as if we have a core bonds and ETF portfolio,2 individual tactical portfolios.

For this to work the bonds and ETF portfolio, will have a lower rate of return. For the withdrawal rate of 3%, you probably need more money than if you are a little risk seeking. the rate of return of this portfolio could be higher or average, but the idea is that you are spending a small amount of 3% and this might mean you need more. Of course since you are covering your survival expenses and not all of your expenses, this will not get to a stage where its like 1.8 mil for some people. if its $2000/mt, that will be 800,000.

the question is how much do we need to generate a higher amount for our stage 4.5 and above, at greater risk, greater volatility and greater return. it feels to me is that we gain more out of going through this portfolio construction exercise, then the actual practice. the actual practice is likely you boost your rate of return with more risk, but you are spending 2-3% on survival and another 1-1.5% if times are good and not that amount if times are bad.

Thanks for letting me know that the new stages of wealth is messy and could need parental guidance. It took me some time to come up with the terms, and maybe I would change it. But at that time, it is a term that more people can identify with, so you got to run with it.

Wing

Monday 6th of August 2018

My retirement plan is having a portfolio of stocks that consist of high yielding REITs and growth stocks to pay for my living expenses. To be conservative, if currently I am generating 4% of dividend from my portfolio of stocks, then I am planning the portfolio to be large enough to use only 2% for my retirement expenses and the portfolio can generally remain as is. Any inflation will be taken care by the CPF Life.

Eddy

Tuesday 7th of August 2018

what happens if there's rights issue for REITs? are you going touch your saving/emergency fund?

Kyith

Tuesday 7th of August 2018

Hi Wing, if I were to expand on your comment, the dividend yielding portfolio of average 4%, might be growing at a rate of return of 6% in total. Thus when you spend 2% it is being conservative. you do need a larger amount of money or keep your expenses low or flexible.but if the growth rate of that portfolio conservatively is 8-9% in total, then that is being conservative.

Sinkie

Monday 6th of August 2018

Ideally should have buffer of 50% i.e. save 1/3 of passive income & spend 2/3 of it.

Need to maintain emergency funds & warchest for stuff like home repairs, replacement of appliances / IT electronics, GP visits, deductible & co-payment for major medical, excess for car repairs, rights issues, etc.

And so far in the last 50 years, don't think there's much S'pore companies who won't cut dividends during recessions. Of such companies, there aren't enough of them to build a sufficiently diversified portfolio.

Kyith

Tuesday 7th of August 2018

You might not need to be restricted to companies locally. You could find companies in HK that does this. To a certain extend i disagree with having too much of a "warchest" for stuff like that. its money sitting idly and its asset liability matching.