I received 2 questions on dividend investing and cash flowing for financial independence question and I would try to address them here.

These questions were sent to me as part of my organizing Investors Exchange 2018. And while I am not always in the best position to answer, I will try my best where I can.

Its even more awkward when the questions are on my friend B‘s The Evolution of Dividend Strategy presentation.

So here are the questions:

- Brian Halim’s strategy is to buy stocks with 6% Dividend and 4% Growth. Over what period is the 4% growth measured? That 4% will be past performance right?

- Brian Halim achieves FI when his dividend income matches his expenses. However his portfolio is 100% stocks. During an economic downturn, dividends might be affected. How can we handle that? If we switch to safer assets like bonds, the yield might not be high enough to match expenses.

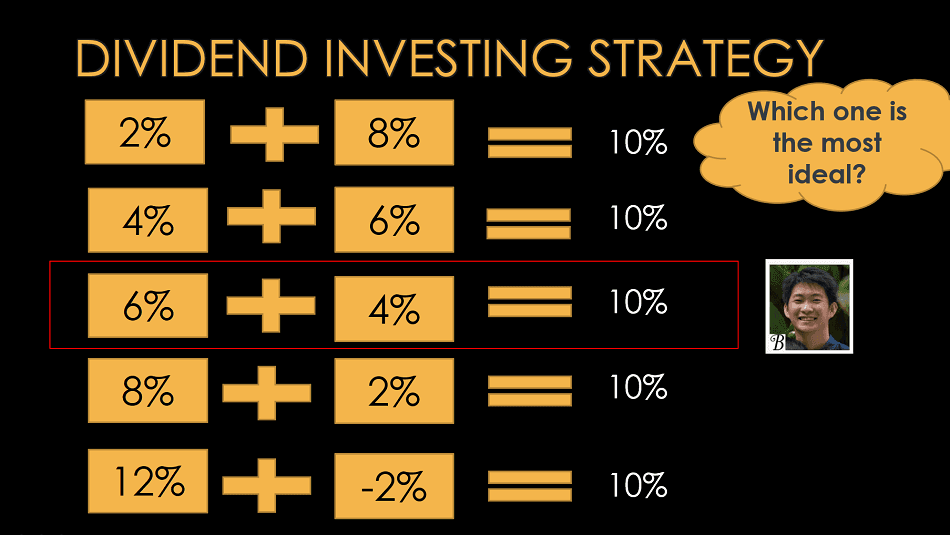

The 6% Dividend and 4% Growth Model

Think during the presentation, B shared with us how he frames and pigeon hole the companies that gives out a dividend into any of these 5 segments.

And then he shares their characteristics and one example on them.

The one he prefers the most is the 6% dividend and 4% growth strategy.

The growth in this case can refer to many things but in my opinion it has to be capital growth. This means that the net asset value of the business grows at roughly 3-5% per year.

When the net asset value grow, usually the share price will follow. (If it doesn’t then perhaps that stock is undervalue).

The other way is that the share price, or market capitalization grows at an average of 3-5% per year.

This is almost the same as my previous net asset value explanation. It just skips the net asset value, in that the market accords the stock to trade at a consistent 6% dividend yield.

If you look under my Dividend Stock Tracker, you can find that there are many stocks/REITs that currently gives a dividend of 5.5%-6.5%.

Let’s take the example of Ascendas REIT. It is a real estate investment trust, the biggest in Singapore that owns a lot of industrial properties in Singapore, Australia and now UK.

Its share price is $2.75 and the last dividend per share is $0.162.

So this gives it a dividend yield of $0.162/$2.75 = 5.89%.

According to B’s model, for Ascendas REIT to fit into this, it should grow at 3-5% and it is possible through a combination of:

- filling up the vacancy in a cyclical growth scenario

- acquisition

- organic rental growth

- asset enhancement

So suppose that you hold Ascendas share today at $2.75.

Come next year, Ascendas business did well and they were able to bump the dividends up by 10%.

So the dividend per share for next year is $0.162 x 1.1 = $0.1782.

Your yield on cost would be $0.1782/$2.75 = 6.48%. That is a pretty good dividend yield for a quality portfolio, big sponsor and quality management team!

However, the price usually won’t stay at $2.75, if the dividend is able to improve by 10%. The market participants will buy and sell, buy and sell and eventually the prevailing share price will make Ascendas REIT trade at 6% dividend yield again.

Since the dividend per share now is $0.1782 and to make Ascendas REIT trade at 6% again, the share price would need to be $0.1782/0.06 = $2.97.

So how much did the share price change? ($2.97-$2.75)/$2.75 = 0.08 or 8%.

So you get a 5.9% dividend yield and a 8% capital growth.

Is Ascendas REIT always going to trade at 6%?

Not always.

We can tell this if we track Ascendas REIT’s historical dividend yield.

The above forward dividend yield graph is taken from a CITI analyst report.

We observe that over its 15 year history, there are times when the mean is closer to 6.2%, sometimes 6.6%.

The market does not always value Ascendas REIT on the spot, but would gravitate back and forth to it.

The market valuation of Ascendas REIT will always change as the REIT’s quality changes:

- Improvement in portfolio of properties

- Improvement in management

- Changes in the risk free asset rate. If Risk free asset is more attractive, that would affect Ascendas valuation

- Investor sentiment. If investor is panicky, then it might not always be this band

So this is how growth or deceleration happens. The gyration of dividend per share and the share price. 2 items that are affected by business fundamentals (dpu) and market forces (share price).

Is the Growth Past Performance?

The answer here is no.

It should be forward looking and into the future.

This is because why would we be investing in the past? We should be investing in the future.

Thus B’s 4% is based on his analysis of this particular business, how its growth trajectory is likely to be in the future.

To find its future growth, we have to look at the past performance to understand its nature.

That is not enough.

You have to look at the market in general going forward and mesh the past and market together.

In Ascendas case, real estate goes through period of boom and bust, and because the properties are in different geographical regions, we have to see the near term or far future of 3 different markets (Singapore, Australia and UK).

If we want to position for 4% growth, these markets, their production manufacturing, should be good. Otherwise why would we put money in an investment where in the past it shows that it grows 4%/yr but in the future the growth is -2%/yr?

B: A Quick and Dirty Way to Forecast Forward Returns in the Near Term

Probably what was lost in the translation while I was typing this reply out is that each of these 5 dividend strategies allow you a quick and dirty way to pigeon hole the likely return of the company in the near term.

The idea is that, you do not know what kind of total return you are going to get. You pair a sustainable, recurring dividend, with the appropriate near term growth rate.

This growth rate can come in different ways on inspection:

- The existing GDP growth, country production growth as an organic baseline growth rate

- Increase in orders, sustainable margins over the past year

- New asset purchases that will increase recurring cash flow that is not factored into the news

- Potential fix to long standing problems

If you can approximate the revenue, the margins and the cash flow, you can see the bump up.

Thus it lets you see whether the stock is priced reasonably for the risk and for speculation.

Ok this concludes my answer to the first part. Got to get to work.

Let me know if you have any queries.

My consolidated resources on:

- Wealth Foundation

- Active Investing

- Investing in REITs

- Dividend Stock Tracker

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024