Since the 2007-2009 recession, countries around the world’s interest rates were lowered to very low levels to stimulate each countries’ economies.

Many economies have recovered, but some have not. But the common trait is that around the world inflation have creep up. Sooner or later countries have to increase the interest rates to combat that.

When it comes to Singapore REITs, most of the reits survived and more properties have been securitized as REITs.

The one advantage taken by REITs is to re-finance debts at lower interest rates. Not able to re-finance debts was a big problem for REITs during the credit crisis.

Pros of rising interest rates

When interest rates rise, it generally also means that the economy is growing.

- Rent revision up

- More yield accretive assets

- Current Assets rise in value

- Rising interest rates reduces the propensity to build new properties thus reduces supply

Cons of rising interest rates

However, there are more negative aspects as well

- Maintenance cost rises

- Property costs rises

- Debts are re-finance at higher interest rates

- Rising floating interest rates reduces dividend payouts

- Rising interest rates reduces the propensity to build new properties thus reduces supply

Rate of rise in interest rates

Much of whether rising interest rates is good for REITs or not really depends on how predictable the rate of rise.

If the rate of rise is slow and predictable,

- Rent revisions greater than rising property expenses result in increase dividend payouts.

- Economy expands well and provides opportunity for most REITs to correct their mistakes and make use of the opportunity.

- REITs are able to revised rent higher or make good acquisitions as compared to lower-risk financial assets.

If the rate of rise is too fast and unpredictable,

- Rent revisions could not keep up with other costs

- Re-finance of debts at much much higher rates cuts dividend payouts

- Lower-risk financial assets become much attractive compared to REITs. REITs price would have to revise down to stay competitive.

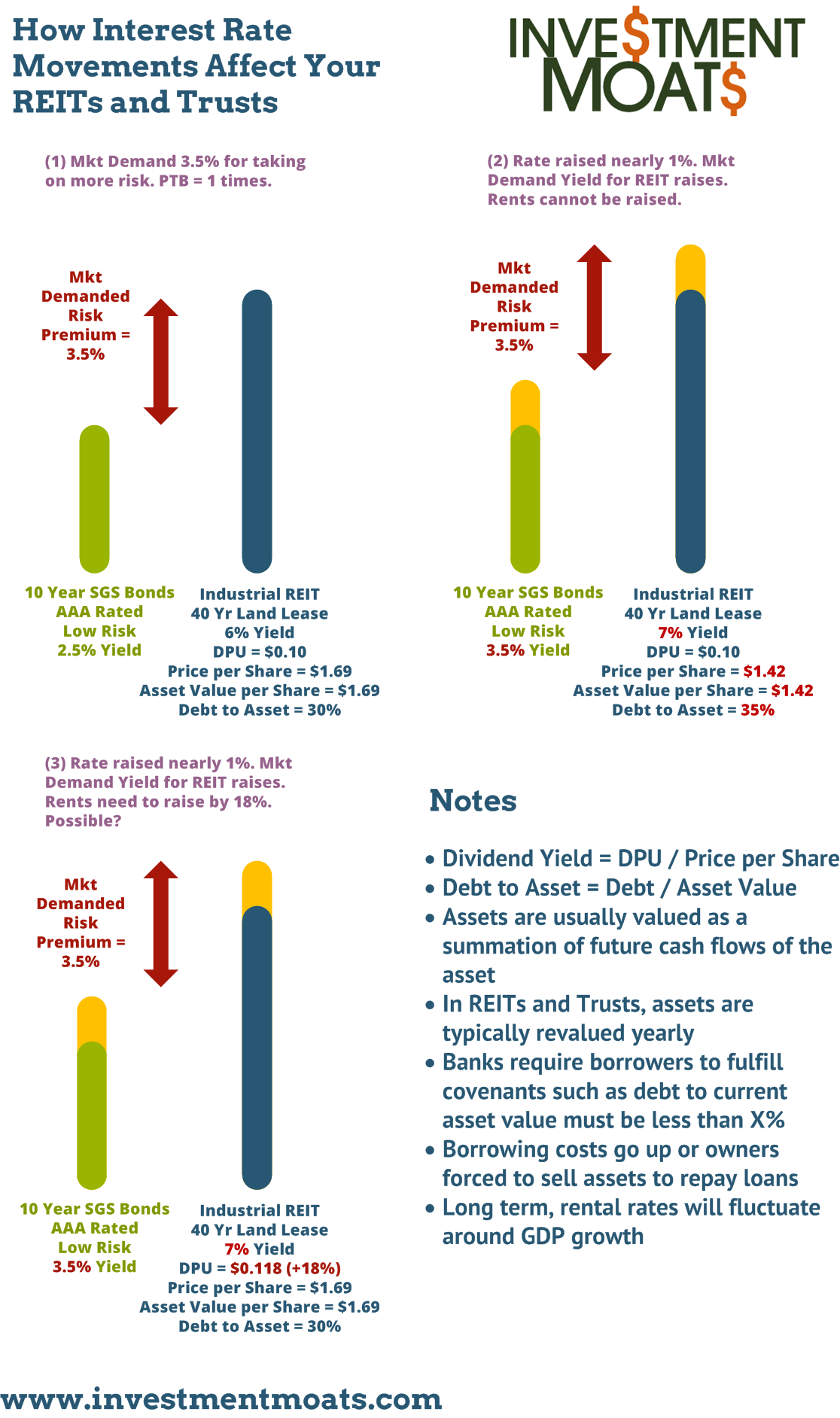

How Interest Rate Rises Will Negatively Affect Leverage and Stock Price

An easy way to illustrate the concept is in the Infographic below

Conclusion

AT the end of the day, every manager that is competent to run a REIT should be aware of these factors affecting their business.

Good managers will navigate challenges like this well and profit from it. Bad managers are reactive to them and will likely be detrimental to share holders.

We saw during the last recession that even some large REIT who have strong sponsor backing did worse then smaller REITs that are more prudent.

As investors it is our decision to discern those REITs that can profit in such an environment and are managed well.

I run a free Singapore Dividend Stock Tracker . It contains Singapore’s top dividend stocks both blue chip and high yield stock that are great for high yield investing. Do follow my Dividend Stock Tracker which is updated nightly here.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Edmund

Saturday 14th of December 2013

Hi Drizzt, great article and this gives a lot of confidence to REITS investors like myself. Thanks for posting good articles.

Kyith

Sunday 15th of December 2013

i dont think i did much. i think the message is to be more realistic about things like value rather than yield.

Marti

Saturday 7th of May 2011

This is why I prefer REITs with low gearing: interests can only go up from where they are now, and this will eat into DPU. That and I get higher peace of mind when thinking of a possible new credit-crunch...

Drizzt

Sunday 8th of May 2011

Hi Marti,

I believe whether highly geared or not the difference in interest servicing between REITs may not matter that much. But there could be a diff if rates start to rise and different REITs' debt financing is different. those that are on floating would be adversely impacted if not hedged well.