Keppel Infrastructure Trust (KIT) is the merger of K-Green and Cityspring in the past.

K-Green is very clean, no debt but its assets are concession based and the highest contributing had a concession of 10 years. Cityspring turned out to be 50% leveraged and didn’t performed as what retail investors thinks it should.

Worse, they made an acquisition in Basslink in Australia that was nothing short of a disaster.

So the merger of K-Green and Cityspring helps both sides, in that it gives the entity a “longer WALE” and less leverage.

KIT just announced that they are proposing to shareholders to acquire IXOM a chemical specialty company in Australia from Blackstone Group for A$1.1 billion dollars.

The transaction itself is not going to be very yield accretive, given any of the financing methods.

However, it does help the business trust reduce its dependency on some concession based source of cash flow. But it does not hid the fact that there are some returns that are based on return of capital then a return of capital.

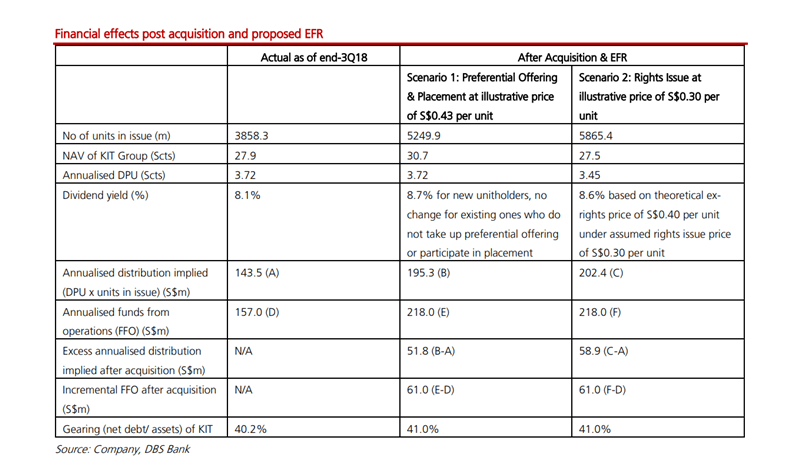

KIT does present itself with an attractive 8.1% dividend yield.

It will leave KIT with a net debt to asset of 41%.

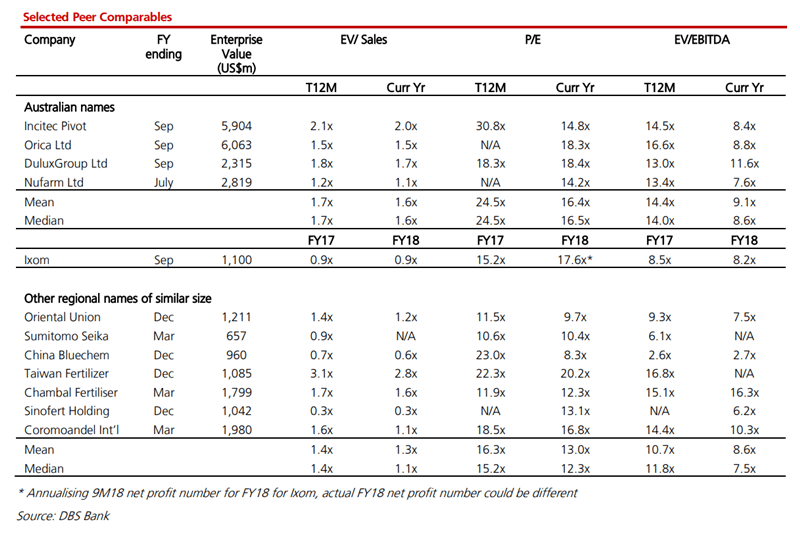

Acquisition Price do not look Overly Expensive

The first thing that I noticed is that at 8.2 times EV/EBITDA, this acquisition does not look too expensive. And given that it looks like a perpetual business, it looks an investment that I am more willing to fork out money for, as a shareholder, rather than one that is a limited concession again.

Then again, shareholders of KIT is not getting any bargains here as well, as majority of the peers are trading at a mean or median valuation close to them.

Buying form a private equity group, who needs to hit a hurdle rate of return, often does not sound like you can get a good proposition so I am not sure why Blackstone Group would wish to sell Ixom.

Back in 2014, Blackstone group acquire what would be Ixom from Australian mining and explosive company Orica for A$750 mil.

Ixom became their cornerstone investment, in their venture into Australia.

Orica, had a motivation to sell because they were facing some challenges in their core business and selling the chemicals business (which became Ixom) would allow them to do a massive share buyback.

It has been almost 4 years since then, and Blackstone was shopping Ixom around for at least A$1 bil.

This sale would have netted them 10% CAGR.

I do wonder how recurring this business is. I do like that its a capital intensive business that might not be so easy to replicate.

Ixom is:

- Sole manufacturer of liquefied chlorine in Australia from what management estimates

- Number 1 chemicals manufacturer and distributor in Australia and New Zealand

- Number 1 distributor of manufactured caustic soda in Australia and New Zealand

The chemical products are mainly used in treatment of water, as well as specialty chemicals in a few industries. Their customer base is wide such that no one customer makes up more than 6% of their income, well spread out among the industry.

And since their customer consistently need these chemical supply, they need an infrastructure base to make, store and distribute. This is not easily to replicate.

Cash Flows might not be that steady as we think

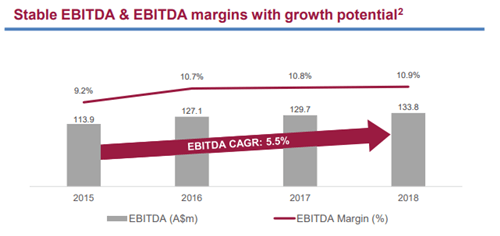

In KIT’s acquisition slides, KIT listed the past EBITDA trends. Since Blackstone took control in 2015 and made this their cornerstone Australian asset, the EBITDA growth was 5%/yr.

Per Australian financial review, potential buyers was told Ixom would be making A$133 mil in EBITDA in 2018 and A$139 in 2019.

Now I wonder whether the EBITDA or EBIT would spring some surprises down the road.

I do not have an issue finding out the nature of the cash flow prior to 2015.

I just need to take a look at Orica’s annual report.

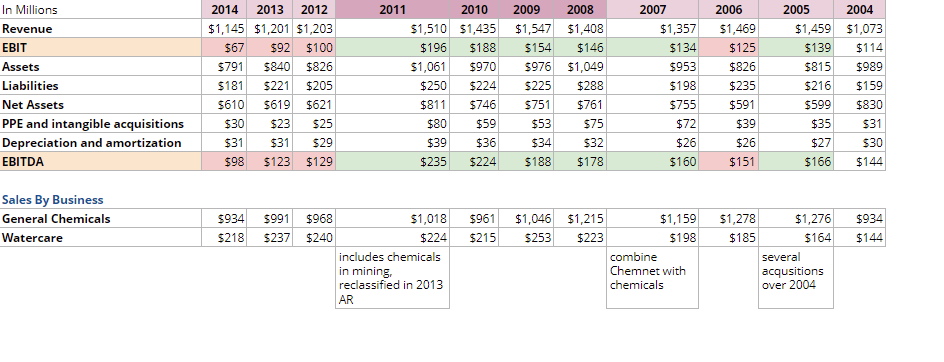

I have gone through the report and tabulated some of the financial data. There were a few periods that gave me some grief as the EBITDA looked funny. 2007 was the year where management decided to combine their specialty chemicals Chemnet into the chemicals segment. In 2013, Orica reclassified the chemicals in mining from chemicals back into their mining segment.

I have gone through the report and tabulated some of the financial data. There were a few periods that gave me some grief as the EBITDA looked funny. 2007 was the year where management decided to combine their specialty chemicals Chemnet into the chemicals segment. In 2013, Orica reclassified the chemicals in mining from chemicals back into their mining segment.

From the data that I see, it is not as if the mining chemical outperformed the other chemical business. I think this is because they do see that aspect of the chemical business to still be strategic in their service delivery.

If we focus on the EBIT and EBITDA the red cells mark the years where there is a decline in EBIT and EBITDA.

Coincidentally. it was 3 years before they sold off to Blackstone group. 2014 saw a big plunge but I feel that my data could be “tainted” by some one off write downs because another source showed otherwise.

From 2004 to 2011, we are able to see the data where Chemnet and mining chemicals was integrated. While revenue was very very stable, there is somewhat some growth in the EBIT and EBITDA.

It is also interesting that during the financial crisis, the business was pretty stable.

Business was not well from 2012 to 2014, and that might make it a rational decision to sell the chemical segment off, take the money and use it better.

But I do wonder, is it that Blackstone is just a better manager than Orica and therefore they can achieve a much splendid CAGR the past 4 years?

This would mean that if Keppel could not keep the management, they would really need to dig within their own resources to find a management team to keep this up.

The following are snippets taken from operation review, during those years where things were challenging. I hope that this would add some color to the nature of the business:

2006

Chemnet profitability down 26% due to ongoing difficult trading conditions. Restructuring program commenced in April 2006.

Sales down 4% due to slower conditions in Australia and New Zealand. EBIT declined due to lower volume. Key customers carried out aggressive cost cutting, including direct sourcing some of their materials. Bronson and Jacobs lost volume and market share.

Chemical services sales was up 13%, if we exclude acquisitions due to strong performance from mining chemicals.

Watercare have strong sales growth due to high caustic soda prices. However volumes was down due to lower industrial consumptions.

Mining chemicals volume was up 28% due to growth in gold productions. Pricing improved due to lower margins but higher volume.

2013

EBIT was down 8% due to subdued conditions in most industrial markets in Australia and New Zealand and increase competition. General soft demand in Australian construction, manufacturing and agriculture industries.

Performance improved in the New Zealand chemical business. Growth in Latin American construction markets and improved sales of industrial chemicals.

Watercare sales lower due to lower global caustic soda prices and increased pricing pressure from competitors.

2014

EBIT down 29% due to write downs and restructuring costs of the Latin America. General Chemicals Sales is down 6% due to lower volumes from mining, agricultural and plastics sector in Australia and reduced revenues in Latin America. New Zealand sales improved due to increase demand in dairy, pulp and paper sectors.

Watercare sales is down 9% due to reduced demand in global caustic soda pricing which stabilized at lower levels.

I think we do not see large one time capital expenditure and depreciation is rather stable.

While I have highlighted the downside in EBITDA volatility, you could also see that potentially, cash flows could grow as well.

Summary

I think that is a lot of work just to understand whether a purchase is good or not.

However, I am glad to do this as I always thought chemical business is damn volatile. However in the case of Orica’s data, the cash flows can go up and down, but due to their advantage as stated, their cash flows are rather recurring.

The method of financing have not been finalize but I thought the dividend yield is rather attractive at 8.6-8.7% post PO or rights issue.

As a package, I think there is a reason why KIT is trading at a high yield:

- its gearing is rather high

- while many of its assets are recurring but their cash flows can be volatile

- as explained, part of their assets have limited concessions

A fair dividend yield for this should be at 8% for the nature of this business. While I think it is undervalued, I think there are other things that are undervalued as well. So pick your high yield investments carefully.

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.