My co-worker told me he is leaving our office shortly in the next 2 weeks. (for context this article was first posted in April 2018, when I was with my old company)

I will address my co-worker J, just to preserve some anonymity.

A person leaving our office is not something new.

I work in a place where most of us are deployed here from different companies to work in different projects for the same organization.

Due to the pay-scale that on-site staff commanded, and the mismatched in aspirations and the scope of work, we will see turnover a fair bit.

Some of the other reasons for the turnover are projects were short. Some found better employment opportunities. Some don’t like to be attached out and be away from the main office because this reduces their visibility, and hence career progression. Some work in scope that they do not like. Some do not like being in a contract role.

I was rummaging through my cabinet, looking for that hard disk I was suppose to bring on site to replace but not sure if its still there (lucky it was!) and casually, I asked J where is he going to next.

J told me he is not joining any company.

He is not going to work after this.

I froze there for 2 sec, looked up and ask: “What do you mean by you are not going to work?”

He replied,”There is only so long you can spend your time earning money. I have earned enough so I am taking a break.”

Most people might just leave this like that, thinking this guy must be a bit screw loose.

However, J didn’t realize his co-worker writes a small blog, sometimes talking about the topic of wealth, financial independence and stock investing.

I just realize someone beat me to it! This is so fascinating!

I could only get my chance to ask J a few days later: “how much is enough to retire?”.

This lead to 2 conversations how it was all possible for him.

What Motivated Him to Wanting to Stop Working

J told me that if you have a goal of not wanting to work, you have to plan for it.

It won’t take place immediately for you.

He had this idea 15 years ago. That was back in 2003.

He was single then, and still is and living alone now.

J is around 45 years old now, so this idea was seeded when he was 30 years old.

He have been working in a different field back then, and got really frustrated about working.

I asked what pushed him over the edge.

J said he had a friend who asked him “how long do you want to keep working?”.

J said he doesn’t want to work forever.

His friend asked him “so what are you going to do once you stop working?”.

J said he would start his own business (Kyith: this is something I heard from a lot of people as well!).

His friend then ask him what kind of business would he do and what kind of competency does he have.

J realize that he has no clue at this point.

Back then, J probably have worked for 8 years and he was pretty much drunk on most days.

His friend told him that if he continue his drinking ways, he would not only develop more health issues and also he would spend the rest of his life working.

That was the main motivation trigger.

The thought of not liking work, but to be forced to work indefinitely is a scary image in his mind.

So he asked his friend what could he do?

How much Wealth does he Need to Retire?

J’s friend introduce him to some of the ways he could build up his wealth.

Particularly, he made J understand that how much wealth he needs is a function of his annual expenses.

When J got a feel of his annual expenses, he will have an idea how much wealth that he needs to retire. (I didn’t probe much about the exact amount that is required, if that is what you are interested in. Sometimes, I think what people needs might not be a concrete number but a rough target that they conjured up)

I could sense that J has a grasp on his annual expense. He explains later on some of the break down of how much cash flow he needs in his retirement. In order to do that, you have to have certain awareness of how much you been spending for the past few years.

You realize that whether its from Investment Moats, or another place, the equation of how much is needed is not too different from what I wrote about.

How did He Built up his Wealth?

Prior to 2007 or the first 13 years of his career, he has been rather frugal.

So in that span, he has saved up $100,000 at least.

It was during this point that his friend (the same friend who introduce all these to him) ask him for capital to invest. This friend does not have capital, and he knew J was rather good at saving.

His friend proposed a 50%/50% profit sharing. J seeded him with $100,000 in 2007.

His friend grew that sum to $300,000 in 1 year. (I suppose the time line might be a little messed up. That was during the start of the financial crisis. Either he did such a good job shorting the market during the market draw down, or that the money was made from 2009 to 2010).

So his friend kept $100,000 and J have $200,000 now.

So I asked J did he continue to put the $200,000 with his friend.

J said that, since he didn’t have capital initially, now that he has capital, he does not need J’s money any more.

I asked J, so what happened next?

Since his friend could not do it for him, he had to go back to diligently saving.

So in the next 8-9 years, he saved another $100,000.

In total, his sum is around $300,000.

Would $300,000 be enough for him to Stop Working?

Would this $300,000 be enough? I have seen older folks retire with less than that.

My philosophy on how much is enough is: The sum itself is meaningless.

It depends on whether a person, or a couple can see how functional this $300,000 is in front of their eyes, or in their heads clearly.

I asked J why does he think $300,000 is adequate.

J told me: “You have to know your ideal living condition in retirement. This means the type of lifestyle that you can accept.”

For him, his monthly expenses is $500/mth. This worked out to be $6,000/yr.

“If I am careful with my money, this amount could last me 50 years. Of course this does not factor in inflation, so the amount that it could last is probably less. Given my age of 45-46, it will be when I am rather old before it runs out”.

“With more time on my hand, I can look to invest in blue chip dividend stocks that pay me 4-8%/yr”.

I helped him do some of the math, and realize with $300,000, he could generate between $12,000 to $24,000/yr.

That looks to be enough if his current first year retirement expenses is $6,000/yr.

But how the hell do you survive on $500/mth??

People will be incredulous how they can do it, even for those who tracked their expenses. Kyith is also surprised. I seen some crazy budget from acquaintance.

The lowest that makes the most sense is that of my friend Daniel Tay, who has been the news for his Freegan exploits (you can read Freegan, Dumpster Diving and Financial Security)

Daniel was able to spend less because all his cost are the fixed costs of life such as adequate insurance, fees for housing and conservancy, utilities. He doesn’t spend on food since he gets his food sources for free.

I asked J how its done. It is only then that I realize that the $500/mth are for the fixed expenses.

What he would do is to find unstructured work, part time work to cover his food expenses.

In my dictionary, that is not “retiring” but somewhat of “semi-retirement” but I don’t want to spend time discussing about these semantics with him.

How Tough was it to Consistently Put Away Money?

Working backwards, to save $100,000 over 8-9 years would require putting away $925 to $1040/mth.

I assess the earnings power of the folks in my office.

The folks older than me probably earns close to middle income. Those younger slightly less. Its not an environment where you will see the envious earnings power of financial bloggers.

If you earn more, have less commitments, $100,000 is not hard. Given, what most in our group come to terms with, putting away this much is remarkable.

J tells me its not that difficult, you just got to make life simpler.

You Need to Secure Your Dwelling Before You can Stop Working

The three biggest expenses for most people are the cost of dwelling, transportation and food.

I do consider in Singapore dwelling and food is a large part but if you take public transportation, this is much manageable. If its for the family, it could add up.

To retire, J would have to secure a place.

Usually, a single would live in his/her parents place but at some point they would have to be independent and get their own place.

For my co-worker, he manage to get a 2 room BTO somewhere in my neighborhood.

I knew this some time ago while one of our short conversation veered towards that direction.

The balloting for 2 room BTO is a bit crazy so its a good thing he manage to secure it. He also shared with me a trick to increase the chances, which I will not say, not because its some deep secret, but that I do not know how true it is.

A two room BTO with grant, or without grant should be affordable for a single who have worked 20 years in their career.

With a possibly paid off flat with a long lease, all the stars are aligned.

Here are Some of My Thoughts on My Colleagues Situation

Its debatable whether J’s plan is a foolproof plan.

When I see a discussion on retirement, many would mention the follow things they are worried about:

- the future rising inflation costs

- other unexpected/unforseen things that comes a long that adds to what they need

- if you return to work, you will not command the same level of salary, or become unemployable

These are valid concerns. I do challenge that many stopped here and didn’t push further to find out “how much additional would I need to set aside?”

The answer might tell you, you can still make it.

We have to make sure we understand how to think about our concerns, and how do we find out if there is a real concern there.

I think there is definitely some things to think about, and as I did not wish to reveal too much, I didn’t probe him through these common questions.

All the above would affect how much wealth assets you need to prepare for retirement, or semi-retirement.

The Importance of Being Comfortable with Your Investing Method

When J’s friend left, he did not have a fall back plan.

J did not have another wealth building method that he trust enough to deploy $200,000 to.

This is what I called a lack of required wealth building competency.

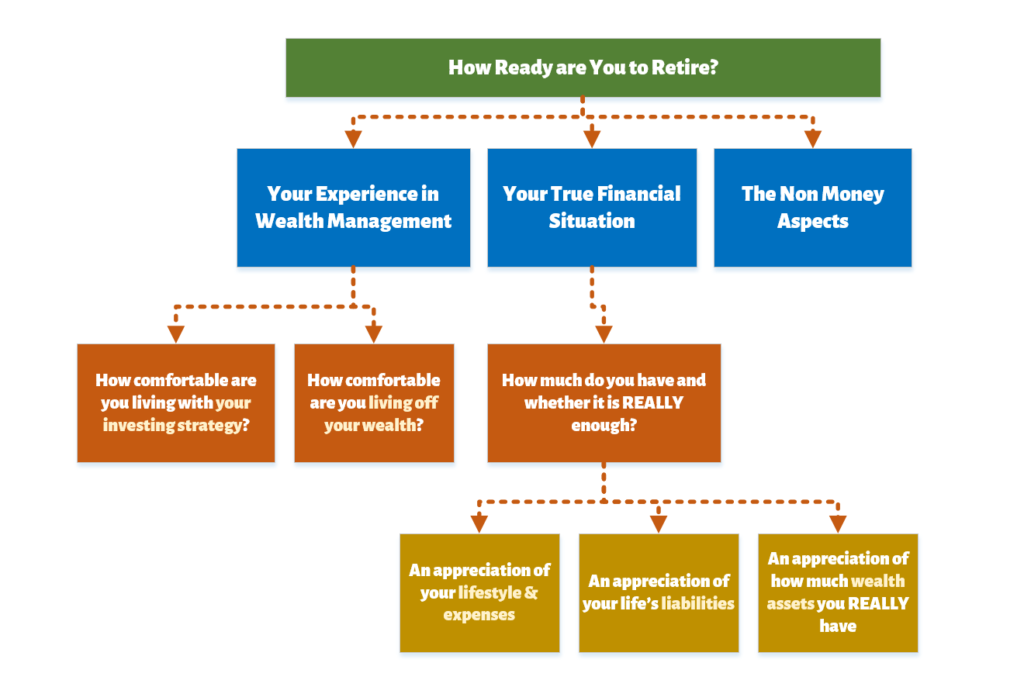

In my article about finding out whether you are read to retire, how comfortable you are at living with your investing strategy features pretty prominently.

When you do not know much other ways of building wealth other than owning properties and fixed deposits, you may never got far enough to explore the potential of wealth assets.

I do find messing with these investing stuff at a young age helps. It allowed myself to figure out which method worked better, which absolutely not.

When I have more money, I have already build up that competency along the way.

I find it worth emphasizing again is the need to:

- understand how wealth is built (can take a look at my building a wealth foundation segment here)

- learn about some different financial assets, their returns, their risks, their characteristics

- equip with competencies to build wealth in a sustainable manner or find the right people to delegate to

When J’s friend made his capital, suddenly the great growth wealth machine was cut off.

If you have some overall understanding of bonds, bond unit trust, equity unit trust, stocks, exchange traded funds, REITs, insurance savings plans, you would then be able to relate so if I am able to generate 5% return, I can grow my money to XXX in Y years. This may be enough for my retirement.

In my observation, people only start having that intent to build wealth only when they are triggered emotionally, or when they really needed it. The problem is that you cannot squeeze battle experiences, technical competency in 1 year.

If you have never invest, could you immediately know how to create a portfolio that yields 4% a year? How much diversification do you need to reduce the non-systematic risk?

I thought this is challenging for those that have invested for 4-5 years, its even more challenging if you need the wealth assets to be functional immediately.

Given all this, I think its remarkable for J to pull the trigger.

I think it will be remarkable if any of the people in my office is able to do it within 15 years, so this is something to be impressed about.

Some never got round it because they know too much, considered too much and never got round this. Perhaps due to my many years in projects, I belong to the school that you can try to find out all and plan as much as you can, but plans will go crazy and its up to you to make the best of the situation.

The thing that I was most impressed with is that it is one thing to listen to someone giving you advice on how to do it, and another to really carry it out. And its pretty challenging staying the course, quit drinking and working towards that vision when your salary is not that high and volatile.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

SeekingPrivateReturns

Monday 9th of April 2018

I did a double-take when I read the part where the friend gave $100K to his friend to invest. Very brave of him!

Kyith

Wednesday 11th of April 2018

It is very brave and not many people can do it. but it is also a flaw in a certain way.

kehyi

Monday 9th of April 2018

One common theme i've noticed for those who attain FIRE: single & living alone ...

Kyith

Monday 9th of April 2018

Not really. There should be some that is couple based. Der Shing who co-founded Jobs Central and sold his company is one with a lot of kids.