Annuities is a financial instrument normally sold by insurance agents with the view of taking a lump sum from you in exchange of returning a fixed sum of money every month.

In Singapore, the most common annuity that we come across is our CPF Life. It is very unpopular and people seem to think it is a way the government refuse to let us take back our money.

But for me it does have its use, just that people find it hard to justify whether they are getting a good payout our return out of it.

The rate of return of annuities

To calculate the rate of return we can use an IRR excel formula to help us. I have come up with a easy rate of return calculator here for you guys to play around. Make a copy of it if you have a Google account. [Calculator here >>]

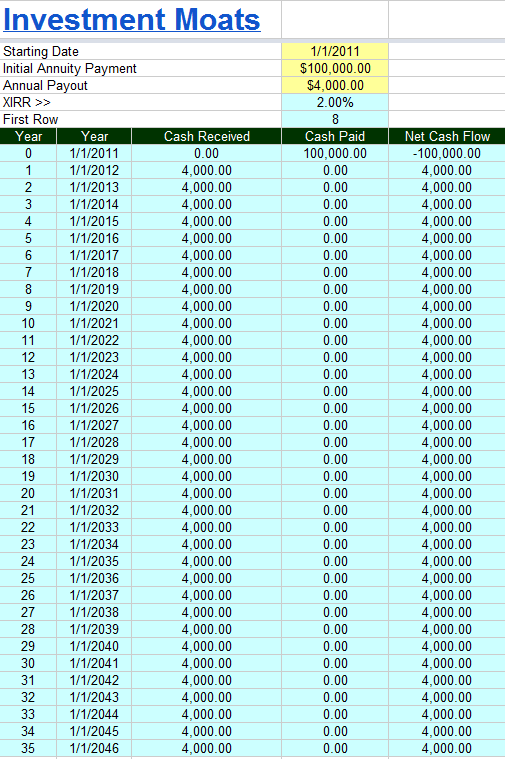

Lets say we have Jack who has $100k and would like a yearly payout annuity. He buys an annuity with a yearly payout of $4k. What is his return like?

If Jack lives till the age of 100 years old, his rate of return from his payout would have been 2%. That sounds low, but I suspect that is the prevailing annuity rates.

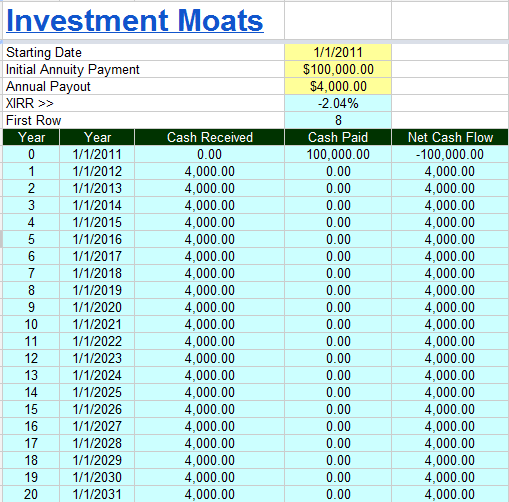

However had Jack not live for so long but till 85 years old, his rate of return would be –2.04%. This would mean that he is getting less than what he originally payout.

Longevity Insurance

Given the risk that you would not outlive to see a good payout, why do you still buy it? For one thing, this is a bet that medical science will improve to the extend that life expectancy will go up and that you may outlive your income stream.

Annuities would provide a fix payout.

Hyperinflation

Should at the age of 66 onwards, the world experience higher than expected inflation, what is going to happen is that your $4k payout will not keep up with inflation, which is the same as bonds.

In this scenario, perhaps investing in a core group of companies that have a track record of raising dividends and increasing dividend payouts may be a better option for retirees since their payout from dividend will have a likelihood of keeping up with inflation. [Read dividend investing historical returns >>]

The opposite can be said that had we have a 18 year cycle of deflation, your annuity would have done better.

How do insurance companies fund these payout

This got me curious about why there are advertisement claiming 7% income guaranteed payouts.

The Aleph Blog is a blog I read often. This guy is a bond guy but his posts are well written and really useful for the average investor. Do bookmark and read what he writes if you can.

In his latest post on annuity, he opens up how this high return can be achieved:

So why the difference? Immediate annuities work off of the idea that a lot of people will die, and money from their annuities is reallocated to the living (minus a profit for the insurer, on average). The insurer earns 4.5% on its investments, and additional money of 3.5-5.0% from deaths of annuitants supports the payments of those living, with 1% to cover commissions, administration, and profits.

So, they advertise that they are paying you 7-8%+, when they are really paying you 4.0-4.5%, and exposing you to the risk of inflation, because that payment will never rise. Ask them for payout levels on inflation-adjusted immediate annuities, and watch your jaw drop as you see how relatively low the payments are.

Conclusion

Given the bad press in general about CPF Life, I do find that this is a logical promotion by the government of Singapore. For the investment savvy, my take is that you should not totally rely on annuities.

Building up a nest egg that keeps up with inflation at a low cost to supplement your CPF Life annuities.

To get started with dividend investing, start by bookmarking my Dividend Stock Tracker which shows the prevailing yields of blue chip dividend stocks, utilities, REITs updated nightly.

Make use of the free Stock Portfolio Tracker to track your dividend stock by transactions to show your total returns.

For my best articles on investing, growing money check out the resources section.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

jack

Wednesday 31st of October 2012

good effort to write. an annuity is a hedge for longevity risk. You should emphasize more on the financial strength (default risk) of the insurer firm, not on 'returns'.

Drizzt

Wednesday 31st of October 2012

hi jack,

thanks for highlighting the shortfall in my analysis. it is true that should you expect certain payments indefinitely the financial strength of the institution becomes an important factor.