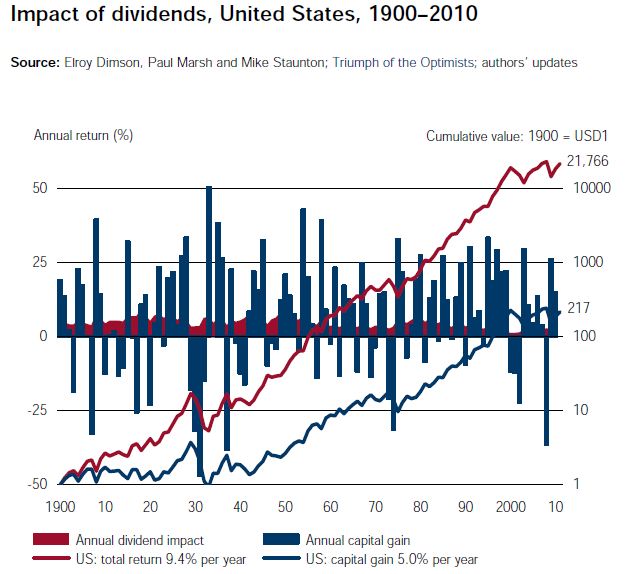

Dividend makes up 45% of average annual total returns

If we take the full time frame of 1871 to 2009, the difference with or without dividends is startling. Not taking into consideration dividends re-invested grossly undervalues stock performance.

In Credit Suisse Global Investment Returns Yearbook 2011, it again illustrates almost > 40% of total returns are directly impacted by dividends. The outperformance becomes more steep as time passes.

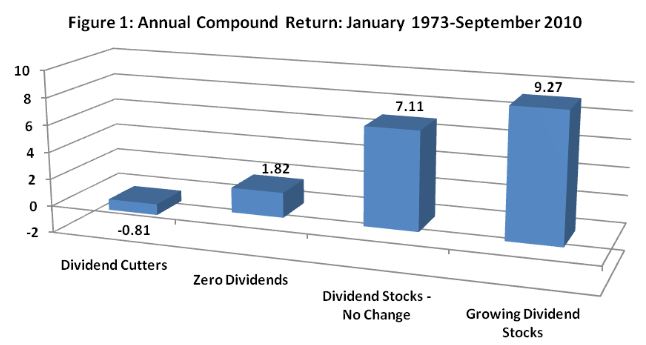

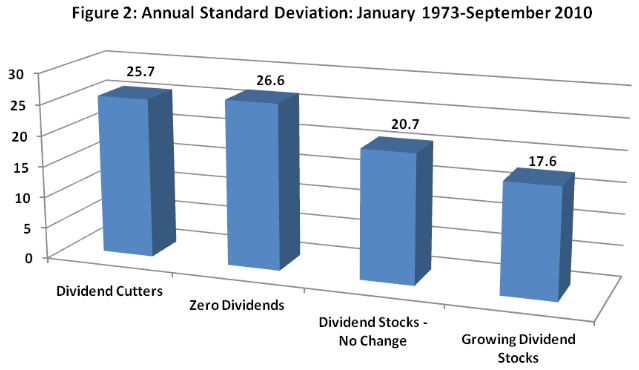

Dividend stocks and Dividend growth stocks outperforms others (1973-2010)

In a study of annual returns from 1973 to 2010 of equal weighted portfolios of the S&P500 stocks broken down into

- Stocks that grow dividends

- Stocks that pay dividends but do not grow their dividends

- Stocks that pays no dividends

- Stocks that cut their dividends

The outperformance of stocks paying and not paying dividends show a big difference, big enough to offset the tax disadvantages of dividends (most country levied taxes on dividends)

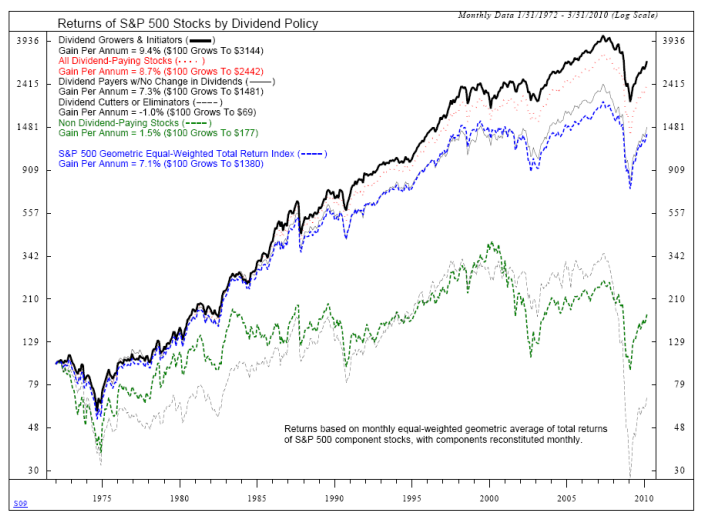

In Allianz Globals reports that compares dividend policy from 1972 to 2009, it illustrates the problem investing in non dividend paying stocks and the outperformance of the stocks that pays dividends and grow their dividends.

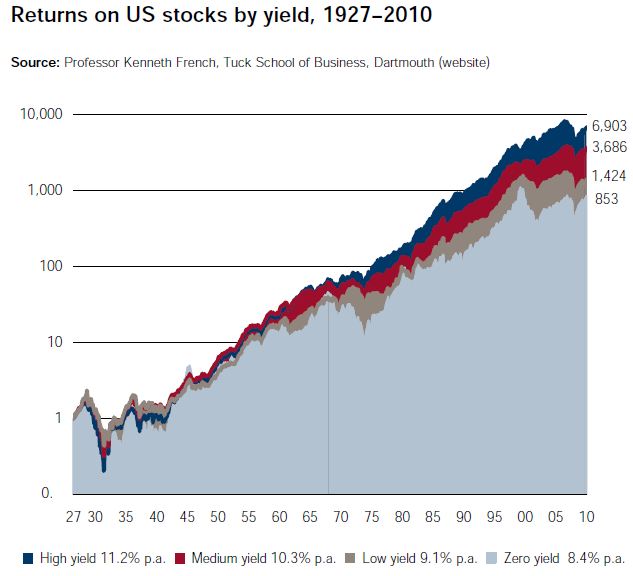

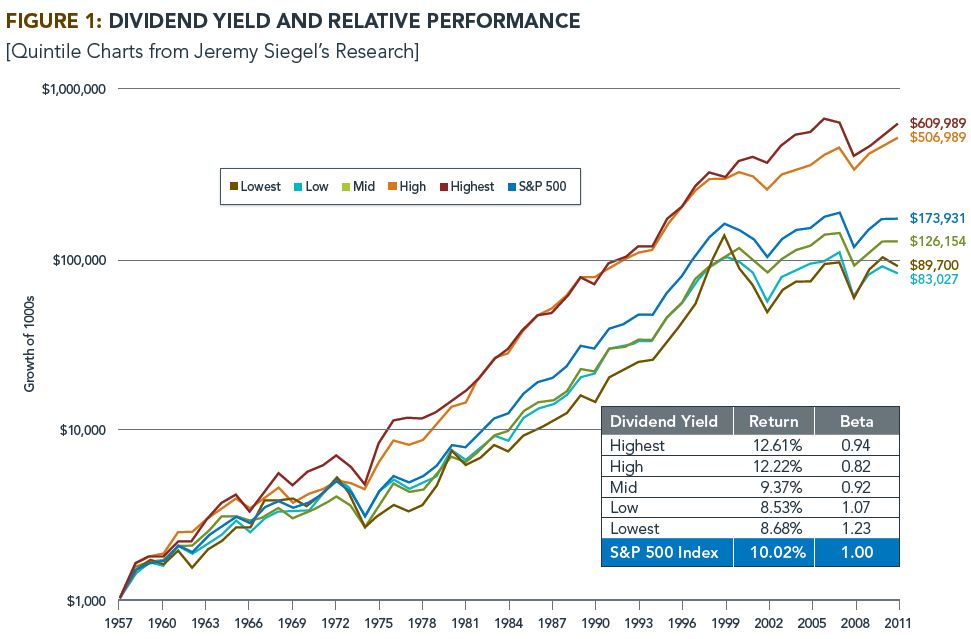

High Dividend Yield does not mean low performance (1927 – 2010)

In the Credit Suisse Global Investment Returns Yearbook 2011, the above chart illustrates that since the 1970s, high dividend stocks have been doing very well. However the most consistent outperformers have been the medium dividend stocks.

Whatever it is, the consistent underperformers have been the stocks that do not pay any dividends.

In another research by Jeremy Siegel, it does point to the same thing

Internationally high dividend stocks outperforms

In the Credit Suisse Global Investment Returns Yearbook 2011, it shows that the outperformance of high yielders is not constraint to only US stocks but also stocks around the world including Singapore.

Risk versus Return from different yield strategies

In the Credit Suisse Global Investment Returns Yearbook 2011, it illustrates the risks of different yield stocks, their correlation to the market (Beta) and the risk adjusted returns (Sharpe ratio)

In all categories the higher yielding stocks all look much better compare to no dividends but it is worth nothing that the Total Country strategy is not too shabby as well.

Highest Yield doesn’t mean always highest returns

It’s important to understand that it’s not the very highest payers you want – many high-yielding stocks got there the hard way through share price declines. It’s really the 8th decile of payers that puts you in the sweet spot for total returns. Nominal yields alone are not the story.

How re-invest dividends and compounding affects your wealth

So what happens when you invest $1 in 1871, factoring with or without dividends?

- The $1 would have been worth $181 in 2009 without dividends

- The $1 would have been worth $70,000 in 2009 with dividends

To further illustrate the dividend compounding effect, and a guide to a 5 step dividend portfolio action plan view the article compounding dividends.

In BlackRock’s March 2012 Report on Dividend Investing in a New World of Lower Yields and Longer Lives, it again illustrates that re-investing the dividends back into the market greatly improves the compounding effect and the effect can get enormous with time.

Dividends varies as a percentage of total returns

In different decades, dividend forms a different percentage of returns. It gets more important during secular bear markets such as the 30s, 70s and current 2000s

Dividend growth is very important

While reinvested dividends do make an important impact, stocks that pays dividends and grows at a good rate is also important.

In BlackRock’s March 2012 Report on Dividend Investing in a New World of Lower Yields and Longer Lives, dividend growth is the largest contributor to nominal returns across key developed markets over the past 40 years.

There’s a very important lesson in the below chart involving not sticking with just US equities for dividend exposure. This is a point I’ve made many times. In the US, we have this concept where companies only pay dividends when they’ve run out of things to invest in to grow the business. It explains that overseas, this is not how it works at all. Foreign companies that are growing are also paying good dividends, there’s no stigma about paying shareholders today and over the long-term in capital appreciation like we have here. He didn’t mention it, but I would also add that many foreign countries have tax laws that actually punish companies that retain too much profit, so dividends are actually favored by legislation. Above you’ll find the universe of international dividends by sector yields and country

In the same report, it illustrates that while the best case is a high dividend yielding stock that have high growth rate, a high dividend stock that does not grow as fast tends to underperforms the broad market index as well.

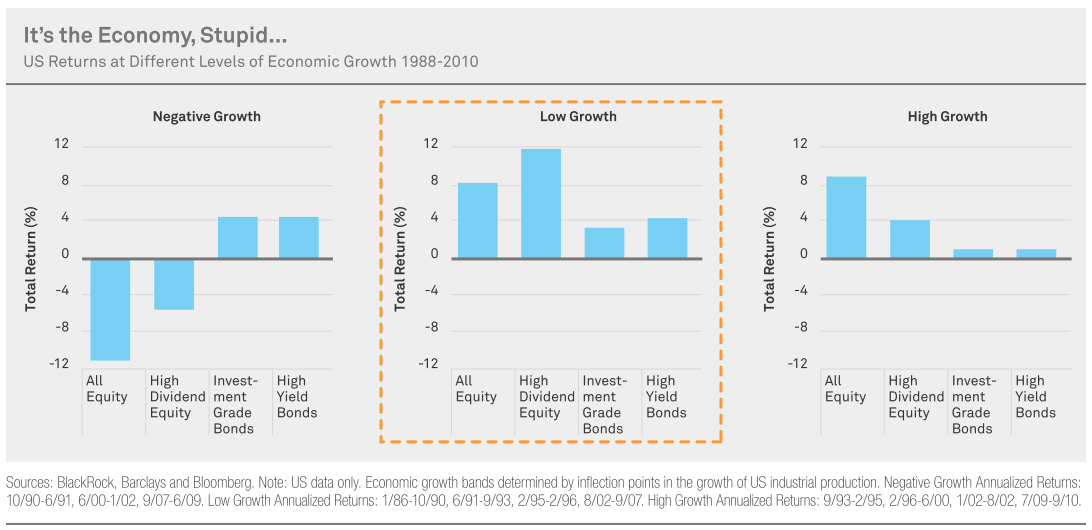

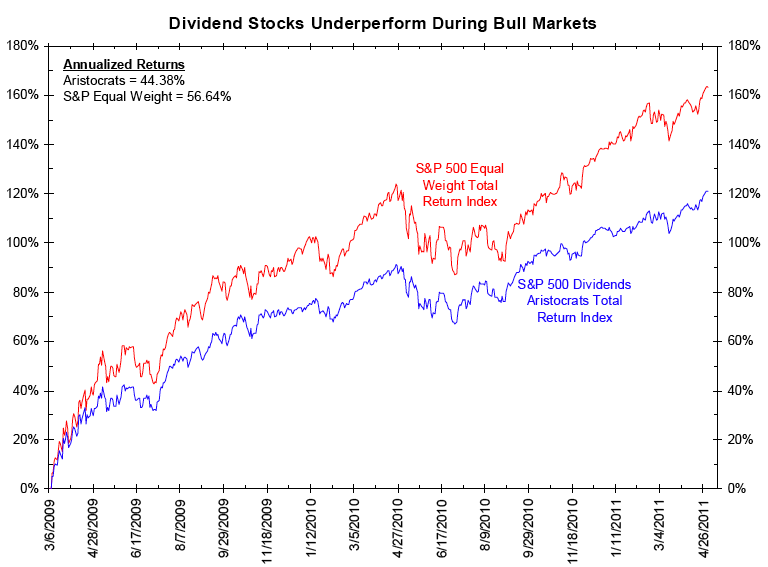

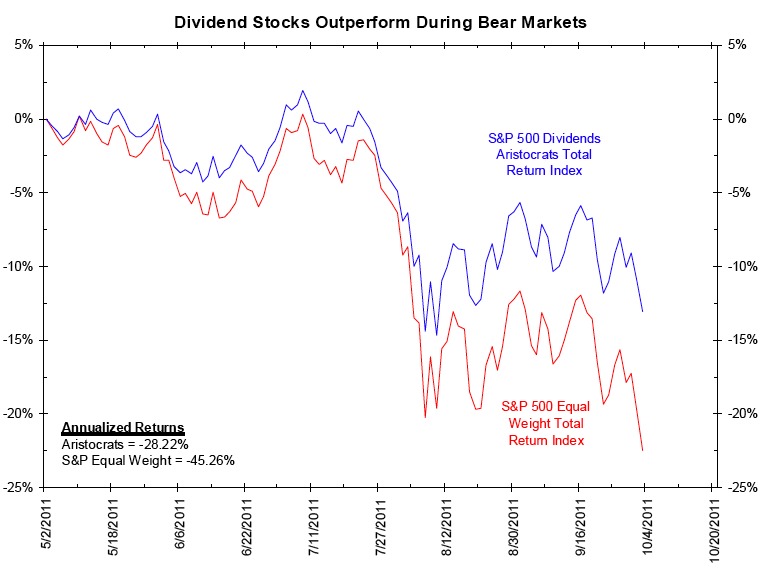

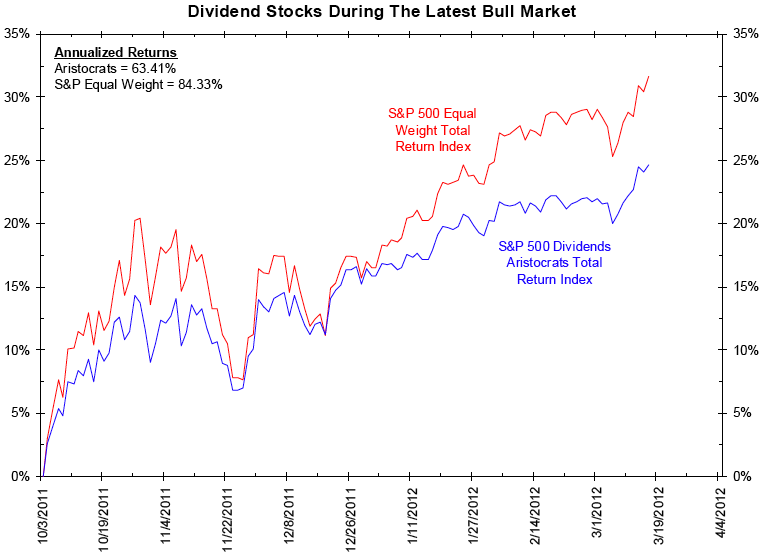

Dividend stocks versus other asset classes during bull and bear markets

(Click to view larger image)

In BlackRock’s March 2012 Report on Dividend Investing in a New World of Lower Yields and Longer Lives,it illustrates the current low growth environment and how historically, high dividend equity tends to outperform other asset classes.

During periods of negative growth, high dividend stocks take a smaller hit.

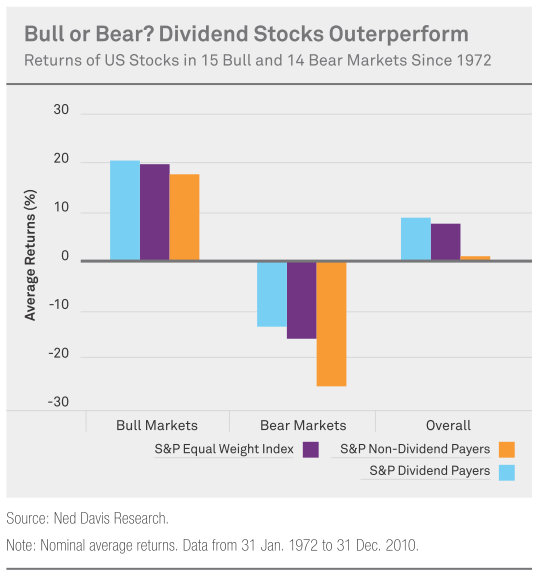

In the same report, it illustrates that for US markets no matter bull or bear, dividend paying stocks outperforms non dividend paying stocks.

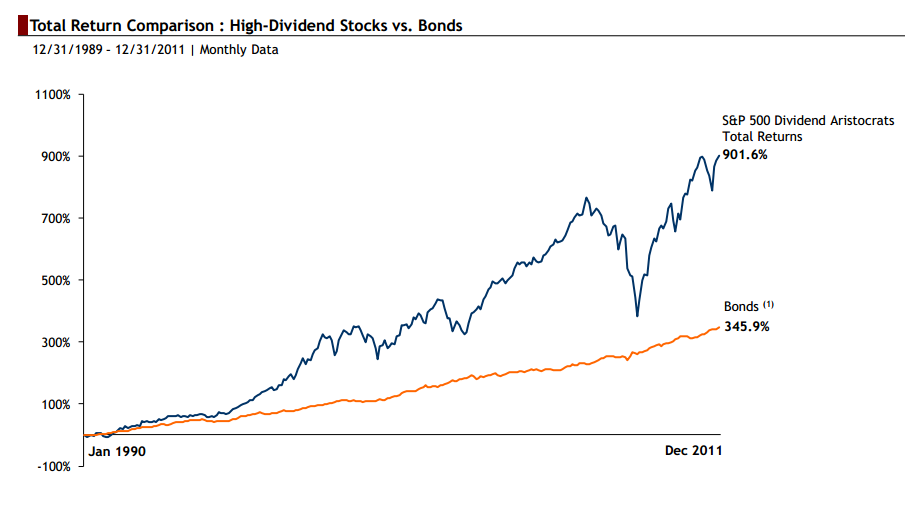

In a February 2012 Equity Compass report, it illustrates the outperformance of US Dividend Aristocrats, which are stocks that raise dividends for 25 years straight.

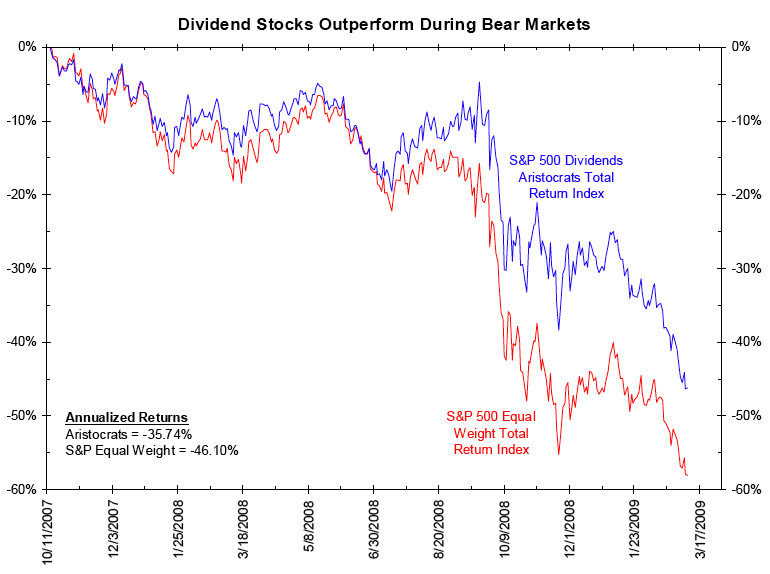

In James Bianco’s 2012 post, the relationship between stocks that consistently pay increasing dividends (aristocrats) and equal weighted stocks is what was illustrated previously. In bull markets dividend aristocrats underpreform and during bear markets dividend aristocrats outperform.

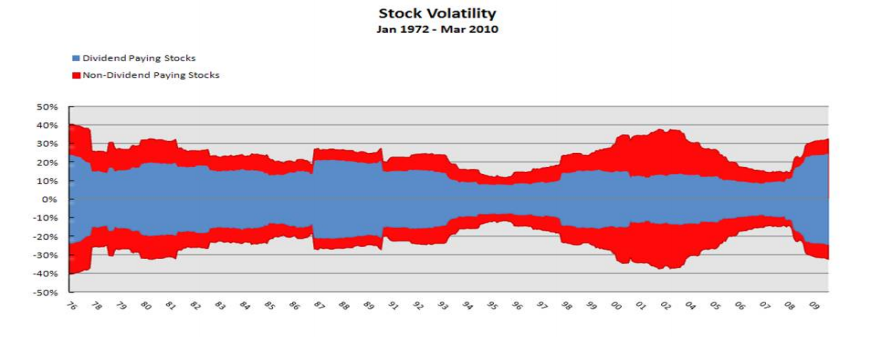

Dividend stocks and Dividend growth stocks lower volatility

In the same study of 4 differing stock categories it is found that stocks that pays dividends or grow their dividend payout, on average have a lower standard deviation.This indicates lower volatility which affects investors propensity to do rash things.

Here is another illustration.

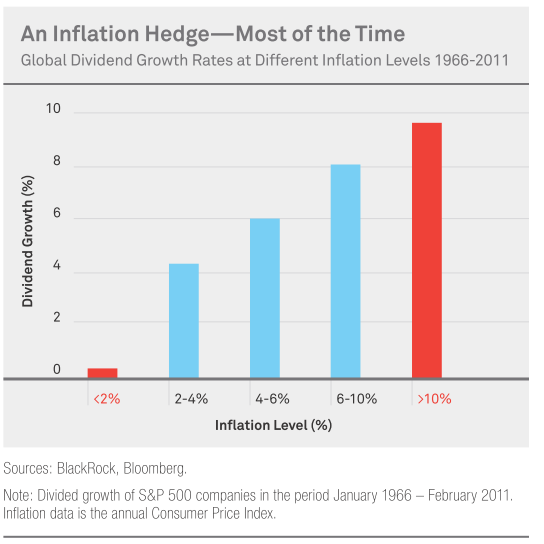

How inflation affects dividend stocks

Inflation is a silent killer for savings, for those that are uninformed about it. Bonds in the 1970s are known as “certificates of confiscation”. Current scenario mirrors that of the 1970s where the rates are at ultra low and the only way to go is up.

In BlackRock’s March 2012 Report on Dividend Investing in a New World of Lower Yields and Longer Lives, equities can be a haven during inflationary times for stocks that provide dividend growth as the growth rates generally tracks the inflation level

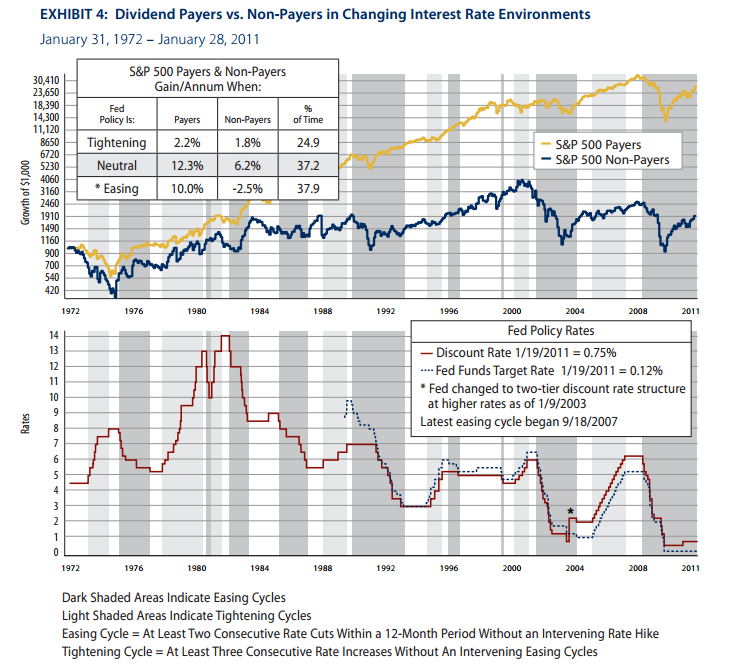

How interest rate easing and tightening affects dividend stocks

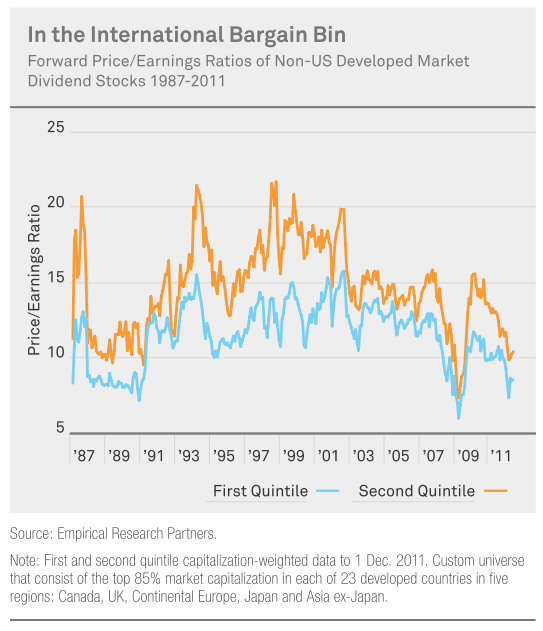

Valuation

Price Earnings

In BlackRock’s March 2012 Report on Dividend Investing in a New World of Lower Yields and Longer Lives, the non US dividend stocks have shown to be not in favor. In this aspect it shows that for international investors they are not lapping up to dividend stocks in this lost decade (2001-2010).

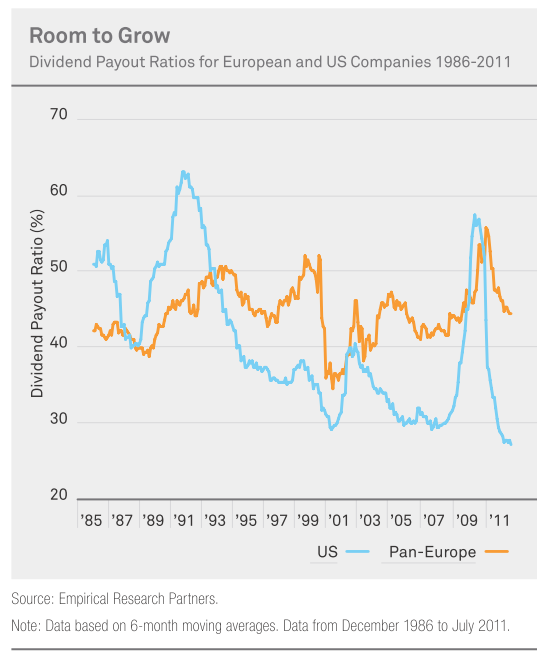

Dividend Payout Ratio

In BlackRock’s March 2012 Report on Dividend Investing in a New World of Lower Yields and Longer Lives,US dividend stocks looks to have unusually low payout ratio. This may indicate that a reversion to higher dividend payouts.

For international stocks, payout are low but are not excessively low.

One thing to note is that payout increase seem to coincide with financial crisis where to pay out the same amount, the companies would have to pay out more cash from earnings, thus the escalation of payout.

It might be the case where another bear comes around to create that same effect

Conclusion

From the past history we can come to some conclusion

- Dividend stocks can generate income, grow income and offer the potential of capital appreciation

- Dividend stocks does best when the environment is low growth

- Dividend stocks do not protect against market down turns. They just lose less money and are less volatile. This reduce the likely hood of doing anything rash to your portfolio

- The yield, dividend growth and payout ratio are crucial components of total return. Further reading here, here and here.

To get started with dividend investing, start by bookmarking my Dividend Stock Tracker which shows the prevailing yields of blue chip dividend stocks, utilities, REITs updated nightly.

Make use of the free Stock Portfolio Tracker to track your dividend stock by transactions to show your total returns.

For my best articles on investing, growing money check out the resources section.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

Dan Mac

Friday 22nd of June 2012

Dividend investing is definately a great way to go if you are looking to build long term wealth. I like looking for companies that annually increase thier dividends at a rate faster than inflation. Great info here about the effects of dividends on long term returns compared to companies that pay no dividends!

Drizzt

Friday 22nd of June 2012

hi Dan,

Thanks for visiting. I am also looking for some of those. Unfortunately stocks in Singapore don't always grow like some of these international companies. What have been your best growing dividend play?

temperament

Tuesday 13th of March 2012

Aiyah, so complicated. i only know my record of absolute "ROI" after all these years, about 31% is from dividends income.(No re-ivestment of dividends). So tell me, "Is my "ROI" correlated with your historical data?