Today I want to think about investing in Dividend Stocks while in Financial Independence or Retirement.

I think it is a type of stocks that in idea, has become a favorite of many wealth builders to spend down their wealth during financial independence.

The concept is appealing.

A portfolio of dividend stocks naturally provides an aggregate dividend income. If you keep your expenses within the dividend income, your capital of stocks remains intact. When your capital is intact, your asset based do not get eroded. This would last for a longer time. It is ideal, if the duration you need to spend down is longer.

I think a portfolio of stocks that distributes dividend income fit the purpose of wealth de-accumulation.

However, if you were to ask me, can you increase the certainty of your dividend income stream, make it less volatile and increase the passivity of the income stream?

My honest answer is that it is tough to make your dividend income stream less volatile, but we can move towards that spectrum.

For that your portfolio of stocks should:

- Increase its quality

- Purchase at attractive valuations given its quality

- We do most of the prospecting of Higher quality stocks upfront, and they can be more tolerant to shocks, thus the Maintenance Effort is lower, and your portfolio tends to be more passive

- Reduce the amount you withdraw from your portfolio relative to your rate of return

- A portfolio size that is larger than what you are thinking about

Your original idea is to have a portfolio of stocks that gives you a minimum dividend yield of 5%/yr. Over time, the capital or dividend growth is 2%/yr.

This gives the portfolio aggregate total rate of return per year to be 5% + 2% = 7%.

If your initial year annual expenses requirement is $24,000/yr then you will need $24,000/0.05 = $480,000.

So according to my recommendation, if you wish for your financial independence plan to be more conservative:

- The portfolio should consist of stocks that are higher in quality spectrum and best if they are purchase at undemanding valuations

- These stocks tend to have a lower dividend yield of perhaps 3.5%

- However, their overall earnings yield is 10%. Thus after paying out 3.5%, there is still 6.5% of its earnings retained for growth

- Assume the ROE to be at the normal cost of capital of 10%, the total rate of return per year in the long run is 10%.

If your annual expenses requirement is $24,000/yr then you will need $24,000/0.035 = $685,700. This is 43% more than the previous plan. However it should be more sturdier.

In this article, we will try to explore some of these agile strategic portfolio ideas.

Risk Seeking or Risk Adverse in Financial Independence Target

One of the reasons why I think there is a consideration to move down the spectrum to be more conservative is that each of our fear of ruin is different.

By fear of ruin, I mean that if you do not have accumulate enough, you would one day ran out of money, and catastrophic things will happen.

For some, they tend to have a more risk seeking character. They think that they should be agile enough to take things in their stride.

For others, they do not wish to go back to work, when their skill set is already obsolete and they have no choice but to work.

Your competency, your age, and the job nature you are trained at, can shift you between this spectrum.

For the risk adverse, there is a pull factor to work longer to accumulate more.

Select Higher Quality Grade of Stocks, Preferably at Attractive Valuations

The first recommendation deals with the kind of stocks that make up your portfolio.

For some, there is a tendency to go for the highest yielding stocks. This would make the amount you require for your portfolio to be less.

The problem here is that, you might earn this aggregate dividend income one year, two year, overtime, your dividend income might go down.

The reason is that high dividend stocks tend to have some challenges, hence the stock price takes a plunge and the dividend yield is high.

These high dividend stocks have 2 trajectory:

- They are misunderstood. Their share price should trade higher, and the dividend is sustainable. These are good stuff

- There is a reason the price falls. The fundamentals of these stocks have deteriorated. These are not good stuff

When you are in financial independence, I doubt you wish to keep monitoring and chopping and changing your portfolio. You could closely monitor these high dividend stocks to see if they show the signs of weakness. That might not be the ideal retirement scenario.

Active stock investing requires effort, and high dividend strategy might not be worth the effort.

Higher quality stocks are stocks whose underlying businesses have a positive growth trajectory. They can be in mature or non-mature business. However, your assessment is that the long term growth of these business is positive. This means you assessed their business to not be degenerating.

Generally, you can find stocks that are:

- Owner has strong vested interest

- The management team are good capital allocators

- The management team have skin in the game

- Have a sturdy economic moat or competitive advantage

With a profile like that, which is slanted towards growth, the dividend payout ratio tends to be less.

If you spend some effort prospecting whether their quality is higher, in the future the maintenance effort tends to be less. This means that, at the back of your mind, you have less of a worry that the upcoming results would show some fundamental deterioration. Spotting deterioration in results is key to identifying changes in a stock’s fundamentals and nipping the problem in the bud. Generally, higher quality businesses, you can be more tolerant if the results have negative surprises. This is because you would expect #1 and #2 to work the poor results over time and be more tolerant.

If you have not identify that the business have #1 and #2, then we should be less tolerant about it. We would need to watch it more. These stocks provide you with the opportunity for higher rate of return. However, they also have higher effort. That might not lean towards the level of passivity that you require.

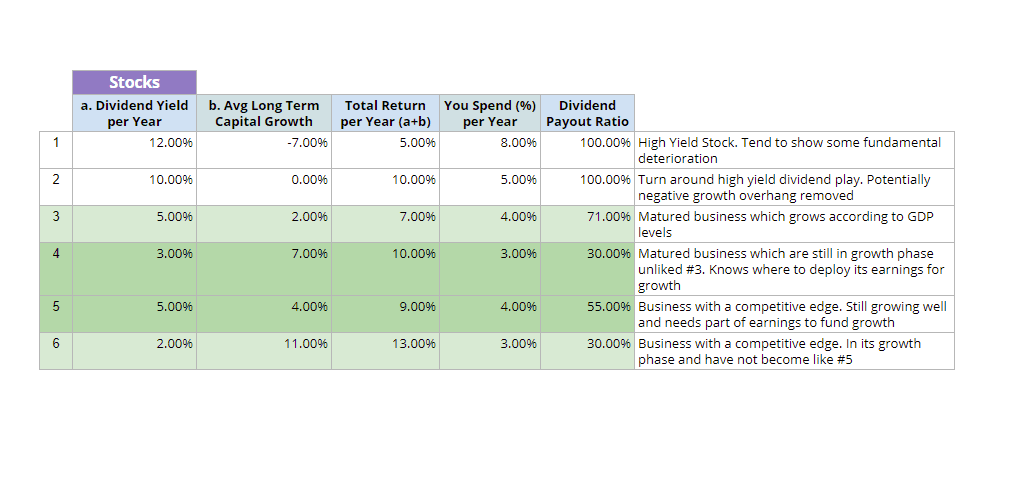

The table above shows 6 different profile of dividend stocks that we may encounter in the market. This is what I can come up with in my head. This probably will look pretty similar to my friend B‘s model given in this year’s Investors Exchange 2018.

Firstly, your Total Returns over time, would be made up of your dividend yield per year and the average long term capital growth. So in #1, you will see a high yield dividend stock giving you 12%, but over time its business will deteriorate by 7%/yr. The total return nets you about 5%/yr.

Given this dividend yield and this growth profile, I listed a column call You Spend (%) per Year. This is how much you think you could spend down from your dividend of this kind of stock over time. So for #1, given the dividend yield of 12%, you tend to spend 8% of it.

For #6, you get 2% dividend yield, but you spend 3% of it. Where do we get that extra 1%? You sell off some of your stock 6 to spend it.

I have also listed the Dividend Payout Ratio. This is the amount the management of the company for the stock payout of earnings for its dividends. Dividends do not come out from thin air. If I earn $100 this year, I can choose to pay out $30 and put the $70 back into my business to grow. This is like stock 4 in the profile above. Or I could earn $100 and choose to pay out $120 this year. This is stock 1.

Lets go through them in words.

Stock 1. Stock 1 is the dividend stock that matches my explanation of high dividend stocks. These stocks could potentially be undervalued. However, undervalued stuff most of the time, look like they are going to die. Thus there is a need for prospecting work there. Some good examples here are HPH Trust, APTT and Starhub on the Singapore Stock Exchange. At some point some of the stocks were misunderstood, have a relatively good business model, and are very undervalued. Challenger Tech at 15% dividend yield, Valuetronics at 10% dividend yield and UMS at 10% dividend yield comes to mind.

You can own the latter but the former is where you need to see if they end up like the latter. Like I say, prospecting skills are required here. If I were to advise assess the financial results, see if the dividend payout is less than the free cash flow. Check to see if that free cash flow is realistically sustainable. A lot of these business tends to be cyclical in nature. That might not fit very well in your financial independence portfolio. More monitoring effort is required.

Stock 2. Stock 2 is like a better cousin of Stock 1. These stocks tend to look like Stock 1 but you have assessed that the there isn’t negative growth. You also assess that the dividend yield is attractive relative to historical dividend yield, but also relative to the general market.

These could also be stocks that used to give a dividend yield of 7% and 3% growth, but due to poor earnings or business, their share price fell, earnings fell, such that at current valuations, the dividend yield is 10%.

If you are able to spot that the negative growth have worked itself out, you can see if there is a value point.

That is, if you assume growth is zero, whether the earnings yield is at attractive valuations. 10% is attractive anytime in my books, if the business has some quality to it. Of course, if its a more high quality, matured turn around play that has zero growth but earnings yield of 7%, pays 7% dividend yield on a 100% payout, I would consider it as the quality of this business is assessed to be higher.

However, turnaround plays… could turn out to be businesses that have fixed their problems and are re-rated by the market (this means the 10% + 0%. goes back to 7% + 3%. Given the same earnings, your share price rises!). However, my hunch is that some of these businesses tend to have lost their mojo over time. And it will be some time later the same weakness hit them again.

As someone who requires more passivity, would you want a stock like that in your portfolio? Probably not. However, I can see that if you have gotten good in your skills and would like to spare part of your portfolio to see if a Stock 2 turns out to be a Stock 3, which we will go to shortly, then that is good.

If the business is turnaround, but less of a high quality, where the business tends to show that it does better during boom times and worse in bad times, this is probably not a good stock to be in your portfolio.

Stock 3. Stock 3 looks like your ideal dividend stock that belongs to your portfolio. The dividend yield is somewhere in the medium and its growth rate tends to be around the country’s long term growth rate. This means that it is the kind of stock that follows the economy. Usually this is the kind of stock that have went through its growth phase and have matured.

One key characteristics is that Stock 3 tends to have a problem reinvesting its earnings at a good return on equity.

This company can have good earnings but due to its problem reinvest its large amount of cash flow / earnings, its growth rate is limited. To translate to the financials, the business have a high return on investment capital (ROIC > 10%) but they have a problem deploying it due to limited opportunities.

If we are to discuss some stocks that look like this, Singapore Press Holdings used to be something in this area. What happened here is that the 2% growth rate became negative.

The problem with matured business is that they could remain strong over time, but they could lose their edge. In this age of disruption, many matured businesses are seeing their once strong edge and moat being eroded. SPH is one of those.

You will see that in this example, this business gives a dividend yield of 5% and a growth of 2%. The total return here is 7%. That looks worse than the total return profile of the other stocks.

The reason for that lower total return is that the market participants tend to demand for this kind of safe stocks, and their prices tend to be higher, thus the total return that you may get is lower.

In return for the higher valuation, the expectation is that the cash flow / earnings tend to be more sturdy. That is to say, you would expect them to have this kind of slow growing cash flow over a longer period of time.

If you are able to buy a Stock 3 at much better valuation, your total return profile will look much better. The opportunity is always there.

Because the cash flow / earnings are sturdier, if the dividend yield is 5%, you could possibly spend a higher amount of it. Thus in my example I listed the spending rate to be 4%.

Stock 4. Stock 4 is probably a kind of stock that are similar to Stock 3 but also could be slightly different. In terms of its business, it has its competitive edge, or its moat can be rather sturdy. However the difference is that it has a stronger reinvestment ability.

The idea is that Stock 3 is sturdy, but if it can reinvest its cash flow at its >10% ROE well, they should reinvest more of its payout instead of its 71% dividend payout ratio. You should perhaps take a 40-50% dividend payout from its earnings / cash flow and let the management reinvest the rest.

Hence what you have is something like Stock 4. The earnings yield is 10%, but they only pay out 3% as dividend yield, thus the dividend payout ratio is 30%. For the rest of the 7%, it can reinvest at > 10% ROE.

Your ROE and the amount that you did not payout as dividend, or your retention rate (computed as 1 – dividend payout ratio) determines the growth of the business.

So if the ROE for a Stock 4 is stagnant at 10%, and they retained 70% of earnings, the growth rate is 10% x 0.70 = 7%. If you payout 70% and retained only 30%, your growth rate is 10% x 0.30 = 3%.

So on the first year is whether you want a high dividend or low dividend.

But how important is the ROE and low payout?

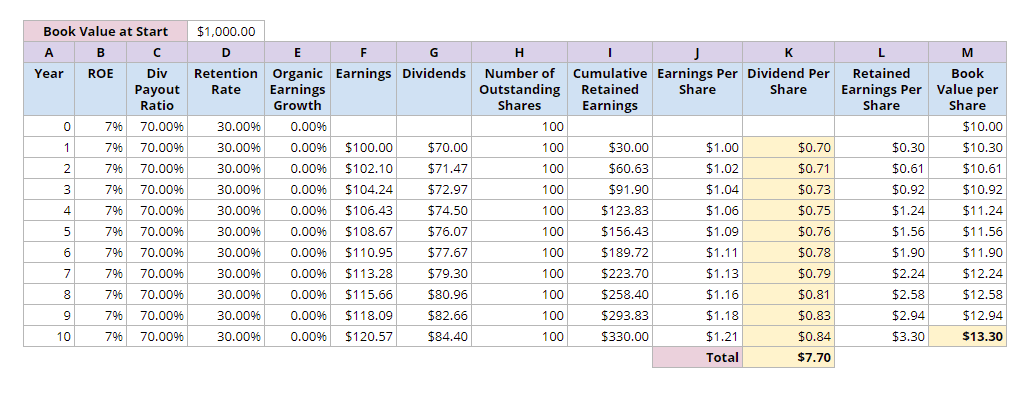

The above table illustrates the 10 year return you will get if you invest in a share of something similar to Stock 4 at the start of year 0. The book value of Stock 4 is $1000 and since there are 100 number of shares, each share is worth $10.

The above table illustrates the 10 year return you will get if you invest in a share of something similar to Stock 4 at the start of year 0. The book value of Stock 4 is $1000 and since there are 100 number of shares, each share is worth $10.

Suppose on the first year the earnings is 10%, or $100. The management of Stock 1 pays out 30% or $30 and retains 70% or $70 on the equity. Since we assume that there are no other external factors that drive growth (0% organic earnings growth) other than the business management ability, the sustainable growth rate for Stock 1 is equivalent to the ROE (10%) x Retention Rate (70%). In this case the sustainable growth rate is 10% x 0.7 = 7%.

For these 10 years the earnings go up due to the ROE applied on the cumulative retained earnings. The dividends go up from $30 to $55.15.

The book value or the equity starts a $10 and go up till $19.67. In 10 years the book value almost doubled.

If the book value shows what Stock 4 really worth then the share price should follow the book value.

In these 10 years, the total dividend per share paid out amount to $4.14.

The total return roughly is $19.67 + $4.14 = $23.81.

How does this contrast to Stock 3?

The table above sought to simulate Stock 3. The dividend payout ratio is higher at 70%, the ROE is lower at 7% instead of 10%. So the sustainable growth rate is 7% x 0.30 = 2.1%, which is pretty close to the growth rate of Stock 3. The book value growth is lower. It reached $13.30 but the dividend paid out is higher at $7.70.

The total return is $13.30 + $7.70 = $21.00

The difference is not so much, most likely because the resultant sustainable growth rate of 7% and 2.1% is pretty close together.

In reality, it will be tough to find a business that can consistently reinvest and maintained the ROE or ROIC.

The main appeal of a Stock 4 business is that there is a growth component and it “protects” the dividend.

As the dividend payout is low, and the business is quality, these 2 factors result in the management likely to retained the dividend, because the dividend as a percentage of free cash flow is not demanding.

What this means that if Stock 4 pays out 3% dividend, you can spend that whole 3%. You do not need to put in a buffer like Stock 1 to 3.

And that 3% will grow over time.

Whats more is you will retain growth.

These kind of dividend stocks are similar to the Dividend Aristocrats in the USA. These are companies who paid and raised dividends for a long period of time. One good reason is that the dividend payout ratio is not demanding at the start. So when there are challenges, the management can still maintain the dividend.

In the local context, while not 10% total return you have stocks like Ho Bee Land which gives an recurring earnings yield above 6%. But they currently paid out only 3% in dividend or less. Because the earnings are recurring, and based on longer term contracts, it is likely they can sustain that 3% during tough times. Thus if you portfolio contains Ho Bee like stocks, you could spend those 3-4% dividends while the management have rooms to retain and grow.

In the case of developers such as Ho Bee, their key strength is in the connections of the management team, the foresight to spot asymmetrical rewards. These are intangibles and probably not on the balance sheet. With the help of debt funding, they can choose to develop properties for additional growth when the opportunity arises.

It seems that there are a lot of family owned property companies that fit this profile:

- This is where their wealth is so they have skin in the game

- They have shown to have the experience and the past records to allocate their retained earnings, reinvest for growth

One good example is Cheung Kong Assets (CKA, HK:1113). CKA is one of the assets that was helmed by Li Kar Shing. A few years ago, he restructured his portfolio of assets to what it was today. CKA now housed their development works, investment properties, global utilities.

In recent times, they put their connections and their superior balance sheets to use to acquire aircrafts to lease to airlines, and Australian,Europe and Canadian infrastructure companies such as DUET, ISTA and Reliance. And they are in talks to acquire APA in Australia for their distribution network.

The dividend yield is pretty low at 3.21% but its recurring cash flow should be around 6.5%. This makes the dividend payout to be very sturdy. And the upside is the organic growth in the portfolio of recurring assets and the growth from further acquisitions.

Stock 5. Stock 5 is also an area that can be highly considered. The stocks in Stock 4 tend to be good capital allocators. In Stock 5, these are businesses that have a moat or have the factor that give them a distinct edge over their competitors.

Due to these factors, they are able to grow in size.

The difference between stock 5 and Stock 6, which we will mentioned later, is that they are much of a known business now. They have gone past the stage where people are questioning whether they have a competitive advantage or not.

When those uncertainty are weeded out, This for me, becomes a better business to invest in.

As these business are still growing, despite their size, their dividend payout tends to be lower. Their growth rate, while not as high as in the past, is still pretty good.

As a person that requires more passivity and a more conservative portfolio, a bunch of Stock 5 makes sense because, like Stock 4, the dividend yield is growing, you can spend most of it, yet the asset can still grow organically.

There are very little local examples. I do not have one that comes to mind.

However, you do have international companies that fit these profiles.

Stock 6. Stock 6 are the kind of stocks that Stock 5 was at, before they become more matured. Depending on your prospecting skills, you might hit some winners here. These companies are low payout. They could payout only 1-2% dividend or they could payout none.

However, the cash flow that they retained can grow at a great growth rate.

The problem for you as a dividend investor that is ready to spend down is that, these stocks can be volatile. You still have to spend a fair bit of time wondering if they becomes the kind of stock in Stock 5.

The strategy with these Stock 6 is to sharpen your prospecting skills, spread out your capital among more of these. If a subset of these Stock 6 work out, their returns will drive your portfolio. There would be more failures. Take a chance with them and weed them out over time.

For your overall portfolio, don’t let a bunch of Stock 6 overwhelm your portfolio.

The Types of Stocks to Form your Core Dividend Stock Portfolio

Given my explanation, my recommendation is to have more of the kind of Stock 4 and 5 as a basis of your portfolio.

I think Stock 3 and Stock 6 as the next band. Your hope is that you have some future great dividend stocks in the Stock 6 category. Stock 3 will pull up the overall dividend yield while providing the stability.

However Stock 4 and 5 as the core will drive adequate growth in your portfolio.

Having enough of stocks that have a better chance of higher rate of return would increase the gap between the percentage you spend versus the rate of return.

Why You Need to Have an Adequate Average Total Rate of Return

So one of the reason you need to increase the gap between your average total rate of return and the percentage you spend is because of the problem of sequence of return risk.

When you are financially independent, you stop having capital injection. You start having capital outflows for your annual expenses.

A negative sequence of return is when you have a period of poor returns, before a series of good returns. On its own, a series of poor returns follow by a series of good returns would not harm your portfolio, all else being equal.

However since you are withdrawing from your portfolio in your capital outflows, it further amplifies the poor returns. The end result is that you have less capital to build on, when the good returns comes back, because you were withdrawing from the portfolio.

You can read more about the sequence of return risk in this article I have written.

There are some possible solutions in the article above and I have explored the pros and cons. However, there are some articles with further exploration:

- Variable Withdrawal Strategies. Basically flexible spending. It is an anti-fragile solution but the down side is that your spending might not keep up with inflation.

- Have more Equities. Equities are more volatile, but the rate of return is higher. This makes your safe withdrawal rate safer. It may allow you to withdraw more money as well.

- Having more cash to prevent the first market crash. This is so that you can spend the cash instead of having to withdraw from your portfolio. Note that this will only work for the first crash.

- Other Retirement Planning Notes

Sequence of return risk can be pretty hard to deal with. You run the risk of failure, but if you read some of the finer points in the list above, it will prevent you from suffering from the risk of ruin, which is going into debt or reaching zero money.

A higher rate of return helps you generate more wealth so that the eventual amount that you withdraw during your financial independence phase is lesser. This makes your financial independence plan more sturdy.

Could you form your dividend portfolio with high dividend payout companies with relatively high dividend yield?

For a lot of people, dividend investing entails having a portfolio with a cross of stocks between Stock 2 and Stock 3.

While your dividend yield might not be 10%, you might choose something that is closer to 6% with an organic growth rate of 2%, which is around the growth rate of the GDP of the country.

The payout ratio is close to 100%.

What would happen with a portfolio that is largely made up of this profile of stock?

My concern is that this portfolio would have a problem sustaining this result over time.

A business that gives 100% of its earnings as dividends would struggle to have the capital to sustain growth.

There are exceptions. If you have a business that do not need much capital to grow, this is possible. However, not a lot of business do not need large amount of capital expenditure, so thus the business is rare.

In Singapore, there are many property companies. What they could do is leverage on their balance sheet to temporary finance their property development. If not, it will be something like Seas Candies which require very little capital expenditure relative to their revenue.

The short answer is that you could choose a 100% dividend payout stock.

If your stock portfolio is full of these, it means that your portfolio is more towards risk seeking then towards being risk adverse.

You can make your own adjustment.

If the dividend stock payout 100%, you could choose to retain your own dividend income instead of spending it. Then you could choose to reinvest the dividends yourself in higher return companies.

You could choose to spend most of it, if you sought to pursue other forms of financial independence schemes:

- Traditional Retirement

- Semi Retirement

- Being Financially Secure, Financially Independent and still Working

- Coasting Financial Independence

#2 to #3 might entail that the time you require the portfolio to generate wealth cash flow to be temporary.

If that is the case, having stocks that yield 5-7%, 100% payout with growth that correspond to GDP would work. When you do not need the money, the dividend income can be plow back and reinvested into the portfolio.

When you need it, learn to spend less, or have a script how to spend the cash flow. When your cash flow are known to be volatile, you need to exercise some flexibility. #2 to #4 have shown to be schemes that accommodate flexibility.

How do You Get that Kind of Total Return?

One question you might have is that how do you get a good quality stock that gives a good dividend yield of 3-5%, yet forward looking there are still 5-7% of growth. Or a business that have competitive edge with good dividends but still growing well as Stock 5.

There are some search costs required, and you would have to be doing this for some time to be able to filter out companies that seem better than the rest.

To know that they are better than the rest, you have to see enough of those that lack quality as well.

And then, most importantly, you have to acquire them at reasonable valuations. How much you buy, for this profile of quality business is important. It doesn’t make a lot of sense to overpay too much even for good quality.

You won’t get 3% + 7% if its bought more expensive.

This is why I explained that it is preferred if you purchase at fair to attractive valuations.

Summary

I think this post will be helpful for those who are more of an active stock investor. This will enable you to sort of pigeon hole some of the stocks in your portfolio as you transition to financial independence.

This is a bit tough on my brains, so I am not sure if I should do an equivalent for a pure Real estate investment trust (REIT) portfolio. Do let me know.

Here are My Topical Resources on:

- Building Your Wealth Foundation – It is imperative you know these stuff as early as possible, because this is the most important stuff

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – The Deeper stuff on REIT investing

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Incomeinvestor

Tuesday 28th of August 2018

Hi Kyith,

Thank you for this piece of article.

I have a question for you.

I would like to use quantitative ratios such dividend payout ratio, ROE, Cash flow - net income ratio etc to do my first screening, that is to screen and select Stock 3, 4, 5 and 6 before analysing them qualitatively. What other ratios can retail investors use to tell apart Stock 3, 4, 5 and 6?

Stock 3 : ROE: 10 % Dividend payout : 30% What other ratios required to select Stock 3 type of counters?

Stock 4: ROE: 7% Dividend payout : 70 % What other ratios required to select out Stock 4 type of counters?

Stock 5: ROE: ? Dividend payout : ?

Stock 6: ROE: ? Dividend payout : ?

Kyith

Tuesday 28th of August 2018

Hi Income Investor, I cant put a clear ROE to them, this is because it is a bit philosophical. I can tell you my benchmark for Stock 5 is a 10% ROE, but what good can that do us? Stock 6 most likely have a pretty high ROE. Given something above 10%, and if the leverage is low, it is definitely something I would look at.

Sinkie

Monday 27th of August 2018

First off, you NEED to be comfortable with a -40% or -50% drawdown in your equities portion. because it WILL happen .... Especially with Singapore equities. This is important if most e.g. 80% of your portfolio need to be in equities / risk assets in order to generate the required amount of dividends.

2ndly it *may* be possible to use a lot of REITs. But bearing in mind that these are essentially leveraged entities that give away at least 90% of earnings i.e. very cash light. So if a big % of your dividend portfolio is composed of such things .... just make sure that your dividends is at least 50% more than your expenses .... and SAVE the excess. Becoz you WILL NEED it for the heavy rights issues during recessions.

Accumulating strong cash-gushing companies is already hard. It takes many years, maybe a couple of decades, and a hell of patience. The time taken especially through bull-bear business cycles will also help prove the robustness of the companies & the overall portfolio.

The harder part is having the stomach & the psychology to stay the course when you no longer have active income & your equities go down by 50%.

Kyith

Tuesday 28th of August 2018

Hi Sinkie, can't say that you are wrong there.

Bob

Monday 27th of August 2018

I am not sure that there are an unusually large number of rights issues by REITs during a recession. I would have expected the opposite, as during a downturn it will be harder to sell the rights and REIT managers will be cautious about expanding the AUM.

It is also not always clearly the case that not taking up rights is a huge penalty. The rights issue will be made for a specific purpose, generally to increase the AUM by an income generating asset, which should as a minimum match the yield of the existing AUM. This means that the DPU should remain similar. If it doesn't, then it is time to question the REIT manager about his actions. Simply increasing the AUM for no reason other than to have more AUM and a bigger management fee is not acting in the best interests of the share holders.

There might be a lost opportunity to purchase units at a discount to market price for a one off capital gain.

REITs generally have multi year lease agreements with their tennants. Although the market value of the units might go down, the DPU should remain relatively stable through a recession. That is important for unit holders, who are not primarily seeking capital gains. This year is an example of my REITs declining by 6% but my income has not been affected, indeed it has increased. And as a plus I can reinvest by buying more units.

Regards,

Divy123

Sunday 26th of August 2018

Hi Kyith thanks for this very useful article.I was just mulling over my own portfolio of stocks ( which is heavily geared towards dividend stocks for cashflow which I look to tap on starting in about 6 years). For most retail investors a portfolio that requires prospecting and monitoring fairly consistently is not ideal. What I am planning to have is more than 1 stream of " income". 1. CPF life ( enhcanced retirement sum): 18-19% of retirement cashflow 2. CPF OA ( 2.5% p.a. draw out this amount yearly): makes up 17% of retirement cashflow 3. net rental income: 10% of retirement income 4. Income from equities ( self managed) with average dividend yield on cost of about 4% of capital invested ( not market value of portfolio as this will fluctuate): 23% of retirement cashflow 5. Income from professionally managed no fee fund ( like aggregate Value fund that averages about 10% over long term, withdrawing 4-5% p.a. from this fund. Have planned to give investment in this fund a lead time of at least 6 years or more before starting to draw on this to give buffer): about 30-31% of retirement cashflow.

Singapore Dividend Collector

Sunday 26th of August 2018

Very informative. Thank for taking the time to write such quality blog posts.

Bob

Sunday 26th of August 2018

Thanks for the info, once your brain has recovered I would appreciate a similar post for a REITS based portfolio.

My portfolio is 90% REITS, which will be my main source of income in retirement. I prefer REITS over stocks for a retirement portfolio as a REIT is much easier to understand than analysing a company, its product line, its competition, and future prospects. This might become more important as I get older and my cognitive abilities are not so sharp. Which is a worry.

One aspect of SG REITS is that the majority of the REITS' assets are leasehold, and a fair number of them are expiring in the 25 to 45 year time frame, which is uncomfortably within the retirement span. I am not sure what happens in Singapore when these leaseholds expire, what happens to the REITS' valuations as the leases approach their end and whether this is something I should also worry about. At the moment I am ignoring it, and trusting the managers will have enough competence to mitigate any negative factors. Do you have any insights?

Regards.

Nigel

Monday 27th of August 2018

Would also like to know your thoughts of a highly concentrated reit portfolio. Essentially one of a highly diversified reit portfolio where its overall performance is dependent on the performance of various companies across different sectors.

Phil

Sunday 26th of August 2018

I am in the same boat as you though i'm just starting with REITs investing. I do also have same concern about SG REITs.

Hope to see a post from Kyith regarding REITs-based portfolio.