There is a reason some stocks are never to be touched. Stocks that you do not understand what their business is. Stocks that have business subjecting them to risks of losing all their capital.

Global Investments Limited (GIL) is one of them. It exists in 2007 at IPO time as Babcock and Brown Global Management Pte Ltd. Back then if you are chasing for yields, this one yields high together with then favorite Macquarie International Infrastructure Fund (MIIF) (coincidentally both Australian)

The problem of it versus MIIF is that while MIIF then are overpriced assets, at least you know the problem. Babcock and Brown Structured Finance invested in assets ranging from aircraft leasing, various kinds of loans and music copyrights. Its parent which owned the majority stake fell to bankruptcy during the financial crisis and its book value got smashed through the floor as they end up non performing.

Its not a pretty sight as a new dividend investor as you could very well be the one caught in that.

A few months ago we decide to relook at GIL. Since the debacle, a new management ST Asset Management (STAM) have been appointed the new manager of GIL. STAM is affiliated with Temasek (doesn’t mean they will do a good job by their recent records).

We decide to look because of the attractive yield and cash build up through numerous rights issue. Like MIIF this classifies as another Leopard may not change its spots deal, and thus this post is more of a note to myself rather than a recommendation.

GIL declared another round of 1 for 2 rights issue and I decide to write this post to collect my thoughts and evaluation of the rights issue.

Rights Issue

1 For 2 Shares Rights Issue

Currently TERP XR Price => S$0.133

Current outstanding number of shares => 550 mil shares

Current market capitalization => S$73.15mil

Rights issue price => S$0.128

No of rights shares issuing => 275 mil shares

New cash injection => S$35mil

Market capitalization after rights => S$0.133 x (550+275) = S$109.72mil

No of shares after rights => 825mil

Change in investment policy

At the SGM on 5 Dec 2011, the shareholders of GIL approved the expansion of the company’s investment policy so that its investments are not limited to the original three sectors.

The company’s strategy is to invest in a portfolio of assets in different sectors through different means which include but not limited to

- direct asset ownership

- swaps

- credit default swaps

- debts

- warrants

- options

- convertibles

- preference shares

- equity

- guarantees of assets and performance

- securities lending

- participating loan agreements

The company will not make any direct investments in

- real estate

- commodities

- Basically, they changed their terms to have more toys to play with, i.e. more kitchen knives, AK71, MP5s

Assets analysis

Total assets before rights issue => S$167 mil = Aircraft (S$31mil) + Loans Portfolio (S$71mil) + Fly Leasing and Avoca Notes (S$21mil) + Cash (S$42mil)

Total liabilities before rights issue => Interest Bearing debts (S$17mil)

Net Asset Value before rights issue => S$150mil

Total assets after rights issue => S$202 mil = Aircraft (S$31mil) + Loans Portfolio (S$71mil) + Fly Leasing and Avoca Notes (S$21mil) + Cash (S$77mil)

Net Asset Value after rights issue => S$185mil

Price to Book => 109/185 = 0.59 times

Net cash after rights issue => S$60mil. 54% of market capitalization is net cash

In addition, 8 months later, in 2014, the 2 Aircraft (S$31mil) will be sold for S$34mil. This will increase the net cash level from S$60mil to S$94mil.

Essentially, the market, by valuing GIL at S$109mil ex rights, is valuing it as S$94mil in cash and the rest of its assets (Fly Leasing & Notes – S$21mil, Loans Portfolio – S$71mil) at only S$15mil.

Profit analysis

Revenue

Rental Income from Aircraft (S$31mil) => S$4.7mil, ROA => 15%

Dividend Income from Fly Leasing (S$16mil) => S$1.054mil, ROA => 6.6%

Interest Income from Loans Portfolio (S$71mil) => S$9.866mil, ROA => 14%

Gain from sale of investments => S$3.6mil

Total Revenue => S$19.22

Expenses

Management fees => S$0.8mil

Exchange losses => S$0.38mil

Depreciation => S$1.3mil

Finance cost => S$1.325mil, average interest rate (1.325/17=7.8%)

Impairment cost => S$1.772mil

Other => S$1.9mil

Total Expenses => S$7.5mil

Profit

Net Profit => S$11.72mil

Net Profit (ex gain from sale of investments) => S$11.72 – S$3.6 = S$8.12mil

As mentioned, the sale of the 2 aircraft will change GIL’s 2014 profit in a very big way. As each aircraft is leased at USD $160k per month, GIL will lose the S$4.7mil in revenue.

I seem to think part of the motivation to sell could be that the loans are tied to this 2 asset. So selling this would enable GIL to pay off the 7.8% interest rate debts.

Then again the equity yield that investor demand is pretty steep as well at > 10% yield.

Selling off for S$34mil will clear off S$17mil in debts, as well as finance and depreciation costs. At the same time the other S$17mil can be channel to cash pool.

Profit(ex sale) => (19.22-4.7-3.6) – (7.5-1.3-1.325) = S$6mil.

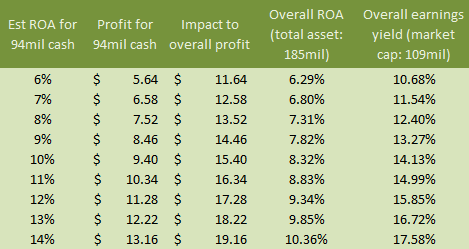

The potential to replenish the loss revenue will depend on how GIL make use of the 94mil cash holding.

Different investments (GIL have not state yet) have different risks, costs and potential returns.

We can estimate the potential return on asset (ROA) from 6% upwards, since the prevailing return on assets for most financial instruments seem to be 6% (in absence of leverage and trading at discount)

Based on the current ROA of assets, the ROA can hit as high as 15%

In the following table we compare what are the estimated ROA and its effect to the earnings, return on assets and earnings yield

Some profit caveats:

- A base ROA of 6% will assume that GIL does not invest in highly leverage or risky assets. Assuming PTB of 1 times, these assets would be in the class of SIAEC, PLife REIT, SPH. Relatively safe instruments

- An ROA of 14% is likely to be assets or instruments that have a finite lifespan, that requires adequate compensation. Paying out the full earnings yield and not accumulating cash as retained earnings would more or less result in future fall of NAV

- An ROA of 14% can also instruments that are highly leverage within and as such explains the premium in yield. In times of crisis, it is likely to be negatively impaired

- An ROA of 14% can also be hard to understand instruments (notes, CLO, CDO, swaps) with larger than expected counterparty risks. Thus it explains the higher premium

- Also note that sans the 94mil, the current Loan Portfolio are likely to have valid terms, whereby they may be redeemed at lower if not zero value.

- As the underlying of the Loans Portfolio contains mortgage backed securities and other loans that can be greatly impacted by mark downs and impairments

- GIL may not use up ALL the cash to fund investments, thus a lower ROA.

Dividend

In this past year, GIL paid a total of $0.015 cents dividend. At my average price of $0.16, the yield is 9.3%. My new average price should be reduced to $0.14. As such the yield is 10.7%.

To pay out this yield, GIL will need S$8.25mil. This amount is equivalent to the net profit sans the one time gain from selling some of the notes.

Obviously the payout will be affected by the sale of 2 aircraft as profit will be dropped to S$6mil, but with a huge capital, they should be able to pay 2.25mil more.

The potential dividend yield is listed in the table above under earnings yield. That is the potential safe payout range.

Valuation

The Price Earnings ranges from a high 9.3 times to 5.6 times depend on how GIL invests its S$94mil

Although GIL trades at a huge discount to book value (PTB:0.59times), it is only useful if we know how valuable and tangible the underlying assets are.

We know that out of $109mil, $94mil will be in cash, the rest of the $92mil is valued at $15mil.

This is hugely undervalue had the $92mil be hotels, or houses, or functional factory equipment. The underlying are stakes in Fly Leasing and Loan Portfolio and while Fly Leasing is valued at S$16mil, you can make the case that the market is valuing GIL’s loan portfolio to be worthless tomorrow.

The key thing to find out before the right’s issue is how much is that actually worth to you. For instruments like credit default swaps, warrants, options, CLO it is very plausible to see them being heavily impaired.

That is perhaps one of the reason GIL under its old management Babcock and Brown fell from a high of $1 plus to where it is today in the GFC.

If you invest, it is a bet that the underlying portfolio and its risks are actually less than what the market anticipates.

Conclusion

I am likely to subscribe for the rights issue and some excess rights. Even with such an appealing potential yield, I will not go overboard.

At the same time, the yield is tempting enough to invest in potential upside. If the loans portfolio crash totally, I at least know that $0.113 of GIL is in cash potential.

This is not an inducement to buy, as this baby can turn sour overnight. I don’t want to cause too much broken hearts.

To get started with dividend investing, start by bookmarking my Dividend Stock Tracker which shows the prevailing yields of blue chip dividend stocks, utilities, REITs updated nightly.

Make use of the free Stock Portfolio Tracker to track your dividend stock by transactions to show your total returns.

For my best articles on investing, growing money check out the resources section.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Jay

Friday 10th of July 2020

Hi Drizzt, I revisted your post on GIL as I am currently re-evaluating this counter. Overall, it's risk-reward return looks pretty attractive to me. Appreciate any thoughts you may have to share, thanks.

Cheers, Jay

Kyith

Friday 10th of July 2020

Hi Jay, I have not taken a look at GIL for some time! Perhaps you can share your perspective why you find that GIL is attractive now.

t

Friday 27th of April 2012

Hey Drizzt,

Chanced upon this as I was researching into GIL. I think your analysis is thorough and amazing. Myself Im quite new to investing and have quite a hard time grappling with fundamental analysis e.g. income, cash flow statements are all greek to me. Wanted to ask if you recommend any books or blogs I can read to get a better understanding of FA.

Also do you know if it is natural for price to increase after a rights issue?

SnOOpy168

Wednesday 11th of April 2012

Interesting to read that they have made 1H2012 Dividend Guidance. Meaning that it is most likely expected and perhaps for 2H2012 too ?

http://www.globalinvestmentslimited.com/SiteMedia/w3svc1120/Uploads/Documents/11_20120409_1H2012DividendGuidance.pdf

10-11% yield is reasonable expectation. Just that it pays twice a year.

Drizzt

Wednesday 11th of April 2012

hi Snoopy168, thanks for taking interest in this. the management did state that based on cash economic income they did not distribute alot of the sale of assets as dividends, so they should have enough to cover the dividend.

we have to be careful here and monitor they invest the cash in assets that are dividend accretive. else it is money down the drain. what do you think?

#Frequentreaderofinvestmentmoat

Sunday 25th of March 2012

Hey Drizzt,

Thanks for this wonderful article. It spurred me to do some research on it as well. I've got two comments:

1. The Income Statement in the latest quarterly report appears to be understating the Management Fees paid to STAM. Yes, the income statement stated that the management fees is 813k but just two pages earlier, a total of $2.072 (inc 760k for base management fees and 650k for fixed management fees( mil was reportedly paid to STAM. Since no new shares were issued in the to the Manager in the last financial year, this fees are most probably categorized under "Other Operating Expenses"

2. The improvement in the global economy will make it more challenging for STAM to achieve the attractive returns of 14% it is currently enjoying from its loan portfolio. Much of these impressive returns are generated from its US Residential Mortgage Based Securities. These were successfully purchased at below face value in 2010 (a more uncertain economic environment than the present). For instance, the total face value of Structured Asset Mortgage Investments II Trust 2006-AR7 and Bear Stearns Mortgage Funding Trust 2006-AR5 was US$10.071 mil but was purchased for US$5.75 mil. Because neither of these RMBS defaulted, the principal + interest payments have boosted the performance of the loans portfolio. Contrast the RMBS to the CLO, which were purchased in 2011 using equity raised from the previous rights issue. They were purchased close to or at face value. With the exception of Sealane II (Trade Finance) Limited, the coupon rate for the other four CLOs are far from impressive. The highest is a 3 month LIBOR rate + 425 bp. Although I will very much like to see STAM enter the European debt market to pick up a couple of distressed assets at way below face value, it is most likely be that the performance of any new assets purchased will be close to that of the CLOs.

With all that said, the amount of cash it will potentially be holding on to is making it very tempting to pick up some shares in the company.

Drizzt

Sunday 25th of March 2012

hi FROI, you couldn't have done a better digging then i did. The Sealene bond was the standout, but you may be right that the margin of safety for these distress loans would be much less during a better economic climate. STAM looks to be an opportunist in this area so it is hard for me to believe they would go for something safe with an unleavaged 6% ROA.

As of now, STAM could screw the investors by blowing this cash injection the way Babcock did.

Drizzt

Saturday 17th of March 2012

quite true uncle.