China Merchants buys new toll road; plans more acquisitions, placements

Jiang Yanfei, CEO of toll-road operator China Merchants Holdings (Pacific) (CMHP), is on a fundraising drive to finance the recently completed acquisition of the Yongtaiwen …

Jiang Yanfei, CEO of toll-road operator China Merchants Holdings (Pacific) (CMHP), is on a fundraising drive to finance the recently completed acquisition of the Yongtaiwen …

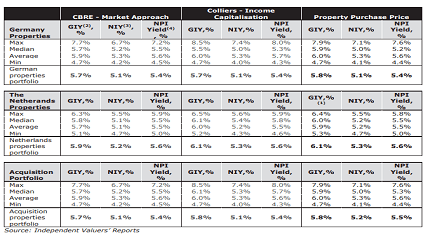

SGX Listed Frasers Logistics & Industrial Trust (FLT | quote: BUOU) over the past week proposed an acquisition of 21 properties in Germany and Netherlands. …

SBS Transit currently has a market capitalization of $802 mil with 311 mil in outstanding shares. This is one company that I have invested in …

Not too long ago, Frasers Logistics and Industrial Trust announced that they will be acquiring a portfolio of logistics properties in Australia. I am gonna …

We are winding down the year end, but for industrial real estate investment trust Sabana (dividend yield 9.3%), they are not taking it easy. We …

When prospecting listed companies to buy, good companies might not always have a lot of cash. You cannot prioritize cash being higher in the decision …

Japan based retail business trust Croesus Retail Trust made an acquisition with debts and rights issue. Current Share Price: $0.85 Last Dividend per Share: $0.0808 …

At the start of 2013, I selected 20 small cap stocks listed on SGX that I thought would do well, and allocated $10,000. I put …

I got into a discussion recently when someone highlighted that an Yishun flat is still rented out for 7.8% yield and have helped another landlord …

If you are looking to start purchasing individual stocks listed on the Singapore stock exchanges SGX and Catalist, your best bet to get information is …