Working in a wealth advisory firm made me more acutely aware of different aspects of the business.

I don’t handle client servicing but if you work in a narrow, humble conservation shophouse, there are times when I have to double hat as the coffee auntie so knowing a little about what not to do might be useful in helping the firm not lose a couple of million dollars in AUA.

A couple of days ago, I came across this short post from Rivershedge. Rivershedge is written by a 63-year-old retiree who spends part of his retirement time meditating deeply over the serious risk-management considerations of retirement income.

In the two latest posts, the author of the blog (let us call him RH for short) shared with us his rather painful experience with his former financial advisory firm, which lead him to leave the firm and use a fee-only adviser.

The context is in the United States, but you may find the experience familiar.

He started off with two statements from his former adviser, in two different situations:

- “Live a little bro…”

- “I gotta make a (commission) living, too”

The first comment is directed at RH over his very careful spending rate. If you read his content (and grow to understand them), you would realize that he probably knew a lot more about the box surrounding what is considered safe and unsafe in retirement income than a lot of certified advisers.

His conservatism is not without reason, as he does not have a pension and has to fully depend on his portfolio. That statement basically reveals the disconnect between what is considered safe enough between two different people.

And I get that a lot myself as well.

I get enough of this kind of disconnect when I discuss some of these financial planning risk management stuff with others. I am quite sure there will be enough people that came away with the thought “Why does Kyith fuss over this aspect of financial planning when we already have a ‘workable conclusion’?”

Usually, in these kinds of situations, either RH is overly conservative and doesn’t know it, or the adviser is too unsophisticated about retirement income. Or somewhere in between.

As an adviser, it might be important to listen to others better and in this case, sadly I think it is a case where RH explained a little, and the adviser decided this freak client is worrying over nothing.

The most important thing is that the adviser failed to untangle some concerns that the client has: Financial security risk management.

The second statement was made after he wanted to discuss the reduction of the fees charged. And some of you might be able to identify with this.

After his divorce, RH realizes that the fees reduce his spending rate. Originally, RH had a female adviser and trust developed. But as his net worth (I think) went up, she handed him over to a person in the Wells Fargo private/IFS system.

If I was to pay a fee, I would expect adequate sophistication. Any evidence of a lack of sophistication undermines the fee justification.

Two years after he got this replacement adviser, RH needed him to handle a complex split process due to his divorce.

After promising that “he got this”, in the middle of his traumatic divorce and the great financial crisis of 2008, the adviser disappeared and RH got orphaned. There was no one RH could turn to except for a team, which is a bunch of 20-something back-office types, who messed up his divorce split, even after being told 5 times what he wanted them to do.

If you read, the customer experience at Wells Fargo is kind of lacklustre and aggressive when threatened.

RH eventually fired Wells Fargo and went with a fiduciary adviser.

Why do Sophisticated People still need an Adviser?

If you try to read some of RH’s past write-ups (I really mean try), a question that may pop into your head is why RH still need an adviser.

It is even more remarkable that before his divorce, he did not know the trading, investing, modern portfolio theory, retirement finance, and writing that he knows now.

If you are motivated the right way, with urgency, given adequate time as a retiree, and are very focused, then you can reach a level of mastery that even professionals cannot achieve.

RH shared more about his divorce and why he still makes use of an adviser today in this follow-up blog post.

Basically, he found the right adviser that matches his needs and negotiated the terms of service with the adviser so that he shares part of the work and the adviser handles the rest. After the discounts, it worked out to be 60 basis points compared to 125 basis points if he were stuck at Wells Fargo.

RH framed this cost to be equivalent to what used cost of a mid-tier unit trust.

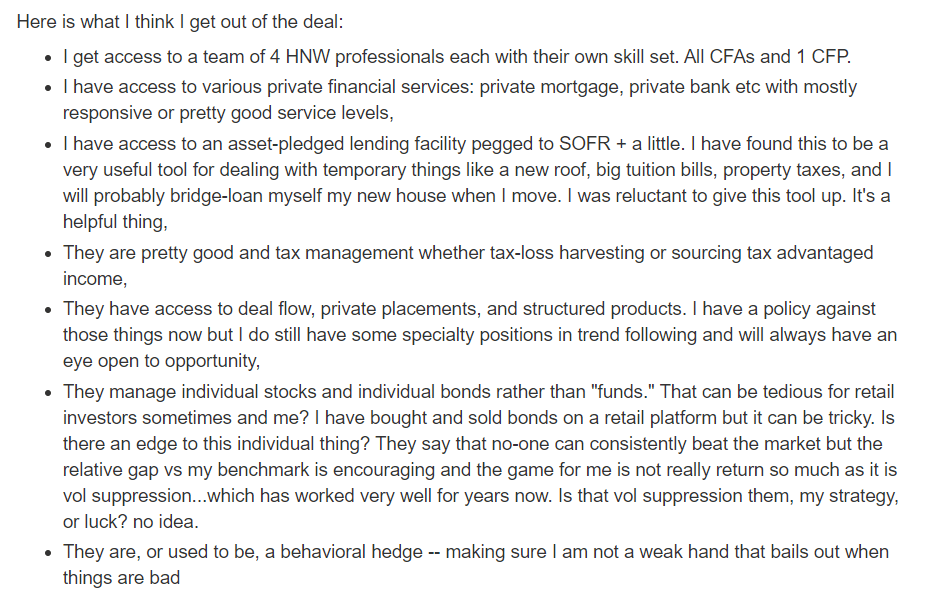

It is also interesting to see from his perspective the range of services that may appeal to him:

RH cited an assortment of services which mainly are good-to-haves or services that he may need but not on a periodic basis. It is damn difficult to know when you need them and when you do, you want a quarterback that knows your personal situation to help you communicate your needs to the tax and legal professionals.

The truly sophisticated people would also recognize the value pretenders of sophistication failed to see.

However, they are also under no illusion that there is an optimal price to pay for the value.

Why?

Financial math in reality.

If the initial safe rate of spending is 3-3.5% (as an example) and your recurring cost is 0.60% a year, then how does that impact how long your money would last?

Conclusion

I derived three big takeaways from RH’s two blog posts.

The easiest one is maintaining the level of sophistication, trust and execution, with enough care is what will build strong client-adviser relationships that last.

The other two takeaway is less clear.

The second one is… be careful about dismissing a client or prospect’s concerns if you have not spent enough time exploring why it is a big deal to them. If we do not untangle some of these major knots, they might be less assured to listen to anything we say.

It also makes me try and pay more attention if someone keeps circling back to a point again and again. Just recently, it took me a while to detect a point that a colleague was trying to impress upon me. I think over time, I realize that understanding that point and its implication was something the person felt important enough for us to be aware of, and that made me go out of my way to try to understand it better. If you want someone to understand you, you should do the same as well.

Lastly, an observation of the space and discussion with some is that the real sophisticated people can make better clients. If you price your fee correctly. This is a debate that I sometimes have, and despite my sophistication, I often ended up on the losing end of the argument.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024