Been a while since I talked about IREIT Global and since I was facing some glitches with Investment Moats, I might as well give some updates. Btw, do let me know if the Singapore Prices of the Stock Portfolio Tracker is still not being updated or served.

IREIT Global gives a dividend yield of 7.5% on my Dividend Stock tracker. This is pretty high if you compare to the local and even the office REITs with international properties but listed on the SGX.

This is a Germany based REIT where the management changed.

In this first quarter results, the dividend per unit went up 1.4% year on year mainly due to more favorable hedging.

Revenue wise, the result was poorer. This is due to lower rental income from Munster south Building following the vacation of one floor with effect from Apr 2017 and finalization of prior years service charge reconciliation and increase in non recoverable repair and maintenance expenses.

The management took a more unit holder unfavorable decision to reduce their payout from annual distributable income from 100% to 90%. This reduce a juicy 8%+ dividend yield to a 7.4% one. The management are still taking management fees in units.

One of the reason for the good result was the very favorable hedging of S$1.63 to 1 Euro. They hedge it at a high. This translate to a better dividend yield.

All this seems likely to change, with the announcement that from 2019, in accordance to its currency hedging policy, IREIT will be hedging income to be repatriated from overseas to Singapore on a quarterly basis.

IREIT and the previously listed Croesus Retail Trust were the guys that practice longer years hedging, and some shareholders favor it. In my opinion, it is like trying to avert a fear that you know its going to happen sooner rather than later.

They are expecting the management to market time the currency. Not always going to work well.

The change in hedging is something we should take note of.

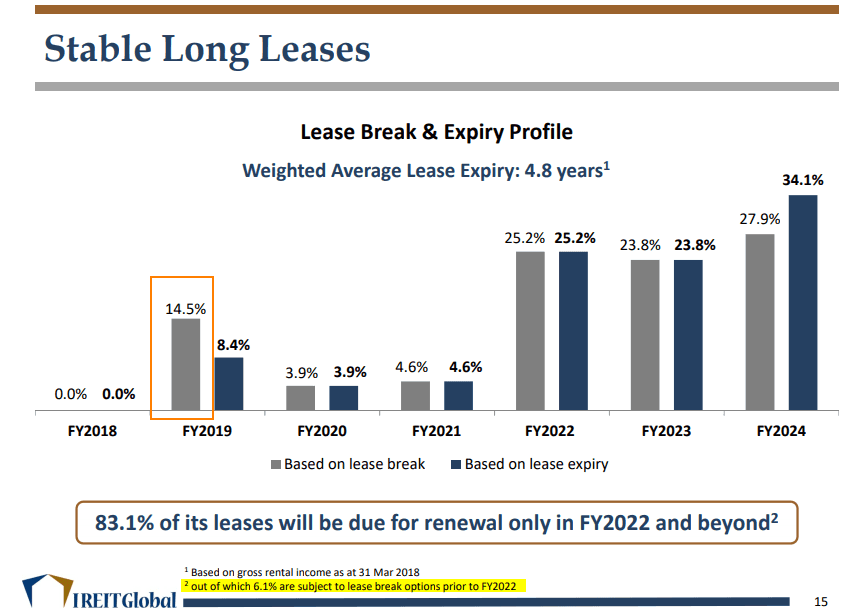

Another potential problem area is that while FY2018 brings no expiry, in 2019 we have some potential early break in lease. This could result in a larger amount of vacancy.

Why this is a concern, is the narrative.

These leases was part of the IPO package. Usually these sale and leaseback can be seen as a way for the owners of the property to sell to another party at a good price. To sell at a good price, they continue to rent from the people that they sell to (in this case IREIT) at an attractive rent structure.

However, the tenants (previous owners) may not renew the lease, and it might not be so easy to find a new tenant.

If that is the case, then IREIT’s shareholders end up with a problem rather similar to local REIT Sabana.

Potentially, 6.1% of gross rental income will be impacted and this is a test of management capability.

How probable would the manager do a good job? For a REIT with short history investors tend to be rather unforgiving there. IREIT has a floor in Munster that was vacated, and till today they have yet to update whether they are able to fill it with tenant.

Do share with me your thoughts.

I shared more about stuff on REITs like this in my section on REIT where I go deep into the weeds of investing in REIT. It is FREE and available:

If you like this do check out the FREE Stock Portfolio Tracker and FREE Dividend Stock Tracker today

Want to read the best articles on Investment Moats? You can read them here >

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Pythia

Friday 11th of May 2018

I wish they'd just drop the whole hedging thing and paid their dividend in Euro, as Cromwell REIT does. Hedging seems counter productive, for one thing there's about as much chance of the currency going up than down, but the hedging cost money (so the net statistical gain is negative, as it is with any insurance). For two, hedging last only so long so sooner or later, you have to deal with the currency variations. The hedging just delays it by a few months.