Singtel just declared their 4th quarter 2011 results and full year results.

Among the highlight is that they are boosting their dividends from 14.8 cents to 25.8 cents. This is made up of a regular dividend of 15.8 cents and a special dividend of 10 cents.

A total of 19 cents will be paid out this time.

At the current price of $3.16, the yield inclusive of this special dividend is 8.16%.

Without this 10 cent special dividend, the 15.8 cents dividend represents a dividend yield of 5%.

In finding the dividends cash king, I talk about Singtel paying out much less of their free cash flow compare to Starhub and M1, and have more room to grow.

The question on everyone’s mind is that are they paying out too much to make Singtel attractive as a stock?

Singtel’s Dividend Policy

Singtel doesn’t have a policy of paying out a consistent dividend like Starhub, which tries to make their shares attractive by declaring a 20 cent dividend.

This has led to one international dividend income portfolio manager being unable to add Singtel to his portfolio despite seeing the moat in Singtel.

The closest thing to a policy is that they will pay out within 55-70% of their Net Profit After Tax.

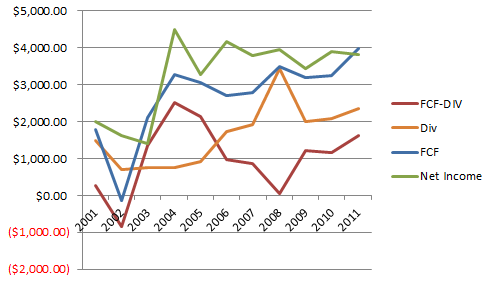

The Net Income for FY 2011 is $3822 million, which is actually lower than FY2010. From the green line in the above chart, you will see that their net income have been stagnating.

How much is a 25.8 cents payout? That is about a $4100 million dividend payout.

A 15.8 cents regular payout is about $2350 million dividend payout.

If we talk about this $2350 million it is an increase of 14% from FY2011’s payout of 14.8 cents or $2084 million.

$2350 million represents 61% of FY2011 Net Income after tax.

If we push their dividend payout to 70% which is the max of their policy, the amount will be $2700 million. That translates to a rough dividend yield of 5.75% at current price.

If you are an income investor looking for Singtel to increase their dividend payout, and knowing their net income have not been increasing since 2003, the max payout at current price you are looking at is 5.75%

Will special dividend be finance by existing cash or debts?

Lets not kid ourselves that Singtel will always pay out 8.2% yield from now on. This is a special situation that Singtel arrange and the last time they did that was in 2005 and 2007.

Companies typically pay out special dividends when their cash holdings becomes big enough.

For Singtel’s case, their cash holdings did increase from 1.6 billion to 2.7 billion, but that’s hardly big consider their 1 year net income is already 3.8 billion.

Back to our chart above, the blue line represents the free cash flow, and it has been increasing consistently versus the net income. FY2011 free cash flow stands at nearly $4000 million compare to $3200 million in FY2010.

If we talk about paying out this total of $4100 in dividends, they have the capability to pay out entirely with their free cash flow. This is a great because essentially it means Singtel do not need to touch their cash or take on more debts to appease the share holders.

It also means that if you think Singtel’s business is going to be doing as well as FY2011, their actual capability of generating cash for dividends is actually yielding 8% which is up from 6.7% in FY 2010 and 6.5% in FY 2009.

I always say that it is probably more meaningful to use a % payout of Free Cash Flow instead of Net Income as a gauge of prudence in dividend payout but guess most companies will stick to net income.

The devil is in the details

Why is there such a bump up in free cash flow from 3200 mil to 4000 mil when net income is reduced?

I been asking myself that question and really a study of their cash flow statement didn’t yield a lot of favorable results.

For one thing Singtel’s official free cash flow of 4000 mil takes out $669 mil in Investment in associated and joint venture companies. Adding this into the equation and the free cash flow is actually $3300 mil, which isn’t far off from $3200 mil. Singtel is trying to pull a fast one on us!

It can be argued that this 669 mil was intended to be funded by Notes and Cash Holdings, but we are talking about prudence here and if they want to show that they can pay the dividends from free cash flow they should take off this 669 mil.

The increase in free cash flow is more or less due to 2 items, a reduction in share of results of associated and join ventures companies and an increase in dividends received from associated and joint venture companies.

This in total translates to about 500 mil in difference.

It goes to show that the future of Singtel every one of these companies from Telkomsel, AIS, Globe and Bharti needs to do well to pay us enough. failure to and dividend growth is likely to stagnate.

Business actually declining

In terms of business, they aren’t having a great time.

- Net Profit Margins declined from 23% to 21%. This is not good as more investments will result in poorer takings.

- Singapore’s EBITDA actually decline despite gaining more market share.

- OPTUS have been a great performer. EBITDA rose 8%. This offset much of the bad results elseware.

- Bharti is still the main reason for the stall in growth engine. This may or may not improve in the near term. A profit reduction of 567 mil vesus 834 mil a year ago.

- AIS have been a good performer but it is only a small portion of Singtel’s portfolio

- Telkomsel is not growing as well.

Conclusion

My opinion is that we should ask ourselves if a 5% yield at current price is a good return for the risk in investing in Singtel.

I had a chat with my colleague who thinks that Singtel is the best stock for risk-adverse investor.

I tend to agree if what you want is a stock that is well diversified, provides little growth in income and capital gains. This is a stock that is likely to be in a great shape should another recession comes along and I will pick up more at lower price as my yield on cost will be higher.

Still, with all these growth in the next 2 years, I doubt it will beat Starhub’s 7.2% yield, which provides greater income and growth.

The common fallacy is that Singtel has growth, Starhub and M1 do not, but if you look at their results, Singtel hasn’t been growing much in terms of income! They just been paying out more cash! They have been investing in growth but that doesn’t mean they are getting what they want.

Still 5% yield is great as the payout of free cash flow is 70% and if they payout all their free cash flow it is 6.7%. I just wish that their ventures will not have those big problems.

If 5% is too low for you, take a look at the other Singapore stocks in the dividend stock tracker, they have much greater returns but also much greater risks attached.

I run a free Singapore Dividend Stock Tracker . It contains Singapore’s top dividend stocks both blue chip and high yield stock that are great for high yield investing. Do follow my Dividend Stock Tracker which is updated nightly here.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Thai. Fook

Wednesday 15th of May 2019

What is divident is Z77 distributing date? How much shares holders will get?

Kyith

Friday 17th of May 2019

Singtel is Z74. You can check out how much dividend you can get as shareholders if you go to the SGX.com > Corporate Actions. Search for Singtel.

JS

Sunday 22nd of May 2011

Hi Drizzt,

SOrry for asking a noob question that is, if i buy a stock e.g. Starhub before its Dividend announcement date, will i still qualify for the dividends? And how do i receive and how often are the dividends paid?

thanks so much for answering my enquiries and other than starhubs, what other high yielding dividend stocks with margin of safety is recommended?

Regards JS

gregg

Saturday 14th of May 2011

Hi Drizzt,

Looks like selling pressure going to weaken stock market in May, any best defensive stock to buy in?

I am trimming my stock counters, sold Etika and Breadtalk and bought in Singtel (only 1lot) and added 6lots of First REIT.

I believe all of us are waiting for the correction so that we can accummulate more high yield stock like Starhub, REIT.. etc...

WealthBuch

Friday 13th of May 2011

Hi,

My opinion is, are we thinknig too long, too hard, too much, over Singtel?

Too much analysis could cause paralysis.

Singtel is a highly manipulated stock in SGX. No matter how big a company everyone says it is, it is still a tiny blip to international funds.

It shouldn't and wouldn't beat Starhub's yield. This is a special dividend, and special dividends could be one-off events.

Simply put, I bought and will continue to buy this without much thinking as long as it is under $2.90. To me, it's a good return on my time as well.

Just my 2 cents. :)

Drizzt

Friday 13th of May 2011

hi Wealthbuch, yeah its abit of paralaysis but what i love to delve on is to prove or disprove a common idea, whether there is any truth in that quantitatively.