There is this article from Clear Eye Investing I would like to share. It touches on some problems that I observed recently during the REIT ran up as well as some investors.

There is an absence of looking at the importance of valuation.

In most models the much discussed aspects have been the Business, the Cash Flow nature, and the operation conditions.

With that in mind, a stock like SATS with a business model that does seems very sturdy when it was announced we will have terminal 4 and 5.

Some will look at 4-4.5% as a good return with a 3% growth rate and buy based on that premise.

At times the share price of 3.40 could have already baked in a 4% yield growing at 3%. In fact, to be worthy of 3.40, the growth rate would need to be 7-8%.

Is that possible? Perhaps. You have to be right on the conditions for it to grow above average.

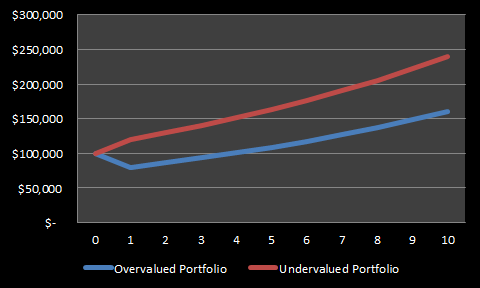

What happens if you overpay?

Consider two investors that each invested $100,000 in dividend portfolios with 5% starting yields. Over the course of ten years each investor realizes annual dividend growth of 3%.

The first investor (blue line) bought stocks that were considerably overvalued and subsequently lost 20% in capital value in year one; alternatively, the other (red line) invested in stocks that were undervalued and gained 20% in capital value in year one.

After the year one corrections to fair value, both portfolios grow at 8% per year through year 10.

At the end of ten years, both portfolios generated the same amount of dividend income ($57,319), but their ending capital values are nearly $80,000 apart ($159,920 vs. $239,880). It’s hard to imagine that the two investors would feel equally good about their performance even though they realized equal dividend income over the ten year period.

Dividend is only one kind of shareholder return. An asset listed price on the stock exchange could have baked in that X no of years of cash flow yield growing at Y% + a Z amount of premium.

Don’t think you guys would like to pay $2000 for a IPAD (Which is a great product).

[Clear Eye Investing | An Easy Mistake Made by Dividend Investors]

To get started with dividend investing, start by bookmarking my Dividend Stock Tracker which shows the prevailing yields of blue chip dividend stocks, utilities, REITs updated nightly.

Make use of the free Stock Portfolio Tracker to track your dividend stock by transactions to show your total returns.

For my best articles on investing, growing money check out theresources section.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

greenrookie

Sunday 27th of October 2013

"At times the share price of 3.40 could have already baked in a 4% yield growing at 3%. In fact, to be worthy of 3.40, the growth rate would need to be 7-8%"

Hi Drizzit, Can you explain why to be worthy of 3.4, the growth rate would need to be 7-8%?

Kyith

Monday 28th of October 2013

Hi green rookie, not as a dig at SATS but mainly using SATS as an example here.

Tan KangKai

Sunday 27th of October 2013

No doubt that car population (due to Coe ) will be restricting the profit growth but hoping high pricing would bring in high revenue ...

Kyith

Sunday 27th of October 2013

What do you mean high pricing. Restricted car growth is supposed to be a good thing for Vicom

Tan KangKai

Sunday 27th of October 2013

Hi drizzt, I am agreed that we should look for dividend stock that come with potential dividend growth,typically low payout ratio, my bet on silverlake ... It already grew to 6%base on my initial cost (was 3-4% at that time)....hoping to add more Vicom in coming months ....

Tan KangKai

Sunday 27th of October 2013

Hi drizzt, I am agreed that we should look for dividend stock that come with potential dividend growth,typically low payout ratio, my bet on silverlake ... It already grew to 6%base on my initial cost (was 3-4% at that time)....hoping to add more Vicom in coming months ....

Kyith

Sunday 27th of October 2013

To argue that perhaps your Vicom growth rate you may be expecting a rather generous one. The question is whether that growth rate can substantiate it