We went through some policies such as Aviva’s MyRetirement Choice and OCBC PremierLife Generation showing the projected returns the policyholder could potentially get.

Through the article, we realize that the biggest determinant of the policy performance is in the investment return of the participating fund.

This is because the participating fund is the investment fund that provides the return for the policy.

Typically, to be able to sell these endowment or retirement policies, the insurance salesperson would need to make some projection of the investment return that you are able to earn.

So how is the return in reality compare to the investment projections in the past?.

Today, we look at some historical returns.

What You Need to Know About Your Insurance Policies’ Participating Fund

For the uninitiated, we can group insurance protection into 2 groups:

- Those policies with cash values

- Those policies without cash values.

Your whole life insurance, limited whole life insurance, insurance savings endowments, and universal life policies are policies with cash values.

When you purchase such policies with cash values, you are TRANSFERRING the job of building wealth to the insurance company.

Your insurance premiums paid contribute to participating funds, which are either the main funds or sub funds formed by the investment managers in the insurance companies to meet the objectives of the various cash value insurance policies.

How well your insurance policies do eventually in terms of returns will depend on the performance of the participating funds.

The participating funds invest in a combination of:

- equities

- government and corporate bonds

- property

- cash

Every year, if your policy has some sort of cash value that links to a participating fund, they will provide an update on investment returns and their current allocation to these asset classes.

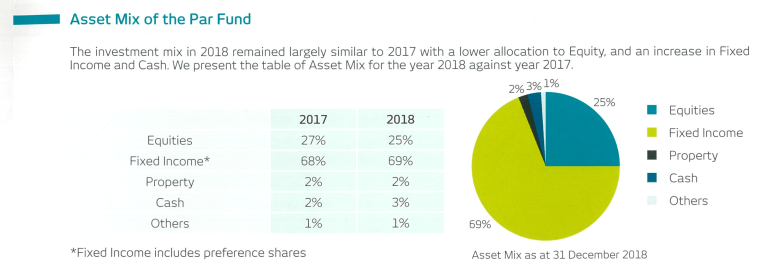

Here is an example of the allocation of the participating fund of my Tokio Marine Limited whole life plan.

The following is taken from the Benefits Illustration (BI) , which explains your policy in detail.

The surrender value illustrates to you the projected surrender value you could get, if you liquidate your policy at that specific year, or age.

Notice that there are 2 sets of figures, one for projected at 3.25% investment return and one 4.75% investment return.

This is to give you an illustration of the potential of your policy.

The sales conversation often is lead in such a way that the insurance adviser and the client were discussing as if the 4.75% return is given.

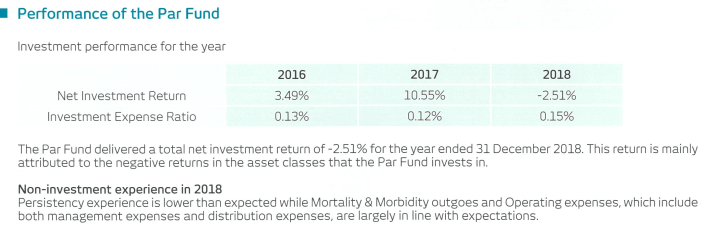

In their annual update, the insurance company will also provide you with the latest performance.

Here is how mine look. One thing you will realize is that… on a short term basis, the net investment return look not so different from your other unit trust portfolio.

These returns are abstracted away from you. They are published only once a year. Thus, unlike your unit trust or stocks, you are unable to see the volatility in the portfolio so much.

This is not the net return that will into your endowment or whole life plan. There are still commission and other costs to net off.

The insurance companies will also smooth out the returns that you will eventually see. This means that they reserve returns during the good years so that they can supplement those years where returns don’t do so well.

Net Investment Returns is Not the Returns You will Eventually Get

If you read your benefits illustration, they will tell you that your projected returns depend on the investment performance of the fund.

There are cost deductions from the returns of this fund.

What this means is that the returns that you will see are LOWER than the net investment returns you see in the illustrations.

The best way to think of the net investment returns is:

If it hits 4.75%, you will likely see what was projected in the benefits illustration when the policy was first sold to you.

If it hits 3.25%, then most likely the returns will be at the lower end.

Let us take a look some data.

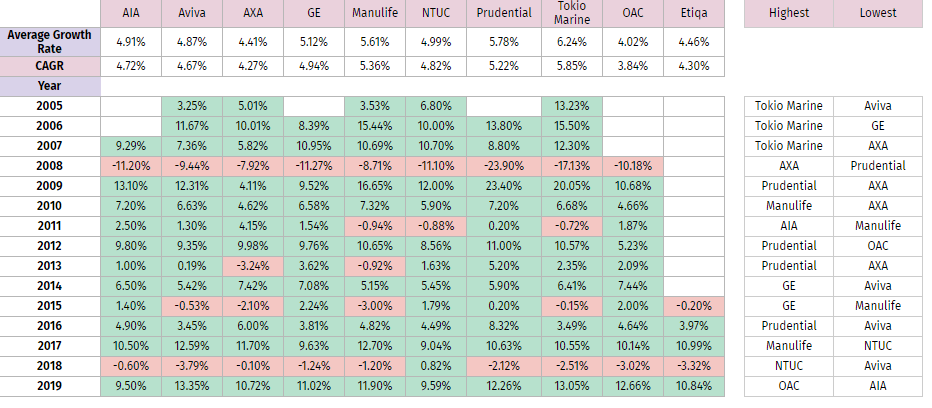

The Investment Return Performance of Participating Fund Year on Year

Various sources have provided the historical net investment returns of the participating funds.

Here is my own compilation.

The first observation is that while you do not experience any volatility, what underlies your policy is no different from equities and bonds.

Their returns fluctuate over time.

I tabulated the best and poorest performing fund for the year. What we observe is that they do not stay constant.

There do have some constant names. AXA appeared the most in the poorest years. Prudential appeared the most in the best years.

Some Insurers Were Able to Clear the 4.75% Hurdle over Long Term

If we observe the 12 to 14-year average, some insurer was able to hit 4.75%:

- Manulife

- Tokio Marine

- Prudential

No surprises as Tokio Marine and Prudential appeared the most in the best returns in the previous table.

Lower Bond Rates Will Affect Future Insurance Participating Fund Returns

The market returns for the past 5 years have been respectable.

However, if we look at the shorter average, you cannot find one insurer that can consistently hit 4.75% a year return.

Based on MAS Guidelines, most participating funds will hold more bonds than equity.

Typically, the equity to bonds/cash/property allocation is 35% to 65%.

In such a low yield environment, it will be rather challenging for the funds to achieve that 4.75% returns unless they

- Shift more to the more volatile equities

- Take on bonds at a higher end of the risk spectrum (like high yield, emerging market bonds)

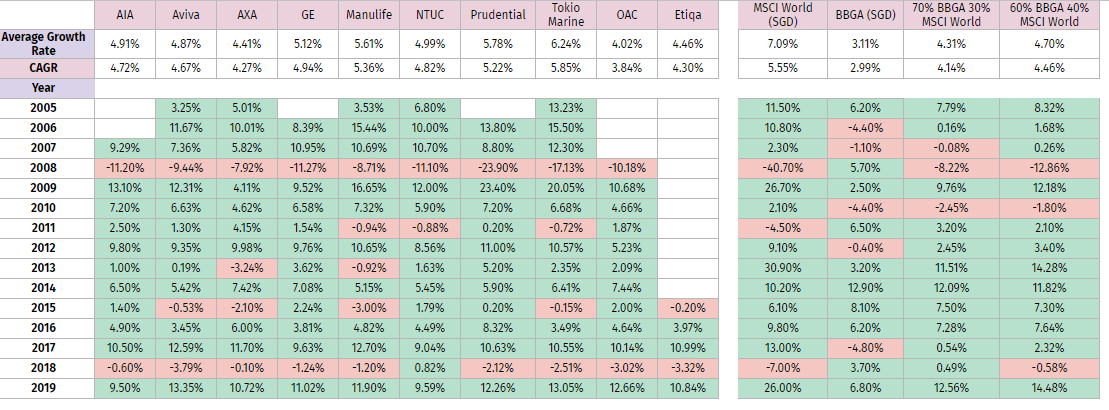

Comparing the Performance of Insurance Participating Fund Versus a Portfolio of Low-Cost Index Funds

There are a lot of propoonents that believe that you could do better than this if you invest on your own.

Not everyone can invest on their own. However, the closest thing to a passive investment is to add on to a portfolio of low-cost index funds or ETFs.

The biggest problem I feel is that they are not doing an apple to apple comparison.

They will compare the participating fund returns versus a 100% equity ETF.

This to me is unfair because the 100% equity ETF is more volatile, higher in the risk spectrum. Part of the investment objectives of the participating fund may be to ensure that the volatility is lower so that the returns are more predictable.

This is a constrain and you have to factor that in when you are comparing.

A more appropriate comparison would be either a

- 40% MSCI World Index 60% Bloomberg Barclays Aggregate Bond Index

- 35% MSCI World Index 65% Bloomberg Barclays Aggregate Bond Index

So that is what I did:

On the right, I have included the performance of MSCI World and BBGA (Bloomberg Barclays Global Aggregate Bond) in SGD as well as the two different allocation.

If you compare the average growth and CAGR, the passive option might not be better.

The returns are lower.

I got a feeling that by using MSCI World, it might not be fair. The funds in this region like to invest in Asia ex Japan.

Comparing against MSCI Asia Ex Japan might be a better proxy. That will be for the next update.

My conclusion is that those who say they can do better, yet be more passive, are doing an unfair comparison.

Summary

Here are some general takeaways that I hope you will have:

- The cash value of your policies are determine by the performance of the insurers’ participating funds

- Each insurer can have more than one participating fund. Some of their paritcipating fund may be more conservative in their investments

- If you peel off the layers, what drives your returns are no different from your unit trust, stocks and bonds. The difference is that it is managed differently by someone

- Peeling off the layers, the investment returns follow market forces.

- Think of the projection as a hurdle rate rather than the returns you will see

- Most partcipating funds have a high proportion of bonds. Current bond yields indicate future total returns that you can get from bonds. This likely points to lower future participating fund returns unless they take on more risk

If you would like to find out how is the performance of some matured insurance savings plans of my friends and family, you can read Does your insurance savings plan give you 3% to 5% returns?

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

GW

Wednesday 15th of September 2021

You did not even consider the expense ratios incurred by the funds. The investment returns stated above are gross returns. Hence, your article is highly redundant and inaccurate to asses the peer-to-peer participating funds.

Kyith

Wednesday 15th of September 2021

Hi GW, I think what I am doing is explaining how some of these things work. This information is available to the public. The expense ratio vary from insurance company to insurance company.But I think it is also good for readers to appreciate the performance of the participating funds, before the expense ratios.

The idea is to encourage readers to think.

Perhaps you have a table that compares the performance of participating funds (after cost) over long time periods? I am ok to do an update to this article if you are open to sharing.

Divy123

Tuesday 23rd of January 2018

Hi Kyith do you have any information on distribution costs levied by the major insurance companies on their endowment /regular payout policies? I have recently been asked to consider the NTUC VivoWealth Solitaire plan which sounds quite interesting on the surface ( capital protected with regular monthly payouts from year 6 until year 100. projected payout quoted at the usual 3.25% and 4.75% return. I notice that the distribution cost per year ( for a lump sum placed of 500k) is $39450 per year (7.89% of principal sum) which seems quite high to me. Any idea how this compares with other similar plans? Thank you!

Kyith

Sunday 28th of January 2018

Hi Divy123, no I do not have that information unfortunately.

Dennis

Tuesday 9th of January 2018

I think when we look at the 4.75%, we are looking at it like a compounding basis.

Therefore the 11 years average we are looking at is not that accurate to be exact.

If we want to, we should derive the individual year participating returns and compound it so as to get the actual returns on a compounded basis.

I have done the calculation on Prudential one and notice that the compounded figure is 4.10% only.

Individual Year Returns 2016: 7.95% 2015: -0.03% 2014: 5.2800% 2013: 4.4400% 2012: 9.6600% 2011: 0.48% 2010: 6.5200% 2009: 20.900% 2008: -23.9700% 2007: 8.4700% 2006: 12.00%

For Manulife, Effective Rate of Return is 4.56%.

Although the performance does not seem to hit 4.75% no matter what, it should be good to assume that they are able to deliver approximately 3% compounded basis returns to client as most of the policy assumes returns of approximately 3.3% based on 4.75%.

Guess it serves its purpose of hedging against inflation and forced savings.

Kyith

Wednesday 10th of January 2018

Whoa, Dennis thanks for pointing that out. After I wrote this, I was thinking maybe i am comparing arithmetic and geometric addition, which is a bit wrong. But taking average geometric addition is also not accurate. I suppose they have their reasons for using arithmetic maths. In any case, the numbers are lower but orders are the same.

Winston

Monday 21st of December 2015

Hi Kiyth,

In the older days, there is only one maturity value, hence buyers did not have anchoring beliefs. Naturally, they have to settle for whatever figures were projected, a case of WYSIWYG.

The key point is that insurance companies have experts to do such projections. It is within their management power to manage these objectives. If they believe such projections are unrealistic, then lower them, nobody forced them to do it. Further, endowment premiums are invested over a long period of time typically 20 years or more, to so call smoothen the returns. With these, is it fair for buyers to lower their expectations? Shouldn't the companies find ways to lower expenses and improve returns?

Imagine the Government reducing committed CPF interest, do you think voters will be so forgiving? Private sectors are supposed to be able to perform better than Government,.

There should be some form of governance or laws by the Government to prevent irresponsible companies from inflating projections. Otherwise, buyers may be hookwinked and they have no recourse against the non guaranteed clause.

During the GFC, capital protected phrases were used in place of guaranteed. Now you don't see this anymore. Perhaps it is time to let the non guarantee clause go too.

Having said this, endowment is not exactly a bad product for those with no time to monitor other investments. However, consumers must look for companies who can be trusted to deliver what they projected. What this means is to ask the companies to provide this information and compare them. Caveat Emptor is easier said than done if past maturity paid out information out is unavailable. For those detractors advising past performance does not reflect the future, can they provide a better alternative?

Perhaps you can ask your reader to share the actual percentage maturity value paid out vs projections so that we have more information on which companies are more trustworthy.

Kyith

Tuesday 22nd of December 2015

Hi Winston, thank you for the detail reply. It will be difficult for the readers to show that. I can try but it is likely they dun have the papers haha. Then again the projections should be in the original policy.

We already have too high of a compliance cost. The insurance firms are like an oligopoly. The game theory states that staying in this status quo is better for everyone, so why be the smart alec and try to disrupt.

We needed someone to do that. But to be honest it is difficult to change people's perception. Their need for cash value is still overwhelming.

When they see their insurance do not have cash values they think they are not getting "insurance"

we have social media to influence people but it seems some of these stuff are still hard to shake off

Tan Siak Lim

Friday 18th of December 2015

Please do note comparison insurance product to investment. You are comparing apple to orange.

Insurance is primary for instant protection, and investment return. You pay $200/month, something bad happens to you, you get $200,000 if you are still alive, otherwise your love ones gets it. This is guaranteed. After many years, if nothing bad happens to you, congratulation, you get your premium back and perhaps some interest. Investment don't provide this feature.

You have just wasted all your time comparing return and miss the point....

josh

Saturday 19th of December 2015

It is ok to compare. But most PAR funds have >40% in bonds (My NTUC policy has 62%) which reduces the portfolio variance.

Kyith

Saturday 19th of December 2015

i don't think i missed the point here. the reason for a participating fund is that folks expect their policy to be a form of wealth building rather than protection. if they view it as that way then they have the intention to get sonmething out when they are alive. hence it is important to look into it.

why shouldn't we look at how the investment portion of an insurance company perform? would you want to benchmark how well the teacher teaching your child the right thing? I would.if you spend so much and send him or her to Eton house and turns out what they teach is really not all that better than what they teach in My First Skool, shouldn't that be important?