When I was inexperience in all these investing stuff, I had this fear that if I invest a large amount of money tomorrow, and the market goes down by a large amount, it will seriously mess me up.

And it did happen during the financial crisis.

We find it difficult to sleep soundly at night, because we are afraid that we will lose a large part of the wealth we put into investment. When you are near retirement, that fear is bigger, because if you lose more than 50% of your wealth, you do not have time to make them back. that will jeopardize your financial independence.

So financial institutions came up with questionnaires to segment us into categories depending on our tolerance to risks.

I find that there is a misunderstanding about what risk is.

I think people do not understand risk enough.

Or why it is important to build up a competency to understand risk.

Let me try to distill what I understand about risk, when it comes to building wealth in general.

This article answers some questions such as

- difference between risks and volatility

- the impact of risks

- how you can understand this and improve your wealth building

- how to sleep better at night

Which Wealth Machines does this article apply to

This applies to whether it is property, stocks and bonds, business building.

In general, if your wealth machine requires you to prospect them, and think about uncertainty, this is a good piece to read.

We think that Volatility and Risk are the Same Thing

When you talk to your insurance agents or financial planners, they often tell you that, to earn high returns, you need to take more risk.

They are not exactly correct.

What they meant to say is that, you HOPE that by taking on more risk, you HOPE the reward at the end of the tunnel is greater.

The reward at the end is by no means a given.

It doesn’t mean that when you buy stocks, after 10 years, your return from stocks is a definite 8%/yr compounded. It might vary from -4%/yr to 12%/yr for example.

Risk is a Deviation from an Outcome.

There can be positive risk or negative risk.

If you manage a project there is negative risk such as the raw materials that your construction is based on cost a whole lot more. But it could also cost a whole lot less, which is good for you. Is this what you were expecting? They deviate from your original outcome.

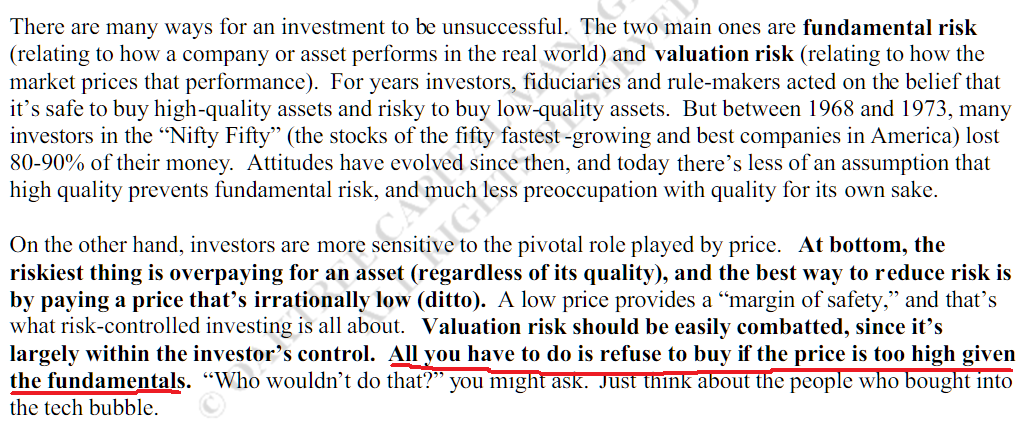

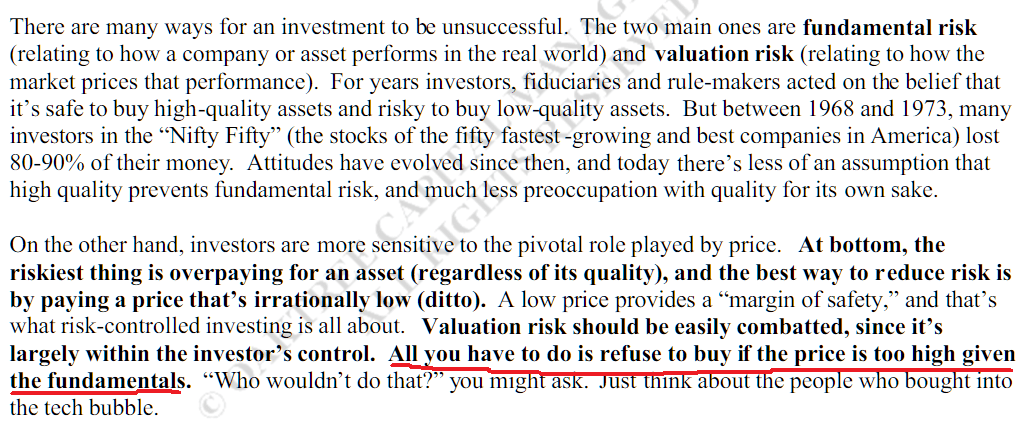

Howard Marks, Oaktree Capital Chairman writes a great newsletter on how we should look at risk. I will be lifting various portions from the news letter.

The first is his explanation of why risk is not volatility:

You have a negative risk when your investment outcome is not the same as what you originally plan for:

- your original investment cannot be recovered (go to $0)

- you lost conviction in the investment you bought, and turned an unrealized loss to a realized loss by selling

- the value of your investment fell by so much, because the business have negatively evolve so much that it will take a miracle to recover your original investment capital

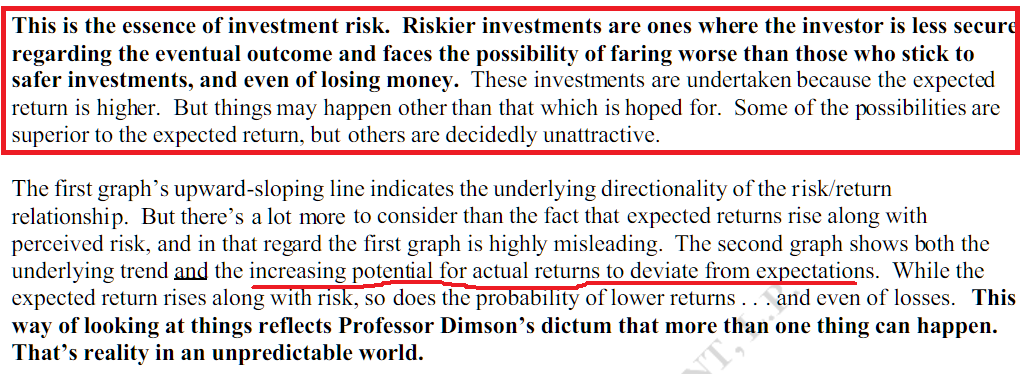

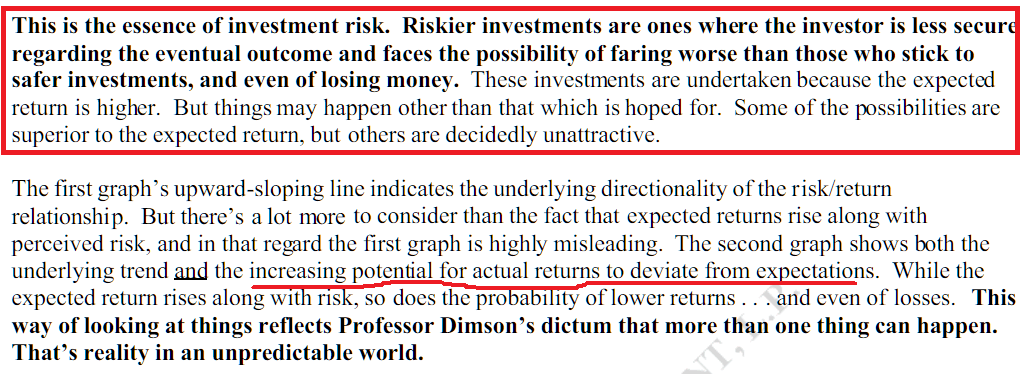

Mr Marks have probably the best illustration for return and risk.

We tend to look at risk and return as a straight line. More risk, higher return. Less risk, lower return.

We should visualize how we look at risk and return like this illustration here.

Here is how Mr Marks explains:

To explain, every point on the line in the illustration is a normal distribution. A normal distribution is how the returns of a sample of people taking the SAME level of risk gets. A normal distribution means that majority of the people taking the same risk will fall in the middle (the fat part of the normal distribution) and the minority will fall into the tail end.

This means that majority of those taking the same level of risk will earn an average reward, but there are the minority that will earn much better than average, although they took the same risk, and there will be minority that will lose badly, despite taking the same risk.

When your risk is low, the normal distribution shows that your returns might vary, but they tend to be always positive. You either get a little bit more or less, but you won’t lose money.

However, when your risk increases, the distribution of that risk point is much wider. This means that the range of outcomes for that risk point span a larger normal distribution. Starting from the third fan distribution, if you count from the left, the range of outcomes can be very good or very mediocre, but still positive.

That changes when you look at the forth fan. In some low probabilities, your long term return can be negative, which means that you risk capital loss. Or that you could shoot to them moon, in some low probabilities!

This means that when you take on more risk, you HOPE your average returns is close to what is the average on that risk point, or to the right of the average (where you earn exceptional returns despite taking the same risks as your sample), but NOT the left (because you would be losing money)

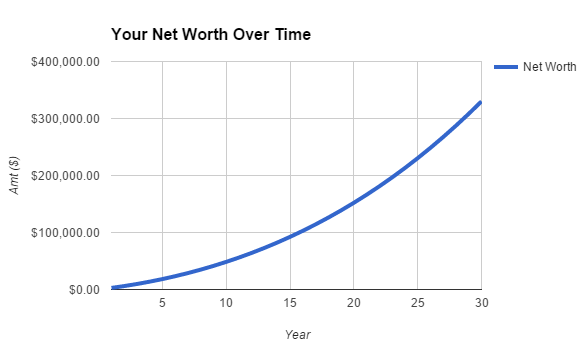

In wealth building, your intended outcome is like this:

This is what your financial planner, or investment manager will sell you.

A consistent wealth growth rate of 6-9%/year, compounding your wealth over time.

This is also what financial bloggers like myself sells you to make it simple for your understanding.

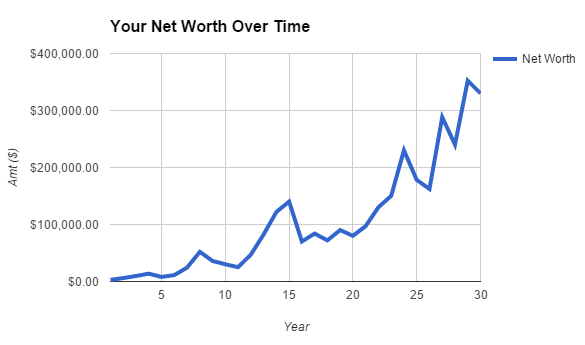

However, usually the reality is like the illustration above.

The prices go up and down. They don’t go straight up. In this sequence there are -22%, -49%,-30% declines but they are also 115%, 49%, 87% rises.

This is volatility.

At certain times, the prices deviate from the mean line, if you draw one line up. Different Wealth Machines, may have different volatility.

Notice this: In this net worth chart, your net worth ends up the same place as the smooth chart you see previously. The outcome is the same. Volatility is not risk.

What are the Negative Risks we are REALLY afraid of

If the outcome of our net worth eventually ends up where we THINK we will get to, then there is no risk.

We are afraid of these deviation of the final outcome:

- When your capital is permanently impaired

- When your wealth machine losses so much capital that they have no way of recovering

Both #1 and #2 may refer to the same thing.

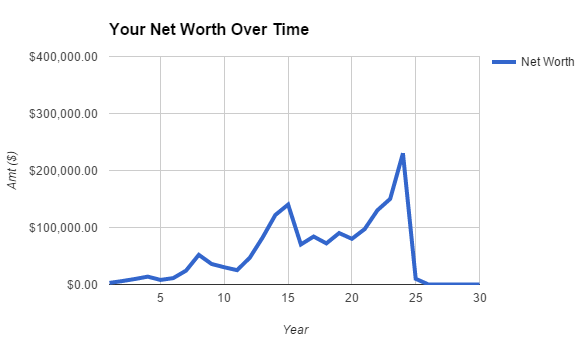

This is similar to the 2 charts before. The only difference is that at year 24, the wealth asset value went to $10,000, then to less than that.

This is a permanent loss of capital.

How is this possible?

Tell that the folks who put their net worth betting on a single stock called GTAT (read it here)

This is risk.

#1 is possible in the follow scenarios:

- Putting all your wealth in one stock and that one stock turned out to be a con job

- Being suckered into scams

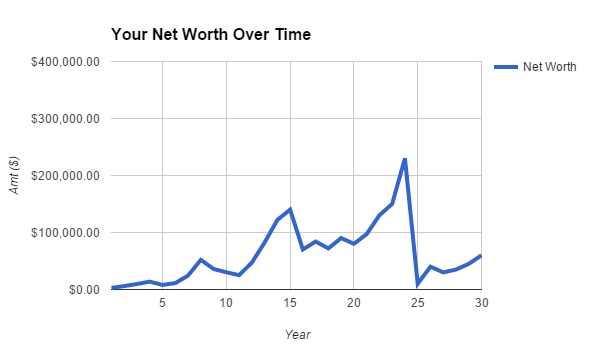

In more prevalent cases, negative risk outcomes is like #2:

This one looks similar to the one above, but this is not so bad.

Essentially your net worth loss so much that, even though its not zero, and there is every chance that you can cling on a slight hope for recovery, the hope is very small.

Your net worth is a much smaller percentage of your capital that it will be tough to recover back.

This is permanent impairment of capital.

If you are doing individual stock investing, that is, buying and selling a portfolio of individual stocks, here are some examples:

Ezra is in the oil and gas sector. While much of its recent woes can be due to the cyclical nature of the sector, purchasing the stock at the wrong valuation would possibly lead to large unrealized capital losses.

Due to the cyclical nature, the stock would recovery, but the duration to wait till recovery could be very long, the business nature may have changed, such that, the Ezra might not go back to your original entry price.

Much opportunity costs are incurred while waiting.

Business Trust FSL Trust have been undergoing some revival from $0.10 to $0.17 cents. For the old investors, it has been a stock to forget if you purchase it at $0.60.

Even with a more than 50% rise in recent times, the price is still a far cry from 2010 prices.

Prospecting individual stocks can be challenging, and while you can take the volatility, you may have failed to mitigate the negative outcome.

What good is a stock that goes up and down, up and down only for it to end up being much lower with not much hope of getting out with your capital intact?

This doesn’t only happen to stocks. The above shows the price performance chart of a corporate bond of Swiber, a oil and gas company that was unable to pay the interest and principal of the money they lend to shareholders.

You can read the full article here.

I hope I convinced you that volatility and risk are different.

Risk: There is not just one Outcome

What are the kind of wealth building risks?

We can go on all day about what are the kind of risks, but for a good list, check out the list of risks that Howard Marks provides at the end of this article.

Here are some of the risks that he provides:

- Risk of permanent loss

- Risk of falling short (your cash flow pay outs are not enough)

- Risk of missing opportunities

- Credit Risk

- Illiquidity Risk

- Concentration Risk

- Leverage Risk

- Funding Risk

- Volatility Risk (this is advance. read his explanation)

- Model Risk

- Career Risk

- Event Risk

- Interest Rate Risk

- Purchasing Power Risk

How Can we Manage Risks or Negative Outcomes in Building Wealth?

The first thing is to have an awareness that risks is a big deal in wealth building and that you need to pay attention to it.

1. Be Competent in the risk management of your type of Wealth Machine

Each form of wealth machine will have a set of general risks characteristics that applies to all wealth machines and also a set of risks that is pertaining to your particular type of wealth building.

To sleep soundly at night, you need to first identify the risks in your investments well.

You need to also find out the probability they do happen and its impact on your investment. To do that, you need to gain knowledge and wisdom about how to determine the risks in your wealth machine.

Here are some examples:

- General: If you buy an asset that is vastly overpriced relative to its intrinsic value, you run the risk of capital impairment

- General: If you put all your money in 1 or 2 assets, capital impairment can wipe off a large chunk of your net worth

- Buy and Hold Growth Businesses with Great Founders: While you may get some exponential growth businesses, there are also likely to have mediocre business that you perceived to be great but are not

- Investing in Businesses based on Value Approach: While you can deep dive and do due diligence, at the end of the day you are not the owner, and because you are not the owner operator, the governance is a black box to you. What may look like a value business, actually holds little value when poor corporate governance is uncovered

- Property Rental: Freehold properties that do not offer much differentiation in an area filled with leasehold properties can be more expensive, yet you do not expect them to rent out at a premium. There is little reason tenants will pay extra

- Stock Investing: Order book business tends to be cyclical and once cycle turns, the value of the business might be drastically different

Competency allows you to list out a range of outcomes for each risks. Here is Mr Mark’s explaining:

Listing out the outcomes, you can proceed to identify how likely the outcome will happen in terms of probabilities,

Then you can assess the impact to your assets, and to your investments. In the case where there is a earnings impact or balance sheet impact risk, assess what is the dollar value and how that affects the price you would pay for the property, listed business (stocks), exchange traded fund.

To summarize:

- List out the range of outcome for the risk

- Assess how likely the outcome will happen

- What is the impact in money value to your assets or your investments

With this you can analyse in terms of the standard risk management actions.

If you study basic risk management, there are a few risk management decisions:

- Avoid Risk: You steer clear of the risky outcome

- Mitigate Risk: You reduce the probability that the risky outcome happens

- Transfer Risk: You do not take on the risk yourself but let others take it and you pay them a fee for it

- Accept Risk: Recognize that it is a risk and that there is a possibility of the negative outcome

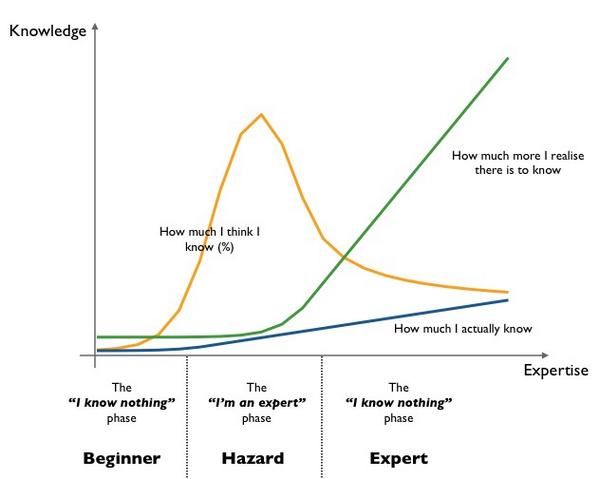

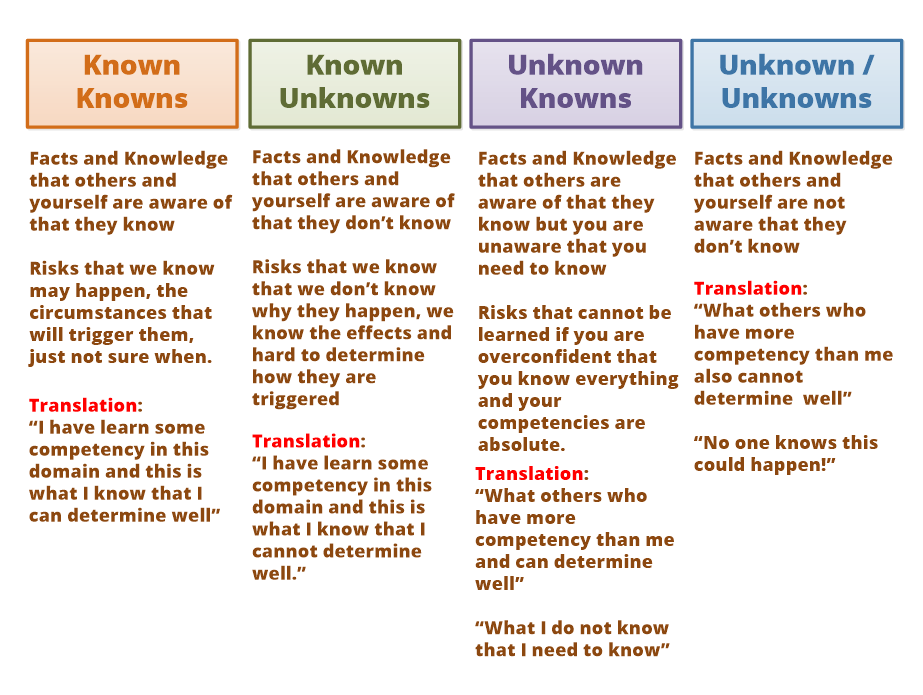

2. Being Aware of What you know and what you don’t know

When it comes to awareness of risks, be sure to use the following matrix as a guidepost of what you know and what you don’t know.

No matter how competent we are in our form of wealth building, there are areas that we have no control over, or that we are not competent enough to be aware.

Failure to understand this matrix would make you think that once you have this level of competency, you know almost everything and nothing will go wrong.

In wealth building, you never master everything. After a while you realize you don’t know a lot and you have to constantly build competency.

The following categorization can help you visualize what is within your control and what is not within your control:

Known Knowns and Known Unknowns are what we strive to be able to figure out when we improve our competency.

With Known Knowns, you will be able to come up with the right risk responses (avoid, mitigate, transfer or accept) and let us know roughly how much we may stand to lose or gain.

Known Unknowns are what we know we will not be within our control. As such we may want to take a hard look whether there are risk mitigation and transfers that can be carried out or we need to accept these risks.

The danger for most people are the Unkown Knowns. This is what I termed the knowledge gap, what you need to know to be competent to risk manage your wealth machine well but you are not aware that you don’t know.

Unfortunately there is not much you can do but have a good system to continuously work on increasing your competency.

Some good examples of Unknown Knowns are:

- You are only aware that stock prices or property prices can only drop by 20% because your experience is constraint to the past 15 years of price data. The veterans would have seen bigger draw downs in that they have data going back 40 years

- You didn’t know that there are ways to present financial figures in annual reports legitimately that puts the business in a good light, which hides the fact that there are bad points in the business

- Building on to #2, you didn’t know that receivables rises when comparing year on year financial statements is a way of knowing if much of the business is not bringing in actual cash. You will only know this as you continue to improve

- As a Low Cost Passive Portfolio Wealth Builder, you may not know that one of the biggest risk is how you manage your emotions when there is a 15% market draw down to your net worth. This will only come when you dive deep into the full spectrum of what is required to manage a portfolio passively

3. Build up your Competency to Value Assets – Refuse to Overpay, Know how much you are paying

If your Wealth Machines involve:

- Listed Businesses such as stocks for Income or Flipping

- Individual Bonds, Preference Shares

- Buying and Holding Properties

- Buying and Flipping Properties

What is of utmost importance is to not overpay for more than its intrinsic value.

If you do not like to pay $2500 for an IPAD that is worth $700, why would you be willing to do that on a potential asset that is worth 5 to 20 times that amount?

In the section on impairment to capital, we have seen that if you do not value these wealth assets well, you end up buying assets that is worth only a small amount compare to what you originally pay for.

Mr Marks:

Your question would be: How do I know how to value bonds, preference shares, stocks , properties better?

By increasing your competency so that you get better at it.

This sounds like a high level answer which it is but the way to value each can be rather different. If you would like to read some of my resources on fundamental valuation of wealth assets or stocks.

A lot of the times, we get our valuations wrong (we think its worth $1 but essentially its only worth $0.75) is because we lack the competency to see more risky outcomes and thus we value them too highly.

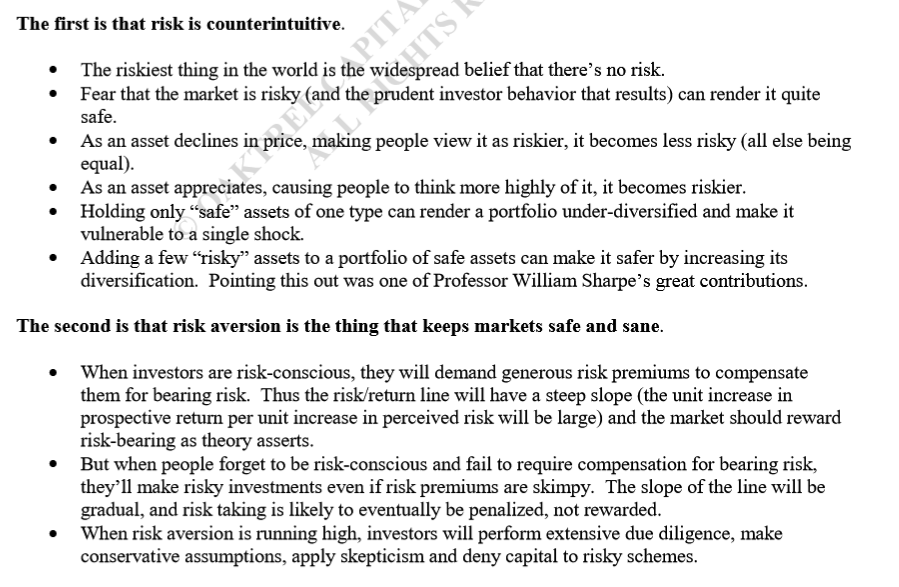

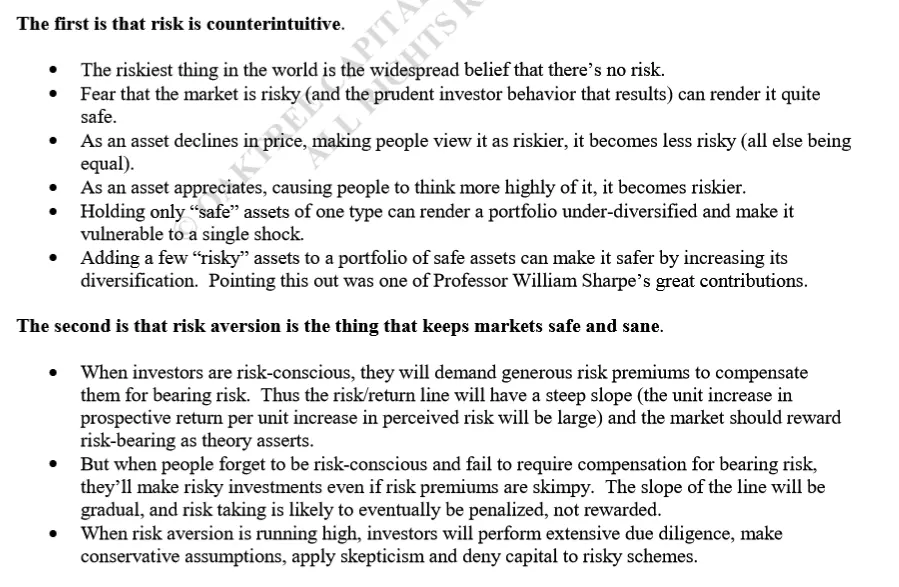

4. Mitigate Risk by Choosing to Buy in Fearful Situations

Why do people always say its better to buy during a bear market?

I interpret it in a very different manner.

Bear Market is when all the unknown knowns, and unknown unknowns surfaced.

You see the ugly stuff you previously failed to see.

When the ugly stuff is brought out, you can then use your competence to assess what is the right price to pay for the assets.

Mr Marks:

He means that risk and safety should be view inversely.

When things are looking good during a bull market, that is where people discount away the risky outcomes, that they would not happen.

This is inherently risky.

Conversely, when in the bear market, the companies that was looking sound, may show that they really can swim when everyone is sinking, and those that cannot, will show they really manage credit risk, liquidity risk, business risk very badly.

You can then assess if the problem is fixable.

When the water level falls, that is where you see who is the naked ones, and then you know which ship is the safest and the better assets.

5. Think of your Assets in terms of Returns Per Unit Risk

To build on the importance of valuation, when we look at the potential return of prospective wealth assets such as stocks, business, property, bonds we would like to purchase, factor in risk.

When you look at a real estate investment trust (REIT) that give you a dividend yield 10%, you will think its a good enough return for you.

However, you failed to see whether there are some risky outcome on the horizon, that is why the dividend yield looks so good:

- Is it facing the prospect that many main tenants are not going to renew or renew their lease at a lower rent

- Their properties actually isn’t worth that much

- The supply and demand in the region is uncertain

These risky outcomes will give you a range of valuations, and there are some things that are known unknowns and then there are some things that are unknown knowns, due to your limitation in competency.

If you look at wealth assets in terms of Returns per unit Risk you get the idea:

- potential returns are good, but with the amount of uncertainty, the risk might not be worth taking

- potential returns after knowing that the potential risky outcomes are this and this happens to be much less. It might not be worth taking this

- markets are down and the credit risks events, poor sector performance are shown in the results. Yet the returns going forward should this continue at this price look adequate return for the risks, which is much less unknown outcomes since most of these outcomes are shown

Returns per unit risk affects on how nimble or how long you can hold on to assets. If you realize you have too much unknown knowns for this wealth asset, you either risk management by avoid buying, or that be more vigilant and mitigate by selling first and asking questions later.

How can you hold an asset longer? When you have build conviction. Conviction is done when you have a certain degree of confidence you have uncovered enough risks, value well thinking with these risks in mind and that you have a good margin of safety, and the potential reward is good.

In other words a good return per unit risk.

6. Some of my Active Value Based Income Investing Risk Management Systems

After going through such an ordeal, I realize that I don’t have a stomach for it. We know its going to come sooner or later. The key is that I hope i have a fundamentally sound plan for it. I hope that being through it once could help me better equipped for it.

- System: Continue to learn and improve the way I prospect business. There are always new angles on business that we failed to grasp and while we cannot know more, increasing the number of mental models how things work allow us to think critically and critic management decisions, business practices and how we value businesses

- System: When prospecting business, always evaluate the scenario’s in whether a business can survive in a challenging recession. A 2009 case study for the business is a good litmus test.

- System: When valuing business and purchase point, understand the stream of cash flow that goes into your valuation model, understand how optimistic or pessimistic they are. The best is purchase them below a pessimistic stream of cash flow

- System: Stick with businesses that will not be a going concern in a challenging recession. Don’t just think what will happen, perhaps find comparable

- System: Market drawdowns is unpredictable and my plan is not to predict them, but have a fundamentally sound plan for different frequency of draw downs. Read here and here.

- System: How strong you will hold on to your holdings depends a lot on your understanding of your plan, your understanding of your holdings ability to do well in that scenario. Understand the kind of goose you are holding. Sell the goose you felt you don’t know well, or the goose you know won’t survive such a scenario.

- Knowledge: Be a bigger student in understanding my behavioural tendency to do something detrimental under these scenarios and what are some systems that can circumvent them

- Knowledge: Learn to better frame your brain for different scenarios. Read and reflect extensively

- Environment: Learn to filter the signals daily from the market. This is especially challenging for bloggers since we have to tune in to some things that goes against how we use for wealth building. Understand what is useful and not useful

- Environment: Stick with peers that you know will call you out and make sure you do the right thing. Ignore detrimental influence. The challenge here is you got to understand and trust your peers as well

It is not an exhaustive list but what I can recall from my head now. The plan is probably more important than the individual businesses. And i remove a lot of naive if this happen then do that because they are likely not going to work.

Number 6 and 7 is what I been working hard on. It is something many think they have mastered. Not me.

I removed all the TA stuff with the moving averages from this plan because this 4-5 years taught me its rather futile. It might work for you. Not me.

I run a free Singapore Dividend Stock Tracker available for everyone’s perusal. Do follow my Dividend Stock Tracker which is updated nightly here.

Here is the outstanding 20 page newsletter that Howard Marks revised to frame our minds correctly how to look at risk:

Howard Marks Letters: Risk Revisited Again by Kyith

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

EarlyRetirement

Wednesday 4th of June 2014

I only put money into company that I am confident with, company with product strongly demanded such that the income stream is strong and continuing. I tend to stay with them even they are down a lot, provided fundamentals still looks right.

Kyith

Thursday 5th of June 2014

hi Early Retirement,

That's very strong conviction but how do you evaluate real problems with your investments.

freedom

Wednesday 4th of June 2014

Point 2 will most likely result in very little investment to be made especially when we are in a bull market. Point 1 and 3 will not be accurate as time goes along. Financial conditions of companies are changing all the time, especially in an uptrend. When the market realizes it, point 2 has long passed. Again, few investment opportunities, though probably safer. Then the question will be: staying cash will always be safe, but who wants to stay in cash forever?

Kyith

Wednesday 4th of June 2014

hi freedom, thanks for that. if point 2 results in lesser opportunities but surer ones so be it.

temperament

Wednesday 4th of June 2014

No matter how much knowledge you can gather from readings is of no use. If you can't read your "inner self". So try read yourself first.

Eric

Thursday 5th of June 2014

It's a concurrent process, the point is to be reflective. I was only able to read my inner self after the GFC happened because i had some knowledge from books

Kyith

Wednesday 4th of June 2014

its a start. if you are not willing to be an active student of it. then you didn't get started at all