A friend of mine asked for help convincing his cousin to start investing.

My friend obviously has his cousin’s welfare at heart, which is why he is getting tips on how to convince her to start investing.

There are many out there who are diligent savers but they do not understand WHY do you need to push them over the edge to take risks and invest.

I would like to think that I understand that since my risk profile shows that I am risk-averse enough.

We cannot convince someone to invest if:

- They do not understand investing to a certain degree. Investing would just look like gambling to them.

- Nothing in their world is at risk.

- There is a major upside to investing and it’s not too difficult to implement.

Now, if we backtrack a little, we are not trying to get people to go from never invest to become astute investors.

We just want to get them to be open about that possibility.

1. Untangling the World View that Investing is Gambling

When I used to know nothing, investing is interchangeable with gambling.

Well, now that I have a good understanding of both, philosophically I think the way people invest is still gambling!

I would have that view when I know nothing because I really do not know the subject well enough.

If we can get my friend’s cousin some formal materials on investing, it will reframe her view that investing is some sort of gambling.

There are fundamental drivers behind investing, how to systematically do it that she can learn from reading.

It would be easier if the cousin reads enough and you can pass her some materials. It would be up to the material to convince her.

If not, my friend would have to untangle each of her views/arguments why she should not invest.

2. One day, their world would be at risk

If our lives go according to our plan, and everything is orderly, then there is no urgency to change.

Many of us may have a life like that.

There are many people out there who did relatively well at a well-paying job. They don’t have to invest because, given their annual expense, and the high personal free cash flow their money will turn into a big stash even if they do not invest.

There aren’t a lot of motivation to do anything special.

If the machine is not broken, why do we tamper with it?

I think not everyone is like that.

My friend tells me his cousin saves well but not to that level.

The hard truth is that experience tells us a very comfortable life can change in an instant. Or that our lives will deviate from the current course when we least expected it.

We felt we have enough usually because based on the current plan we have enough.

And we often don’t realize deviations are common because of our lack of experience.

Here are a few deviations I heard of:

- Suddenly the wife NEEDs to stay at home. (Don’t ask me why it is a NEED. This can be for different reasons, some logical, some really absurd). This changes the household personal free cash flow.

- Boss change. A great work environment becomes not so great. You leave. And then suddenly you realize a good work environment and good bosses are rare.

- Health problems. Change in your family’s health status. This may force you to not able to work, reduced work capacity, increase costs.

- The family needs a maid. To take care of a family member.

- Domain or job gets disrupted. The valuable skills that allow you to command a great salary are not portable.

- Involuntary sack. This can be due to scandal, the grave mistake on your end. Imagine those who get caught and went viral on social media suddenly.

If we have the capacity to save and further enhance it by investing, we could build a larger amount of wealth and that could give us greater optionality.

I always feel that Coast FI is a good financial independence scheme to aim for because the amount to save up is reasonable for people with a good salary and it act as a great safety net.

It is a damn nice feeling to know that you have successfully pre-funded your retirement and you can have greater variation in how you use your current income.

Lastly, we might think our life is not at risk if we think we have a good plan for ourselves.

But what if the plan is flawed.

Whenever I listen to the financial plan for others, I somehow felt that for some, their plans are shakier than the confidence that my friends have.

Providing some reality check might be enough for them to ask the next question: So how do I gain greater optionality?

For most people, there is something that they want that is out of reach.

I don’t believe people desire a certain level of status quo.

We stay in this status quo because deep down, we think that a scheme of life that we desired is out of our reach.

But they may not realize that it may not be far fetch to reach a certain lifestyle scheme with their financial resources if they just invest.

This brings us to the next point.

3. The Virtues of Investing

For the uneducated, investing sounds like a very time-consuming, sophisticated endeavour.

This is a little similar to the first suggestion.

My friend’s job is to untangle this notion that all investing requires high sophistication and a lot of effort.

There are passive investing strategies that most hectic family people like ourselves can practice.

Better yet, if you are able to find reliable, trusted and sophisticated enough advisers like our clients, you have a bridge/link-man to make wealth-building less daunting.

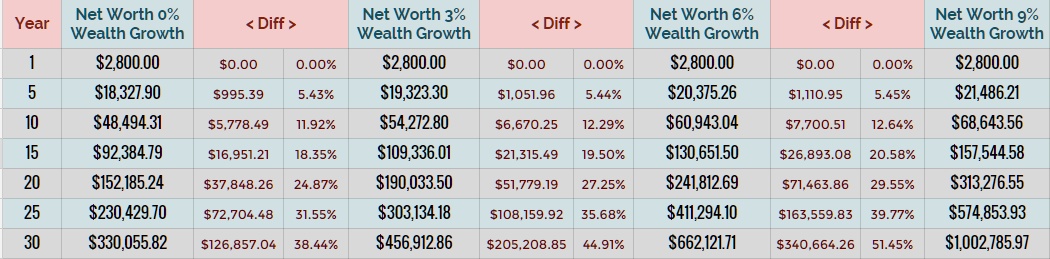

4. The Difference of a Greater Rate of Return

The main reason we need to invest in that, without a greater rate of return, your money may not keep up with inflation.

The following table shows the difference in the amount of wealth built at different rates of return:

This was lifted from my Wealthy Formula article.

If you wish to have enough money for future spending, saving money at a 0% growth rate just would not cut it.

You have to invest and compound at a greater rate of growth.

These two years have shown us how high expenses can inflate. And if what they say about inflation not being transitory is true, you are not investing in assets that traditionally do better when inflation picks up.

What about you? Did you manage to convince a loved one to start? How did you do it?

Convincing people is never easy.

Some tips that I learn from my boss (he is a certified coach) and others that I read is

- Try to make them come up with the solutions. People are more inclined to take action if they feel like they are in control. That the idea we came up with comes from them.

- The underlying problem or motivation is not always about the money. It is something to do with their past life, current life or projecting a future life. Work with that.

- You got to work off the life, communication problems… before the money problems. Money problems are often easier to resolve.

Investment Moats readers may be very good at this compare to others.

If you have a good solution, do share it with us so that we can learn from.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

G

Sunday 17th of October 2021

Thank you!