You wish to put away $1000 per month into a Passive Exchange Traded Fund (ETF) that follows the Straits Times Index (STI).

Doing it periodically every month is what we call Dollar Cost Averaging.

The STI index is a selected Top 20 Blue Chip stocks in Singapore, comprising of DBS, UOB, OCBC, Singtel, SPH, Keppel Corp, Capitaland, Ascendas REIT, Capitaland Mall Trust.

You can do this in Singapore if you periodically purchase the SPDR STI ETF (ticker ES3)

However, you will wonder, what if you start doing this when the market is at an all time high, how will your money do?

This is what I first visit in 2013, when I understand one of my former working counterpart at work did. And I did a study on it.

In this article, I will update on the results, if my friend continues to do this till end July 2016.

This article will interest you:

- if you are interested in passive index portfolio investing

- you are curious about how well dollar cost averaging do

- are always apprehensive and afraid of investing at a high

The DCA at the Top Story continues…….

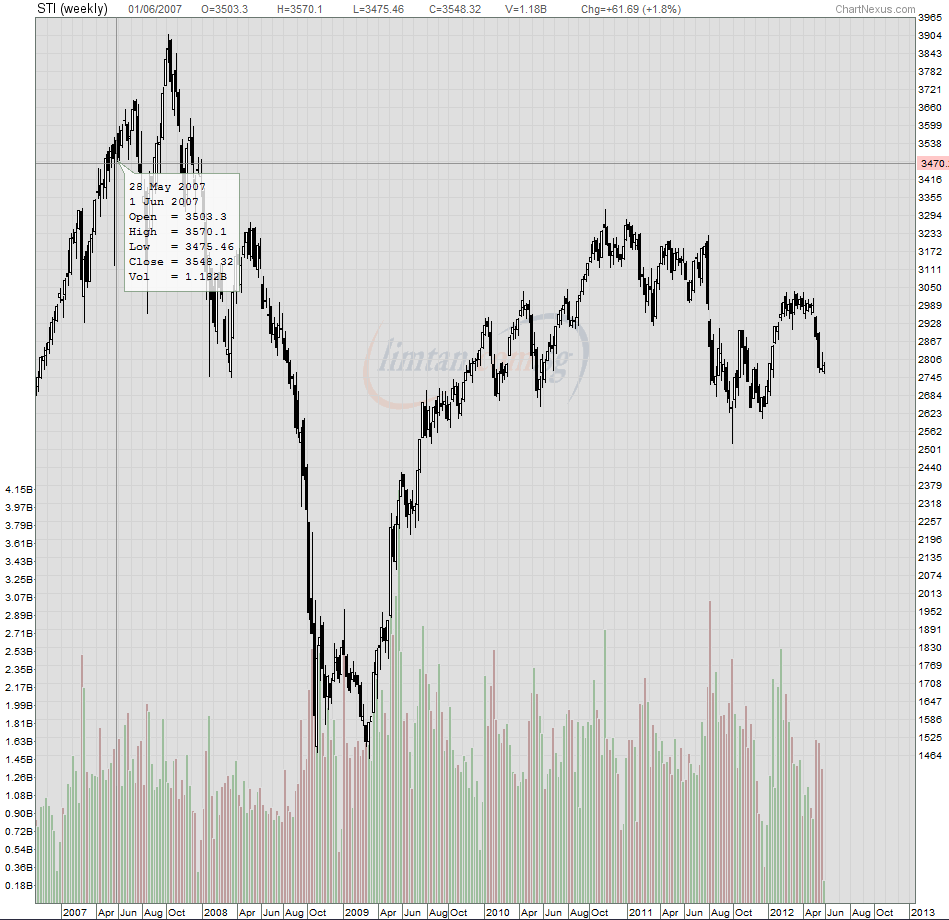

Here is a snapshot of the STI Index from Mar 2007 to Oct 2013.

My friend started a monthly periodical investment of $1000 per month near the top on 28th May 2007, almost 2 months before the top.

He kept doing this.

Another thing he did: His brokerage platform used charges him $25 per trade. So his cost per transaction is nearly 2.5%.

That is as expensive as the sales charges of unit trust (which is a big reason against unit trust as an investment vehicle. Cost matters as you will see later)

The past review can be viewed here:

- Oh Shit! I started DCA investing at the top of the bear market!

- 2014 Jul – Dollar Cost Average into STI ETF right before Great Financial Crisis Revisited -XIRR 4.95%

- 2014 Oct – A Lump Sum investment in STI ETF near the top of the Great Financial Crisis – XIRR 2.82%

- 2015 Mar – The dollar cost average into STI ETF at the peak achieves 5.5% XIRR over past 8 years. – XIRR 5.5%

We will try to continue this story today by doing this review

Recent Price Movement of STI ETF

If you look at the price that my friend first bought in, it was when the index is near 3900 points.

How is the recent price action?

I decide to make use of a new platform that I am beta testing called TraderWave. TraderWave gives you price charts of data as far back as 15 years, but for some reason (not just traderwave) most platforms STI ETF data is getting shorter and shorter.

You can request to beta test TraderWave if you are interested. (I am not paid to say this)

As you can see we had a good run up to equivalent to 3500 on the index.

Then we went into a nosedive below 2600.

This is a 25% fall from the top.

Since then the price have rebounded. God knows the return that we will get if I did this exercise at the start of the year.

Our index hovers closer to 2900 now.

Measuring the Return with XIRR

You may be wondering what is XIRR. It is a way in wealth we measure the performance of a financial asset, be it fixed deposits, property flipping, unit trust, stocks or ETFs.

It stands for Internal Rate of Return which measures what is the annual compounded return for the net asset value of the amount you put in today and next time to be 0.

This can be rather hard to explain but suppose you buy a condo for $1 mil, on a -$250,000 downpayment, paying principal of $-1500 every month, interest of -$1500 every month, getting +$3000 rentals every month, paying -$800 maintenance and condo fee every month, what is your compounded rate of return now?

With a stream of cash flow going in and out it is hard to figure out what is your real return, since you are putting in money, you are getting money out.

That is why we turned to XIRR.

It gives us a good basis of comparison against other investment assets.

The return you get from an ETF such as STI ETF

How do you compute the returns you earned from the STI ETF?

Like many of the listed investment, you cannot just look at what you buy and what you sell!

Always look at the Total Return that you are able to earn.

Your STI ETF Total Return in a year = Dividend Yield + Capital Growth for the Year

As the STI ETF is made up of individual blue chip stocks, which mostly distribute dividend payouts, you will also enjoy the dividends.

If you go to SGX.com > Corporate Information > Corporate Action > Choose STI ETF > Go, you will presented with the past dividend history, rights issue, share splits of STI ETF:

Past XIRR Returns

If you review the previous reports the past XIRR fluctuates:

- 2014 Jul: 4.95%

- 2014 Oct: 2.82%

- 2015 Mar:5.50%

Why such a big difference? This is because the price index goes up and down.

The XIRR factors in the dividends you collected, and also the scenario of what if you sold all your STI ETF holdings at the end of the period, what your returns will be.

How are the returns updated till today?

I have updated the figures.

If my friend continues to do this, his XIRR would be 2.28%.

You can take a look at my worksheet on Google Spreadsheet here >

The above is a snapshot of the updated data.

Firstly remember my friend’s commission cost is 2.5%.

His highest price invested was at a pre-split (STI ETF did a 10 for 1 split) of $37 and the lowest price is nearly $1.66 in the depths of the financial crisis.

The average price when you dollar cost average periodically for him is $3.02.

This average price is still higher than the current price.

His cost put in have been $111,721 for this past 9.38 years.

So why is the XIRR positive? Because Total Dividends Collected was $16,809.

What if the costs are lower?

Let us take a look at the result if you purchase more and minimize the commissions.

The minimum commission for most platform is around $29. So to push your costs down to 1%, your periodic investment amount needs to be a minimum of $2,900.

I use Standard Chartered Online Trading, and since the change in policy the minimum commission is $10.

If I were to use Standard Chartered Online Trading to push the commission cost down to 0.25%, your periodic investment amount needs to be a minimum of $4000.

How does the cost affect?

Suppose we are able to invest $1000 every month at 1% and 0.25% commission costs, we will be able to get the following result:

The above is when the cost is 1%.

The XIRR is bumped up to 2.62%. The main difference is that the average cost is slightly lower, and therefore your unrealized losses is -2.5k versus -4.1k.

If you compare the $15 monthly commission difference over 10 years its about $1,800. You are basically saving the costs for the same kind of product.

The above is when cost is 0.25% or 10 times less the original cost of 2.5%.

The XIRR is bumped up to 2.79%.

On a % return basis 2.8% does look much better and certainly, you will agree with me that we have endured some high volatility.

How does the STI ETF compared to the XIRR of other financial assets?

Is this 2.28% to 2.79% return in 9.38 years good?

To frame this comparison better, do think in terms of:

- Your time spent on this form of wealth building

- The ease for you to periodically get invested. Not all investment allows you periodically invest into

- The risk of the financial instrument (risk is defined as permanent loss of capital not volatility)

- The competency required to do this well

I explain more of this in my article on finding and building your wealth machine(s), its worth a read.

If you hold a portfolio of STI ETF and perhaps a bond index ETF such as the ABF Bond ETF, they can be more passive than a lot of other wealth machine.

Once you compute the XIRR you can compare the financial performance versus other wealth machines.

Insurance Savings Endowment

You could compare this to insurance savings endowment.

In one past article, I crowd sourced what XIRR readers, family members and friends are able to get on their matured insurance savings plans.

You can read Does your Insurance Saving Plans (Endowment) give you 3 to 5% returns?

You will observe that the typical XIRR is around 2.5-3%.

In terms of time spent on insurance savings and STI ETF, they do not differ much. In terms of how easy to periodically invest, they also do not differ much.

Insurance Savings Endowment are more forced savings, as you cannot withdraw. There is a penalty to it.

If you invest in STI ETF, you could stop it on your own (which may be a good or bad thing altogether)

You will need more competency when it comes to investing in STI ETF, particularly what is passive low cost index investing.

Real Estate Investment Trust ( REITs)

REITs are financial trusts that are listed on the SGX stock exchange that invests in a group of properties, primarily to distribute dividend cash flow but also capital appreciation over time.

It has become a favorite of many since property have a huge mind share in the Asia context.

You can check out my article on how do REITs grow and 3 of the important high level metrics when choosing REITs.

I did some XIRR in the past on what if you dollar cost average into some REITs. Apologize but there is no particular selection metrics. I do it on a ‘I happy I do, I not happy, i don’t do’ basis.

While they are not at the same time period as the STI ETF of 2007 to 2016, it gives you a perspective on the XIRR.

To be fair a lot of them were done starting from 2007 and 2008.

While these returns look great, remember there needs to be some competency in selection of REITs, and how you manage them on a long term basis.

REITs have a good run because it has been conducive for them, certainly more so then other listed businesses in the STI index, hence a better performance.

It doesn’t mean this XIRR is repeatable.

Remember, as with STI ETF, insurance endowment and REITs, future performance can be very different.

Some Important Takeaways

I would like to bring your attention to some takeaways that you might have missed out:

- STI ETF can be volatile. If you are thinking of putting your money in and getting a guaranteed return, this financial instrument do not seek to give you that guarantee

- This does not mean that insurance endowment is not volatile. If you look at the returns of your participating fund, which the insurance company invest on your behalf, the returns are volatile. It is just that the risks and competency of investing is transferred from you to the insurance company

- Dollar cost averaging takes advantage of the volatility. If STI price is not volatile, the returns could be much worse. Volatility is not always bad

- Dollar cost averaging works if over the long term the price ends up higher. This result of nearly 10 years show that dollar cost average is not a magic bullet

- If prices end up much higher, it is better to invest in lump sum at the start. If prices end up much lower, it is better to not invest in a lump sum at the start

- With or without the returns, do notice, that my friend have accumulated nearly $100,000 in 10 years. If you have read my Wealthy Formula (worth a read), you will know that it is the action you pledge to do it consistently, funneling more into your Wealth Machines that might make a bigger difference

- Don’t keep dissing its low return, compare to individual stock investing, you could pick a group of poor stocks and end up worse than this. If you like to buy blue chips, your returns might fluctuate around this as well. You are also spending far far far less effort in managing an STI ETF. You don’t have to keep track of the news in the stock market for a start.

What do you guys think of this quantitative performance over such a challenging period?

If you like materials such as these and would like to enhance your Wealth Management towards have a Wealth Machine that gives You Financial Security and Independence, Subscribe to my List Today Here >>

If you like this do check out the FREE Stock Portfolio Tracker and FREE Dividend Stock Tracker today

Want to read the best articles on Investment Moats? You can read them here >

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

RN

Sunday 28th of August 2016

Investing in STI ETF suppose to be a low cost option. With DCA, the cost escalate and that's defeat the purpose of ETF.

One could invest in Index with 'Mean Reversion' concept. Buy (more) when the market is at pessimistic points. While waiting for the pessimistic point, the investor shall use this period to build up his war chest.

Investor could refer to Chan's Channel or STE or EIN55 for reference.

In the past 2 decade, STI achieved ~9% CAGR. However, this growth is likely not realistic for the next 10 years due to SG economy is at her peak. http://www.straitstimes.com/singapore/slower-but-quality-economic-growth-over-next-20-years-0

WONG KENG WAH

Sunday 28th of August 2016

Personally I think DCA is a scam made up by brokerages and financial advisors to suck up transactions fees. Instead of putting one thousand into STI ETF every month. Why not put aside the same amount in a high interest account as a warchest. My rationale is why buy 5000 units of STI ETF @ 3.4 when you can buy 10000 units @ 1.7. The pricing of 1.7 was the lowest STI got during 09 after lehman collapsed. Same for SEMBCORP. 1.5 years it was at above 5dollars. Now its 2 dollars plus. So the price 1.5 years ago can get you double the units at this moment.

Any long term investor should at least be able to determine a realistic target price to buy and sell. You can make that determination by reviewing past data. Or based it on your desirable dividend yield. If 4 percent is your target. Then stick with it. Why bother with a 2 percent dividend at this moment with DCA.

Of course there are different circumstances to deal with: 1. Your current financial status 2. Are you willing to wait for the right price 3. Do you have the cash if the right price is now.

Kyith

Sunday 28th of August 2016

hi Keng Wah, i think partly it does sound scammy, providing them a recurring income for the financial institution and brokers. However, i think not every one will be able to buy at the bottom. Its also not a good idea for everyone to speculate that way. Some may think 3500 to 2800 is low. in that case they wont have the money to put in at 1700.

Individual stocks valuation is different. Sembcorp, for example at this point is worth very different from when it is $5.00.

Qwerty

Sunday 28th of August 2016

I tried using xirr in excel. It keeps getting #value error. I suspect it's the date format? Does it need to be in a specific format type?

Kyith

Sunday 28th of August 2016

whoa you guys are fast. i thought it should work. yes in the past i think you need to do it in a certain way. if you make a copy of my sheet does it work?