This article, was supposed to be my submission into a joint book that a bunch of people have written. But it seems to have not seen the light of the day any time soon.

I just do not like to write a bunch of things and it not seeing the light of day. So I decided to put it out on my site now. This is an analysis of a company which I own. The price have ran up a little but I thought it would still be worth it to bring to your attention. I would try to do less of those horse back carriage front kind of things where I told you “I bought this stock when its distressed and look how great I am” posts.

Their results should be out in early March and I thought it has a pretty interest mix of profile that you can be aware about.

The recent share price trend. Note that it has not been listed for long, since it was spun out of The Wharf not too long ago.

In times like this, where the market is down, I think I would provide investors with a simple to understand investment that might rest at a very sweet spot.

This investment is

- Slightly below its net asset value

- Quality, hard to Replicate Retail and Office Properties with Long Average Land Title

- Provide a recurring 6.2% earnings yield

- With a 65% dividend pay-out ratio

- Potential Dividend Yield of 4% with low leverage (net debt to asset of 15%)

In Nov 2017, Hong Kong listed The Wharf (Holdings) decide to spin off some of their core properties into a new company called Wharf Real Estate Investment Company or Wharf REIC.

Wharf REIC was listed at HK$48 and reached a higher of HK$63. It is currently back at its debut price. After this separation, Wharf Holdings would focus their efforts on investment and development in Mainland China.

I would say, Wharf REIC is the cash flow machine of Wharf Holdings. The owner basically spun off 60% of its EBITDA generator into a new company.

By being a real estate investment company, rather than a REIT, Wharf REIC is not limited by having to pay out 90% of their income as dividends, only using 10% of asset allocations for development and a 45% maximum gross debt to total asset ratio.

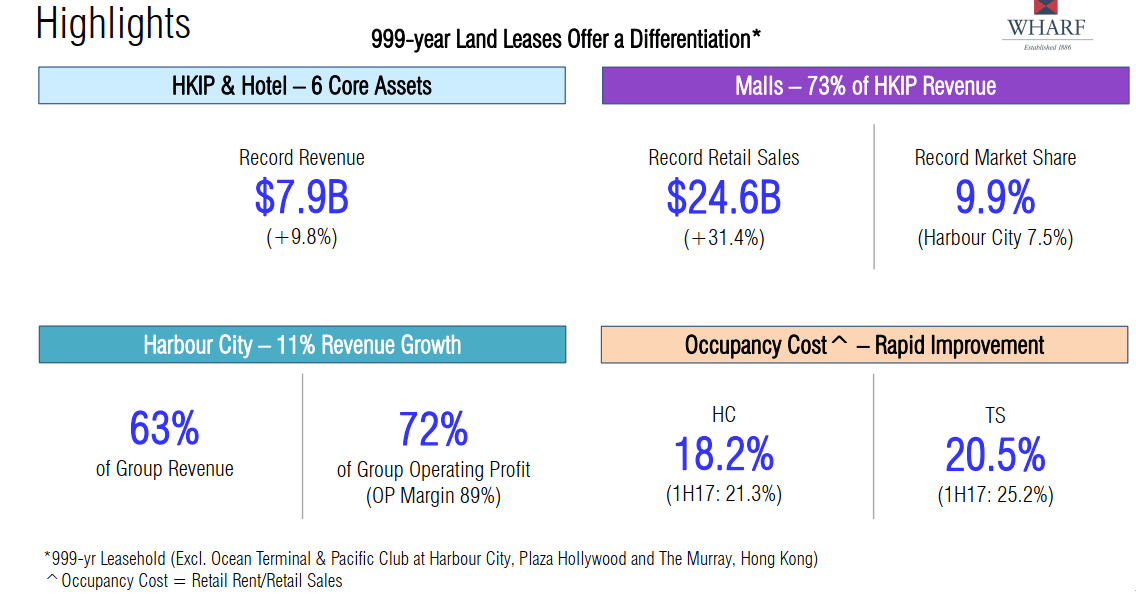

Wharf REIC have the largest retail portfolio by size of investment properties in Hong Kong. This is bigger than Sun Hung Kai Properties and Link REIT. The portfolio is anchored by 2 very prominent retail malls Harbour City and Times Square.

Their current mix of properties is:

- Hotel 5%

- HK Office 24%

- HK Retail 62%

Given this, 70% of the revenue are derived from Hong Kong with the rest from China.

One of the attractiveness of Wharf REIC is that they are committed to pay out 65% of their earnings as dividends. Management have guided that they will use the other 35% to pay down their debt. Compared to other Hong Kong property stocks, Wharf REIC do not pay out the maximum, but provides a higher pay-out then the other property stalwarts such as CK Asset, HK Land, Swire, Sun Hung Kai.

The pay-out ratio allows the investor to earn some decent low leveraged pay-out.

However, the main attractiveness for me is the quality of the property, and the cash flow that the properties generate. The majority of the cash flow is driven by Harbour City and Times Square, which are main tourist attractions in Hong Kong. These are trophy assets located at the heart of Tsim Sha Tsui and Causeway Bay.

The main retail attractions are in superb locations and investing in Wharf REIC allows the investor to tap into the superior retail management abilities of the manager.

By virtual of their strategic locations, strong connectivity, these 2 retail malls enjoy very good footfalls. Due to their size, they cannot be easily replicated as well.

You could say that the rent is high and unsustainable, but take a look at the occupancy cost here. At 18% for Harbour City it is very close to the 16-18% rent to sales cost for Frasers Centerpoint Trust and Capitaland Mall Trust

To give you an idea how big Harbour City is, the total gross floor area is 8.43 mil square feet. The largest mall in Singapore, VivoCity, is 1.5 mil square feet. Harbour City is 5.6 times the size of VivoCity! Times Square have a gross floor area of 1.98 mil square feet.

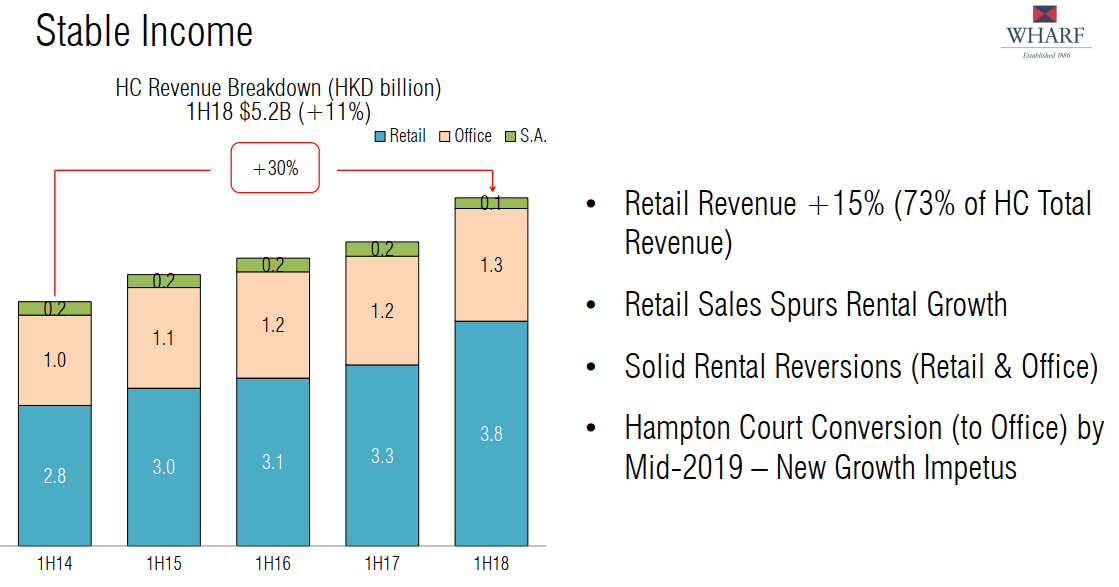

The total revenue of Harbour City increased by 11% in 1H 2018. Retail revenue rose by 15%. Wharf REIC average passing rent grew by 14%.

The recurring earnings per share is HK$3.31. At the current price of HK$48, this is a recurring 6.9% earnings yield. Because of the low leverage, this puts the unleveraged earnings yield possibly around 6.05%. This is higher than a lot of the local REITs, if they are unleveraged.

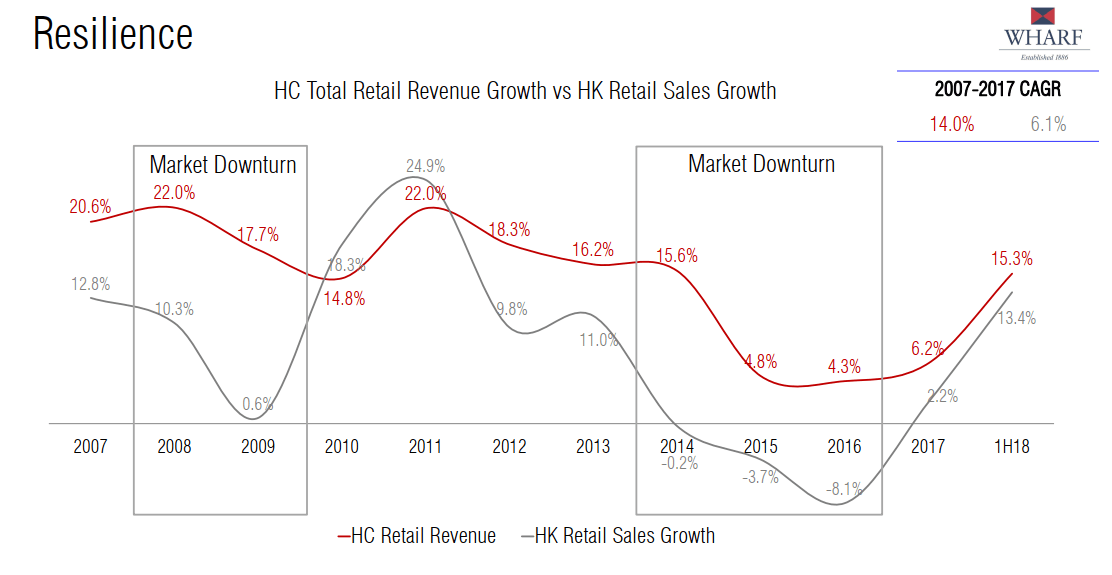

Harbour City, is a powerhouse. Notice the declining sales growth and yes the rental revenue growth has decline, but it is still growing!

Growth in Harbour City is good

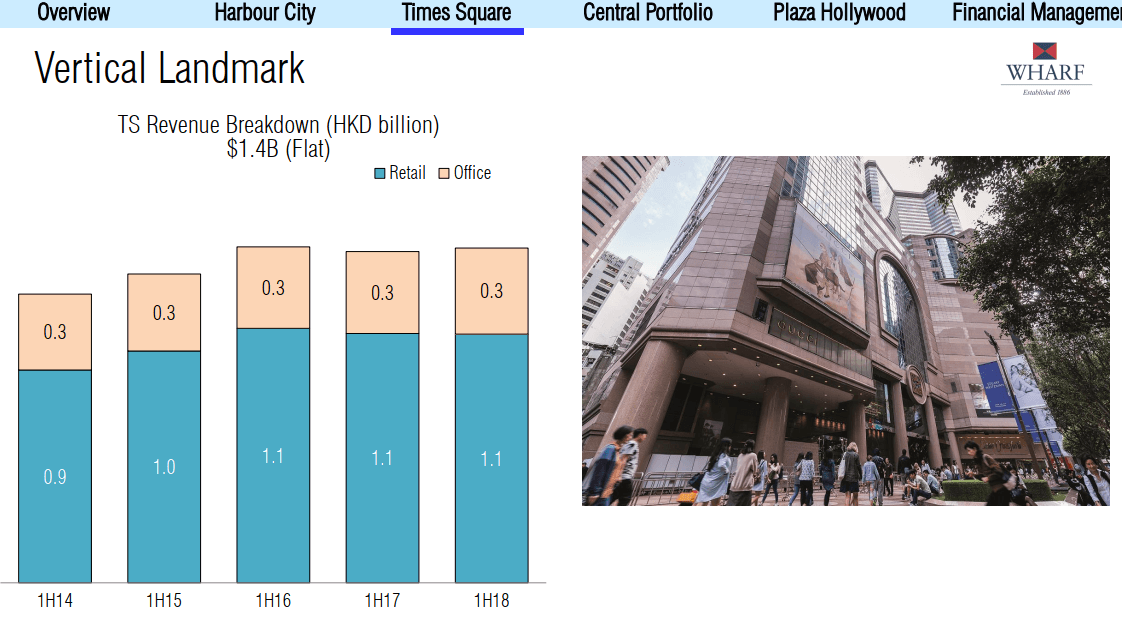

Times Square rental growth is a bit flat though.

Wharf REIC is a play on recovering tourist spending in Hong Kong. The weighted lease expiry of the leases is 2 years. Short leases are excellent if you have a strategic retail moat. This allows the manager to not missed out on growth.

Unfortunately, short leases are double edge swords. It means that if tourist numbers ae not good, this would affect Wharf REIC.

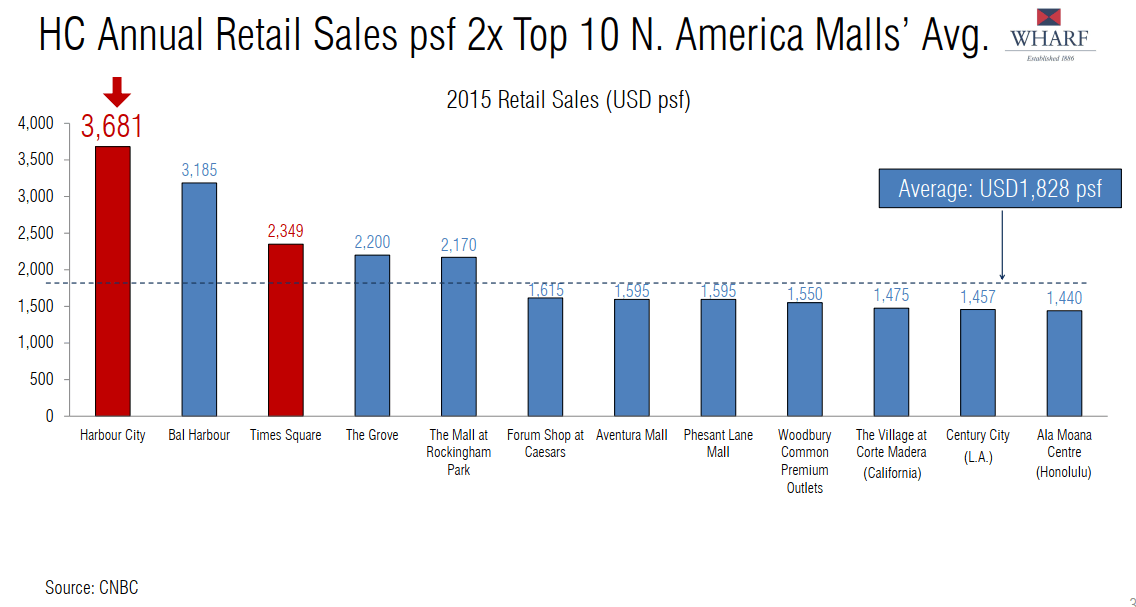

Harbour City and Times Square not just a have a large percentage of Hong Kong retail sales. Compared to some of the Top American malls, their sales figures are top as well

One of the risk for Hong Kong real estate is the unknown risk of what will happen when a lot of the land title expires in 2047. The main bulk of Wharf REIC’s land title has a long expiry:

- Harbour City averages an expiry in year 2880

- Times Square averages in year 2860

- Crawford House averages in year 2842

- Wheelock House averages in year 2854

- Plaza Hollywood, Suzhou International Finance Square, Marco Polo Changzhou: 2047

- The Murray: 2063

In terms of debt, their gearing is lower than REITs. The current net debt to asset is 15%, net debt to equity is 20%, which is very manageable. The groups average borrowing rate in 2017 is 1.5%. All the debts are unsecured. Their debt is in Hong Kong dollars so there is no exceptional currency risk there.

Wharf REIC’s valuation Cap Rate is reasonable. For their HK Retail, the Cap rate used is 5.2%, for Office, the Cap rate used is 4.2% and residential 4.5%. This is probably a little higher than Cheung Kong Asset’s cap rate for their office of 4.75%. To me, Cheung Kong Asset valuation cap rate tends to be rather conservative.

We talked about the Cap Rate because it ties closely with how the properties are being valued. In that way we can determine whether the properties are attractively valued. The net asset value of Wharf REIC is around HK$220 bil. Wharf REIC’s current market capitalization is HK$163 bil. Thus, Wharf REIC trades at a 26% discount to net asset value. It should be noted that a lot of property companies in Hong Kong trades at a large discount, so this is not very special.

What I like about Wharf REIC is that based on recurring earnings yield, the profile of properties, and the low leverage, it shines amongst the competition.

Its dividend payout ratio is conservative, committed to pay out a certain percentage, and back by a cash flow. Assets are high quality and leverage is low. Majority of the income stream is backed by assets that have long land lease.

It is clean and less complicated. Its debt is low, and its short lease works well in an environment where interest rate is rising.

Some Counter Points to My Analysis

My friend, CIMB broker Hayden Huang, shared with me his analysis, which have a fair bit of reservations against Wharf REIC.

So I will post them here.

Wharf REIC is the full collection of Wheelock’s 999 years investment property heirloom in Hong Kong.

Interest rate risk. Any interest rate hike may lead to an expansion in the capitalization rate and in turn adversely affect the stock’s valuation.

Retail Rental Trend in Hong Kong. There was a serious dip in rental rates i 2014 onwards due to China corruption crack down. Some say that the figures have bottomed out but it really depends on the RMB trends and US-Sino relations.

Since rental rates are on the high side, we are likely to see only single digit revisions.

Valuation. The valuation is not as compelling as compared with its competitors Swire, Hysan, Hong Kong Land. However, Wharf REIC is more Hong Kong focused and Semi-REIT (65% locked in payout ratio) with potential investment in greenfield sites. So valuation should be higher than Hong Kong investment property / developers.

As their investment property is marked to market, the recent land sale by HNA showed quite a steep drop in land value. This may mean a correction in land value which indirectly mean the company’s fair value would change and the profit be affected.

Concentration Risk. Bulk of the revenues are determined by 2 prime assets.

Unlikely to see unlocking. Since these assets are considered as heirlooms, they are likely to be passed down for generations, which means the probability of sale is very low.

Potential Catalyst. If they sell their remaining China hotel assets through HCDL (Wharf REIC hotel assets are valued at cost less depreciation). They did mention about wanting to be a pure Hong Kong company during the spin off.

If you would like to get in touch, to have a broker that has this Graham slant to add value, contact me and I will put you in touch with him.

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Kang Kai, Tan

Friday 8th of February 2019

1997 more like a reit structure 0004 has more growth room than 1997 as it is venturing into China market Parent company 0020 also another good choice..

Kyith

Saturday 9th of February 2019

Hi Kang Kai! thanks for the heads up. I think thats the leaning towards predictability. 0004 have to see the projects that they deal with.