About 80% of the Singapore population live in HDB flats. And a large number of us lived in 4 room HDB flats.

HDB flats form the basis of the government’s plan to ensure that the population have affordable shelters.

It is debatable whether the HDB is a way that they wish for us to build our wealth. The late prime minister Lee Kuan Yew have said in past speeches this is the case. This was reinforced in the 1990s by Goh Chok Tong and then eventually by minister Mah Bow Tan.

I see 4 room HDB flat as the most functional unit to start a family.

The 3 room flat have 1 less room, and logistically not ideal for a family. Ideally, people would go for a 5 room flat due to the additional space. However, if you are cost conscious, or wish to stay in an area that is more accessible (which means more expensive), you would go for a 4 room flat.

I had a conversation with a co-worker about some problems he faced while trying to secure a rental unit for a relative from overseas. So I decide to look up some rental figures.

Since I haven’t written anything for the Sunday, I decide to take a snapshot at this interesting segment of Singapore life.

So in this article I will go through a look at how expensive or cheap are our 4 room flats based on various metrics, whether they are affordable and the difference in rents over the past 10 years.

How do we measure the Affordability of properties?

When it comes to valuation of physical assets, there are a few ways doing it:

- Comparing against the replacement cost, or the cost today to create a HDB unit similar

- The discounted cash flow of the stream of rental from the property

These 2 metrics are good. However, it seems that they are meant for assets that are primarily for investment purpose.

While we can argue that many Singaporeans look to profit from it, the majority of people treat their flat as providing shelter over their head.

It is difficult to compute the replacement cost, as it is the subject of political debate. This has been a lot of debate during past election whether the construction cost versus the price they sold to the citizens are much lower.

In personal property, there are some standard affordability indicators:

- Price to Rent

- Price to Annual Income

These 2 indicators measures the affordability of the residential properties.

If price to rent is too high, it means you are paying a lot of annual rent years for the residential property and would take some time to earn back your property.

This is the same of annual income.

Let’s take a look at the data.

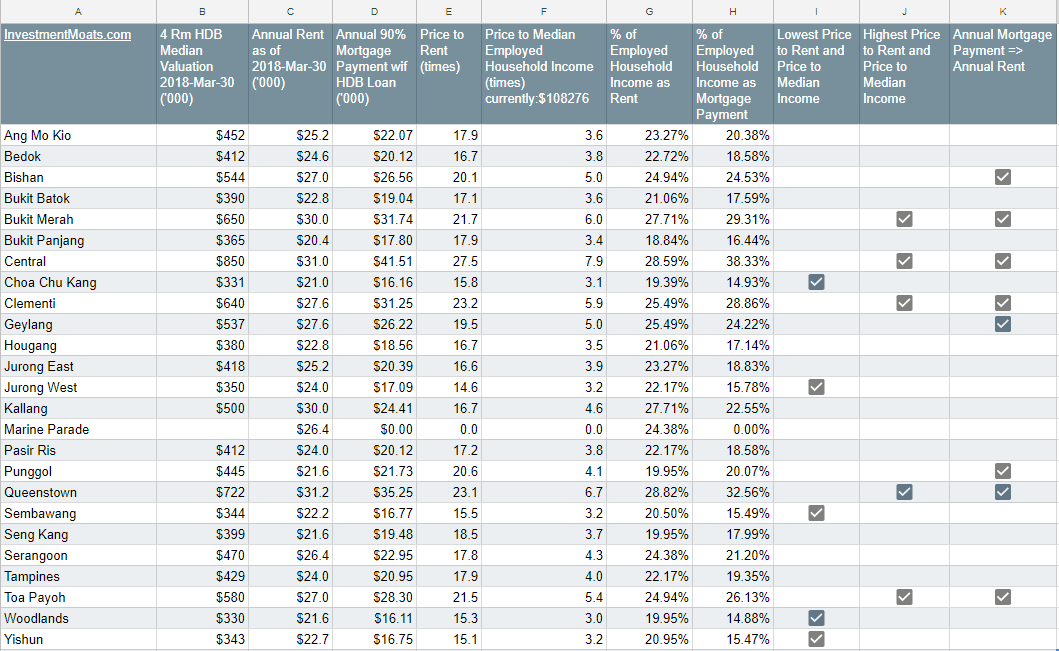

The table above shows some of the latest 4 room HDB prices by different areas of Singapore, as well as the latest annual rent by different areas, against the latest annual median income in Singapore.

So let us slowly go through them.

Top 5 Most Expensive Areas

The first column lists the median valuation by area. The data is as recent as 1st quarter 2018.

The top 5 most expensive areas are:

- Central: $850,000

- Queenstown: $722,000

- Bukit Merah: $650,000

- Clementi: $640,000

- Toa Payoh: $580,000

One commonality is that they tend to be close to town. If you have good income, and being close to where you work is important, there is a reason why you would pay these prices to live in areas like this.

Top 5 Least Expensive Areas

The top 5 least expensive areas are:

- Woodlands: $330,000

- Choa Chu Kang: $331,000

- Yishun: $343,000

- Sembawang: $344,000

- Jurong West: $350,000

I thought my dear Seng Kang will be on the list but it seems the list is dominated by the northern areas.

You can probably buy 2 HDB at the least expensive areas with the amount that you paid for a top 5 4 room HDB in most expensive areas.

You can observe the Geographical Arbitrage Opportunity

Suppose you lived in a top 5 most expensive area, when you are near retirement, or financial independence, you could choose to sell your flat.

Since you do not have to go to town so much, living in the outskirts of Singapore might become possible.

You could sell a $650,000 Bukit Merah HDB and get a $343,000 Yishun HDB, thus freeing up $300,000 in cash flow.

This could augment your retirement.

However, do note that this is a simplistic way of looking at things, since closing costs and renovation cost for the new place is not factored in.

Top 5 Most Expensive Areas based on Price to Rent Areas

Column C shows the Gross Annual Rent paid, as recorded by HDB. It varies in various parts of Singapore.

When we divide the Median Valuation with the Gross Annual Rent, we get the Price to Rent (column E)

How many times is too expensive, how many times is it too cheap?

This is rather subjective, but one figure being thrown around is about 16 times.

The top 5 most expensive areas based on Price to Rent:

- Bukit Merah: 21.7 times

- Central: 27.5 times

- Clementi: 23.2 times

- Queenstown: 23.1 times

- Toa Payoh: 21.5 times

You get the feeling the rents are not going up versus the prices

If you invert these figures you will get the median gross rental yield. So for Queenstown it will be 1/23.1 = 4.3%

Top 5 Least Expensive Areas based on Price to Rent Areas

The top 5 least expensive areas based on Price to Rent:

- Choa Chu Kang: 15.8 times

- Jurong west: 14.6 times

- Sembawang: 15.5 times

- Woodlands: 15.3 times

- Yishun: 15.1 times

There seem to be value if we are talking about purely rental yields. Jurong West would yield 6.8%.

However, do note that perhaps, those areas that are more expensive, have built in greater price appreciation, versus these least expensive areas, where growth could be tepid.

Top 5 Most Expensive Areas based on Price to Household Income

The other way to see if residential home prices is cheap or expensive, is to compare the price of the home to the annual household income.

The annual income we used to compare is the Median Nominal Employed Household Income (incl Employer CPF Contrib).

Currently, using 2017 data, its $108,276.

This figure includes your employer CPF contribution. It includes one month of AWS or 13th month bonus as well. It also means that at least one person in the household is working.

So if a household doesn’t have anyone working, it will not show up here.

What would consider cheap or expensive, if we are comparing price to household income (refer to column F)?

Usually I will use 5 times price to household income. Below that is affordable. Above that is not affordable.

However, since what we used includes the employer’s contribution, perhaps lets be a bit strict here. The median income, excluding the employer’s CPF should be $108,276 / 1.17 = $92,543.

5 times $92k is $462,717.

$462,717 divide by $108,276 = 4.2 times

Instead of 5 times, the conservative estimate is to use 4.2 times.

The top 5 most expensive areas based on Price to Household Income:

- Bukit Merah: 6.0 times

- Central: 7.9 times

- Clementi: 5.9 times

- Queenstown: 6.7 times

- Toa Payoh: 5.4 times

Its the same areas, and they exceed 4.2 times by a lot.

The flaw of using the median household income is that, if you use a different percentile of income, the price to household income will likely be less than 4.2 times.

For example, the median HDB flat in Clementi is $640,000. Can we find an average couple earning $640,000/4.2 = $152,380/yr (not inclusive of employer CPF contribution)?

I think we can.

This means that these area would likely serve the folks that have higher income, who placed a higher priority in choosing the areas that they live.

Also note, you can use price to household income to measure roughly, how long you could own the flat free and clear.

Top 5 Least Expensive Areas based on Price to Household Income

The top 5 least expensive areas based on Price to Household Income:

- Choa Chu Kang: 3.1 times

- Jurong west: 3.2 times

- Sembawang: 3.2 times

- Woodlands: 3.0 times

- Yishun: 3.2 times

They are pretty close to one another and they are below the 4.2 times pivot point.

These areas would most likely cater to the lower income.

For those with higher income, you can look upon these areas where you can genuinely speed up and pay off the mortgage and own these properties within 3 years.

Affordability based on Percentage of Annual Rents or Mortgage Payments

A sensible personal finance indicator is that you should not pay more than 30-35% of your income on your home.

Column G shows the percentage of employed household income that goes into rent.

Column H shows the percentage of employed household income that goes into mortgage payment.

For mortgage payment, we take it that the person took a 10% downpayment and borrow 90%. If you borrow less, your payment may be less. We take it the household repays over 25 years on a 2.6% interest HDB loan.

You can choose to rent, or you can choose to purchase a home and “pay the rent” to HDB or the bank.

Surprisingly, for almost all areas, we are able to pay mortgage or rent that is less than 30% of the household income.

There are 2 areas where the mortgage payment exceeds that of the median household income.

These two areas are Central and Queenstown.

It means again, these places are catered for folks that have a higher income.

This part of the analysis shows that you can have a dwelling to live and still have 70% of your income for other purpose.

Areas where Mortgage Payments is Greater than Rent

The case for rent versus buy is always subject to debate.

My view is that for the Singapore context, it is less of an issue.

The main reason is that most young couples are able to secure a BTO flat. If they are not able to, their first resale flat are subsidized.

All this means that their annual mortgage repayment is less than the rent.

However, if we remove the grants and subsidies, and we compare column C (rent) versus D (mortgage payment), the difference can be small.

In column K, I highlight those areas where the mortgage is more expensive than the rent.

These areas are:

- Bishan

- Bukit Merah

- Central

- Clementi

- Geylang

- Punggol

- Queenstown

- Toa Payoh

The conclusion here is that, at this point, it might make more sense to rent from a landlord then rent from a bank.

However, the comparison is not so straight forward. Your rent from the bank is probably fixed for 25 years, whereas your rent could go up drastically in the future.

This would invalidate the argument.

Rental Growth of Different Areas in Singapore

One of the reasons I went down this rabbit hole was because I was looking through where it might fit my co-worker’s relative price point better.

So why not take a look at the growth in rental rates in different areas.

The follow 2 table shows the change in median rental rates for 4 room flats in different areas from 2007-2018.

Its a wall of figures.

From one glance it seems the rents are around $2000++/mth

We study 4 areas to take a look at the trend (if not it will be rather noisy)

Serangoon’s 4 room HDB flat is not the cheapest. The current median transaction price is $470,000.

You can see that from 2007 to 2013, the rental grew gang busters. The compounded average growth rate was 7.7%/yr.

The peak coincide with the peak in the 2013 property market. Since then, rent have gone down steadily. The rent is lower than that of 2012’s rent.

The 11 year compounded average growth rate is 2.7%/yr.

Seng Kang is an area with a younger set of flats.

You realize the trend is similar to Serangoon. One interesting thing is the rent dipped during 2009 but recovered higher in 2010 to a higher level. This is not constrained to Seng Kang but also other areas.

From 2007 to 2013, the 6 year compounded average growth is 6.9%. The 11 year compounded average growth is 1%/yr.

One of the most expensive area and in demand is Queenstown. Its got not much things, but it is so accessible to the good schools in Clementi, and working areas in town.

This makes the units much in demand.

The median actually peaked one year after all the other 4 room HDB peak! The fall in rents is also must more controlled.

The rent right now is in between the 2012 and 2013 rent.

From 2007 to 2014, the 7 year compounded average growth is 9.1%. The 11 year compounded average growth is 4.3%/yr.

The results look better, but I wonder is it because the rent in end 2007 is lower. The rent is no different then that of Seng Kang and Serangoon. I find that hard to believe.

Finally, we have Bukit Panjang an area where the rental of the 4 room flat is relatively inexpensive.

From 2007 to 2013, the 6 year compounded average growth is 5.7%. The 11 year compounded average growth is 1.1%/yr.

As a summary, those areas that are more expensive do seem to justify their price with higher rental growth rates. Those that is cheaper do have a lower growth rate.

There are some other observations:

In 2009 it was the great financial crisis. Rent fell across the board.

However the following areas was able to raise their rent:

- Marine Parade

- Queenstown

- Serangoon

The following area was able to maintain their rent:

- Clementi

- Jurong East

- Pasir Ris

- Tampines

- Woodlands

Post 2009, all areas recovered their rent. Rental in 2010 was higher than 2009 in all areas.

2011 was a crazy year. Almost all areas increased their rentals by at least $200/mth

In 2013, the property market peaked. However, the following areas was able to see price increases:

- Ang Mo Kio

- Bedok

- Bishan

- Bukit Batok

- Central

- Geylang

- Hougang

- Jurong East

- Kallang

- Queenstown

- Tampines

- Toa Payoh

- Woodlands

In 2015, the stock market in Singapore fell 18%. In that year, probably together with the property market peaking in 2013, the rent in all area fell. All except Geylang.

Tightening of Labor does little effect on the rent. After 2011 election, the criteria for permanent residency and foreign labor was tightened hard.

In the fall of demand, given the fix supply, the rent should moderate.

Yet in most areas, rent seem to be going up. It seems the rent follows the cycle of the property prices more than the demand and supply. Unless you are telling me rent goes up, so does vacancy.

Summary

I hope that you get to know more about the affordability of the 4 room HDB flat.

Given the difference between lowest rent of $21k and $31k, I can see folks paying 50% more to live in an area where they suffer from less commuting stress.

The expensive HDB flat do seem to enjoy better rental growth, and retain the rental rates better. After all, there is a utility since they are located to some prominent working districts.

If we look at it from the total return perspective, the total return of Queenstown is 4.3% + 4.3% = 8.6%. We assume the price of the flats also go up in tandem (could be wrong).

The total return of Bukit Panjang is 5.6% + 1.1% = 6.7%.

While more expensive, if you treat the HDB as an investment after you meet your minimum occupant period (MOP), the Queenstown property might be more worth it.

Of course the property is more than an investment.

For many of us, it is a place where we live. To be close to family.

Thus, we cannot just think from the monetary side of things.

If you like something similar, some years ago, I visualize the different growth of Landed properties, non-landed properties and HDB. This might interest you.

If you like materials such as these and would like to enhance your Wealth Management towards have a Wealth Machine that gives You Financial Security and Independence, Subscribe to my List Today Here >>

If you like this do check out the FREE Stock Portfolio Tracker and FREE Dividend Stock Tracker today

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

K

Saturday 12th of May 2018

Just thinking out loud, the subsidies given really makes hdb very affordable. The up to 80k grants is close to the 1 year median household income (ie reduces your ratios by 1 turn) Furthermore a lot of Singaporean finance their houses with cpf ,which many don't really consider as "income" . They will send to the very most. I think it's quite common to find couples with 4 years of working experience to have at least 80k combined in their cpf account (1k per month x 2 people x 13 month x 4 yesds). Combined with cash on hand and relatively low interest rates ,this allow them to bid aggressively for resale flats. Assume 90% LTV using cpf loan that is 800k flat. Only issue if they can meet the MDSR and TDSR.

I think rental also doesn't take into account of the potential vacancy rates, quality of tenants , like it's probably way easier to lease a house in the central as compared to further away.

Kyith

Sunday 13th of May 2018

Rental doesnt take into account vacancy rates and all. the vacancy rates could be much higher. however, we are leaning closer to the home living affordability angle rather than the landlord angle.

what you have said before actually means higher household income that makes alot of 4 room flat more affordable.

Sinkie

Sunday 6th of May 2018

Regarding replacement costs of HDB flats ... 10+ years ago you could see the actual development costs of new HDB flats as the closing tenders for HDB projects were fully accessible by public on GeBiz website. Costings, blueprints of HDB blocks, floor plans of units, number of units by type, type of building materials, quality & standard of building materials & finishings, etc etc.

At that time, most new HDB projects were roughly 60% 4-rm and 40% 5-rm. From a few of the projects in Punggol in the mid-2000s, I calculated that the average development cost for a new HDB flat was around $110K.

Note that the development cost included the total infrastructure and supporting M&E, which is more realistic, i.e. lifts, electrical, power sub-station, drains, sewers, carpark, internal roads, landscaping, playground, pathways, etc. Even though these infrastructure are public property LOL!

New 5-rm flats then were sold at around $300K ... i.e. the actual development / construction costs made up about 37% of the selling price. The "cost" of land will make up most of the remaining 63%.

If the percentages are maintained till today, then about 40% of the BTO price will be the construction costs.

However the presence of all sorts of grants now means that HDB will have tweaked & included some additional margins into the base BTO prices. Previously new HDB flats didn't have any special grants. The only grant was the Parent Proximity grant which was only available for resale HDB.

Fred

Saturday 8th of February 2020

Hi Sinkie, I remembered I did a similar calculations for the precinct of Punggol Spring, a HDB development in Punggol. It is easier as it comprises all 490 units of 4-room flats. China Construction Company successfully tendered the project for the 4 blocks and a multi storey carpark precinct with the roads, landscape etc. Using the tendered price and divided by all the 4-room BTO flats, I remembered the price came close to $200k each( tender price divided by 490 units) The selling price ranges from $180 -250k each then. Of course here, I did not factor in design, management and land cost etc. I applied a BTO in this project in 2008 and assuming after garnering more than 70% of applicants, HDB proceeded with the constructions. My point is, since your numbers is $110k for each flat in mid 2000, and my precincts of all 4-room flats is in 2008, we need more data to average the development cost of each unit. Already, in the same Punggol, price of each development cost can vary so widely, what more different areas and different contractors.

Calvin

Sunday 6th of May 2018

Very good info for start. However limitation is assumed same household income, which is not realistic in real world. While this data is difficult to get, can assume that areas have different income groups. A basis could be through rental - why by standard benchmarks is around 20~30% of monthly income. Also the housing prices is based in resale prices which would not be "normal", usually upgraders without income ceilings. New young couple would/should buy direct from HDB at 30~50% subsidies. So these aspects, especially income, should be taken into account when studying housing affordability in Singapore.

Kyith

Sunday 6th of May 2018

Hi Calvin, thanks for the pointers. I think I explain that I can only use median income because it is the easiest. By no means does it mean that those expensive places are not affordable. The cheapest and even those that are not expensive are affordable. It just means that these areas, you have to work hard to reap that better quality of life.

Resale prices are good because it removes the intricacies of grants and subsidizes. If we include that, those that struggled would be able to afford even better. If they do not qualify for grants and subsidies, without those grants and subsidies, they can afford them pretty well as well.