There was a point in time when I think that you could not fail with a $10,000/mth income.

If you have never earn that amount, aspire to reach there, you could have thought of how much things you could buy with that.

I have never reached this monthly salary but I do have the months when I get that kind of cash flow when the bonus came in. But if you live a minimalist life, you think this kind of salary is excessive. And someone with this can have a high savings rate that could speed up your journey towards your financial independence.

There is a few levels of class in Singapore and for those who reached middle management in their late thirties and forties, this might be common. It might even be more common for the STEM graduates who worked for a few years.

The myopic part for me is that I failed to understand as you form a family, it’s not just managing 2 person.

It’s managing your clan, the two extended clan, and two or more social circles. The number of people that influence your lives also increases and these complications would make a $10,000 or $20,000 a month salary look inadequate.

In the past, I would have said it’s absurd that this kind of salary is not adequate.

My friend Chris tells me that when you earn 5 figure, struggling to make ends can be more common then you think. If you be less judgmental and sincerely wants to help them, you will learn about this more. My financial planner friend Andrea Kennedy tells me the same thing.

I chanced upon this article by Her World where a lady wrote in to share about her family’s financial situation.

I’m still debating whether this is real or not. However, talking to some friends who mingle with people at that level tell me it’s pretty possible.

So here are the summary:

Tanya and Dave earned a combined monthly income of $30,000. They have been married for 3 years. They worked in the sales line. They do not work in the same company. Naturally, their earnings is commission based.

The nature of their job is that they have to spend money to keep a certain image. This is part of the sales package. For example, Tanya spent $1000 on a dinner for 2 clients and their child. In one month, this could be a few times. It is part and parcel for them to give thoughtful gifts. This means extravagant gifts such as rare whiskey, custom art pieces, crystal desk accessories, designer home ware.

While some of their clients appreciate this as a good to have gesture, there are some, especially the rich ones who expects it. While they can claim work related expenses from their company, there is a cap to it.

To keep up with appearances, they bought an expensive condo. This doubles up as a place to entertain their clients. These gatherings is another additional expense. They also bought 2 luxury cars. Each of them have $20,000 in credit card debt.

They work upwards of 60 hours per week. If we convert this, its like working 8 hours for 7 days a week.

They confessed that they cannot afford to have children right now due to their debt situation. They do not go for movies, or exotic holidays. They could not treat their families as well.

Tanya confessed that they secretly got used to this kind of lifestyle. In her own words, their situation is “dire”. She felt that the more she uses the credit card the more repulsive she felt about it.

What they planned to do is:

- Pay off as many debt as possible

- Commit to saving money

- Hopefully stick to a budget and don’t have to live paycheck to paycheck

Looks tough.

But if you are looking from the outside, you would think that this is the life. Personally, I think I am so slack now that I can never work 60 hours a week again. So that is some mad work ethic.

So here are some of my thoughts.

The Life Energy versus Money Exchange may show a Different Per Hour Wage

Vicki Robins and Joe Dominguez wrote the very popular book Your Money Or Your Life. This book inspire a whole generation of people to question their current job, how they had lived their life, how they used their money.

One of the best concepts they introduced is the Life Energy Exchange.

The Life Energy exchange shows that there is a relationship between your life energy and money.

You use your life energy (in unit time) to earn money.

You can in turn use money to get more life energy.

However, money has no intrinsic reality. Life energy has. Life energy is limited and irretrievable. Our choices show how we use it and express meaning and purpose of our time here on earth.

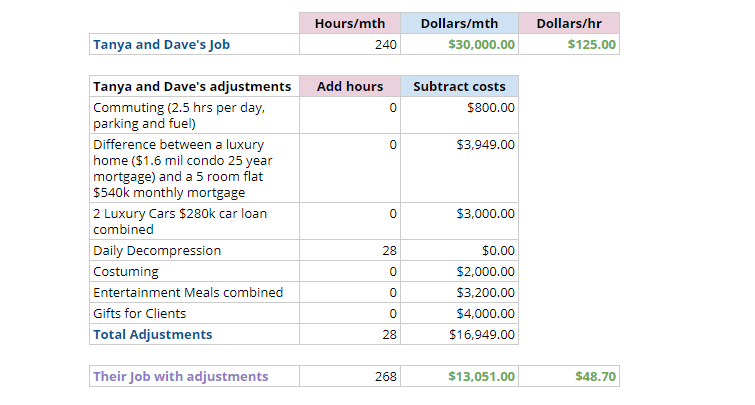

Tanya and Dave spent up to 60 hours per week to earn an average of $30,000/mth.

This gives them $125/hr combined or $62.5/hr each.

Not too shabby. A person earning $3000/mth working for 40 hours/wk earns $18.75/hr. If the person earns $5000/mth and worked 40 hours/wk, she earns $31.25/hr.

However, Tanya and Dave did not spend just this amount of time in their work. Also they will have spent some money that is very related to their work.

You should have noticed the need to keep up with appearances and entertainment.

In general, you would have spent time related to work. If you had not work, you won’t spend that amount of time.

You should add this number of hours worked to the total weekly or monthly number of hours worked.

In general, you would have spend money related to work. If you had not work, you would not spend that amount of money.

You should subtract that amount of money spent from your salary.

Typically, areas related to work can be:

- Commuting

- Costuming. If you did not work, you would not need certain power suits, and an assortment of wardrobe that do not look stale

- Meals

- Daily decompression. This is the time spent talking about work, or thinking about work, even after you are off work

- Escape entertainment. If your life is not so exciting, you need to have entertainment to “escape” that work context. If your work life is exciting and you identify that you are comfortable with that, you would have less of this

- Vacations

- Job-related illnesses

- Other job related expenses

So the following figures show a tabulation of Tanya and Dave’s life energy exchange.

I estimate the difference between a 4 BR $2 mil condo and a $600k HDB had they not taken this route. Also estimate the payments for 2 luxury vehicles and a few expenses mentioned.

It would seem that they still have a lot of buffer. Either my estimation is underwhelming or that they have a lot of costs not said.

If we add the total 28 hours from these adjustment and subtract the $16,949 in costs related to working this job, the per hour rate dropped to $48.70/hr.

In this case, each person’s per hour earnings is less than someone who earned $5,000/mth.

Of course this is not a fair comparison because the person earning $5,000/mth would also have costs that bring down her per hour rate.

What this show you is that, there are more costs associated with your work than you realize. It makes you wonder if its worth it.

Tanya and Dave’s Situation is not as Dire

We usually look at our problem, and down play it’s extent or overestimate it. When she says their problem is dire, I think in the grand scheme of things, it’s not too bad.

Dire is if you struggle to find a job and you have a lot of debts to service. That will happen if the sales business becomes challenging.

Dire is when the whole family struggles to pull themselves out of poverty.

They do have their job. Their relationship with their clients, from what we observe is top notch. They just have an optimization problem.

They have said they would look at how they entertain their clients, and the gifts given. This shows that there are levers to pull. Biting the bullet, taking some losses, and deleveraging by selling and switch assets are ways of optimization that could still improve their situation.

From what is reported, there is some overestimation here.

Having a Realistic Assessment of their Predicament Would Alleviate a lot of Stress

I do think what couples like this need is some motivation to fixed whatever issues they have.

But most of all a good “fixer” would be immensely helpful.

The fixer would give an accurate assessment of their situation, much better than by the couple themselves. The fixer could also give a few approaches how they could untangle themselves from this deep debt situation.

The assessment might let them know that if they take these appropriate steps, the situation and impact to daily life is not too bad.

And this allows them to have a higher morale and very beneficial to living well for their daily lives.

As they are less sophisticated, they might not evaluate these sound strategies if they do not have this fixer.

Who would these fixer be? It would be good if they have a resident close friend that is well verse in this.

Most of the time, it is a competent financial planner.

Unfortunately, the financial planner cannot earn much if they client do not have a cash flow to purchase any product. If he is successful in fixing the situation, he could be able to sell the couple products.

Thus he has to front load the effort spent.

Sometimes what we need the planner to do is really to navigate these financial problems that is not related to insurance or retirement.

Summary

Two things that made me skeptical whether this is a real story. The first one was how little challenges the couple faced when their income is variable.

If they are sales and commission based, most often income is variable unless it is a field that is pretty out of the norm. The second thing is that, I think that if you been interacting with richer folks, a deeper relationship with them would trigger a shift in how you view money and the folly of your ways.

Whether it is real or not, there are folks that earns like Tanya and Dave but would make risky life decisions. There are also a lot of folks that earn less than them making the same risky life decisions.

In a lot of financial situations, they can be solved if:

- you are healthy

- you have jobs

- you have a mentor or fixer to help

- you are motivated

If you do not have these 4, the situation is more dire.

Lastly, the life energy exchange is a way to make you see that sometimes you work less hours but you are mentally more sane, you have more time and still beat folks who draw a higher salary than you because you know what you what you want.

Now is your turn to tell Kyith is this is bullshit or not. Do you see examples of this in your daily lives? Share it with me!!

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

EL

Monday 25th of February 2019

Hi Kyith,

I am an avid reader of your blog ! Love the way you dissect issues.

Anyway just sharing some other possible scenarios (based on true stories) I may not have the exact figures but you can imagine that even if one earns more than $10k per month it would still be insufficient

1. A divorcee with 2 grown children a. Must take care of former wife as she is uneducated and has never worked in her entire life; son who is in his late 20s still unable to get a paid job due to some social impairment. Rental of home for them plus living expenses ($3000- 4000) Also must make provisions for their medical care etc.

b. younger daughter just started overseas university (tuition fees plus boarding costs ) even buying mobile phone and special requests for luxury items once in a while. And have to support her until she completes her doctorate as that is her passion. He can't bear to say no to education needs of his daughter.

c. Rental of his own apartment - $3-4k d. Living expenses for himself (car, helper etc)

Lucky he doesn't have to take care of his elderly mother who is well provided for.

Life circumstances are so different for some and these are sometimes thrust upon them.

What I have witnessed is apparently quite common among the older folks in their 50s and 60s. It seemed like they are still supporting their grown children in their endeavors (further education, overseas study if they cannot cope with the local education system, helping them buy their first home etc).

I know, the kids nowadays are really quite blessed !

cheers EL

anonymous

Sunday 24th of February 2019

Good one Keith. Single income ~ 300,000. Living in HDB, no car, no overseas holidays (except MY , ID but covered by miles/hotel points) but low savings. Reason - Special kid and therapies costing > 150/hr. 300K - 20,400 CPF deduction, 15000 SRS, 10000 spouse CPF; ~25-30K Taxes; 10,000 School fees + Bus for kids; 45,000 therapies; Housing + Groceries - 20,000; Helper & Misc - 12000; Insurance (term & Med ) - 15,000; Medical - 5,000 (OP/Specialist for kid), Other Family essentials (clothes, cleaning, shoes) - 5,000; Potential savings of 100K I look at them very highly as their priorities are clear. Individual circumstances can be different but when I see people intentionally 'wasting' money I have no feelings for them.

Kyith

Monday 25th of February 2019

Hi anonymous, thanks for your kind and clear sharing. at the same time i was struggling to work out some long term care figures and this break down have been helpful. i can see that almost 60 to 70k is being spent as a result of special kid. was wondering if you can reveal if its autism. Thanks a lot.

I guess even in your situation, you could balance life and savings pretty well.

Lim

Sunday 24th of February 2019

The classic book Millionaire Next Door in 1996 (more recent 2nd edition also available) has already talked about this problem and how there are under accumulators of wealth (UAW) and those that are Prodigious Accumulators of Wealth (PAW).

To quote the wikipedia summary: "Their findings, that millionaires are disproportionately clustered in middle-class and blue collar neighborhoods and not in more affluent or white-collar communities, came as a surprise to the authors who anticipated the contrary. Stanley and Danko's book explains why, noting that high-income white-collar professions are more likely to devote their income to luxury goods or status items, thus neglecting savings and investments."

Unknown Stranger

Sunday 24th of February 2019

I'm not surprised by the story. I personally know of a guy earning 52k a month and he's in a lot of debt.

Kyith

Sunday 24th of February 2019

Hi Unknown Stranger, could you share with us roughly how that could happen? Thanks a lot