Yesterday, I posted the latest yield that you can get if you purchase the Singapore Savings Bonds.

And a few readers main comment is that the yield curve is inverting and we should be careful.

As you can see from the 1 year and 10 year SGS bond yield, the yields look to be narrowing.

And if the yield inverts, it is a really bad thing.

I think there is validity about respecting the yield curve, but as an indicator, it might not be the most reliable.

My understanding of the yield curve

The yield curve shows the prevailing interest yield for different duration of the countries government debts.

For debts a longer tenure debt has more risk, because they are subjected to interest rate fluctuations, credit events, inflation, economic factors. Thus, when risks are higher, the interest rate investors demand should be higher.

So in norm situations, the shorter tenure bonds (1 year) should have an interest yield that is lower than a longer tenure bond (2 year), so on and so forth.

This tenure vs return relationship usually are in balance, but there are situations where the relationship is disturbed.

Certain unique demand and supply of these government bonds, would cause them to go wack.

The shorter term rates usually take their cues from the central bank. The central bank controls the short term borrowing rates to the banks. Changes to these rates, usually cause a similar directional change to the short term rates.

And since the tenure vs return relationship is still valid, all the different maturity bond yields should go up.

The yield curve inverts for a few reasons. The main one is that, in a normal economic cycle, the central bank wishes to rein in inflation when the economy is good.

So they raise rates, make borrowing more costly, and slow down expansion.

The corporate bonds are usually priced at a spread above the government bond rates.

While the short term rates will go up, the demand and supply for the long term rates may be affected by other factors.

When the market got to a stage where there are not much to invest in, nothing attractive to purchase, 10 year government bonds becomes attractive and thus the demand for it goes up.

When there are greater demand, the prevailing interest yield need not be high to attract the investors (they would like to deploy to safety more than a super attractive rate of return).

This prevents the yield from going up.

Overtime, the yield curve inverts.

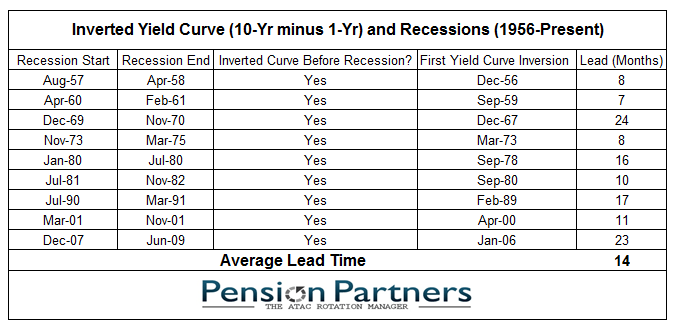

Does the Inverted Yield Curve Precedes a Stock Market Bear?

Every Recession was Lead by an Inverted Yield Curve.

The data point that caught many of our attention is that in the past 60 years, every US recession was preceded by an inverted yield curve.

And that is enough to sound the alarm.

Recession, is a part of the cycle, that happens in main street, or every day life.

What you wish to find out is whether an indicator like the inverted yield curve lets you know a bear market earlier.

And that might not be the case.

There is another thing that precedes a recession normally, and that is the stock market.

So the question is whether the inverted yield curve precedes a bear market?

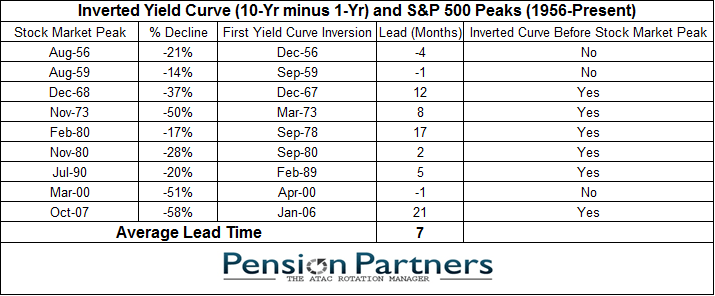

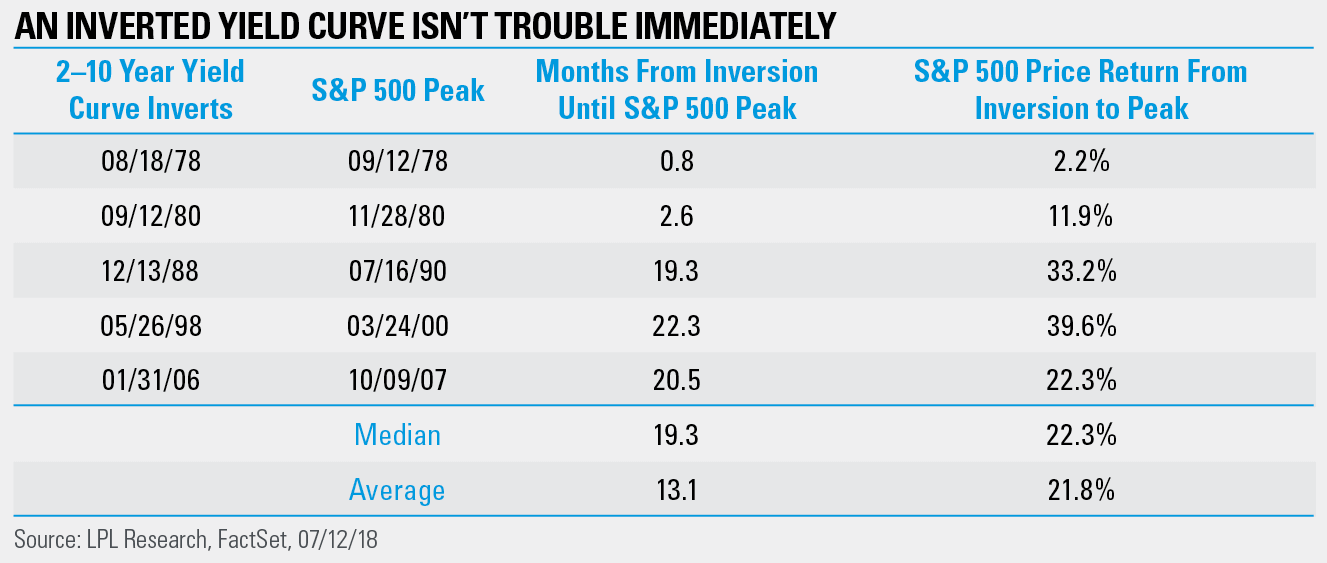

image credit: Pension Partners

The folks at Pension Partners tabulate the following in 2014, trying to see if there is a relationship between an inverted yield curve predicting a bear market.

And it turns out that there are some months where the market peaked before the yield curve inverts.

And then there are some where the yield curve inverts and nearly 2 years later the market peaks.

That is probably the one that I experienced, which is in 2006.

We will talked about it later.

In some other research, they brought about less sample, and you realize they brought up some inversion that Pension Partners did not bring up. The difference could be what was used, whether it is 10 year minus 1 year or 10 year minus 2 year.

As you can see, there are more instances where the peak happen 2 years after inversion.

One other thing you would realize is that, the sample size is very small.

When the sample size is small the result have a tendency to swing to both extremes.

And if you are interested, not every draw down happens because there is a recession. There were some draw downs that are rather nasty, and there weren’t any recessions.

What is the Value of an Inverted Yield Curve…. When we are already drawing down?

I think I think of it like this:

- the indicator should tell me when a bear starts

- if not it should tell me the magnitude of the draw down from the peak

The chart above shows the 2 year price action of the S&P 500. (as a side note, both Hong Kong, China and Singapore are in a draw down as well)

If we say that the curve is about to invert now, and the market is already in a draw down mode, then what do you want the inverted yield curve to tell you at this point?

The magnitude?

If this eventually ends up as a 30% draw down, in quantitative terms, it will be marked more into the group where the market peak but that happens before the yield curve inverts.

My Experience Going Through a Inverted Yield Curve and Bear

As I said, I went through only one episode of inverted yield curve in my life.

And back then the situation is like this as well.

Just that it scared me more than this.

And we have to wait for 2 years later before you see the actual danger.

I think if you look at the above S&P 500 chart, I would be concerned based on the about the cross of the 50 day moving average, cutting the 200 day moving average from above.

It is more sinister due to that the 200 moving average is flat. The moving average cross over tend to be rather lagging and you could use it as a means of controlling the level of your portfolio allocation.

However, there tends to be whipsaw sometimes, and you end up going in and going out. So you got to be comfortable with that.

I think if we are on the topic of indicators, some of the experts who tells a rather coherent narrative in the market peaks in the past and market bottoms such as David Rosenberg do indicate economic indicators are not well ( in a bad way)

There are some of these stuff that seams to make sense, but actually not so useful. I have this article where I consolidate a lot of them.

You can read them here | Mental Blocks, Doomsday Scenarios, Misinterpretations that Kill Your Wealth >>

Lastly, a draw down can be short like a few days, a few months, or 1 to 2 years.

Unless its a 2008 situation, I think a lot of market dynamics shows that you can pick up some stocks at attractive prices.

Don’t be those folks that every time only wait to invest during a bear market, if not they don’t know how to invest.

After that 2 years of draw down, how are you going to deploy your capital you accumulate for the next 20 years?

Keep waiting for a bear?

Do Like Me on Facebook. Join my Email List. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

Sinkie

Wednesday 5th of December 2018

The 1s10s or the 2s10s yield inversion is just a broad & blunt early warning indicator. It's main purpose is for you to avoid being heavily in stocks during recessions becoz that's when the drawdown becomes the deepest (-40% to -50+%). If you're looking to avoid any drawdown at all or even to avoid -15% drawdown without danger of over-trading & whipsaws, then that's not its purpose.

Yield curve inversion just tells you to respect any deep downturns down the road. For e.g. if the 2s10s has already inverted, and many months down the road the stock market encounters strong turbulence and goes down -20% or -25%, you may then re-allocate your assets. Such as moving 50% of risk assets to cash or govt bonds .... or for very risk adverse 100% into cash. And just wait for the coming recession.

And being prepared to scale back in when stocks have dropped over -35% (Coz you never know how deep the bear will be).

The death cross by itself generates a lot of false positive i.e. many instances whereby although stocks drop 15%-20%, but didn't go much beyond -20% before recovering.

One can combine death cross with yield curve inversion i.e. pay attention to death cross only when yield inversion has occurred.

The Conference Board leading economic indicator curve may be a more timely indicator of US recessions e.g. when the curve has dropped -5% from the previous peak.

And as always, I think for those who have balanced portfolio ---- just continue as normal whether recession or boom. Which is why a balanced method i.e. always having a fixed 30% to 50% in cash/safe bonds is usually the best method for most people to invest.

Kyith

Wednesday 5th of December 2018

if it warns me clearly of a 40% draw down then its useful, if not a lot of whipsaws.